Positions Only: Long Fixed Income

We apologize for the delay in publishing the Prometheus ETF Portfolio this week. The team is on a short break, and coordinating multiple time zones has proved challenging. We will resume our regular publishing schedule in April and endeavor to be timely until then.

Welcome to our official publication of the Prometheus ETF Portfolio. The Prometheus ETF portfolio systematically combines our knowledge of macro & markets to create an active portfolio that aims to offer high risk-adjusted returns, durable performance, & low drawdowns. Given its systematic nature, we have tested the Prometheus ETF Portfolio through decades of history and have shown its durability. For those of you who are unacquainted with our systematic process, we offer a detailed explanation here:

In this publication, we will discuss the performance, positioning, & risks of the Prometheus ETF Portfolio and it will be published every week on Fridays to help investors understand how our systematic process is navigating through markets. Before diving into our ETF Portfolio positions, we think it is important for subscribers to understand the context within which our systems choose their exposures. Below, we offer our latest Month In Macro note, which contains the conceptual underpinnings of our systematic process within the context of the latest economic data:

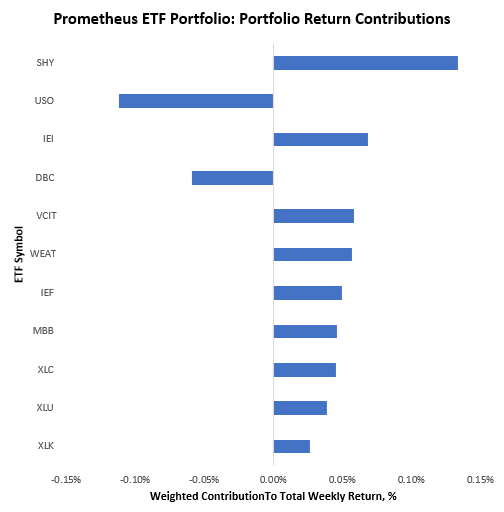

Last week proved positive as our bets on tightening liquidity and weakening growth found support in markets. Our portfolio was largely skewed toward fixed-income securities, and thus our bets were broadly onside:

We ended the week up approximately 0.40% as markets moved to price an eventual loosening of monetary policy. From our standpoint, markets have been quick to price the easing/tightening of policy but behind on pricing the impacts of said policy changes which will continue to create opportunities for us to exploit. Turning to next week, our systems are looking to position as follows:

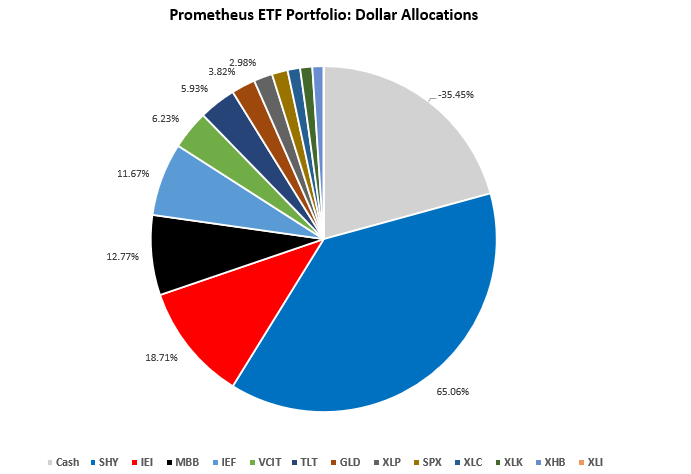

Positions: Cash: -35.45% (LEVERAGE) SHY : 65.06% IEI : 18.71% MBB : 12.77% IEF : 11.67% VCIT: 6.23% TLT : 5.93% GLD : 3.82% XLP : 2.98% SPX : 2.52% XLC : 2% XLK : 1.93% XHB : 1.8%

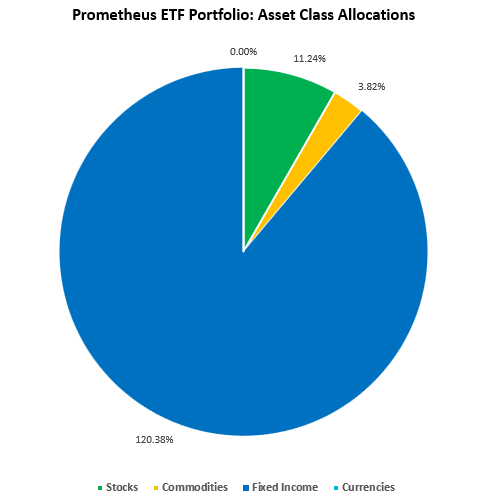

The portfolio is leveraged, which is annotated as a short cash position. Below, we show the non-cash asset class allocations:

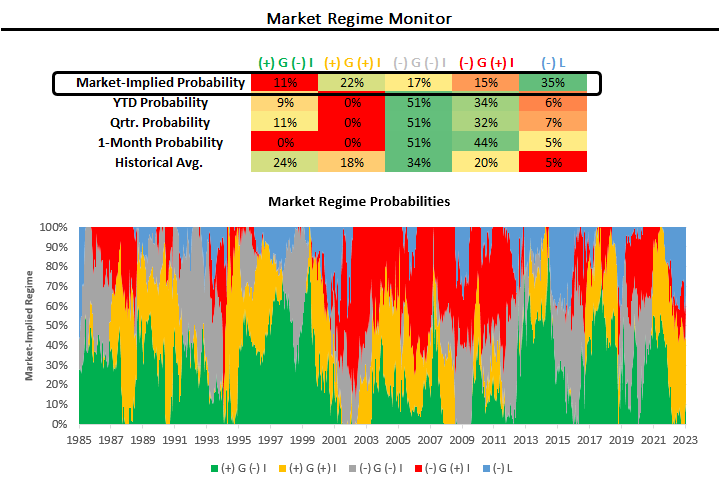

This portfolio allocation has an expected volatility of 8.3% and maximum expected volatility of 10%. The primary risk to this portfolio is a significant upside surprise to nominal growth & inflation expectations which would catalyze a reversal in policy expectations. The economic data calendar for next week is unlikely to bring these risks to fruition as PMI data, goods trade, and consumer spending are seeing considerable pressures in our tracking. There is a potential risk in the form of continually strong (low) initial claims data, which active investors can manage around. Overall, we think it is important to keep in mind that regardless of the first-order impacts of market discounting easing the impacts of tightening liquidity remain in markets. We show our market regime monitors, which continue to show this pricing:

Historically, periods of tightening liquidity have paved the way for disinflationary pressures- this time is unlikely to be very different. Recall that even during stagflationary decades, bonds can have periods of immense strength as the economy heads into recession and policy rates ease. We will offer more guidance in the near future. Until next week.

Hi there! Do you know if they make any plugins to help with SEO?

I’m trying to get my website to rank for some targeted keywords but

I’m not seeing very good success. If you know of any please

share. Kudos! I saw similar blog here: Eco wool

Hello! Do you know if they make any plugins to assist

with Search Engine Optimization? I’m trying to get my

blog to rank for some targeted keywords but I’m not seeing very good results.

If you know of any please share. Thank you! You can read similar art here: Your

destiny

I’m really inspired together with your writing skills as

well as with the layout for your blog. Is this a paid subject

matter or did you customize it yourself? Anyway keep up the

nice quality writing, it’s uncommon to see a great weblog like this

one nowadays. Snipfeed!

I am extremely inspired with your writing skills and also with the

layout in your blog. Is this a paid theme or did you customize it yourself?

Anyway stay up the excellent quality writing, it

is rare to see a nice weblog like this one nowadays.

LinkedIN Scraping!

I am really impressed together with your writing abilities as smartly as with the layout on your weblog. Is this a paid subject or did you modify it your self? Either way keep up the excellent high quality writing, it’s rare to see a nice blog like this one today. I like prometheus-research.com ! It is my: Madgicx

I’m really inspired together with your writing abilities

as neatly as with the layout in your weblog. Is that this a paid theme or did you customize

it yourself? Anyway keep up the nice high quality writing, it’s rare to look a great weblog

like this one today. LinkedIN Scraping!

low side effect steroids