Below, we share a section from our latest Month in Macro report that was shared with our Institutional and Research Suite clients. Month in Macro aims to share our research team’s internal checkpoint process in evaluating the current state of the economy as it pertains to markets. The pages that follow will have familiar content for those who follow our work, but with the added benefit of connecting the dots across all the economic and financial data our systems use to make portfolio decisions. Email us at info@prometheus-research.com to learn more about Institutional Offering.

Alpha is a function of the path of macroeconomic conditions relative to what markets have priced in. We see the current forward path of the macroeconomy as one of stable but potentially decelerating nominal GDP and liquidity conditions. Relative to these expectations, markets are pricing in rising earnings, elevated inflation, and weaker liquidity conditions. We scan across this pricing below, starting with earnings expectations.

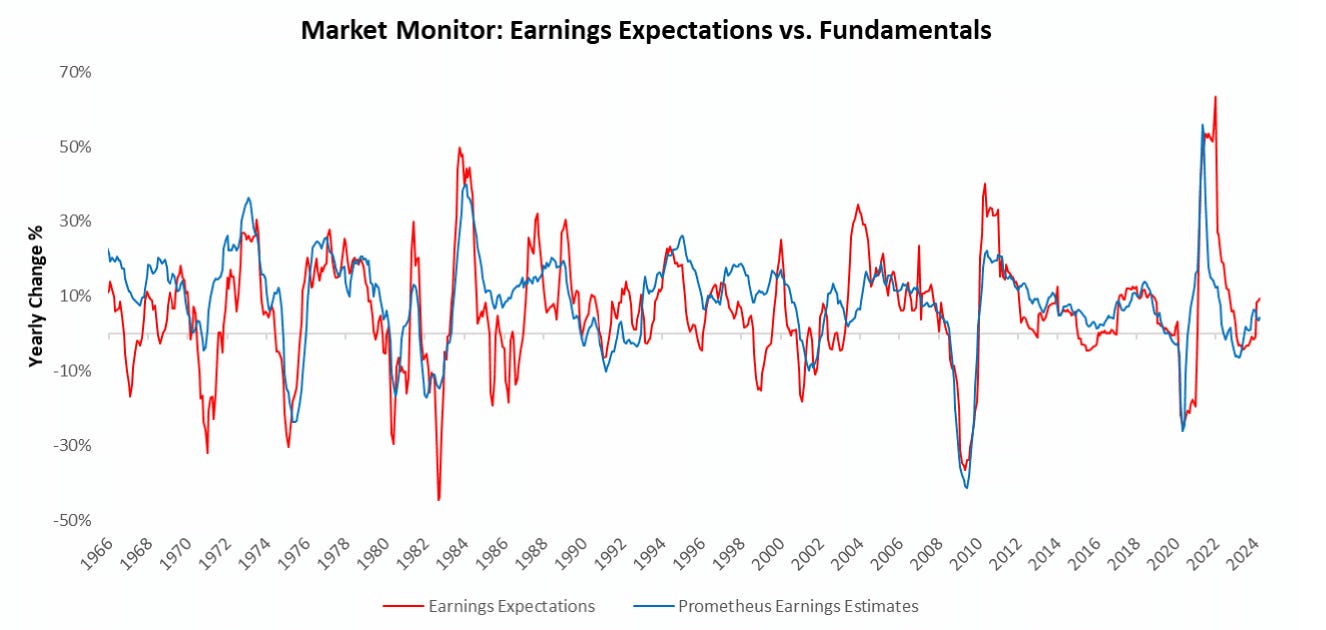

Markets have moved to price in rising earnings expectations in a manner that is modestly ahead of our fundamental estimates.

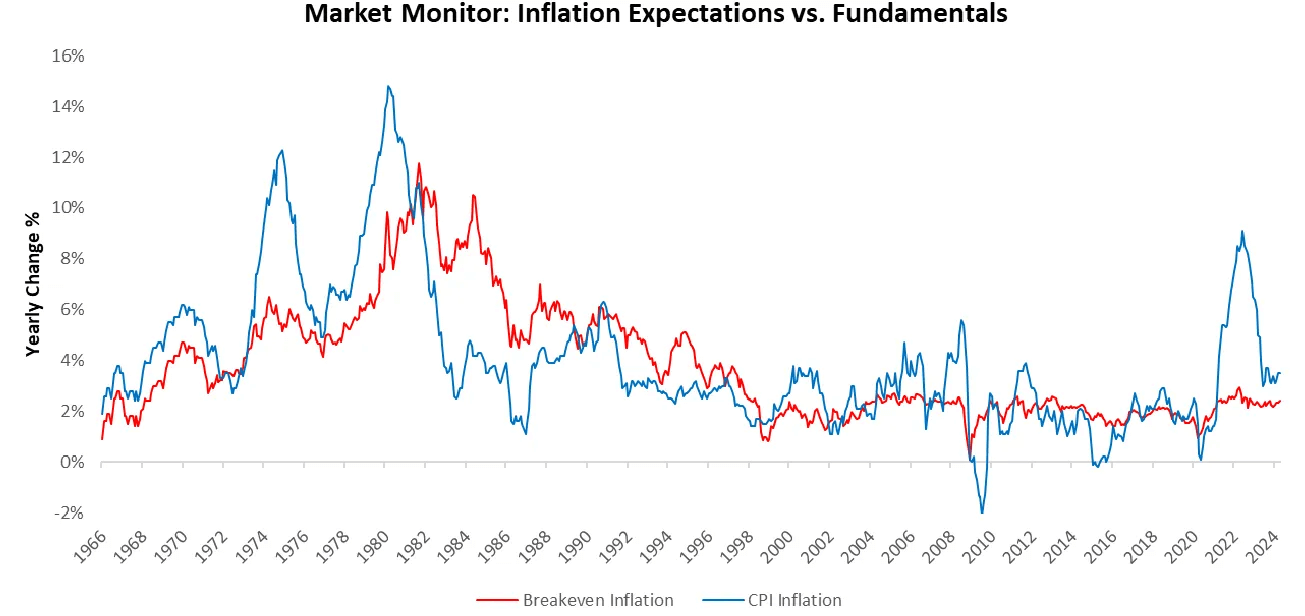

Turning to inflation, we see pricing once again largely consistent with the recent macro impulse:

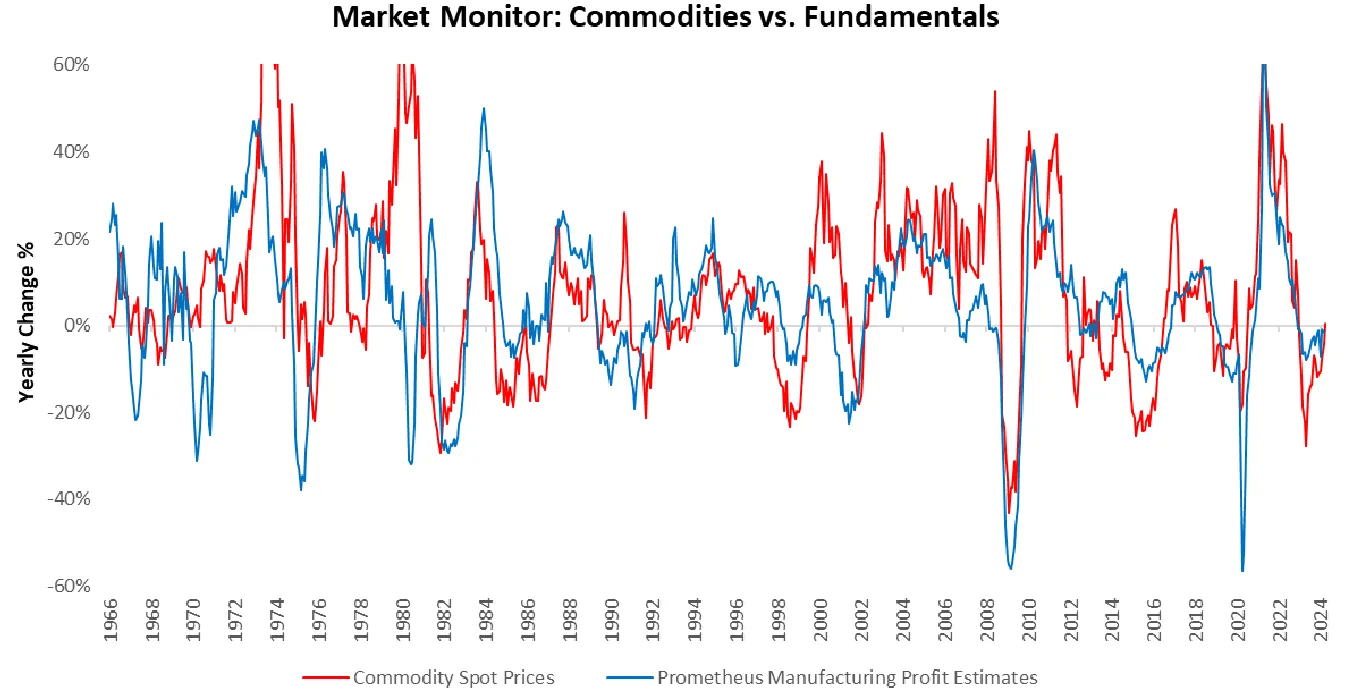

We see similar outcomes in commodity prices:

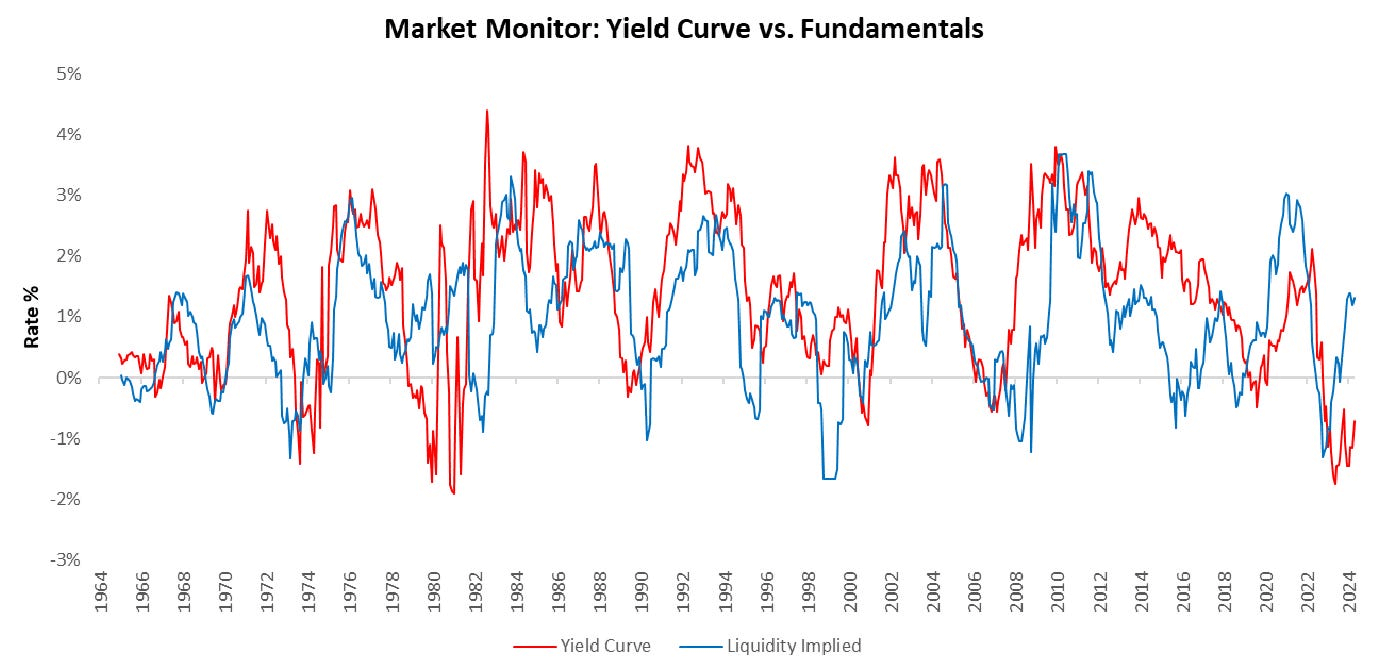

Finally, the most significant mispricing remains of liquidity in the yield curve.

While liquidity is not directly measurable in markets, history has shown the yield curve to largely be a strong barometer of liquidity conditions. Above, we show the fitted values of our liquidity gauge to the yield curve. As we can see, the yield curve remains cheap to current liquidity dynamics.

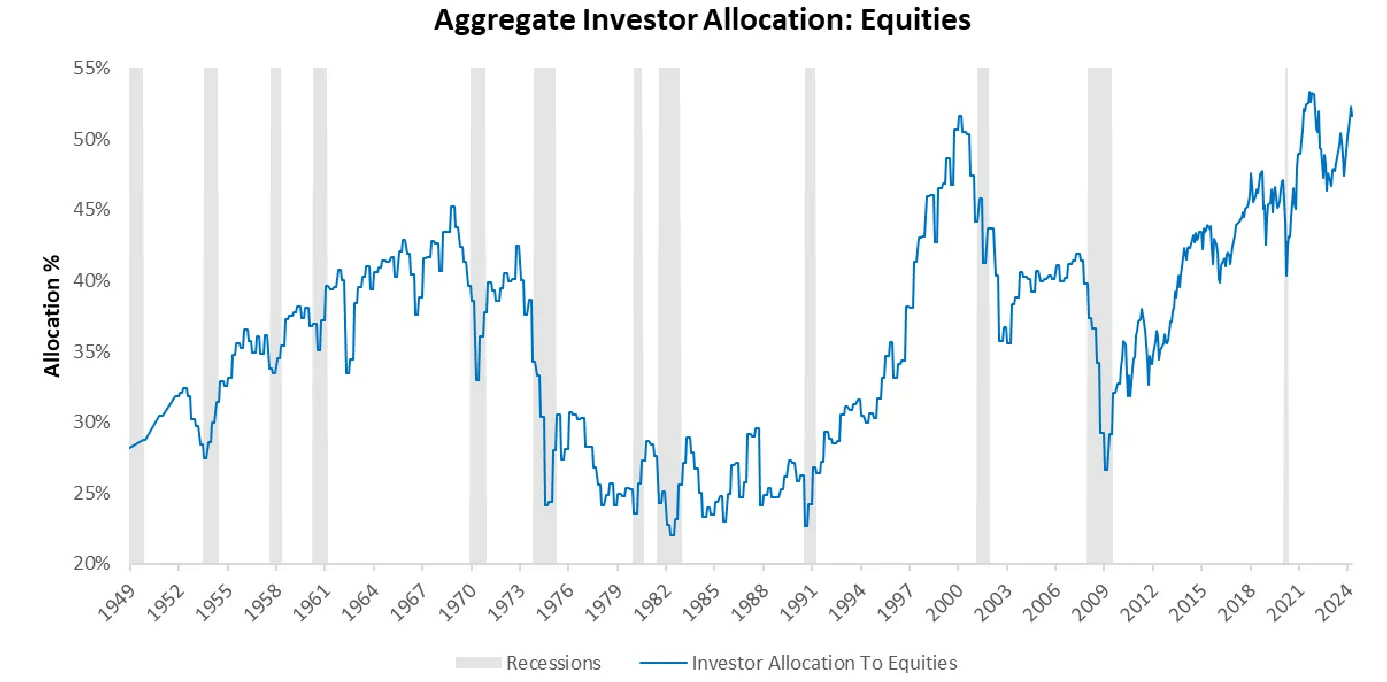

Therefore, scanning across market pricing for growth, inflation, and liquidity- we currently see limited alpha opportunities. While this means there are no significant current alpha opportunities, there remain significant prospective ones. Particularly, we see the recent performance of stocks relative to all other assets as a performance that cannot be sustained indefinitely. This expectation is because our measures of the aggregate private sector allocation to corporate equities are now at all-time highs, consistent with those that last occurred during the COVID-19 rebound and the Dotcom peak. We visualize this allocation below:

As we get further into historically elevated equity allocation levels, the continued outperformance of equities relative to other assets becomes less probable. However, it is critical to recognize that investor allocations can have extremely large time trends, sometimes spanning decades. Said differently, stretched allocation is not a cause of reallocation. For investors to reduce their equity holdings to prefer other assets, we would need to see a meaningful change in economic activity, which, based on our assessment, remains unlikely. If and when we see a macro regime change, the potential alpha opportunity in equities will likely be large. Until next time.

14 thoughts on “Market Pricing: Alpha Opportunities Compressed”

Muchas gracias. ?Como puedo iniciar sesion?

Consistent excellence across continents.

order generic lisinopril pills

Their medication reminders are such a thoughtful touch.

A powerhouse in international pharmacy.

get cipro pill

I’m impressed with their commitment to customer care.

A pharmacy that’s globally recognized and locally loved.

can you get generic clomid without a prescription

I always feel valued and heard at this pharmacy.

I’m impressed with their commitment to customer care.

fluoxetine brand name

They’re at the forefront of international pharmaceutical innovations.

Their worldwide delivery system is impeccable.

where buy generic cipro prices

Their online prescription system is so efficient.

can i buy clomiphene tablets can you get cheap clomid without rx where can i buy cheap clomiphene without prescription where can i get clomid can i buy cheap clomid pill where to buy generic clomid pill where to buy clomid tablets

Greetings! Very useful par‘nesis within this article! It’s the little changes which will obtain the largest changes. Thanks a lot towards sharing!

azithromycin where to buy – tindamax cost buy flagyl generic

buy semaglutide 14 mg for sale – semaglutide 14mg pills buy periactin 4mg

brand domperidone 10mg – generic cyclobenzaprine flexeril without prescription

order inderal pills – purchase methotrexate online cheap methotrexate 5mg uk

purchase amoxicillin for sale – cheap amoxil pill ipratropium brand

buy zithromax sale – bystolic 5mg brand buy nebivolol 5mg online