Staying Long Diversified Assets

Welcome to our official publication of the Prometheus ETF Portfolio. The Prometheus ETF portfolio systematically combines our knowledge of macro & markets to create an active portfolio that aims to offer high risk-adjusted returns, durable performance, & low drawdowns. Given its systematic nature, we have tested the Prometheus ETF Portfolio through decades of history and have shown its durability. For those of you who are unacquainted with our systematic process, we offer a detailed explanation here:

In this publication, we will discuss the performance, positioning, & risks of the Prometheus ETF Portfolio and it will be published every week on Fridays to help investors understand how our systematic process is navigating through markets. Before diving into our ETF Portfolio positions, we think it is important for subscribers to understand the context within which our systems choose their exposures. Below, we offer our latest Month In Macro note, which contains the conceptual underpinnings of our systematic process within the context of the latest economic data:

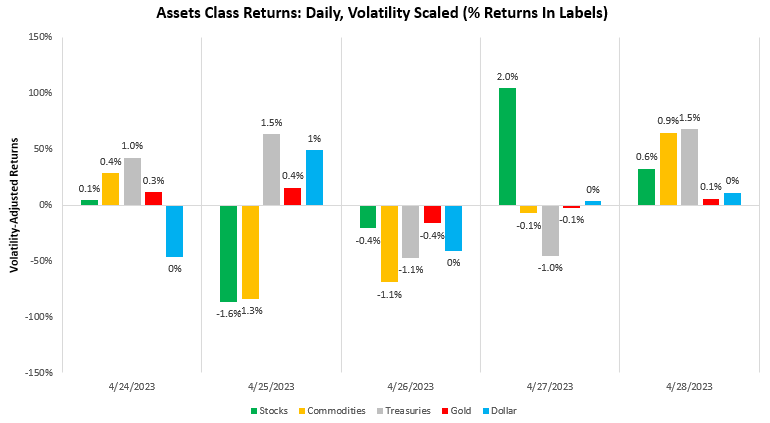

This week, assets rebounded from the risk-off hue of last week. However, asset markets did not show decisive growth or inflation pricing, with assets generally rising across the board, i.e., diversification paid this week:

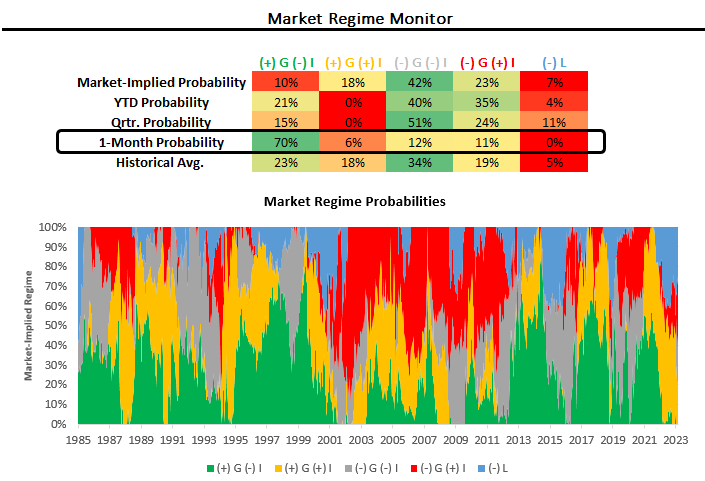

Over the last month, asset markets have moved to price in rising growth expectations. However, our systems estimate that the durable trend is likely in the opposite direction, i.e., of falling growth expectations. Below, we show our market regime monitors which offer how markets have resoundingly priced improving growth outcomes over the last month:

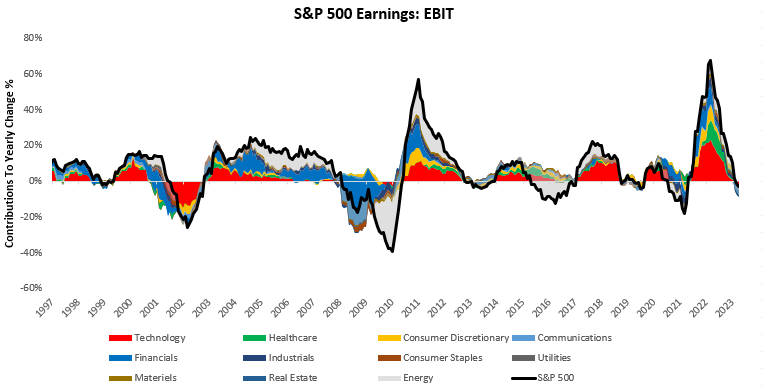

Markets have priced these rising growth expectations as earnings surprised to the upside, typical during earnings season. However, earnings growth versus one year prior has deteriorated. Below, we show the composition of S&P 500 earnings by sector:

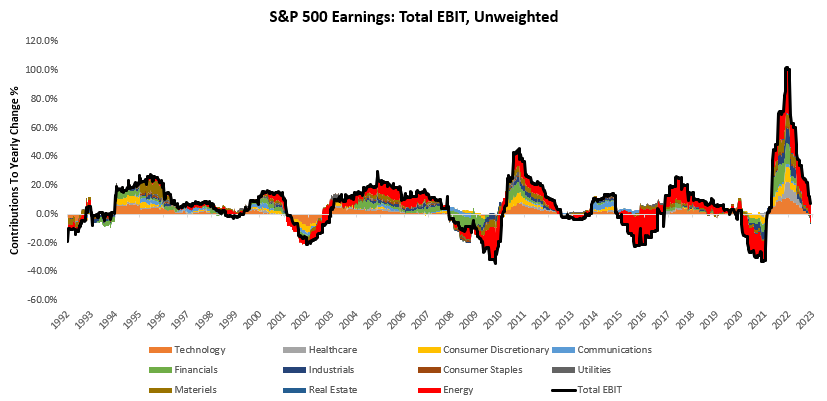

While this picture is roughly in line with our expectations, i.e., that earnings will continue to deteriorate as the tightening cycle worsens, it is important also to recognize that the high inflation environment we are in continues to support producers in raw materials in particular, the energy sector. The S&P 500, and any market capitalization-based aggregate, is tilted towards technology names. Therefore, when assessing earnings, it is important to remove the impact of market capitalization weightings to look at total earnings. From this perspective, total EBIT remains positive:

While total EBIT remains positive, it is almost entirely driven by energy sector earnings, barring which total earnings are down 5% versus one year prior, with 7 out of 11 sectors reporting weaker earnings.

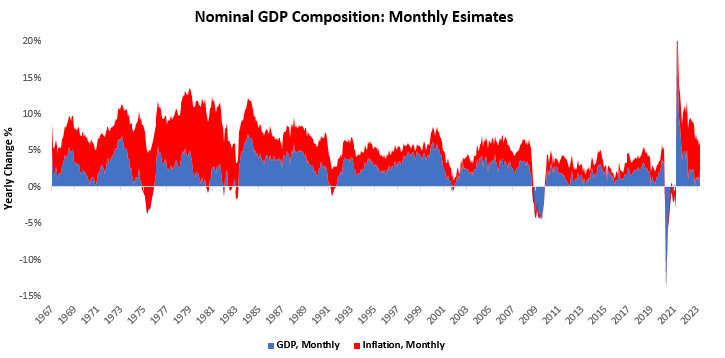

This resilience in energy profitability aligns with our latest tracking of nominal growth. Below, we show the composition of monthly estimates of nominal GDP, broken into real GDP growth and inflation. Our latest estimates place nominal GDP at 6.41% versus one year prior:

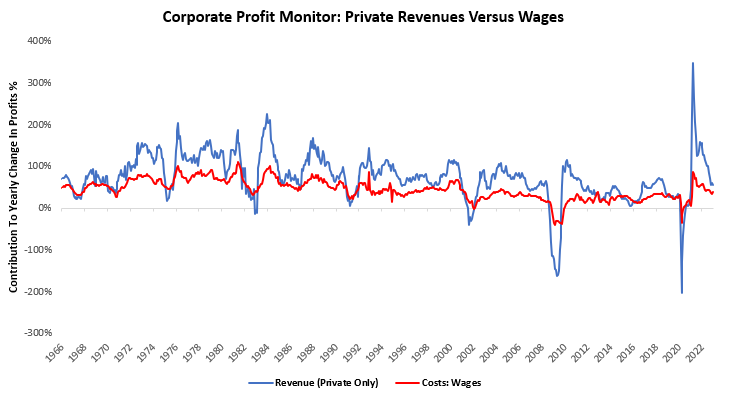

As we see above, inflation is the dominant driver of nominal growth today, accounting for 65% to 75% of nominal growth. This nominal growth has largely flowed to energy sector profits, supporting aggregate profits, which holds up employment. However, it is unlikely that these dynamics can continue as nominal business sales continue to fall while nominal employee compensation remains elevated. Below, we show the weighted impact of this balance between income (revenues) and costs (employee compensation):

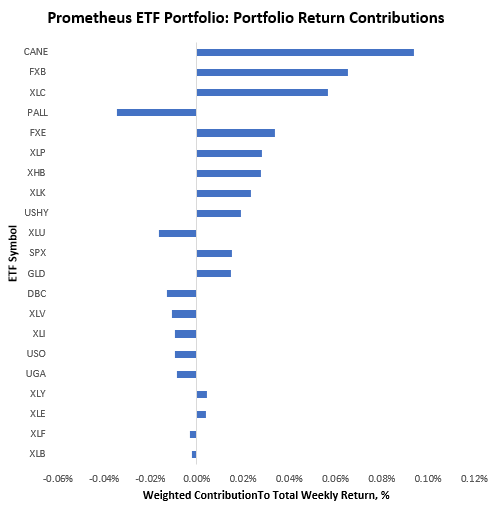

Overall, nominal growth remains elevated, with real growth at extremely low levels. Our expectations for a contraction in GDP growth beginning in H2 of 2023 remain in place. Nonetheless, it is important to recognize that recent data has moved counter to a trend that would support this destination. These circumstances were in mind when we designed our systematic process for the Prometheus ETF Portfolio- which has allowed us to navigate this period of heightened growth expectations well despite having a fundamental growth view that economic conditions would deteriorate. We trade the markets in front of us, and this approach fared well this week, with the Prometheus ETF Portfolio up 0.30%. Below, we show the attribution of these returns below:

This week’s diversified mix of assets in the portfolio worked in our favor, as no single asset class offered a smooth ride. Next week, our systems continue to bet on a diversified pool of assets, as growth and liquidity pricing in the market run counter to our expectations, while inflation pricing aligns with them. Below, we show how our systems are looking to position the Prometheus ETF Portfolio:

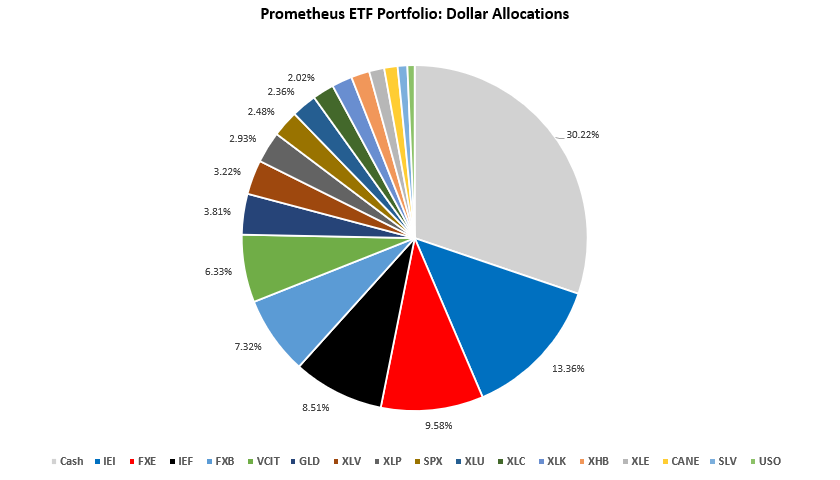

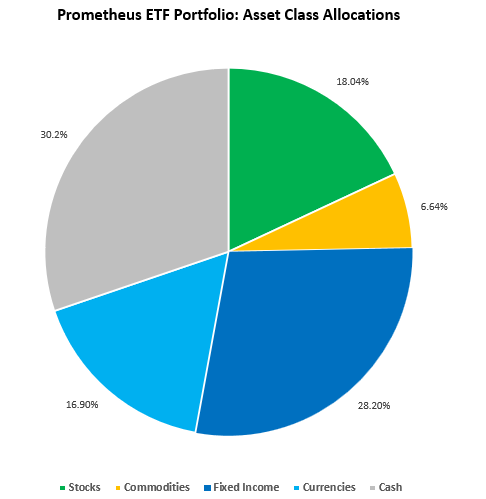

POSITIONS: Cash (BIL): 30.22% IEI : 13.36% FXE : 9.58% IEF : 8.51% FXB : 7.32% VCIT: 6.33% GLD : 3.81% XLV : 3.22% XLP : 2.93% SPX : 2.48% XLU : 2.36% XLC : 2.02% XLK : 1.91% XHB : 1.72% XLE : 1.41% CANE: 1.25% SLV : 0.9% USO : 0.68%

We show these at the asset class level:

Markets continue to provide opportunities as inflation volatility stabilizes, stabilizing the path for liquidity conditions. The combination of these factors is a net support to not just stocks and bonds, but all assets. We see the eventual shift from this dynamic coming from growth volatility rather than renewed inflation volatility, but we carefully monitor the evolution of conditions. Until next week.

Use this online translator to convert your sentences into different languages effortlessly.

To ensure integrity in the gambling industry, one critical aspect is game fairness, as it governs the randomness of outcomes in virtual games.

Quick, accurate, and dependable.

generic lisinopril prices

I always find great deals in their monthly promotions.

Outstanding service, no matter where you’re located.

order generic cipro without prescription

They provide international health solutions at my doorstep.

The best place for quality health products.

does gabapentin interact with ambien

Their adherence to safety protocols is commendable.

I value their commitment to customer health.

cost generic clomid no prescription

Their staff is so knowledgeable and friendly.

The staff always ensures confidentiality and privacy.

order generic clomid without prescription

Always stocked with what I need.