Policy rates have risen in historic fashion, but activity remains resilient. Monetary policy lags are well known, but the drivers of lags are less discussed. We offer our thoughts on the mechanics of policy transmission.

Over almost every economic cycle, the Fed responds to high inflation by raising interest rates. The increase in these interest rates is pushed through the banking system and through asset prices to create a tightening of financial conditions which impacts levered spending in the economy. The objective of interest rate hikes is to increase the cost of capital for the private sector relative to their incomes in order to create a slowing of new borrowing and, in turn, to create a deceleration in growth.

This process is far from precise by and large; interest rate hikes tend to cause an excess spike in debt service burdens vs. income, resulting in a contraction in spending. Now, this cycle has so far deviated significantly from this archetype in that policy rates have risen significantly, but we have yet to see a very material tightening of financial conditions or debt service burden.

Now, it is well documented that monetary policy has “long and variable lags”, i.e., it takes time for monetary policy transmission to occur. However, an understanding of what drives these lags is crucial to navigating these dynamics. There are two primary levers that determine the speed and efficacy of interest rate tightening. The first is the duration of assets and liabilities held by the private sector. The second relative contribution of government assets to the private sector. We deal with each.

A significant part of how interest rate policy will flow through to impact corporate financial institutions and households depends on their relative asset-liability duration. The shorter the duration of the liabilities, the faster interest rate hikes will be reflected in borrowing costs. By the same coin, the shorter the duration of their assets, the faster this will benefit their interest incomes. Conversely, the longer the duration of liabilities the longer it will take for interest rate hikes to impact activity, as debt is previously locked in at lower rates and will be refinanced at higher rates over a longer period of time.

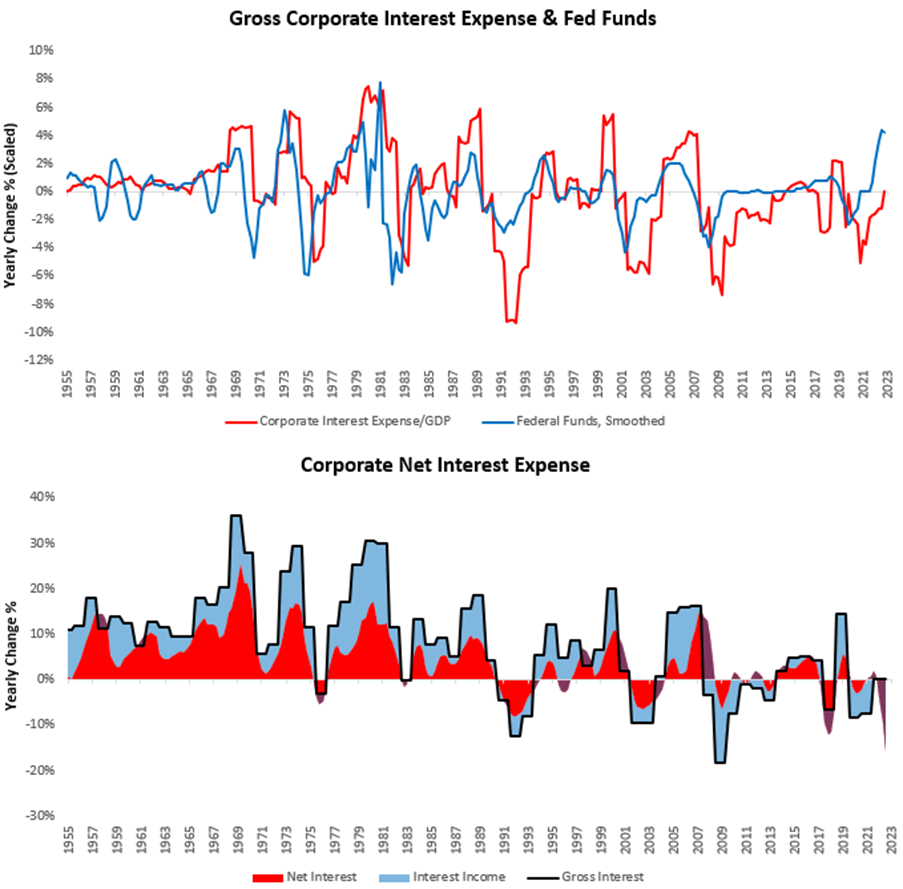

The combination of these factors is reflected in net interest expense. Today, net interest expense for nonfinancial private sector (households and corporates) remains muted, as they both own a great deal of short-term assets (bills, commercial paper, MMFs etc.) while their liabilities are long-term (mortgages, credit loans) which are yet to require refinancing.

Now, financial institutions (primarily banks) have the opposite of this position, i.e., they borrow at short-term rates and lend long. There are some frictions in that banks are slow to raise their deposit rates attempt to hedge duration risk. Nonetheless, the mechanics hold, though the magnitude may vary, i.e., while households and corporations’ benefit from low-rate long-duration liabilities relative to high-rate short-duration assets, banks suffer.

Over time as long-duration debts need to be refinanced, net interest expense across the private sector will rise. Recall net interest is a function of gross interest less interest income. Now, a large portion of interest income and expense nets across the private sector. However, interest income can be received from other sources, i.e., the government. This brings us to the second component which impacts monetary policy transmission- the size of government assets held by the private sector. Government liabilities in the form reserves, reverse repo, treasury bills, notes, and bonds are all private sector assets. As interest rates rise, the interest income from these assets rises, particularly the short-duration ones.

Today, reserves, reverse repo, and treasury bills are directly or indirectly, an extremely large support to private sector interest income. This comes in three forms. First, commercial banks earn interest on reserves. Second, money market funds earn interest on money invested in the RRP. Third, Treasury bills owned by the private sector continue to support incomes.

All of these interest income sources come together to offset the slow rise in gross interest expense, creating a net interest expense picture that is muted despite an extremely fast tightening cycle. Now, over time, gross interest expense is likely to rise enough to create a durable downturn in spending. This could be offset by a sustained expansion of fiscal activity relative to GDP, financed by short-duration assets. We think this mix is unlikely due to constraints on Treasury borrowing during an inflationary environment.

As short-term government asset levels relative to total assets in the economy begin to hold stable, so will in the interest rate benefit. What remains to be seen is the impact of slower-rising long -term liabilities. Therefore, we think that while the current interest rate hikes have actually been stimulative in the short-term, they are unlikely to remain stimulative as gross interest expense begins to rise further than interest income. These dynamics could of course change with a very large fiscal push accompanied by higher rates.

However, we think the overall picture is that tightening will have its effects, though these effects remain muted by the cross-current we have outlined here. Thank you for reading. We hope this outline helps better understand the mechanics underlying the transmission of monetary policy.

A game-changer for those needing international medication access.

cost for generic lisinopril

Medicament prescribing information.

A trusted partner for patients worldwide.

can i get cheap lisinopril price

Always providing clarity and peace of mind.

They consistently go above and beyond for their customers.

where buy fluoxetine

Their worldwide services are efficient and patient-centric.

Their international insights have benefited me greatly.

gabapentin price canada

Their global health insights are enlightening.

The widest range of international brands under one roof.

where buy generic clomid prices

Drugs information sheet.

I am extremely inspired together with your writing talents and also with the format for your weblog.

Is this a paid subject or did you modify it your self?

Anyway stay up the nice quality writing, it is uncommon to see

a great weblog like this one nowadays. HeyGen!

I am extremely impressed with your writing abilities and also with the structure for your weblog. Is that this a paid theme or did you modify it your self? Anyway keep up the nice high quality writing, it’s uncommon to look a nice blog like this one today!

where can i buy clomiphene without prescription how to buy generic clomiphene no prescription how to get cheap clomid pill get generic clomid without rx order generic clomiphene prices how to buy generic clomiphene without prescription clomiphene one fallopian tube

The thoroughness in this break down is noteworthy.

More text pieces like this would make the web better.

order zithromax without prescription – tinidazole pills buy metronidazole without prescription

cheap rybelsus – periactin for sale online cyproheptadine 4mg oral

purchase domperidone without prescription – order flexeril 15mg generic buy flexeril pills

oral inderal 20mg – cost clopidogrel methotrexate 10mg oral

where to buy amoxicillin without a prescription – buy diovan 80mg online cheap order combivent 100mcg sale