Prometheus Cycle Strategies: Trading Stagflation

This report is part of our ongoing effort to provide economic and market guidance to our subscribers during a period of historic levels of uncertainty. This note aims to share our research team’s internal checkpoint process in evaluating the current state of the economy as it pertains to markets. The pages that follow will have familiar content for those who follow our work, but with the added benefit of our connecting the dots across all the economic and financial data that our systems use to make portfolio decisions. Our primary takeaways are as follows:

-

Nominal GDP has slowed modestly in Q1 of 2022. Our latest estimates place nominal GDP at 6.35% versus one year prior.

-

While growth continues to slow and we head towards a real GDP contraction, the current level of nominal spending far exceeds the economy’s output capacity, producing inflationary pressures. To contain inflation, policymakers must significantly deteriorate real economic activity, bringing down nominal spending.

-

Our systems tell us that we remain extremely far from the conditions required to bring inflation to a target of 2%, forcing policymakers to continue on their tightening path. These dynamics create an opportunity set for our systems to exploit as markets move to re-price further tightness.

In this issue, we will continue to weave in our systematic expectations for markets as part of our Month In Macro offering. In this edition, we will be mainly focused on the inflation outlook. Additionally, this edition will be relatively concise relative to our typical publications to focus on the topic at hand. Now, let’s dive in.

Below, we show the two big-picture paths for CPI inflation- one with a recession and one without:

Based on our estimates, inflation will likely stay well above the Fed’s 2% objective without a recession over the next year, creating an opportunity for our Prometheus Cycle Strategies in US Treasuries.

Prometheus Cycle Strategies: Inflation

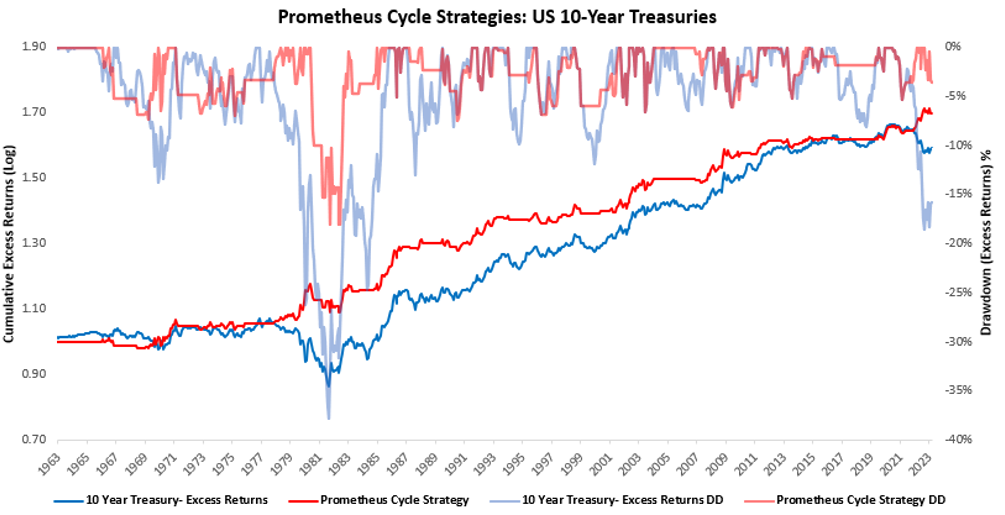

Our Month In Macro report aims to offer a granular and comprehensive understanding of current economic conditions and how they will likely evolve- to help investors navigate markets through the economic cycle. To augment the research and analysis, we have developed Prometheus Cycle Strategies- which use our cyclical expectations to trade markets. These Cycle Strategies reflect the understanding that particular points in the economic cycle offer an asymmetrically positive return on risk, either long or short assets. Using our systematic process, we attempt to forecast these points to harvest these attractive return-to-risk characteristics.. Below, we show the first of the Prometheus Cycle Strategies- which trades the 10-Year Treasury based on inflation regimes:

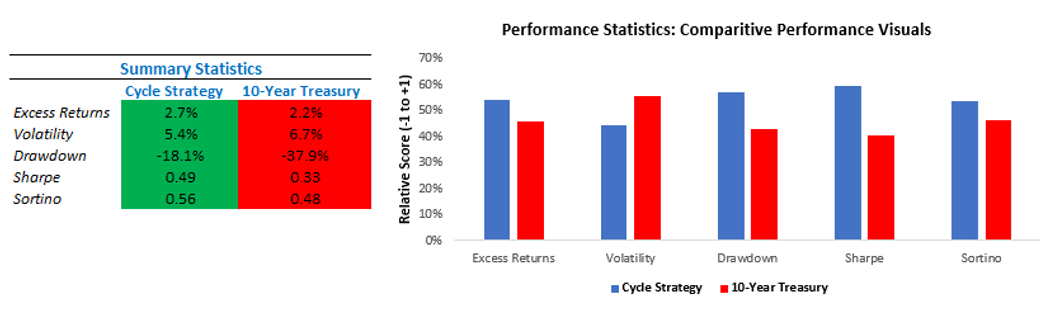

The strategy above seeks to short Treasury bonds during periods where inflationary pressures lead to policy tightening expectations, goes long during easing cycles, and otherwise remains in cash. As shown above, the system performs well, outpacing 10-Year Treasury returns with smaller drawdowns. Importantly, it does so with minimal market exposure- with a beta of 0.24 and remains active in the market only 54% of the time. This performance reflects our understanding that there are particular points in the economic cycle where an asset offers a significantly higher return on risk than during other periods. Harvesting these returns can lead to significant outperformance. Below, we show some summary statistics:

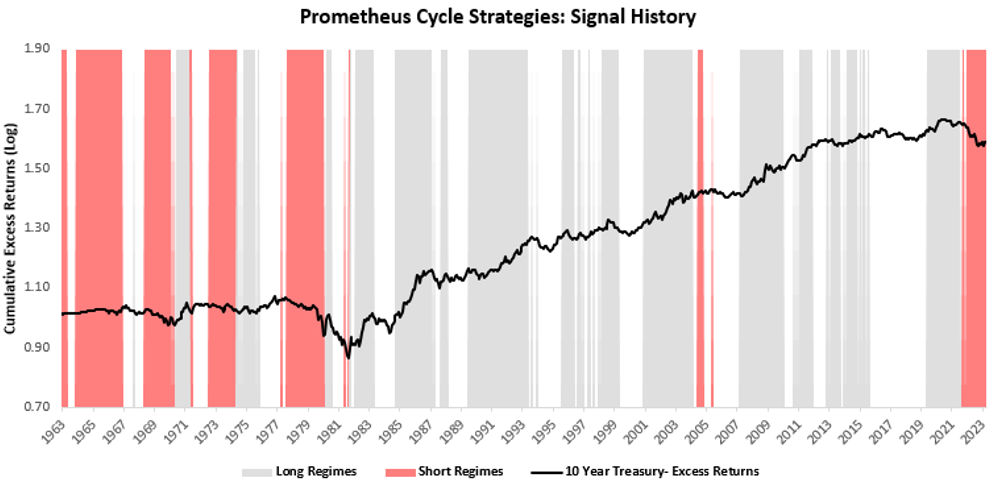

In the case of Treasuries, this pay-off profile can be obtained by shorting bonds as we move into an inflationary hiking cycle and buying them as we enter a recessionary cutting cycle. These turning points in the economic cycle offer some of the most substantial return-on-risk opportunities, both long and short. Below, we show the signal history of the strategy:

We think it is important to address that there is a significant amount of regime clustering in the signals, i.e., the short signals are clustered to the pre-1983 period. In contrast, the long signals are clustered in the periods after 1983 until 2021. This clustering is not due to a mechanical bias in signal construction but rather a function of the path of history. Below, we show the post-1983 period simply did not offer a significant opportunity set on the short side:

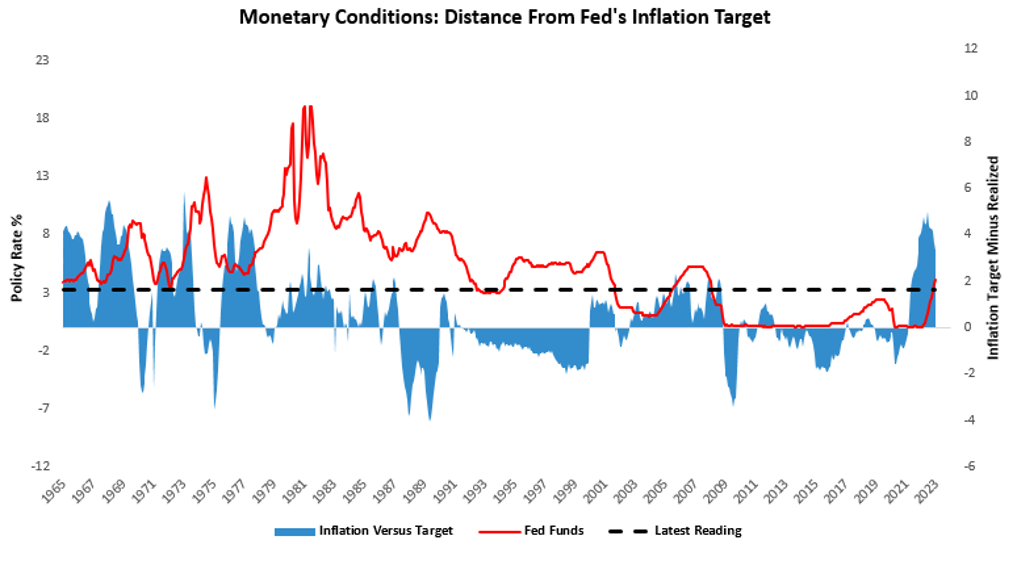

Above, we show our estimates, an implicit estimate of monetary conditions, showing how far realized inflation is from the Fed’s objectives. To construct this estimate, we examined decades of Fed transcripts back to the 1960s to understand the Fed’s contemporaneous inflation objectives. We then look at the difference between the Fed’s inflation target and realized inflation, which tells us how loose or tight monetary policy is at a given time. Our inflation strategy attempts to exploit inflationary hiking cycles, which require inflation to be significantly beyond the Fed’s objectives. As we can see, there was a shortage of these inflationary overshoots until 2021. Therefore, we think the modest long bias in the strategy is a function of the path of history rather than signal construction.

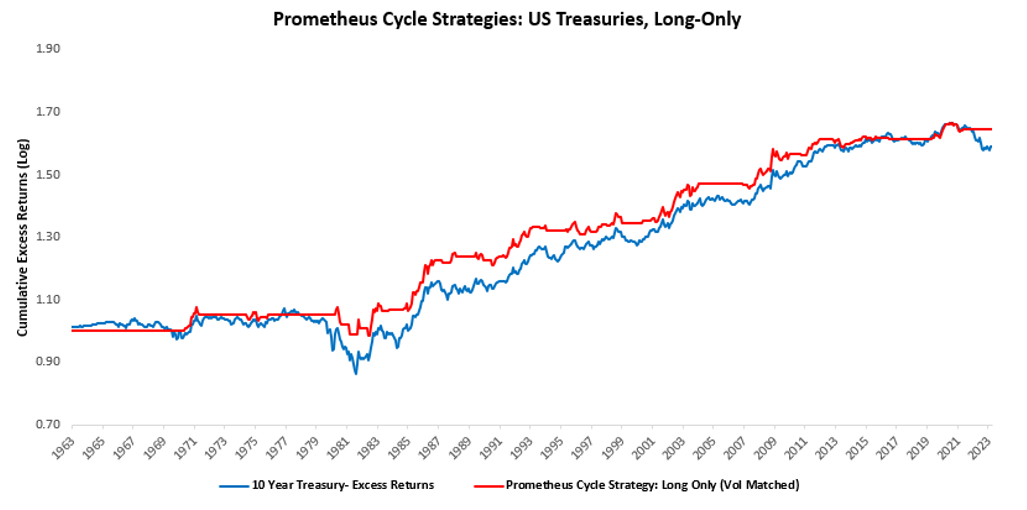

This evaluation is critical today, as inflationary pressures remain at historical extremes. Being well prepared for a sustained battle by the Fed against inflation will be vital in determining portfolio performance. As always, we believe this matters whether you are long-only or long-short. Long-only investors can also gain a modest edge by avoiding the impacts of sustained inflationary hiking cycles by remaining invested only during cutting cycles. Below, we show how our cycle strategies remain value additive to even those that manage long-only portfolios:

The strategy is in a bearish regime and positioned short. Therefore, even if you are a long-only investor, the bearish outlook of our systems implies that the forward-looking returns on treasuries will be weak at best and significantly negative at worst. To protect our edge in markets, we do not share our signal construction; however, we share the logic driving our systems’ expectations over the pages that follow.

I am really inspired along with your writing skills and also with the structure on your blog. Is this a paid topic or did you modify it yourself? Either way stay up the nice high quality writing, it’s uncommon to look a nice blog like this one nowadays!