Gold, Fixed Income, & Commodities

Welcome to our official publication of the Prometheus ETF Portfolio. The Prometheus ETF portfolio systematically combines our knowledge of macro & markets to create an active portfolio that aims to offer high risk-adjusted returns, durable performance, & low drawdowns. Given its systematic nature, we have tested the Prometheus ETF Portfolio through decades of history and have shown its durability. For those of you who are unacquainted with our systematic process, we offer a detailed explanation here:

In this publication, we will discuss the performance, positioning, & risks of the Prometheus ETF Portfolio and it will be published every week on Fridays to help investors understand how our systematic process is navigating through markets. Before we dive into our ETF Portfolio positions, we think it is important for subscribers to understand the context within which our systems are choosing their exposures. Below, we offer our detailed Month In Macro note, which contains the conceptual underpinnings of our systematic process within the context of the latest economic data:

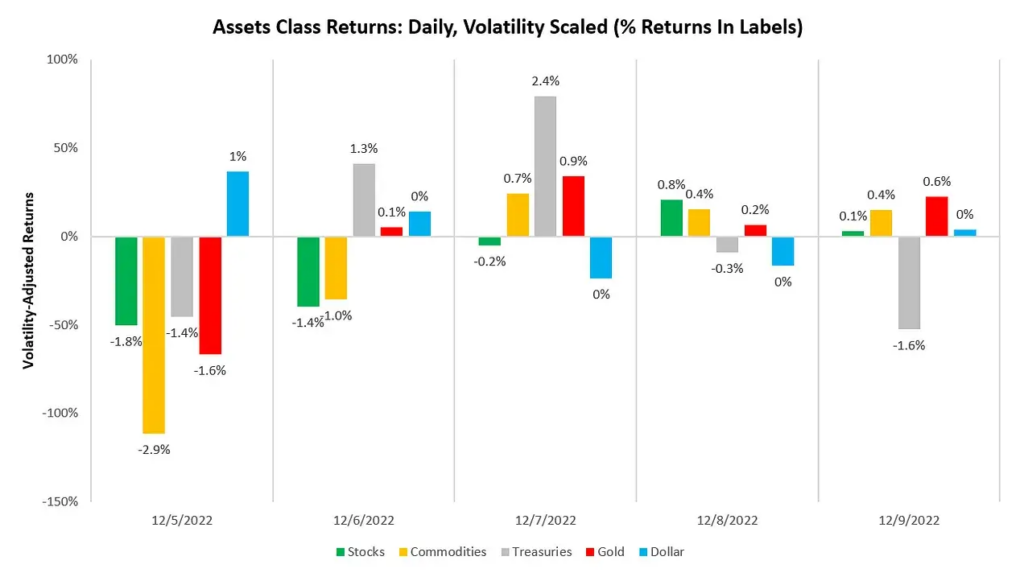

Turning to the week that was asset markets marginally moved to increase their pricing of stagflationary nominal growth and tightening liquidity. This cross-asset pricing saw the dollar, commodities, and gold generally rising through the week; however, sharp sell-offs were seen across assets.

While equities and long treasuries fared poorly, pulses of market moves supported these assets through the week. There is a significant back-and-forth in current market pricing as assets try to ascertain the outlook for inflation and, in turn, the Federal Reserve’s next potential steps. As we have detailed in our Month In Macro note, there is a confluence of competing forces trying to determine the economic environment: the weakening of credit conditions and the strength of income conditions. The give-and-take of these economic forces is creating mixed economic data, which results in mixed market reactions. For our part, this week has shown data fairly consistent with our broader assessment that weaker leverage cycle dynamics will result in lower production. We see incremental signs of these moves in this week’s trade data:

Export contributions to real GDP have moderated and are likely to continue to do so as production continues to decelerate while services spending remains resilient. The combination of these factors will likely turn net exports from a contributor to GDP to a detractor from GDP over the next six months, a path that would be more consistent with historical dynamics. However, alongside these confirmations of a declining production environment, goods orders remained strong, driven by transportation:

New Orders for Industrial Durable Goods came in at 10.8% versus the prior year, a sequential deceleration from the last print. This print disappointed expectations with a monthly change of 1% versus expectations of 1%. Transportation Equipment has been the largest contributor to these moves, with a weighted year-over-year growth of 7.9%. Over the last year, Durable Goods New Orders have been on an uptrend, and the latest values confirm this trend.

Now, while this nominal data remains strong, our estimates tell us that a very large portion of these changes come from price increases. On a real basis, we estimate that total manufacturing new orders have decreased -by 1.32% versus one year ago. Manufacturing new orders are at odds with industrial production, telling us there is pressure on industrial production to fall:

As we can see, the current economic picture is a nuanced one i.e., one that does not lend itself well to sustained trends. This back and forth was further evidenced in PPI data today, which catalyzed a significant sell-off in US Treasuries:

PPI data came in showing a monthly increase of 0.3%, leading to a 7.3% change versus a year ago, exceeding consensus expectations. This reading was a sequential deceleration within a decelerating 12-month trend. Personal Consumption Goods Trade Svcs, Energy, Food, Finished Consumer Services, & Private Capital Equipment Trade Svcs. have exerted the largest influence on PPI over the last twelve months. Below, we show the top 10 contributors to today’s print:

As we can see, two items in the goods economy showed a significant drag on PPI datatransport and energy, i.e., the divergence between the goods and services economy we highlighted in the Month In Macro remains in place, though now with incremental convergence:

Overall, our outlook remains one where nominal economic activity will continue to decelerate, with real growth likely to be weaker than inflation. Activity in the economic can take place through the spending of income or the spending of credit. Currently, we are seeing aggregate private wealth move in a direction that is consistent with slowing nominal spending significantly; however, income remains resilient due to high employment. According to the latest data, both household and corporate balance sheets are contracting:

Furthermore, according to our estimates, the numbers have only gotten worse. Using private sector wealth, we can estimate the potential pass-through to nominal GDP. Below, we show what these estimates imply for future nominal GDP:

As we can see above, the impact of the Fed’s tightening is slowly making its way through the economy. However, the Fed does not have explicit control over the variable it needs to tame to break inflation i.e., nominal income through employment. Therefore, the Fed will need to impact asset prices and credit creation enough to reduce reinvestment and profitability to further contract production, which will eventually show up in employment data. Make no mistake, this process is underway, which creates opposing forces for inflation. We expect the result of these forces to be a leveling out of inflation at a higher level than the Fed is comfortable with. However, over the next six months, it will only mean that the Fed will lean on the duration for which they hold policy rates elevated rather than the speed and size of increases in interest rates. The combination of these factors suggests an environment where growth volatility is likely to be the marginal mover of asset prices rather than inflation volatility. Keep in mind this is a nascent trend, and conditions may very well reverse. However, for the time being, we see increasing potential for this outcome. Our systems reflect these expectations in their positioning of the Prometheus ETF Portfolio heading into next week:

The portfolio is relatively unchanged from this week when the Prometheus ETF Portfolio was down 0.05%. Given the sporadic nature of market moves this week, the combination of commodity and treasury exposure helped neutralize portfolio volatility, which conformed with our expectations. Below, we show the week-to-date attribution of portfolio returns:

Overall, in a violent week of back-and-forth market pricing, this is an acceptable outcome and well within our range of expected losses. Every strategy has losing weeks; they simply need to be constructed to be tolerable ones.

Turning to next week our current portfolio has an expected volatility of 6.75%, with a maximum expected volatility of 10%. The most significant risk to the portfolio is CPI data which will be released on Tuesday, followed by the FOMC on Wednesday. To protect our edge in forecasting, we will provide our subscribers with our CPI forecast on Monday to help risk-manage the event.

Aside from CPI data, the diversification benefit of being long commodities, gold, and fixed income will likely moderate the risk of achieving maximum volatility. For additional color, we share some of our market timing tools to help contextualize the positions within the broader economic context.

-

GLD: Gold remains in a Bull Market. Consistent with this, current market pricing suggests beta capture opportunities.

-

MBB: MBS remains in a Bear Market Rally. Bear market rallies can initiate regime change, and current market pricing suggests beta capture opportunities.

-

IEF: 7-10 Year remains in a Bear Market Rally. Bear market rallies can initiate regime change, and current market pricing suggests beta capture opportunities.

-

TLT: 20-30 Year remains in a Bear Market Rally. Bear market rallies can initiate in regime change, and current market pricing suggests beta capture opportunities.

-

CANE: Sugar remains in a Bull Market Correction. While we are in a correction, our gauges suggest Bull Market conditions continue to support beta capture opportunities.

-

SOYB: Soybeans remain in a Bull Market. Consistent with this, current market pricing suggests beta capture opportunities.

-

SLV: Silver remains in a Bull Market. Consistent with this, current market pricing suggests beta capture opportunities.

Change is afoot in both the economy and markets, with competing forces trying to determine the potential path. The future is dynamic, and our systems will adjust as required. Until next week.