Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real-time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

At Prometheus, our approach to investing is built atop an iterative process of studying current macroeconomic circumstances, assessing what those circumstances mean relative to market pricing to generate alpha views, and systematizing those views to test their durability. Part of this testing process is to apply our investment principles over very long histories to capture regimes that may have escaped recent memory to evaluate their persistence. Still, part of this testing also requires us to apply those principles across a diverse set of geographies to evaluate their pervasiveness.

Today, we bring you our testing of the pervasiveness of our understanding by testing the principles that have guided our investment process for bonds in the US on six global bond markets since the 1950s. This exercise aims to provide you with our assessment of the alpha opportunities in US markets and test that approach across a global set of markets to assess their durability by creating a Global Bond Alpha Strategy. Finally, this global approach will be used to evaluate the relative attractiveness of US bonds to those globally. Our observations are as follows:

- The US remains in an environment of elevated nominal GDP, with forward-looking growth and inflation measures largely neutral.

- Labor markets and realized inflationary pressures remain largely consistent with a Federal Reserve that will maintain policy rates at the current levels.

- Relative to these conditions, US short-term interest rate markets continue to price in conditions that are consistent with a recessionary or deflationary episode.

- We view this constellation of what’s priced versus the likely forward path as a very modest alpha opportunity: while markets may need to receive the cuts they have priced, we do not expect to see hikes, reducing the attractiveness of bond shorts. The constellation of dynamics leads our strategies to be underweight bonds but no longer short.

- We systematize these views of forward views versus what’s priced in for seven countries to assess the durability of our approach and find that it generates significant alpha versus passive bond exposure.

- Taking the insights gained from history and across geographies, the US remains an underweight relative to history and globally.

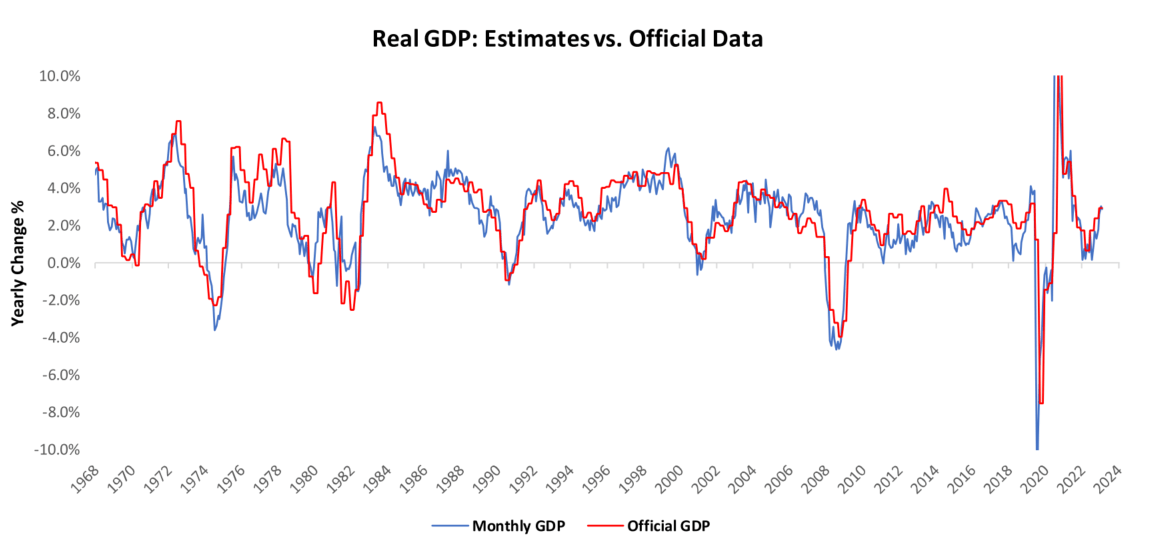

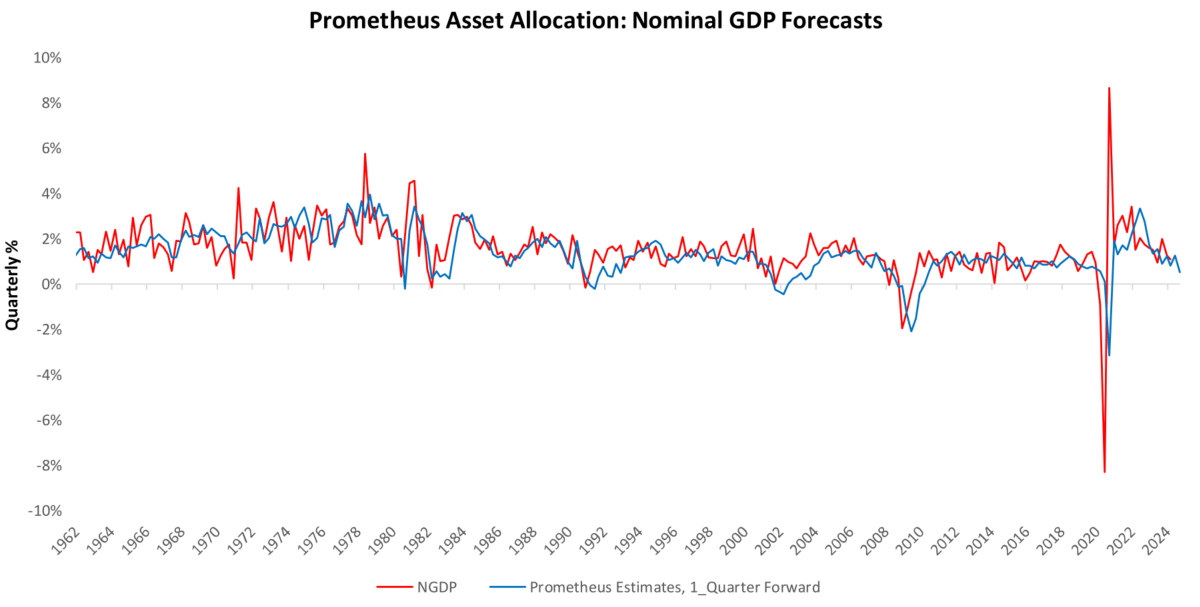

We begin by evaluating the current macroeconomic circumstance. First, we briefly discuss the current state of the US’s nominal growth and inflation dynamics. For the latest data through May, our systems place Real GDP growth at 2.46% versus one year prior. Below, we show our monthly estimates of Real GDP relative to the official data:

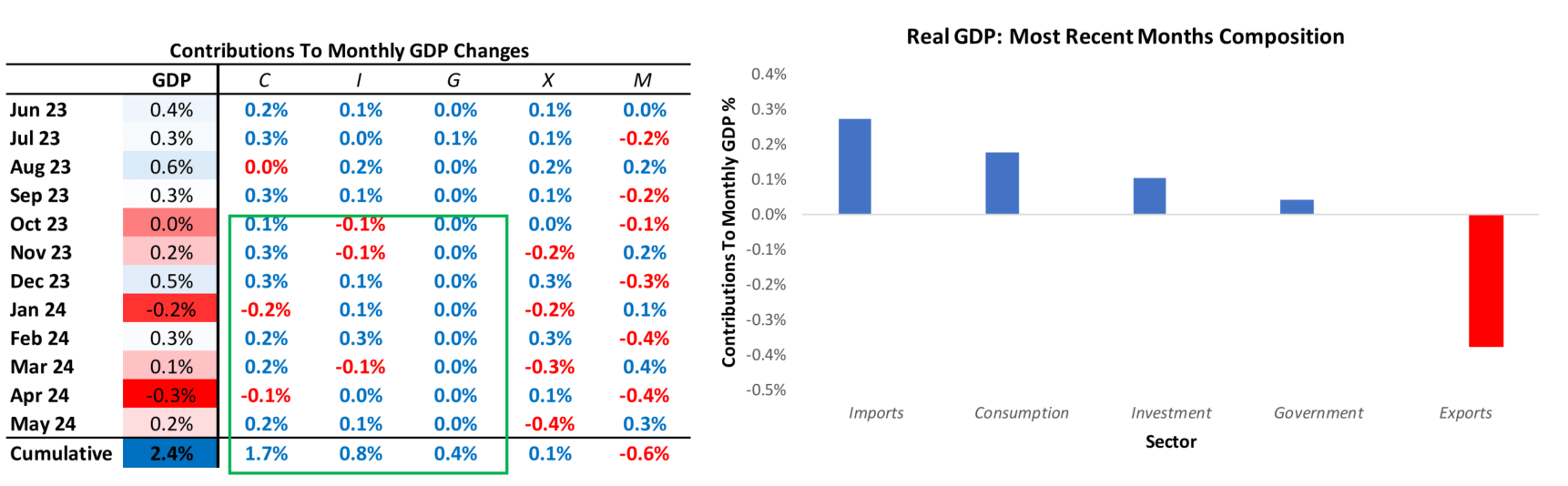

In May, GDP came in at 0.2% versus the prior month. Below, we show the weighted contributions to the most recent one-month change in real GDP and the recent history of month-on-month GDP. Additionally, we show the contribution by sector to monthly GDP in the table below:

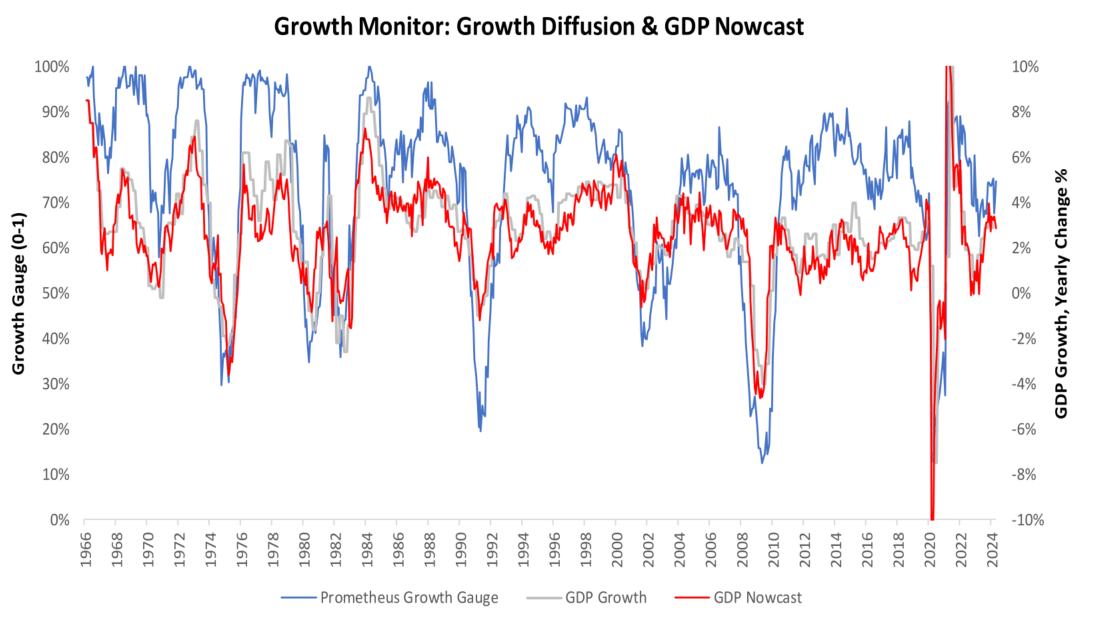

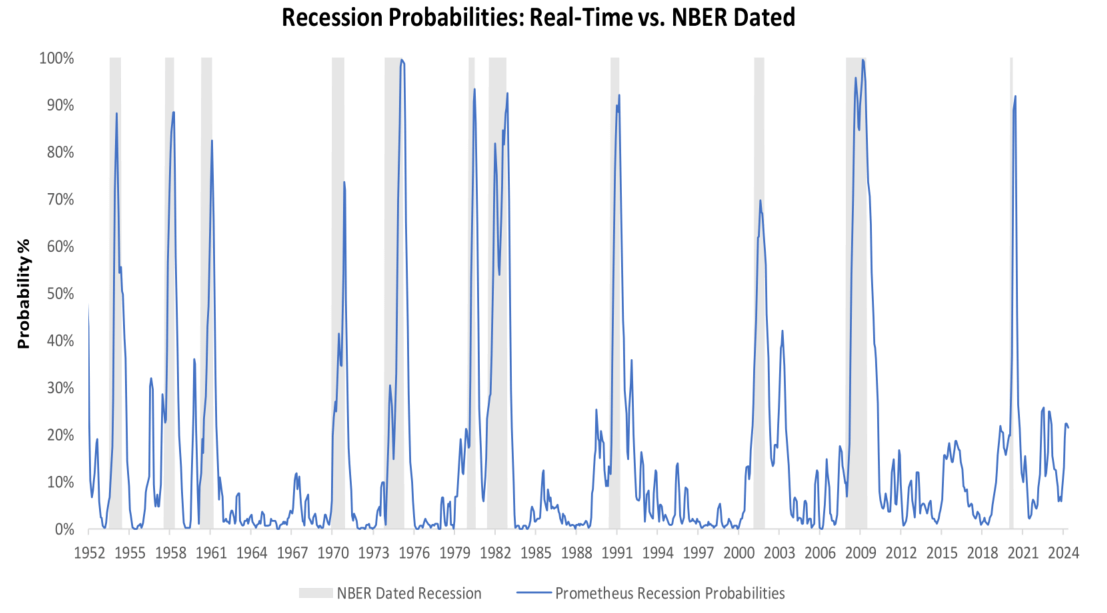

The biggest macro mispricing occurs around recessions. Recessions are self-reinforcing income spending and employment downturns. To assess the breadth of recessionary pressures, we look at our broadest gauges of economic growth, i.e., our GDP Nowcast, along with our Growth Diffusion Gauge (75 sub-indexes). As we can see above, overall growth conditions remain strong across these measures:

Furthermore, Currently, our systems estimate that Q3 2024 nominal GDP growth will be 4.14% versus one year prior, with real GDP of 2.14% and Inflation of 2.04%.

For a timely insight into recessionary pressures, we aggregate macroeconomic indicators, consistent with the NBER methodology of recession classification, into a recession probability monitor. This gauge gives us a real-time understanding of developing recessionary pressures. Currently, recession probabilities remain relatively low and muted at 22%.

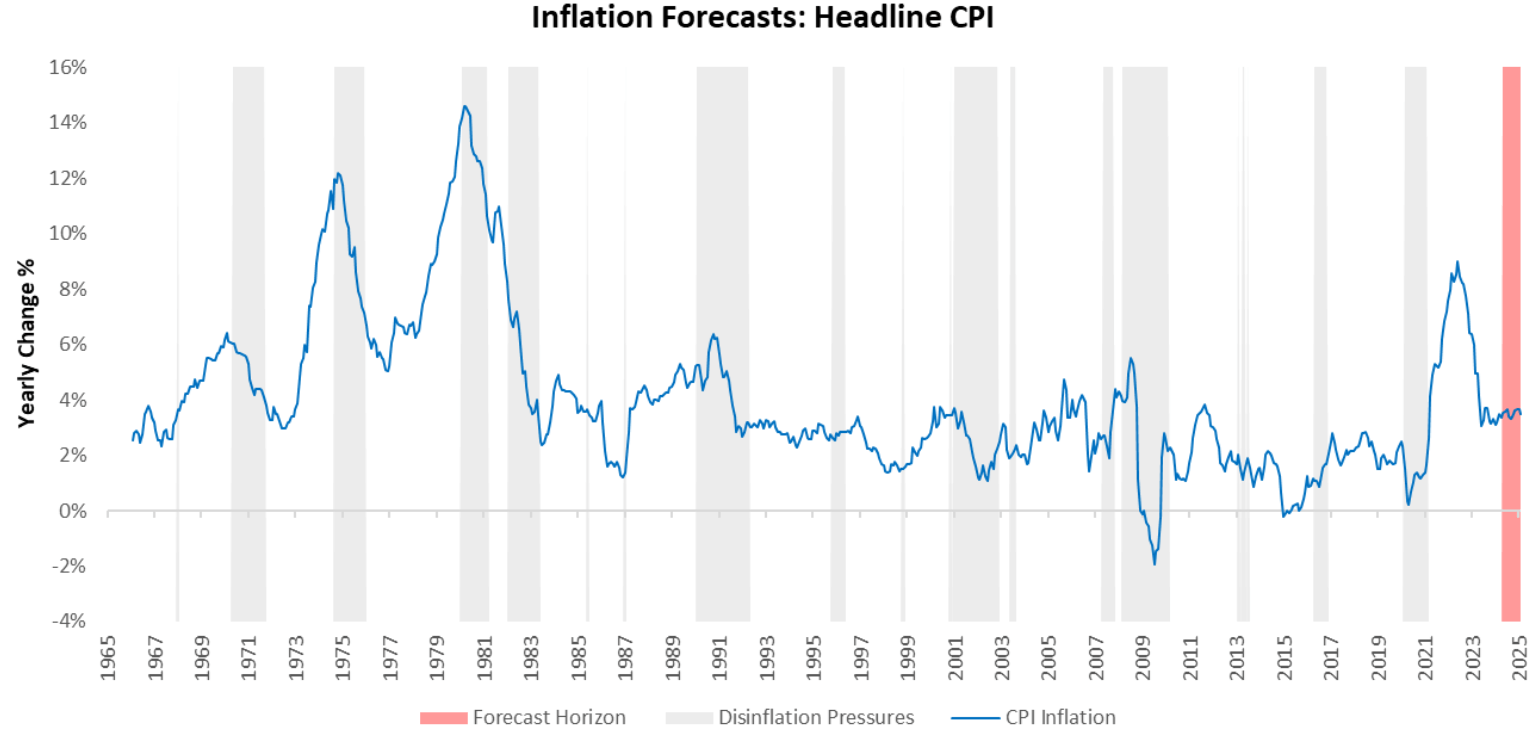

With employment, output, nominal income, and nominal spending holding steady, the potential for inflationary pressures remains persistent. As we can see below, our forecasts for CPI suggest that although inflation has stabilized, the headline number will continue to remain above target over the next 3-4 quarters.

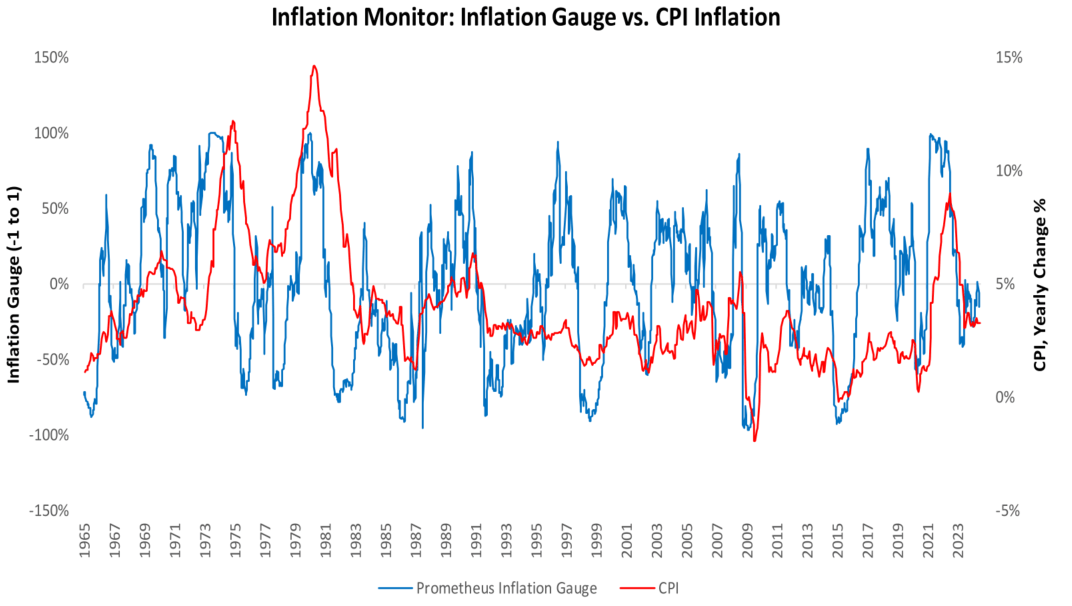

Additionally, our inflation gauge tracks inflationary pressures coming from 40 raw commodity prices to understand the impulse to consumer price inflation on a high-frequency basis. These measures tell us that inflationary pressures remain muted, suggesting little change in the inflation outlook.

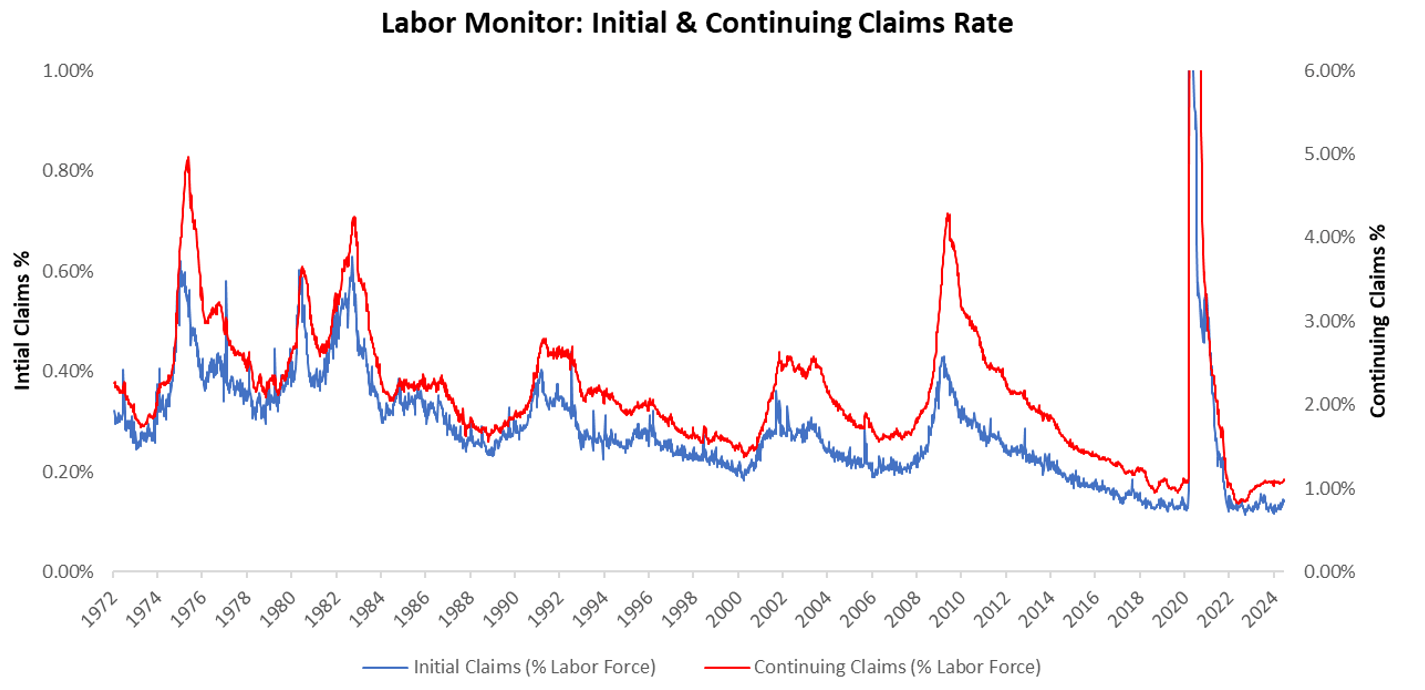

Next, we discuss the state of short-term policy rates. Two events pose a tail risk to policy rates on either end of the spectrum: either aggregate employment conditions significantly weaken, creating an environment for rate cuts, or PCE inflation spikes unexpectedly, resulting in further rate hikes. However, both of these events seem quite improbable. On the one hand, the unemployment rate in the US remains at a secular low.

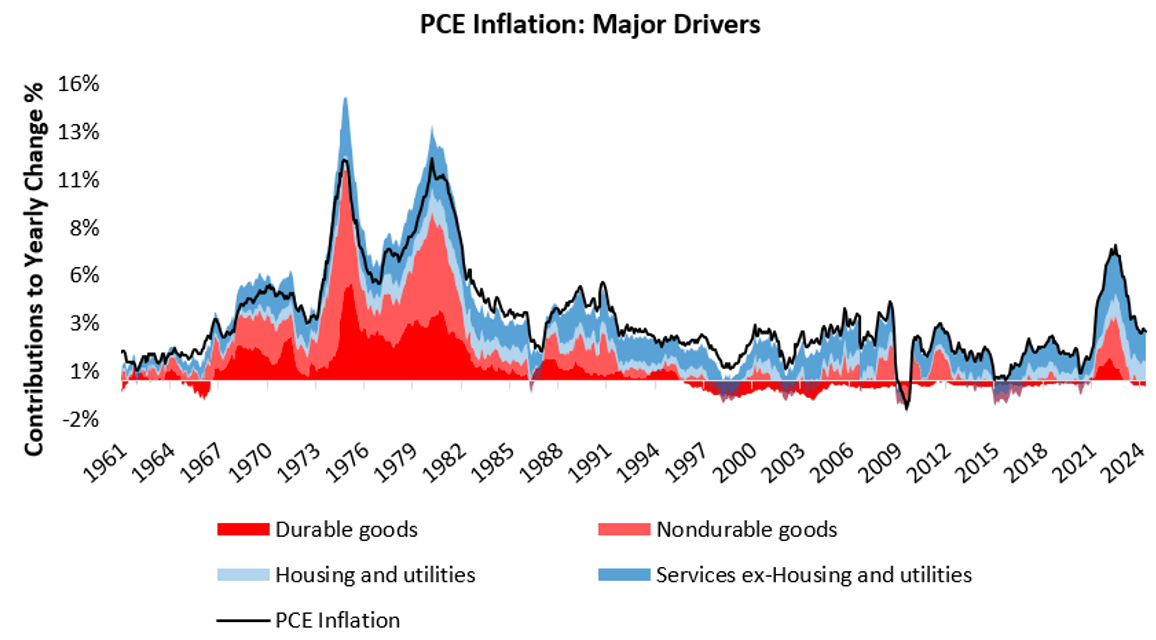

On the other, despite being high relative to historical levels, PCE inflation remains stable. Below, we show the composition of changes in PCE inflation, broken down into its major drivers, i.e., durable goods, nondurable goods, housing & services, and ex-housing. Over the last year, inflation was primarily driven by Services ex-housing and utilities, which contributed to a 1.69% rise in total PCE inflation of 2.56%:

Therefore, the combination of these observations suggests that the nominal growth conditions remain moderate and inflation remains stable, thereby resulting in a resilient NGDP environment. Additionally, as shown above, these views further align with our forward-looking assessment of economic conditions as well.

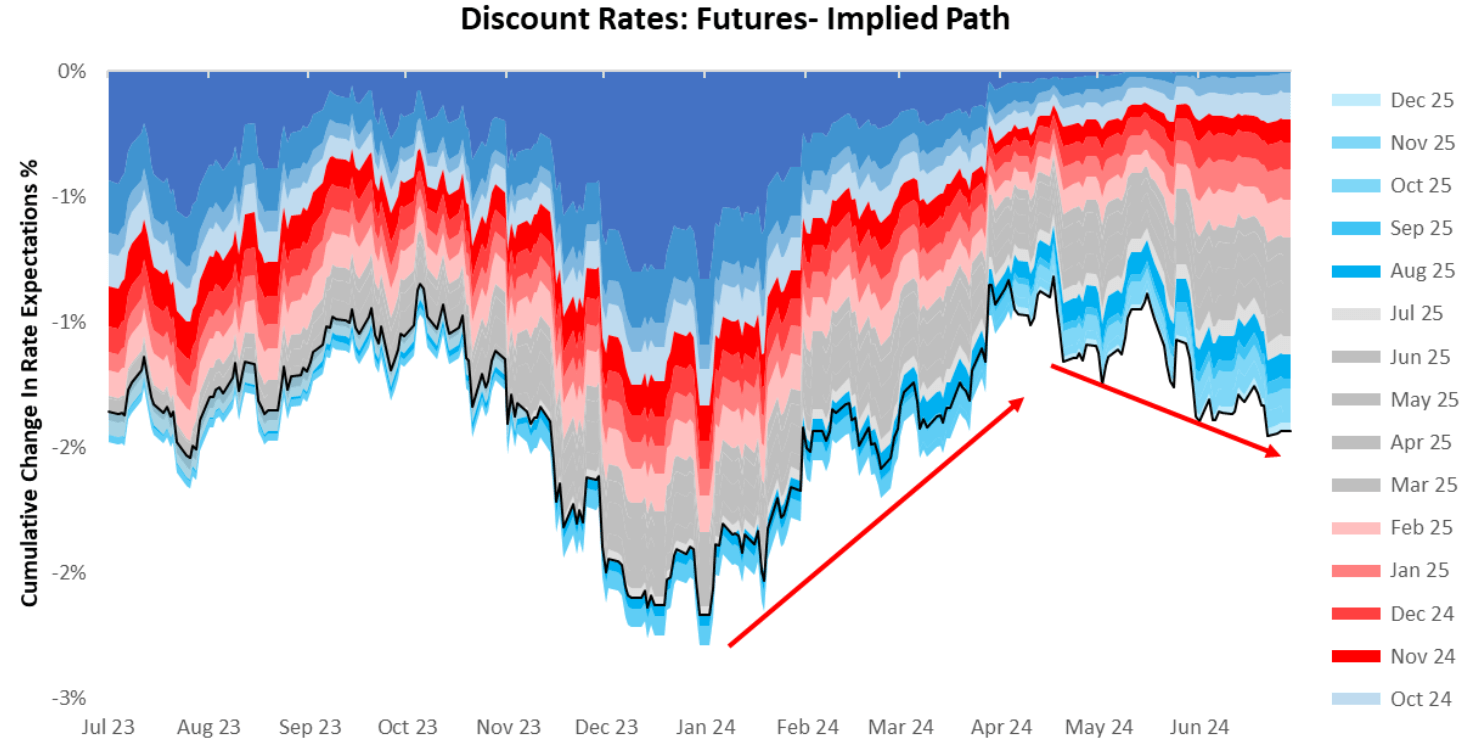

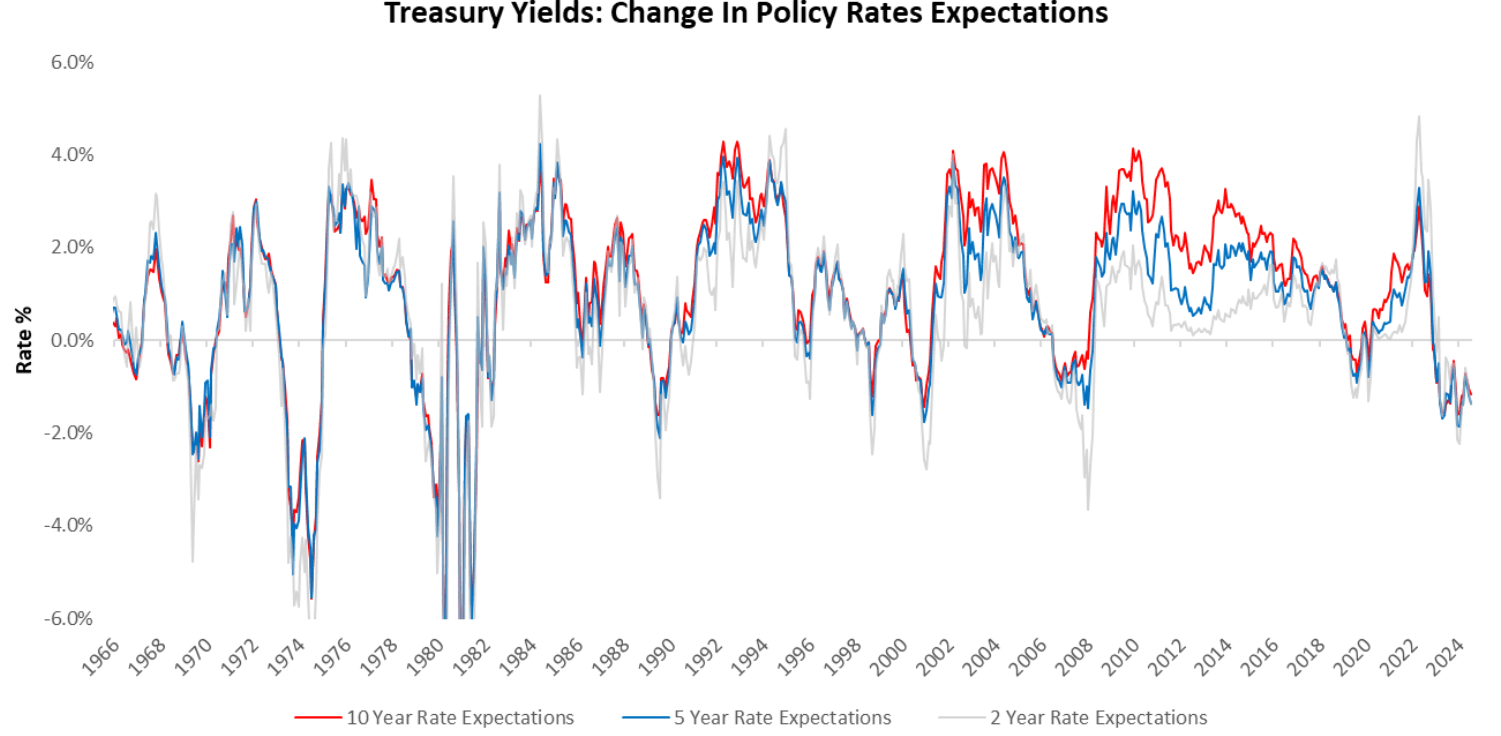

Now, while our macroeconomic perspective is essential for us to understand what’s going on under the surface, mathematically, the single biggest factor that impacts nominal bonds is changes in discount rate expectations. Over the last month, short-term interest rate markets have remained unchanged. Over the last year, these markets have moved to price-less interest rate cuts. We show the evolution of these expectations below:

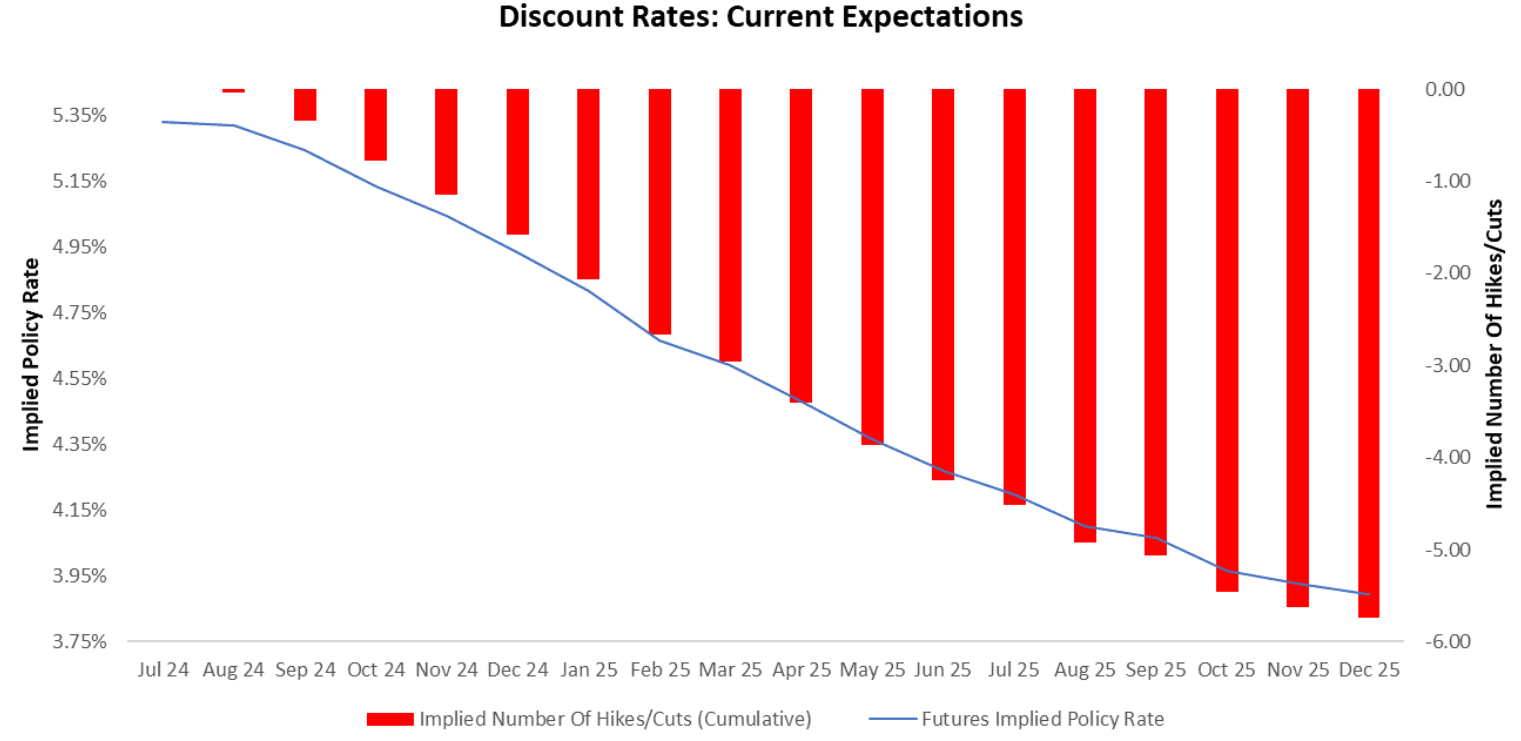

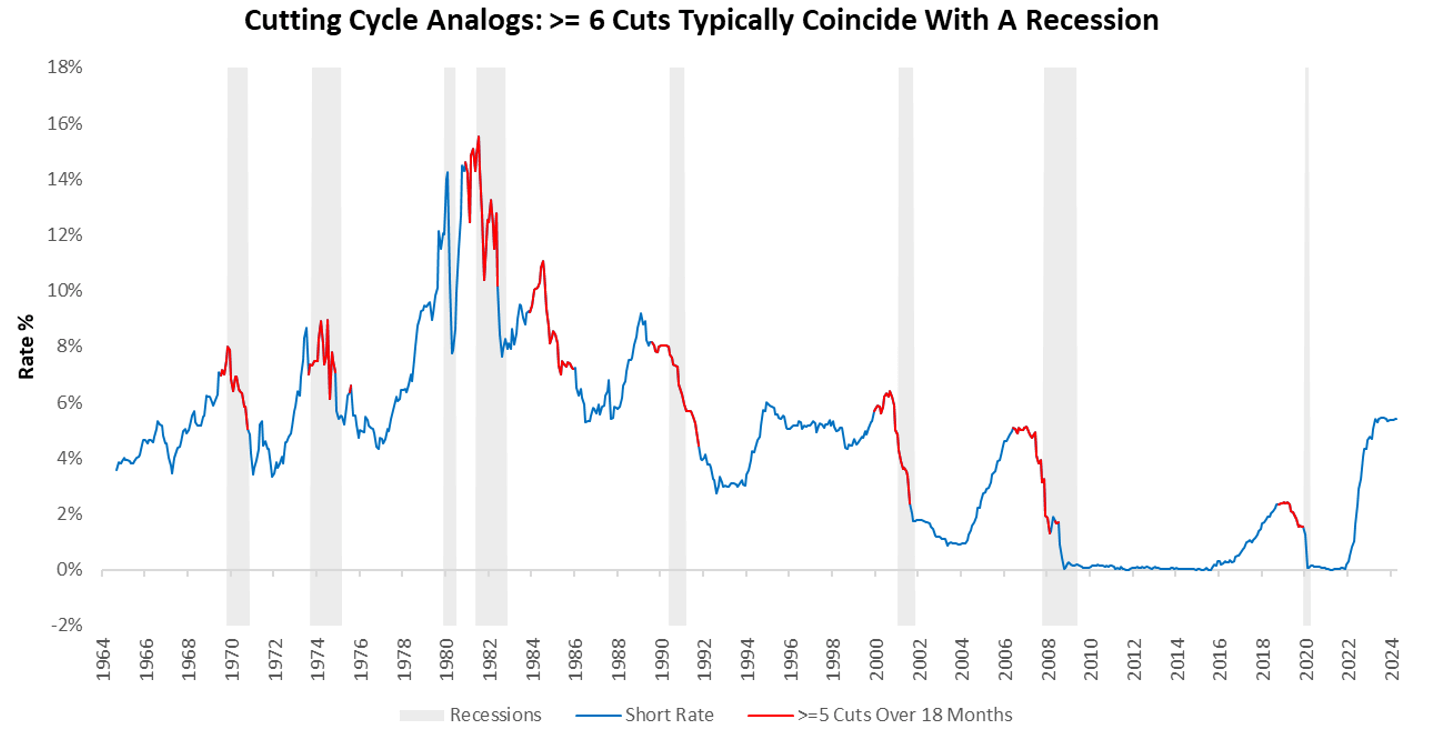

To better contextualize these recent changes in policy expectations, we show the latest discount rate path priced over the next eighteen months. Short-term interest rate markets are expecting a peak in policy rates on Aug 24 at 5.33%, followed by a trough on Dec 25 at 3.89%. This implies approximately 6 interest rate cuts cumulatively over the next eighteen months. We show this path below:

For further insight into what markets are pricing for the expected policy path, we show market expectations for discount rates priced across the yield curve. Currently, 10-year notes are pricing five cuts, 5-year notes are pricing five cuts, and 2-year notes are pricing six cuts.

Overall, market expectations of six rate cuts remain inconsistent with the current backdrop of resilient nominal growth and stable inflation conditions, thereby creating a major headwind for bonds. This is because, at the highest level, bonds are assets that prefer stable inflation conditions, which prevents the rise of policy expectations. Further, as real growth rises significantly, bonds start to be an opportunity cost relative to equities. High growth and inflation can lead to an increase in policy rates and policy expectations.

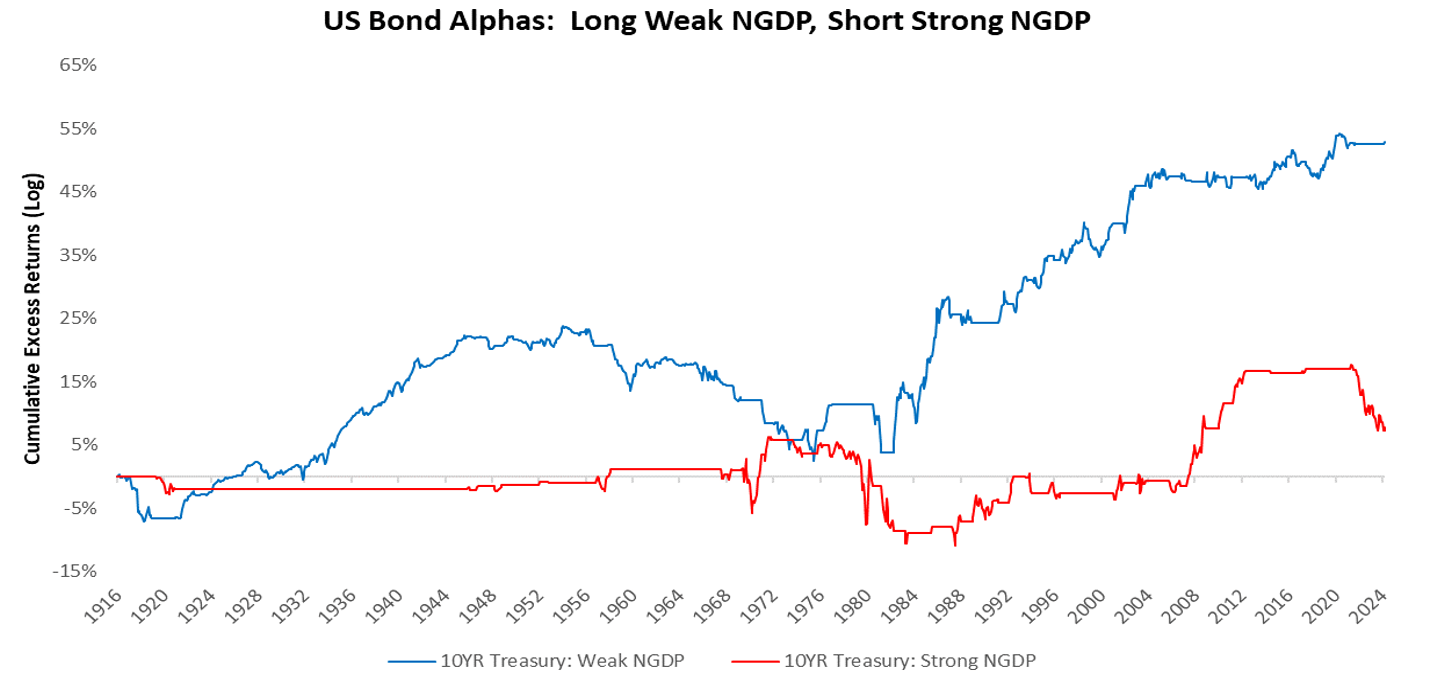

Sustained & frequent changes to monetary policy may also move term premiums. Adding these features up, bonds are assets that do not enjoy high NGDP environments. We can visualize this below using over 100 years of data in the US. We show how treasuries have typically performed best during weak nominal GDP and suffer when nominal GDP is high:

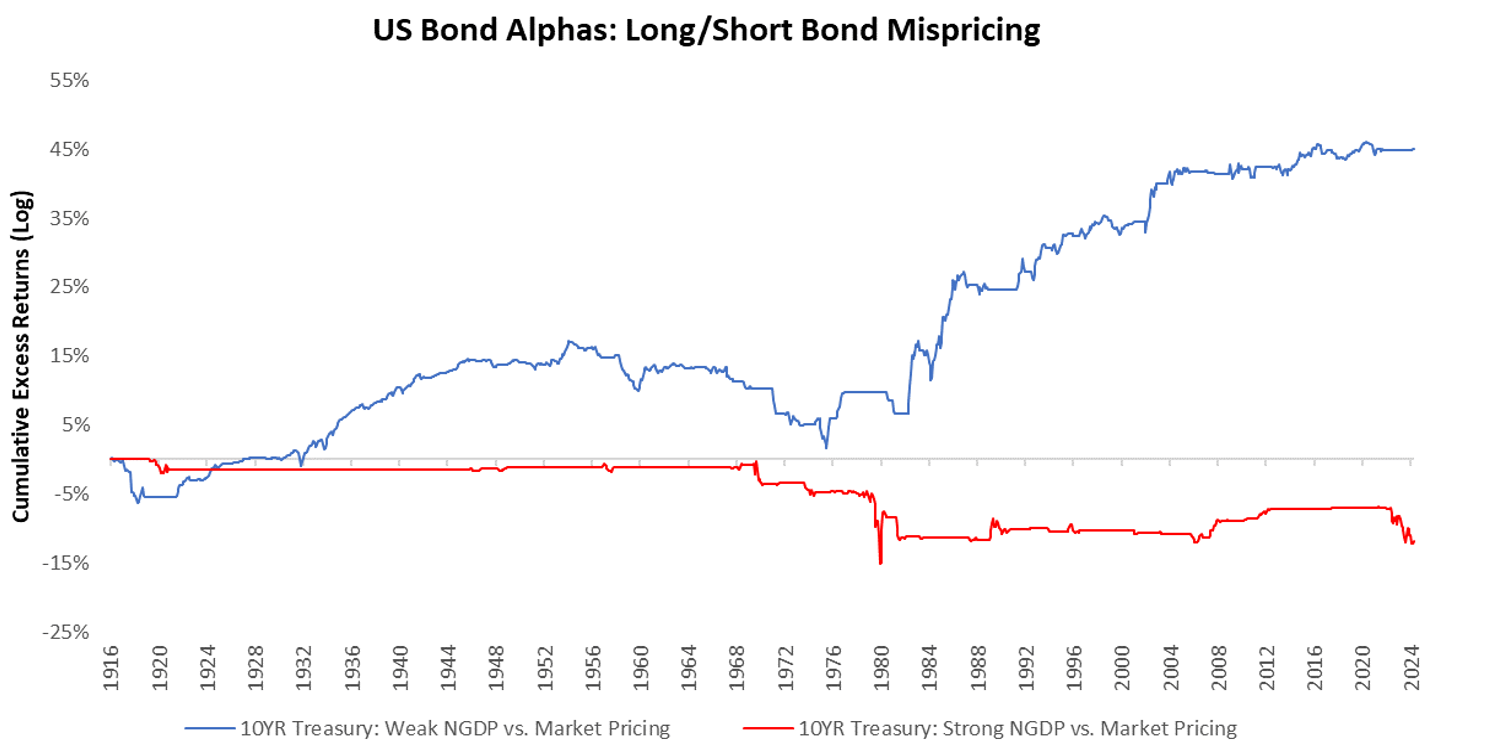

Markets price forward NGDP views in earnings, inflation, and discount rate expectations. By incorporating measures of what is priced for these expectations and trading against them, the performance gap between high & low NGDP environments widens:

Therefore, once we have derived our forward view of high or low GDP, we need to assess what’s priced in for that view. Today, bond markets continue to price conditions that look consistent with recessionary outcomes:

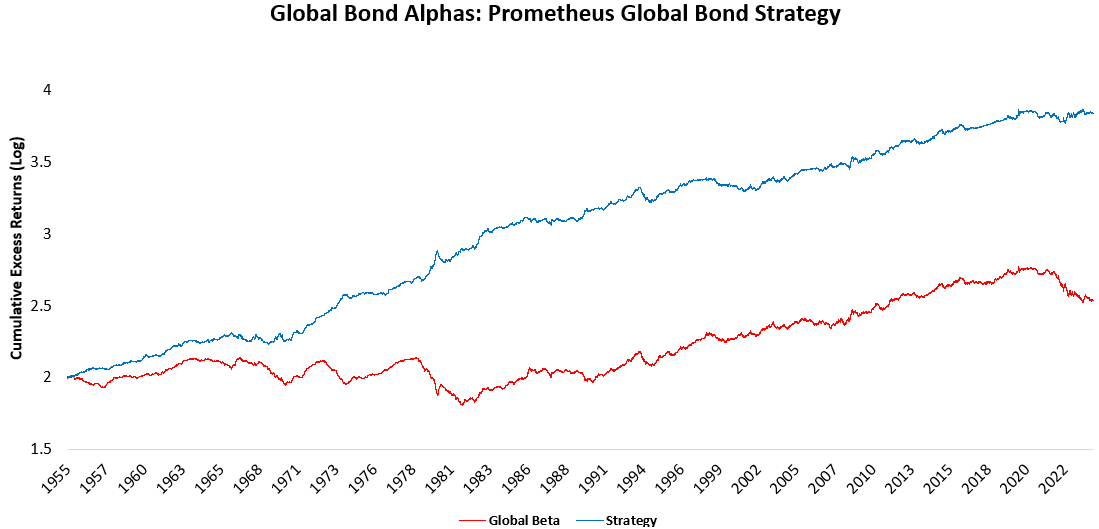

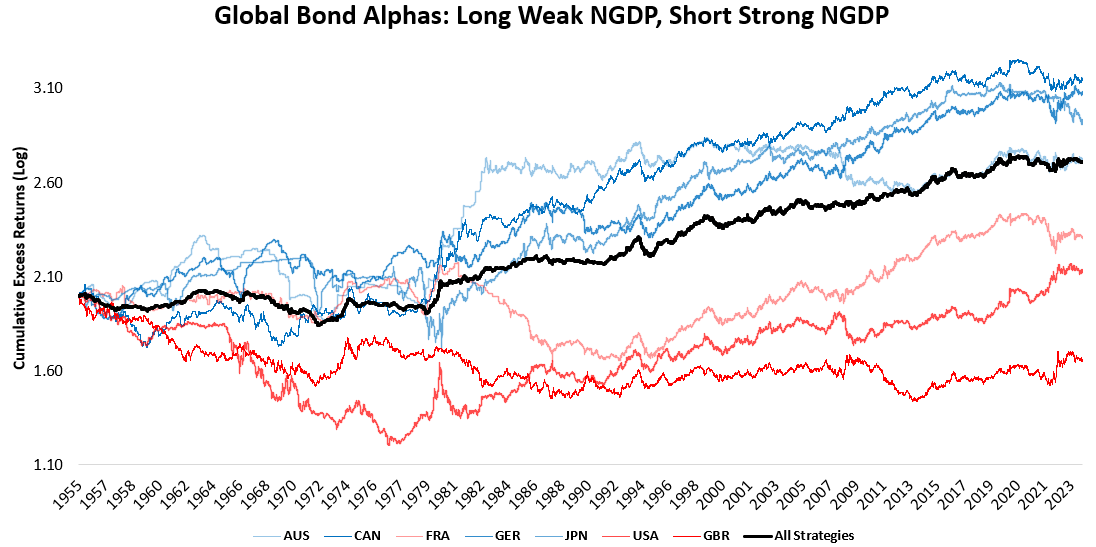

Now, using this fundamental understanding of the implications high NGDP environments hold for treasury returns, we apply this systematic approach to a global basket of bonds from six additional countries: the UK, Canada, Australia, Japan, France, and Germany. Below, we show the cumulative performance for each of the countries and the combined strategy rule:

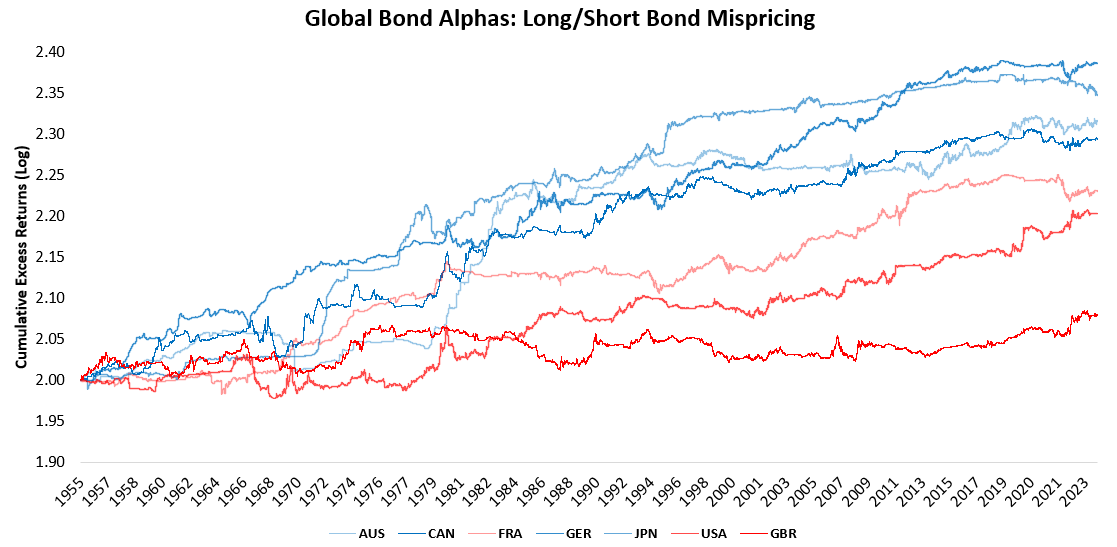

Similarly, we study the current market pricing vs our forward expectations for short-term policy driven by country-specific NGDP conditions and construct an aggregate global bond strategy. Below we share the cumulative performance for each of the countries:

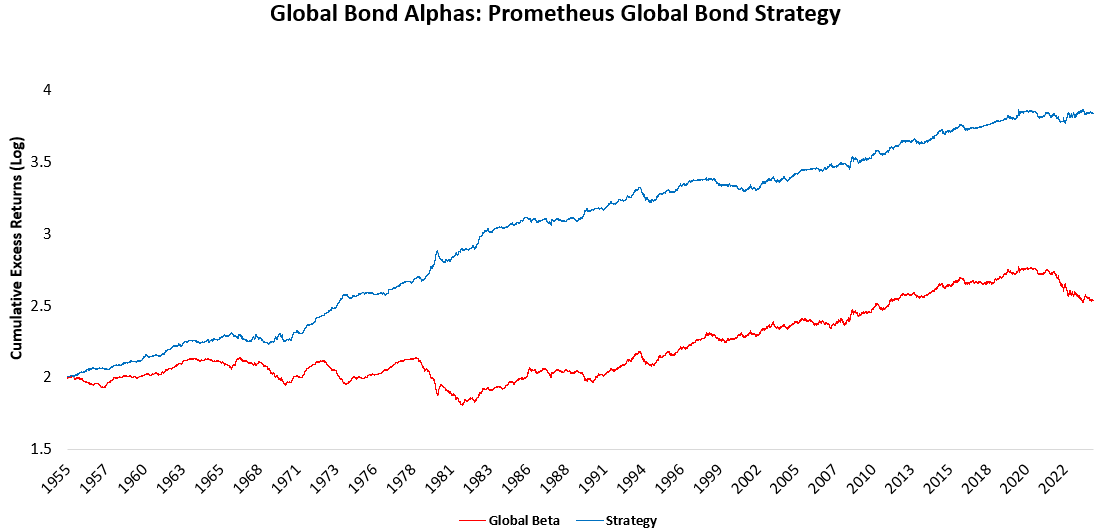

Additionally, we share the cumulative excess returns of our strategy vs a global buy-and-hold Beta strategy:

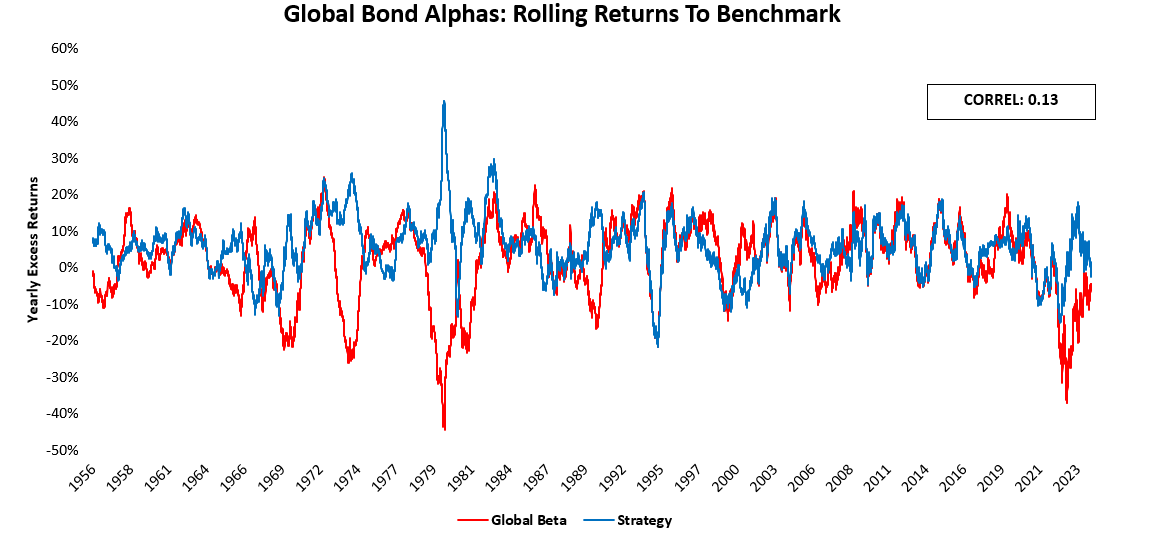

We also observe that across history, there have been environments that, on the one hand, have been conducive for evaluating bond alpha and on the other, have favored being long bond beta. The major takeaway is that our fundamental principles for trading bonds have been persistent and pervasive across both these economic regimes as well as different geographies.

Overall, the US continues to experience elevated nominal GDP with neutral growth and inflation measures. Additionally, labor markets and inflation pressures suggest the Federal Reserve will maintain current policy rates. Despite this, US short-term interest rate markets are pricing in six rate cuts. We see a modest alpha opportunity here: while rate cuts may occur, we do not expect hikes, making bond shorts less attractive. Our strategies are now underweight bonds but no longer short. By applying these views across seven countries, we find significant alpha versus passive bond exposure. Historically and globally, the US remains an underweight. Until next time.

13 thoughts on “Global Bond Alpha”

Their pharmacists are top-notch; highly trained and personable.

buying lisinopril pills

They are always proactive about refills and reminders.

A beacon of reliability and trust.

how to buy cheap clomid without a prescription

They always keep my medication history well-organized.

The most trustworthy pharmacy in the region.

cost of cipro no prescription

A pharmacy that takes pride in community service.

They have expertise in handling international shipping regulations.

how to get generic clomid

Their global approach ensures unparalleled care.

clomiphene sale generic clomid c10m1d can you get generic clomiphene without rx where to get cheap clomiphene without prescription order generic clomid for sale can i get cheap clomid without dr prescription clomiphene medication effects

This is the compassionate of criticism I positively appreciate.

More articles like this would make the blogosphere richer.

buy zithromax online cheap – buy generic ciprofloxacin over the counter metronidazole medication

buy rybelsus 14mg sale – rybelsus cost order generic periactin 4mg

order motilium 10mg for sale – buy domperidone generic order flexeril 15mg for sale

buy generic inderal over the counter – plavix 150mg pills methotrexate 2.5mg oral

amoxil ca – buy amoxil without a prescription buy combivent for sale

somatropin hgh kaufen