Today, we will provide updates on our ETF Strategy. Our ETF Strategy algorithmically employs our systematic analysis of the US economy and financial markets to create a rules-based, quantitative portfolio. At Prometheus, we focus on understanding the underlying mechanics that drive market environments. We use fundamental economic and high-frequency financial data to understand these macroeconomic environments and codify how to best trade markets. This process creates a robust portfolio solution that attempts to provide high return/risk characteristics and high percentage positive ratios at the portfolio level, regardless of the economic environment. Subscribe below so that you never miss out on our systematic insights into markets and portfolio strategy:

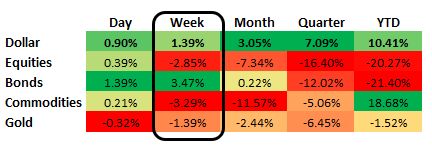

Over the last week, markets have continued to price tightening liquidity conditions, but now with a deflationary tilt. The Dollar continued to power ahead, alongside US Treasuries. Equities and Commodities suffered significant losses, telling us that markets were moving aggressively toward pricing in falling growth expectations.

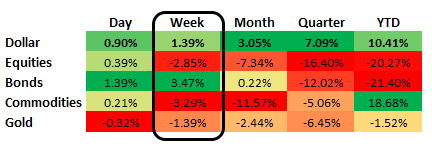

In line with these moves, our market regime monitor continues to show a dominance of tightening liquidity conditions in financial market pricing. With the Fed staying the course of tightening financial conditions, we will likely remain in the territory for a while.

The market-implied pricing of tightening liquidity conditions is currently extremely strong in markets. Over more extended periods, this dynamic is unsustainable. These periods tend to be unnatural for a capital-driven economy as they imply that the return on assets relative to cash is negative. This dynamic cannot hold for a protracted period as this would indicate a halt to capital formation in financial markets, thereby creating a self-reinforcing spiral downwards and lower. However, these periods can last longer than most traditional asset allocations can remain solvent, and therefore risk management in this environment becomes paramount.

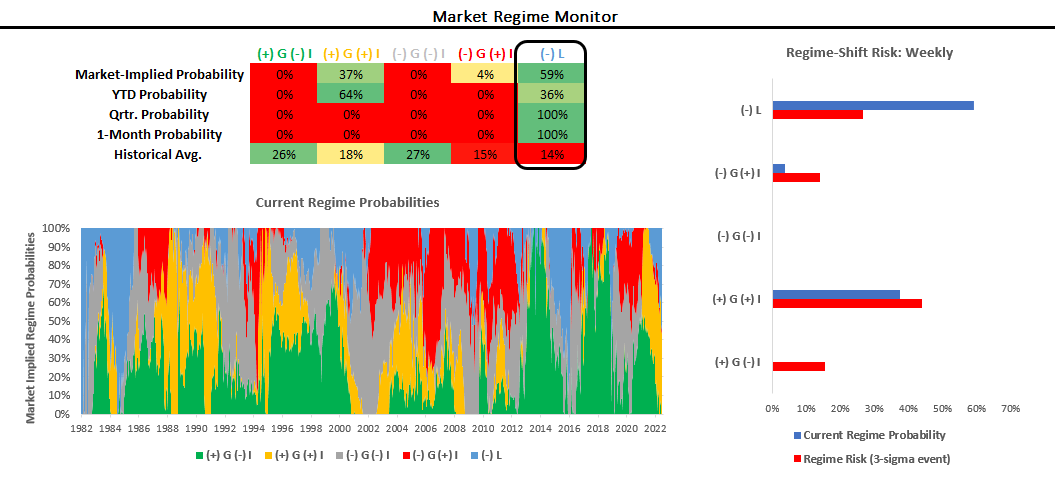

As we mentioned earlier, markets moved primarily to price-falling economic growth conditions this week. These market moves came alongside weak economic data and hawkish commentary from the Federal Reserve. Our systems continue to show there is likely to be a further deterioration in economic growth data (PMIs in particular):

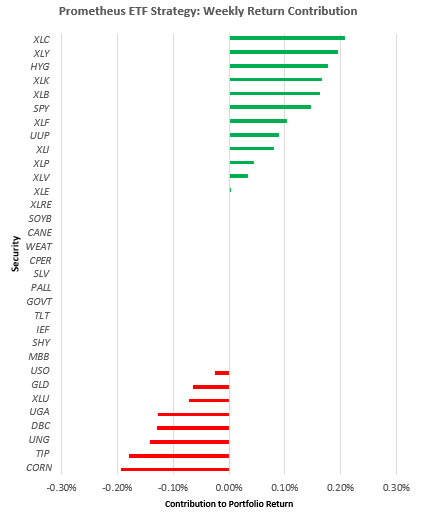

Given these considerations about slowing economic growth, our systems have become increasingly cautious about commodities. As we discussed last week, Commodity momentum has waned, and the pass-through to inflation will decrease. Resultantly, our systems took down our ETF Strategies gross exposure to Commodities this week, which helped the portfolio. This week, the ETF Strategy again performed well, with 60% of positions in positive territory. Equity & Credit shorts played a significant role in this performance:

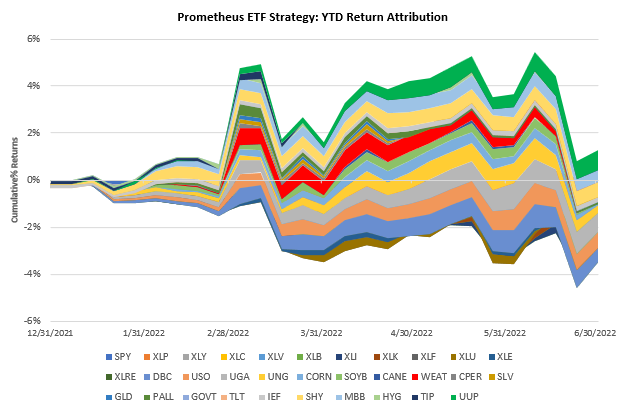

These portfolio moves have resulted in an unleveraged gain of 0.5% (while equities are down about the same), and an application that targets returns akin to the S&P 500 would be up over 1%. Below, we show the cumulative year-to-date performance:

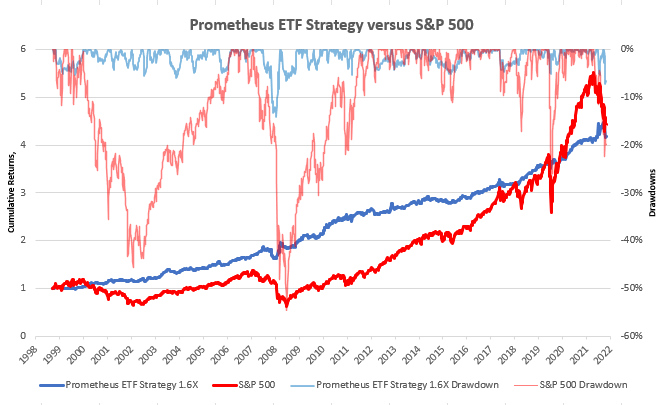

As we can see above, last week led to a significant hit in cumulative returns. These losses could have been mitigated by using stop losses, and we’re developing best practices to communicate these to you soon. Nonetheless, our system’s primary job is to prevent large capital drawdowns and compound returns regardless of where we are in the economic cycle. Cumulative, full-sample backtest performance of the strategy continues to attest to this, especially when compared to the S&P 500:

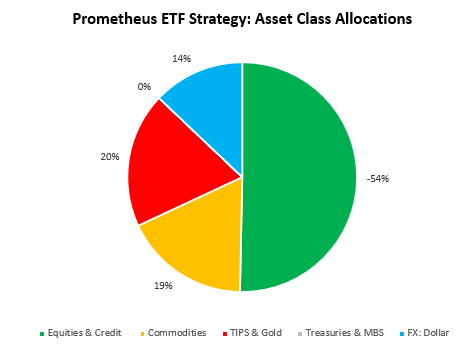

Next week, our systems are again setting up tightening liquidity, with long positions in the Dollar and short positions in Equity & Credit as the primary positions. We show how our systems are positioning the ETF Strategy at the asset class level below:

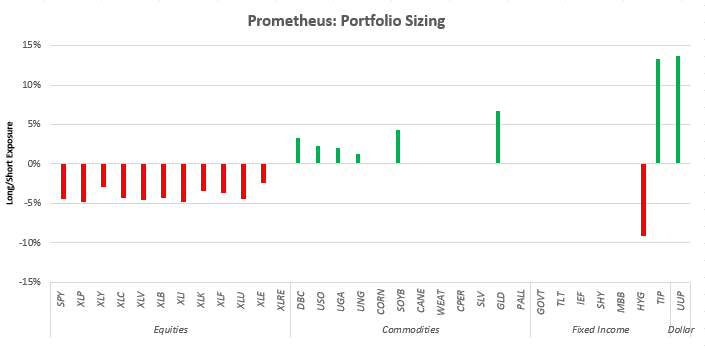

This asset-class level exposure comprises the following allocation at the security level:

-

Stocks: SPY (-5%), XLP (-5%), XLY (-3%), XLC (-5%), XLV (-5%), XLB (-5%), XLI (-5%), XLK (-4%), XLF (-4%), XLU (-5%), XLE (-3%)

-

Commodities: DBC (4%), USO (3%), UGA (2%), UNG (2%), SOYB(5%), GLD (7%), HYG (-10%), TIP (14%)

-

Fixed Income: HYG (-10%), TIP (14%

-

Dollar: UUP (14%)

We show this visually below:

Remember, we’re in a tightening liquidity environment, which is typically kryptonite for economic activity and assets. It may not last long, but our primary concern right now is to preserve capital (and hopefully profit), and when policymakers are forced to react, we will reverse our positioning. Until then, stay nimble.

Good day! Do you know if they make any plugins to help with Search Engine

Optimization? I’m trying to get my site to rank for some targeted keywords but I’m not seeing very good results.

If you know of any please share. Thank you! I saw similar art here:

Eco wool

Hello there! Do you know if they make any plugins to

assist with Search Engine Optimization? I’m trying to get my site to rank for some targeted keywords but I’m not

seeing very good success. If you know of any please share.

Thank you! I saw similar art here: Change your life

I am extremely inspired with your writing abilities and

also with the structure to your blog. Is that this a

paid topic or did you customize it yourself?

Anyway keep up the excellent quality writing, it’s rare to look a great weblog like this one nowadays.

Beacons AI!

I’m really impressed with your writing talents as neatly

as with the layout for your weblog. Is that this a paid topic or did you customize

it your self? Anyway keep up the nice high

quality writing, it’s rare to peer a great weblog like this one

these days. Lemlist!

I’m really inspired with your writing talents as well as with the layout for your weblog. Is this a paid subject or did you customize it yourself? Either way stay up the nice quality writing, it is rare to peer a great blog like this one these days. I like prometheus-research.com ! It’s my: Leonardo AI x Midjourney