Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

We scan through the Treasury market to assess risk vs reward. So far this year, the aggregate Treasury market has had a slow start to the year after a great Q4 2023. We analyse:

While it has been a slow start recently, November and December contributed to a significant improvement in the overall market trend:

We show how this rally has largely come from discount rate expectations, i.e., markets very aggressively priced in a series of interest rate cuts in Q4 last year, which has been the dominant driver of treasury returns:

This dynamic is also consistent with the relatively muted nature of breakeven movements. Below, we show how break-evens have remained somewhat stable as spot inflation pressures have subsided:

Therefore, short-rate expectations are firmly in the driving seat relative to other macro variables. This short-rate pricing has driven the rally last year and the weak performance this year. Below, we show how short-rate expectations for cuts have moderated:

The most important input to get right today is the short-rate path when assessing the future bond prospects. This requires an understanding of nominal growth, which includes real growth and inflation. Using a comprehensive high-frequency assessment (130 indicators), growth conditions remain largely positive, and inflationary pressures are roughly flat:

The combination of the dynamics creates a stable inflation environment. The most persistent of inflationary pressures remains the gap between nominal spending and interest expense. The tighter the gap between these two, the less credit capacity and inflationary potential:

Aggregating these various data points, our leading measures suggest that inflationary pressures are roughly neutral, which suggests a continuation of current inflation trends rather than a breakdown:

Given a raw data approach, we think the short-rate bias should be towards remaining at around current levels for longer. However, monetary policy doesn’t operate programmatically. Furthermore, markets continued to price in outcomes more consistent with previous cutting cycles, via an inverted yield curve:

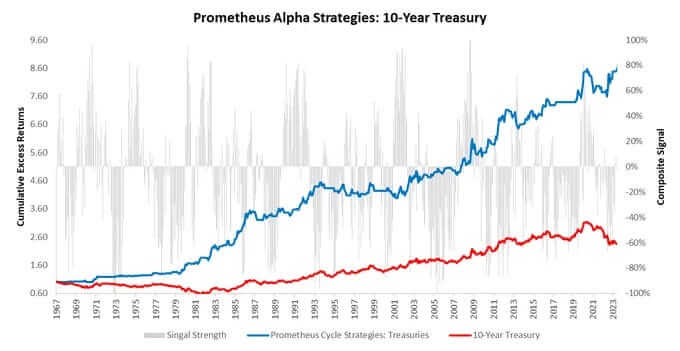

Now, while our fundamental tracking of conditions and what’s priced into markets largely suggest mispricing in markets, we think it is crucial to recognize that once a cutting cycle is underway, it is not a trend to fight. Easing generates the majority of Treasury excess returns:

Overall, we think Treasuries offer the opposite conditions that we see in equities- high alpha opportunities to fade excessive pricing of cuts, with poor dynamics for beta capture. Alpha generations will likely continue to come from the mean reversion of short-rate pricing:

While the positive trend in equities is one not to fight, the positive trend in treasuries remains problematic. We continue to see alpha opportunities in treasuries, skewed to the short side. Beta becomes attractive during the cutting cycle. Until next time.

Hey! Do you know if they make any plugins to assist with Search

Engine Optimization? I’m trying to get my website to rank for some targeted keywords

but I’m not seeing very good success. If you know of any please share.

Appreciate it! You can read similar blog here: Wool

product

Hello! Do you know if they make any plugins to

help with Search Engine Optimization? I’m trying to get my website to rank

for some targeted keywords but I’m not seeing very good success.

If you know of any please share. Cheers! You can read similar art here:

Code of destiny

I am extremely inspired along with your writing skills as well as

with the layout for your blog. Is that this a paid subject matter or did you customize it your self?

Either way stay up the excellent quality writing, it’s uncommon to see a

nice weblog like this one today. TikTok ManyChat!

I am extremely impressed with your writing talents as well

as with the format on your blog. Is this a paid subject matter or did you

modify it your self? Either way keep up the excellent high quality writing,

it is rare to see a nice blog like this one today. LinkedIN Scraping!

I’m really impressed with your writing abilities as smartly as with the structure on your blog. Is this a paid subject or did you modify it your self? Anyway keep up the excellent quality writing, it’s rare to look a nice weblog like this one these days. I like prometheus-research.com ! It’s my: Blaze ai

I am really inspired together with your writing abilities and also with the

structure to your blog. Is that this a paid theme or did you

modify it your self? Anyway keep up the nice quality writing, it is rare to look

a nice weblog like this one nowadays. Blaze AI!