Tightening Liquidity + Recession Signal = Short Equities?

In this note, we outline our thoughts on where we are in the economic cycle and where we think we’re headed next. Particularly, we outline how we’re thinking through real economic growth.

Before we dive into our assessment, we think it’s important to break our relative silence on the banking system and Silicon Valley Bank (SVB). We have refrained from delving into this subject because, as systematic macro investors, the specifics of SVB and similar entities are somewhat beyond our purview. We aren’t in the clickbait business and stay with our expertise. However, our approach has been prescient in informing us of the pressures in the liquidity ecosystem, with SVB simply an outcome of these pressures. The question before us today is whether these issues will morph into a situation resembling 2008 we think this unlikely.

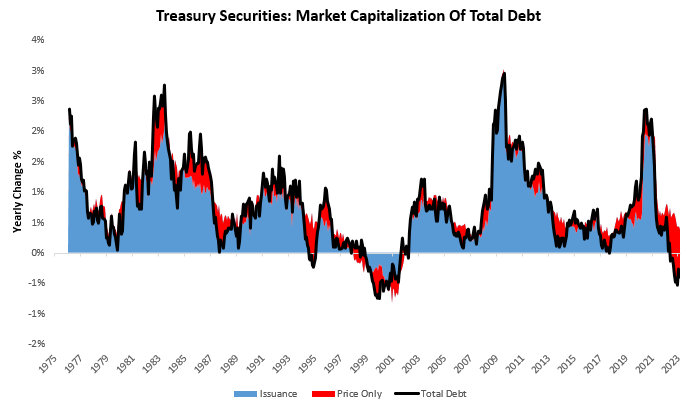

The SVB bankruptcy reflects the losses imposed on the private sector by the US Government balance sheet drawdown. We show this below:

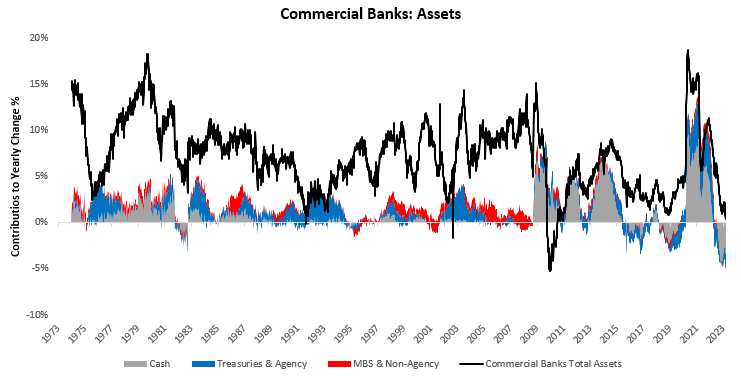

The last twelve months have imposed the largest drawdown in the total market capitalization of US Treasury debt. These debts are assets of the private sector, of which commercial banks occupy a sizeable share. Banks have suffered significant pressure are the combination of QT & rate hikes drained reserves and hurt duration:

We must note that while these losses do sit on commercial bank balance sheets, a significant portion of this exposure is hedged, i.e., a portion of the risk/losses is transferred to other financial intermediaries. However, it is essential to recognize that this loss must be recognized somewhere in the private sector risk cannot be destroyed, just transferred. Therefore, as the drawdown in government securities extended, the risk to private sector assets rose a risk concentrated in SVB. Consequently, financial stress is a sign of the times rather than a harbinger of things to come. Said differently, SVB and other banking stresses are symptoms of tightening liquidity, not the source itself.

Looking ahead, it is unlikely that this will transform into a meltdown like in 2008. This is because, unlike in 2008, the underlying assets causing a softening of balance sheet dynamics have little to no credit risk, i.e., the risk of default on Treasuries is non-existent. This dynamic differs significantly from 2008 in that banks’ assets were highly likely to default, rendering them worthless. Furthermore, this dynamic was exacerbated by short-term funding markets tied to these risky assets. Financial institutions that owned low-quality credit also issued a significant amount of commercial paper, considered highly liquid. However, as the risk of default on MBS became clearer, commercial paper markets froze, accelerating the contagion in the financial system.

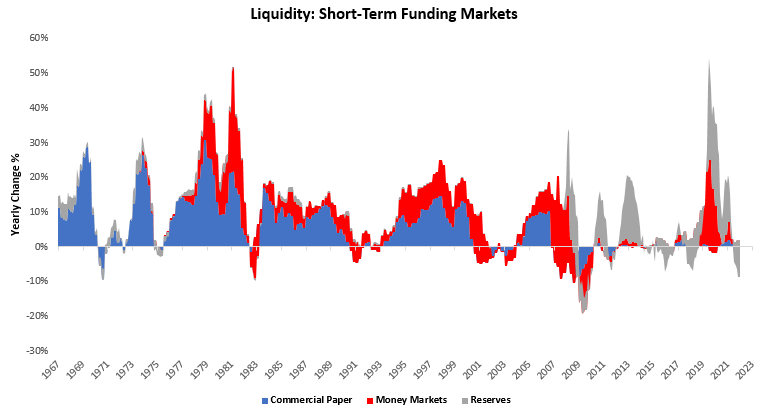

Today, we see a different situation on two accounts. First, the underlying securities causing balance sheet losses (Treasuries) have no risk of default. Second, the composition of short-term funding markets has changed dramatically. The recomposition has primarily come from liquidity pools (from banks, corporates & households) migrating from investments in commercial paper to investments in money markets & maintenance of high reserve balances. We show this below:

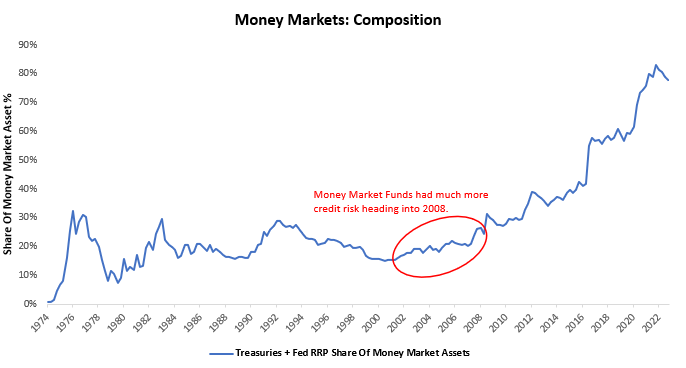

As we can see above, while commercial paper was the most popular investment destination for cash assets prior to the 2008 financial crisis, post-2008, money has flowed primarily to money market funds and reserve balances. This change is an extremely important one. While money market funds, much like commercial paper, are private sector liabilities, 78% of money market fund assets are now invested in Treasury & Federal Reserve securities. We show this below:

This structural change is extremely important to understand today as a true financial contagion like 2008 would require the meltdown of short-term funding markets. This meltdown would require a perception of the solvency risk of the institutions issuing these short-term securities. Today, these markets are almost entirely dominated by government securities, either directly or indirectly. Therefore, for true contagion risk to emerge, we would require serious concerns around the solvency of Treasury securities which we think is highly unlikely. This doesn’t mean that today’s banking stresses are a false signal or even transient but they are not apocalyptic. As said earlier, these financial stresses are symptoms of tightening liquidity. Specifically, these come from a reduction in policy liquidity and morphing into a drawdown in private sector liquidity. We expect these conditions to worsen as the Fed continues to wage its war against inflation and economic growth worsens.

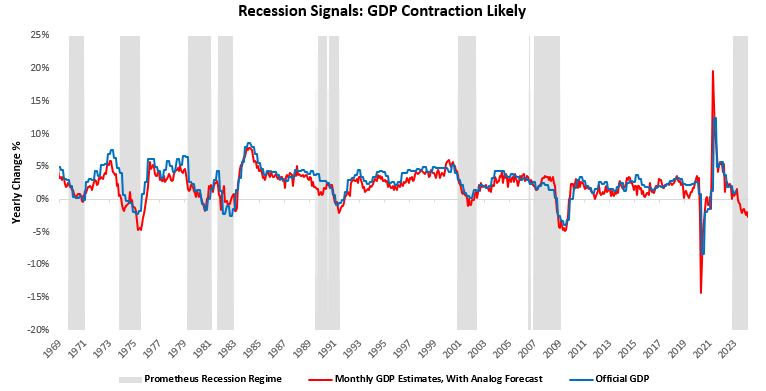

While many today have been focused on the here-and-now of the financial system, our systematic approach has kept us abreast of economic developments, where we see further evidence of recessionary conditions emerging. Below, we show our monthly estimates of real GDP along with official GDP data. Additionally, we offer a projection for real GDP based on historical analogs. Finally, we offer in the shaded areas our systematic regime recognition of recessionary conditions, which allows us to estimate impending recessions:

As we can see above, our regime recognition has done a good job of helping us spot declines in economic activity in real-time. While we don’t share exactly how we estimate these regimes to protect our edge, we share some of the intuitions underlying these estimates. Principally, we expect pressures on business activity to translate into a drag on employment activity, precipitating a recession.

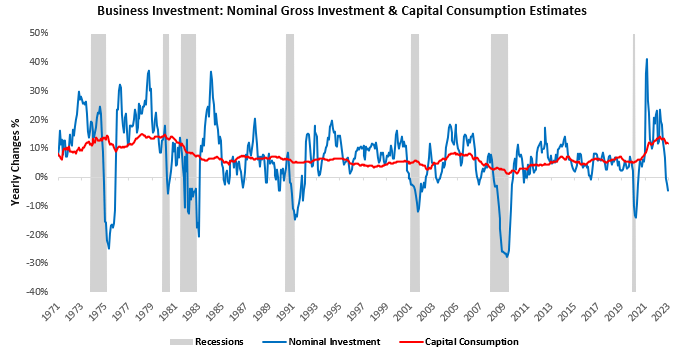

Weakness in business conditions has already led to a pullback in business investment, while capital consumption continues to creep higher, reflecting inflationary pressures:

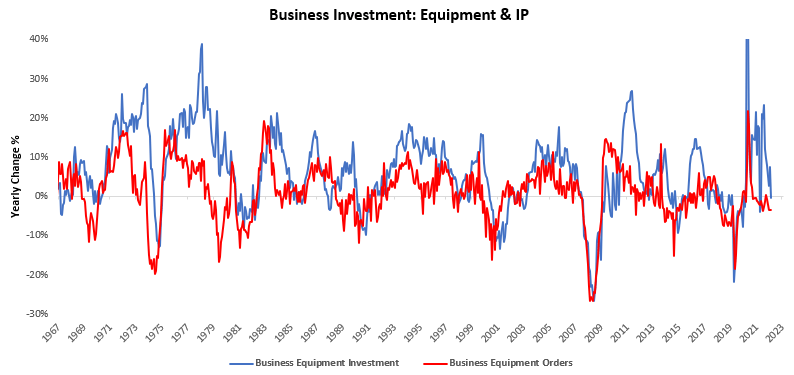

Measures of future business activity continue to decline:

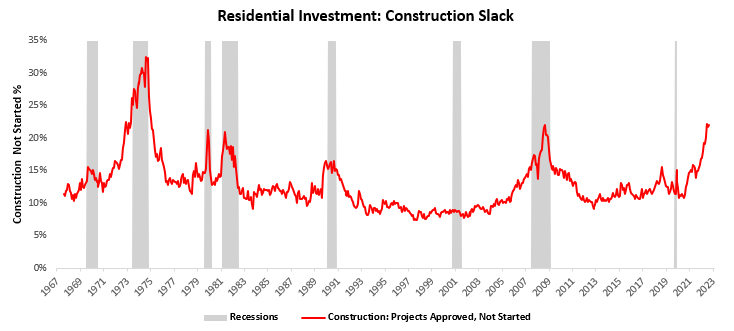

While estimates of investment slack continue to build:

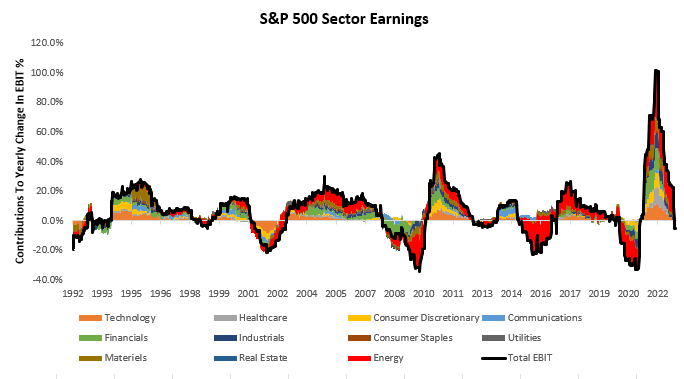

Profits are declining:

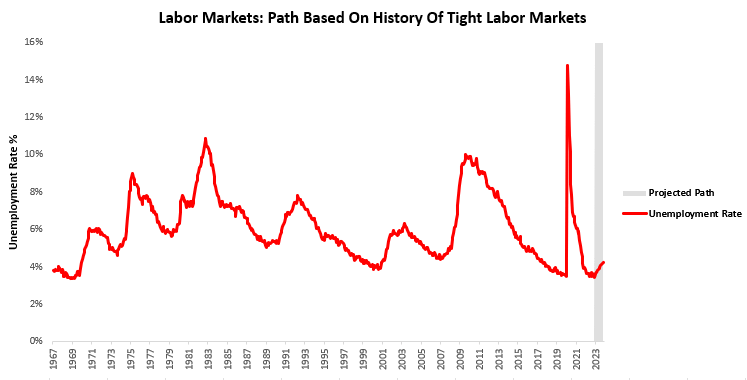

And while labor markets are tight, a reversion to a trend consistent with historical analogs suggests higher unemployment:

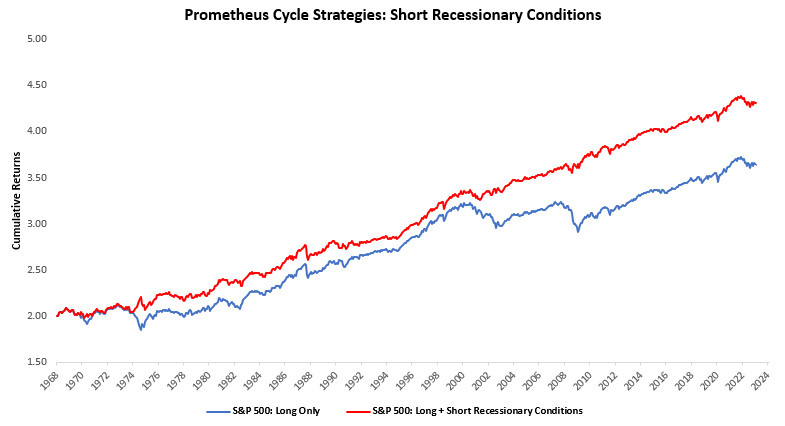

The combination of these factors leads us to believe that the criteria for future recessionary conditions have been met. Now, while many may suggest that the labor market has not indicated recession, we think it is important to recognize that by the time labor markets have confirmed recession, the opportunity to profit from it in markets is long gone. Therefore, to profit from recessionary conditions, we need to be positioned before labor market weakness, not after. Below, we show one of our Prometheus Cycle Strategies, which applies the concepts discussed here to trade markets. The intuition of the strategy is straightforward; as recessionary conditions as described above build, we seek to short stock markets; otherwise, we remain long. We show the cumulative performance below:

As we can see, this approach has been an able guide in navigating recessions. This strategy has turned short this month. Keep in mind this strategy only trades real growth contractions not inflation, liquidity, or other factors. Based upon our construction of this regime recognition, it is unlikely we will experience whipsaw in the recession signal, i.e., it is highly likely to persist. If so, forward-looking equity returns are likely to be weak at best, significantly negative at worst. Until next time.

best non steroid muscle builder