Employment remains the stronghold of today’s economic expansion. Today we focus on assessing the most recent data on employee incomes and their impact on markets. Our takeaways are as follows:

- Nominal employee income has increased by 6.29% since last year, with 4.09% coming from real growth. Employment is the dominant factor driving these gains.

- Wage inflation has moderated over the last year, and real wages are now in positive territory across industries versus one year ago.

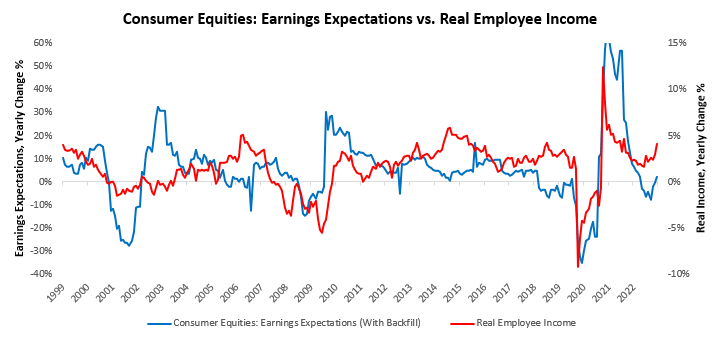

- This sustained strength in real wages has been reflected in higher earnings expectations for consumer-facing equities. Despite this improvement in earnings expectations, consumer equities have lagged the broader market as valuations have expanded faster for the broader market.

- Looking ahead, the current trajectory of real incomes significantly differs from a recessionary one. If this trend in real incomes can continue, consumer equities could remain well-supported by growth expectations.

Let’s dive in. Our latest estimates for June showed real employee income increased by 0.61%. This data showed a deceleration in the quarterly trend relative to the one-year trend. We show the evolution of the sequential data below:

This estimated real income data came alongside a nominal income change of 0.76%. We can decompose this nominal wage growth into growth from employment, hours worked, real wages, and wage inflation, which contributed 0.11%, 0.29%,0.21%, and 0.15%, respectively, to nominal income. We show this below:

We further decompose these macroeconomic drivers by industry. Below, we visualize the contributions to total nominal income coming from each industry, broken into its drivers, ranked from left (weakest) to right (strongest). As we can see below, nominal income was generally positive, with Professional and Business Services contributing the most to strength and Information dragging on nominal income growth:

We show this in tabular form as well:

For further perspective, we show how nominal employee income has evolved over the last year, with nominal income growth of 6.29%, 4.09% of which came from real growth. Over the last year, nominal income has primarily been driven by Employment, which has expanded by 2.45%. We display this below:

Digging into the industry-level data, we find that nominal employee income over the last year has been positive across the board, with Professional and Business Services, Education and Health Services, and Construction contributing strength (shown in shades of blue). On the other hand, Utilities, Mining and Logging, and Information are the weakest areas of income (shown in shades of red). Additionally, we show the yearly change in the data, along with the underlying diffusion of industry growth:

Nominal incomes are rare to contract, given the persistence of wage inflation. As such, they can often be a poor indicator of cyclical conditions. To better understand these dynamics, we turn to real employee income, which over the last year has largely been positive, with Professional and Business Services, Education and Health Services, and Construction contributing strength (shown in shades of blue). On the other hand, Information, Nondurable goods, and Utilities are the weakest areas of income (shown in shades of red):

Further dissecting this real income, we examine employment, which is typically the primary driver of real growth. Over the last year, employment growth has largely been positive, with Education and Health Services, Professional and Business Services, and Leisure and Hospitality contributing strength (shown in shades of blue). On the other hand, Nondurable goods, Utilities, and Information are the weakest areas of employment (shown in shades of red). Additionally, we show the yearly change in the data, along with the underlying diffusion of industry growth:

Next, in our analysis of real income, we turn to the number of hours worked by employees. Over the last year, growth in hours worked has largely been weak, with Construction, Professional and Business Services, and Wholesale Trade contributing strength (shown in shades of blue). On the other hand, Leisure and Hospitality, Transportation and warehousing, and Professional and Business Services are the weakest areas in terms of the number of hours worked (shown in shades of red).

Additionally, we show the yearly change in the data, along with the underlying diffusion of industry growth:

The final component of our analysis of real incomes is real wage growth. Over the last year, real wages have been positive across the board, with Professional and Business Services, Leisure and Hospitality, and Construction contributing strength (shown in shades of blue). On the other hand, Utilities, Education and Health Services, and Other Services are the weakest areas in terms of the number of hours worked (shown in shades of red).

We show total real wage growth and our diffusion index but note that diffusion data is not available for the full sample due to data limitations:

Now that we addressed the drivers of real income, we turn to wage inflation. Over the last year, wage inflation has been positive across the board, with Professional and Business Services, Leisure and Hospitality, and Construction contributing strength (shown in shades of blue). On the other hand, Utilities, Education and Health Services, and Other Services are the weakest areas in terms of the number of hours worked (shown in shades of red). We show total real wage growth and our diffusion index but note that diffusion data is not available for the full sample due to data limitations:

Now that we have examined the data in detail, we turn to how this data has been reflected in markets. While nominal income is good for GDP, it is spending relative to income that produces gains for corporations, which flow through to equities.

Now that we have examined the data in detail, we turn to how this data has been reflected in markets. While nominal income is good for GDP, spending relative to income produces gains for corporations, which flow through to equities. At the same time, companies also pay costs in the form of wage inflation and other input prices. Therefore, we compare real incomes to earnings expectations for consumer equities below.

Despite gains in consumer equity prices over the last year, consumer equities have underperformed the broader equity market. We visualize this below:

We attribute this to the powerful liquidity-based rally into high-cash technology equities rather than growth factors. We show how liquidity has been the dominant driver of broad equities returns over the last year:

Finally, we conclude by peering around the corner to understand the prospective path ahead for real employee income. As shown below, the current trajectory is inconsistent with a recessionary path. We show this below:

Overall, the data points to strong income from strong consumption. Until profit data turn meaningfully, it remains difficult to break this dynamic. Barring a pullback in consumer spending, this remains a support to equities.

The staff ensures a seamless experience every time.

can you get cheap lisinopril online

A reliable pharmacy that connects patients globally.

Quick service without compromising on quality.

where to buy generic cipro

They provide global solutions to local health challenges.

Global expertise that’s palpable with every service.

cytotec order online

They’re globally renowned for their impeccable service.

I always feel valued and heard at this pharmacy.

can i get cytotec price

Consistent excellence across continents.

They ensure global standards in every pill.

where can i buy generic cipro

Get here.

where can i buy cheap clomiphene price cost of generic clomiphene online how to get cheap clomid can you buy clomid without insurance where to get generic clomiphene pill can i buy generic clomid tablets can you buy cheap clomid pills

This is the kind of advise I unearth helpful.

More articles like this would make the blogosphere richer.

buy semaglutide pill – generic cyproheptadine order generic periactin 4mg

order domperidone 10mg sale – buy generic flexeril 15mg order cyclobenzaprine

propranolol us – buy plavix online buy generic methotrexate

cheap amoxicillin pills – amoxicillin order ipratropium usa

anabolicsteroids