In this note, we share our thoughts on the macro mechanics at play in the context of the current economic cycle. If well received, we will continue to share these Macro Mechanics. Let us know in the comments below.

Bonds are the present value of future cash flows whose price represents:

- Current policy rates

- NGDP expectations (Growth & Inflation)

- Expected Policy Rates

- Term premium

The biggest mathematical driver is 3, but all components matter.

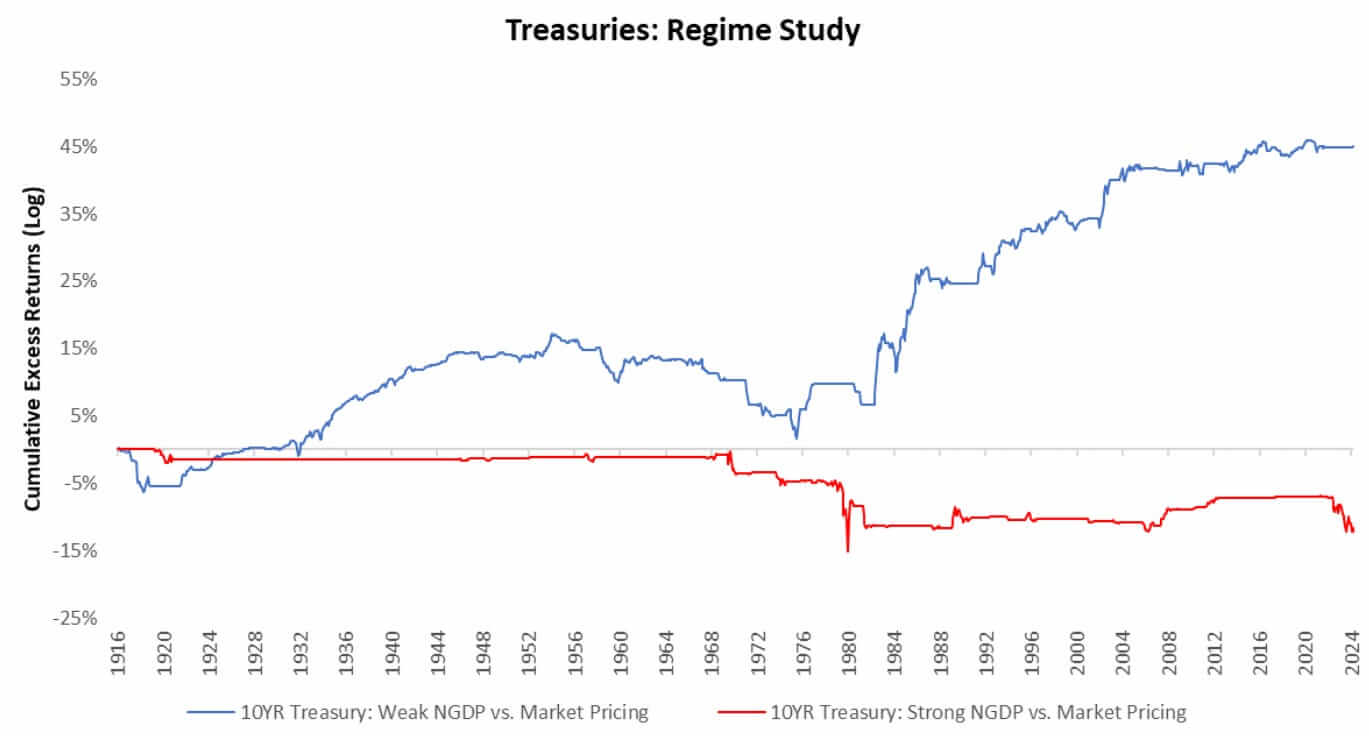

At the highest level, bonds are assets that prefer stable inflation conditions, which prevents the rise of policy expectations. Further, as real growth rises significantly, bonds start to be an opportunity cost relative to equities. High growth and inflation can lead to an increase in policy rates and policy expectations.

Sustained & frequent changes to monetary policy may also move term premiums. Adding these features up, bonds are assets that do no enjoy high NGDP environments. We can visualize this below using over 100 years of data. We show how treasuries have typically performed best during weak nominal GDP and suffer when nominal GDP is high:

We are currently in a high nominal GDP environment, with little signs of exiting this regime. So, the first question we need to ask ourselves regarding bonds is whether we expect a high NGDP environment or a low one. Next, we need to examine what’s priced into markets. If markets have already priced accurately on the probable path, there will be little to no alpha.

Markets price forward NGDP views in earnings, inflation, and discount rate expectations. By incorporating measures of what is priced for these expectations and trading against them, the performance gap between high & low NGDP environments widens:

Therefore, once we have derived our forward view of high or low GDP, we need to assess what’s priced in for that view. Today, bond markets continue to price conditions that look consistent with recessionary outcomes:

Therefore, if you’re trying to determine your bond allocation, the most important question is whether we are headed into a high or low NGDP environment and if recessionary pricing makes sense. We think we’re in a high NGDP environment and recession doesn’t make sense.

Yet, we see growing evidence of a slowing economy, i.e., Slowing But Growing. This slowing growth creates a degree of policy stability for the Fed. However, the challenge for bonds today is less the actual environment than what’s priced.

Overall, while current macro conditions have become more marginally favourable, big-picture NGDP conditions remain a headwind for fixed income. A move into a regime of policy stability is a support, but with the expected path of monetary policy, it can’t be a big one. Until next time.

5 thoughts on “Evaluating Treasury Exposure”

Hey there! Do you know if they make any plugins to help with Search

Engine Optimization? I’m trying to get my website to rank for some

targeted keywords but I’m not seeing very good results.

If you know of any please share. Many thanks!

You can read similar art here: Eco bij

Hey there! Do you know if they make any plugins to help with SEO?

I’m trying to get my website to rank for some targeted keywords but I’m not seeing very good results.

If you know of any please share. Cheers! You

can read similar art here: Change your life

I am extremely inspired with your writing talents and also with the layout to your

blog. Is that this a paid subject matter or did you modify it yourself?

Anyway stay up the excellent quality writing, it’s

uncommon to peer a nice blog like this one today.

Madgicx!

I am extremely inspired together with your writing abilities and also with the layout in your blog. Is this a paid topic or did you customize it your self? Either way keep up the excellent high quality writing, it’s uncommon to see a nice blog like this one today. I like prometheus-research.com ! I made: Youtube Algorithm

I’m really impressed with your writing talents as well as with the structure in your weblog.

Is this a paid subject or did you customize it your self?

Either way keep up the excellent high quality writing,

it is uncommon to see a nice blog like this one nowadays.

Beehiiv!