Our best Month In Macro to date. 50 pages of the most granular and actionable systematic macro research you will find anywhere. Click the link below to begin reading:

This note aims to share our research team’s internal checkpoint process in evaluating the current state of the economy as it pertains to markets. The pages that follow will have familiar content for those who follow our work, but with the added benefit of our connecting the dots across all the economic and financial data that our systems use to make portfolio decisions. Our primary takeaways are as follows:

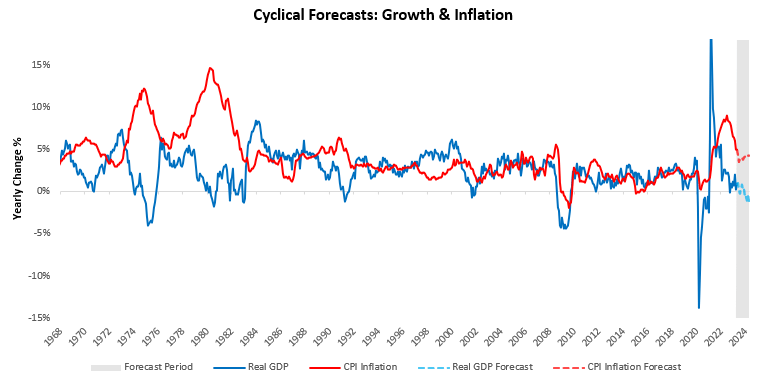

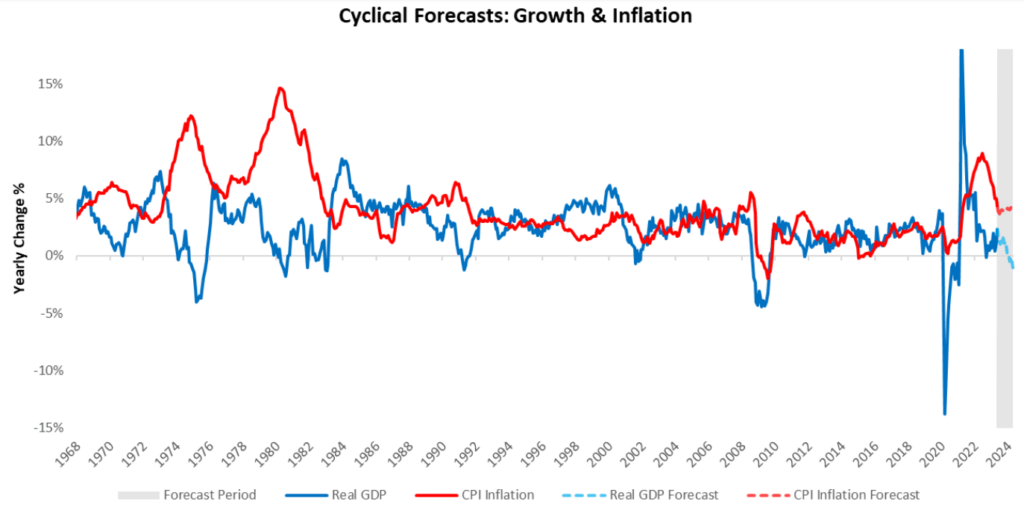

- Nominal GDP expanded by 1.05% in June, with real GDP increasing by 0.86% with inflation rising by 0.14%. This composition was a significant expansion in real activity.

- Liquidity conditions have remained buoyant, with nominal GDP continuing to flow to the money market complex.

- Equity markets have enjoyed this real growth acceleration, and liquidity has facilitated a significant bid for stocks versus bonds. Bonds continue to struggle as markets continue to price interest rate cuts, only to be thwarted by resilient nominal spending data.

- Looking ahead, real growth is unlikely to continue at this pace, though inflation is likely to remain resilient. Liquidity will likely soften as the treasury moves to lengthen its duration.

The views outlined in our last Month In Macro played out well over June; for reference:

“We think that if you’re long equity risk, you’re long liquidity with support from better-than-expected nominal growth. Stocks have continued to cross-current that could swing either way, but stocks look better than bonds until economic activity deteriorates enough to hurt inflation. Bonds remain exposed to losses so long as they price in expectations of cuts.”

The picture remains the same for bonds, though signs of change are emerging for equities. Our expectations for growth and inflation future expectations remain a headwind for assets. Shown below: