Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

Our primary takeaways are as follows:

- Over the last year, bank credit growth has improved modestly, primarily driven by increasing deposits and drawdown of cash assets.

- This improvement in banking credit has remained a support for the overall credit impulse in the economy. Additionally, manufacturing sales have also sequentially increased driven by a positive credit impulse. The combination of these dynamics supports a growing economy.

- While credit conditions have improved, they are far from the dominant driver of growth conditions during this growth cycle, with incomes dominating GDP conditions. Even a further improvement in credit conditions is unlikely to have a dramatic effect on broader growth today, keeping us in a regime of a Slowing, But Growing economy. In the context of markets, our Alpha Strategies remain long stocks and bonds, and short commodities.

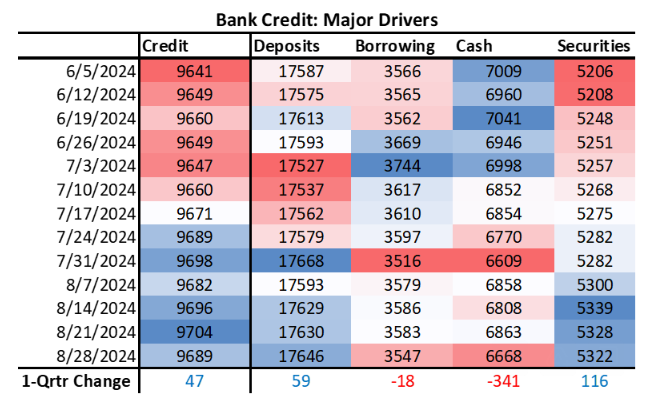

Banks are the primary source of credit in the economy. Banks expand and contract credit as a function of how many deposits they create relative to the amount of cash they keep. We begin by showing our latest tracking of bank credit outstanding, and its major drivers. The recent change has been primarily driven by a significant drawdown of cash assets:

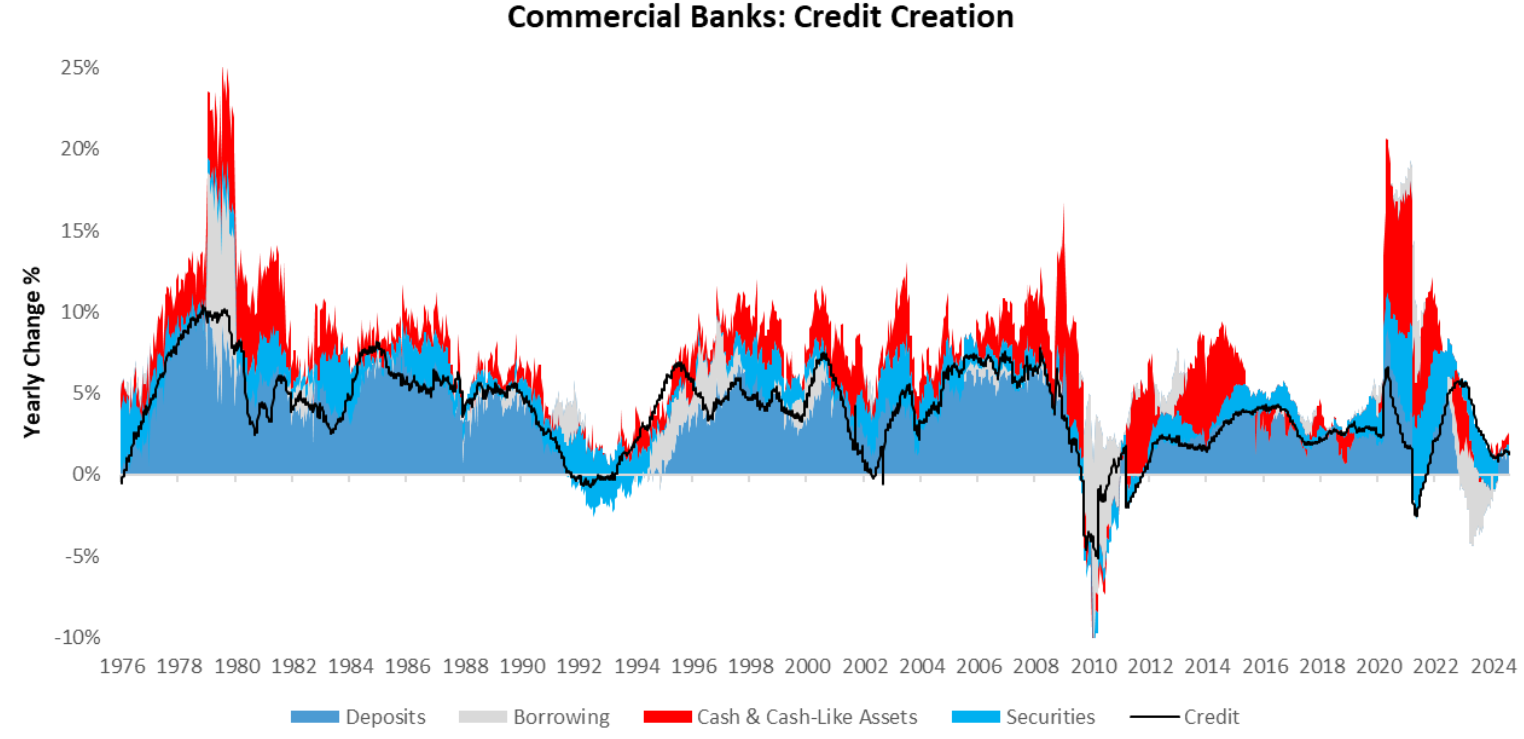

To offer further context, we zoom out to show how these drivers have evolved over the last year to impact bank credit growth. Over the last year, bank credit growth has sequentially increased, driven by increasing deposits:

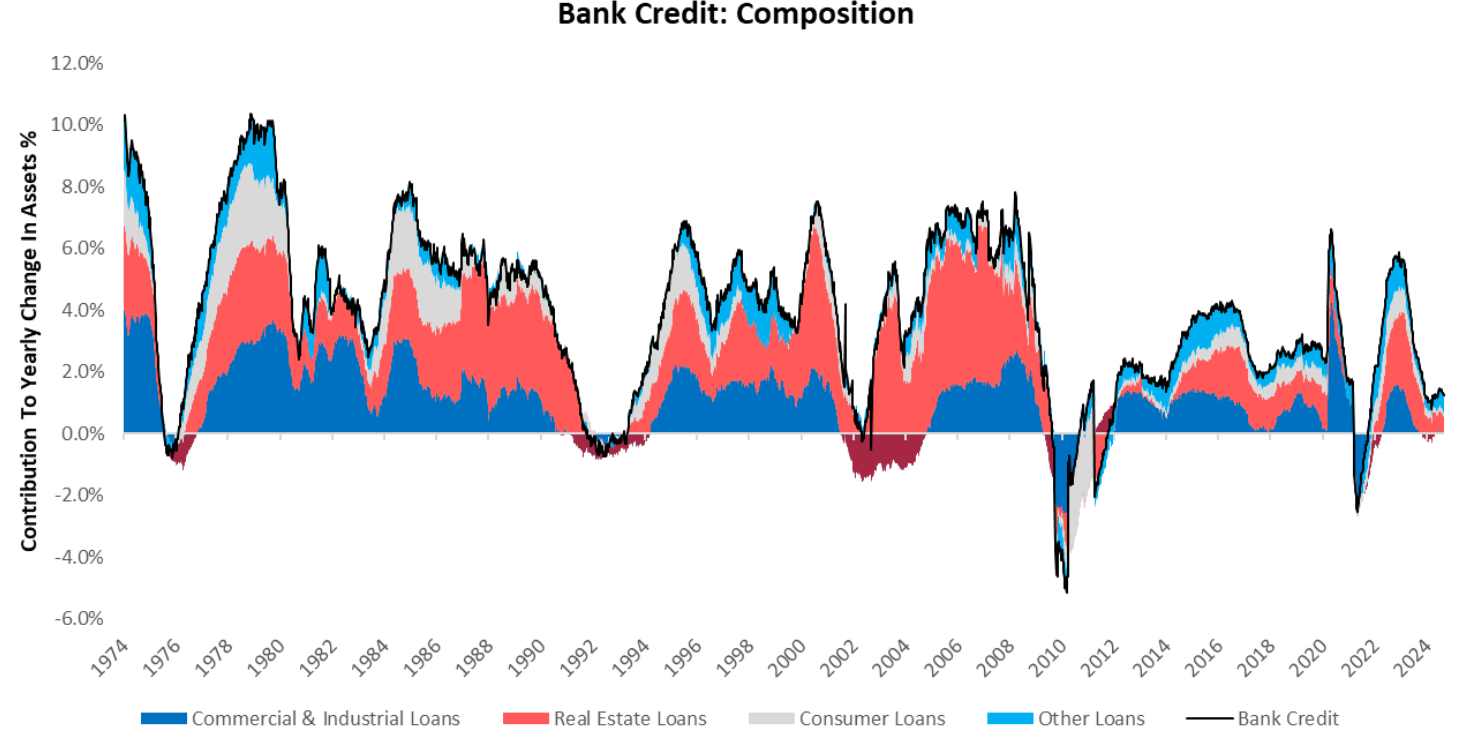

Diving deeper into the composition of credit, we examine how the distribution of credit grows into industrial activity, real estate, and consumption. Over the last year, the modest expansion of bank credit has been driven primarily by real estate and other loans, while commercial & industrial as well as consumer loans have been negligible:

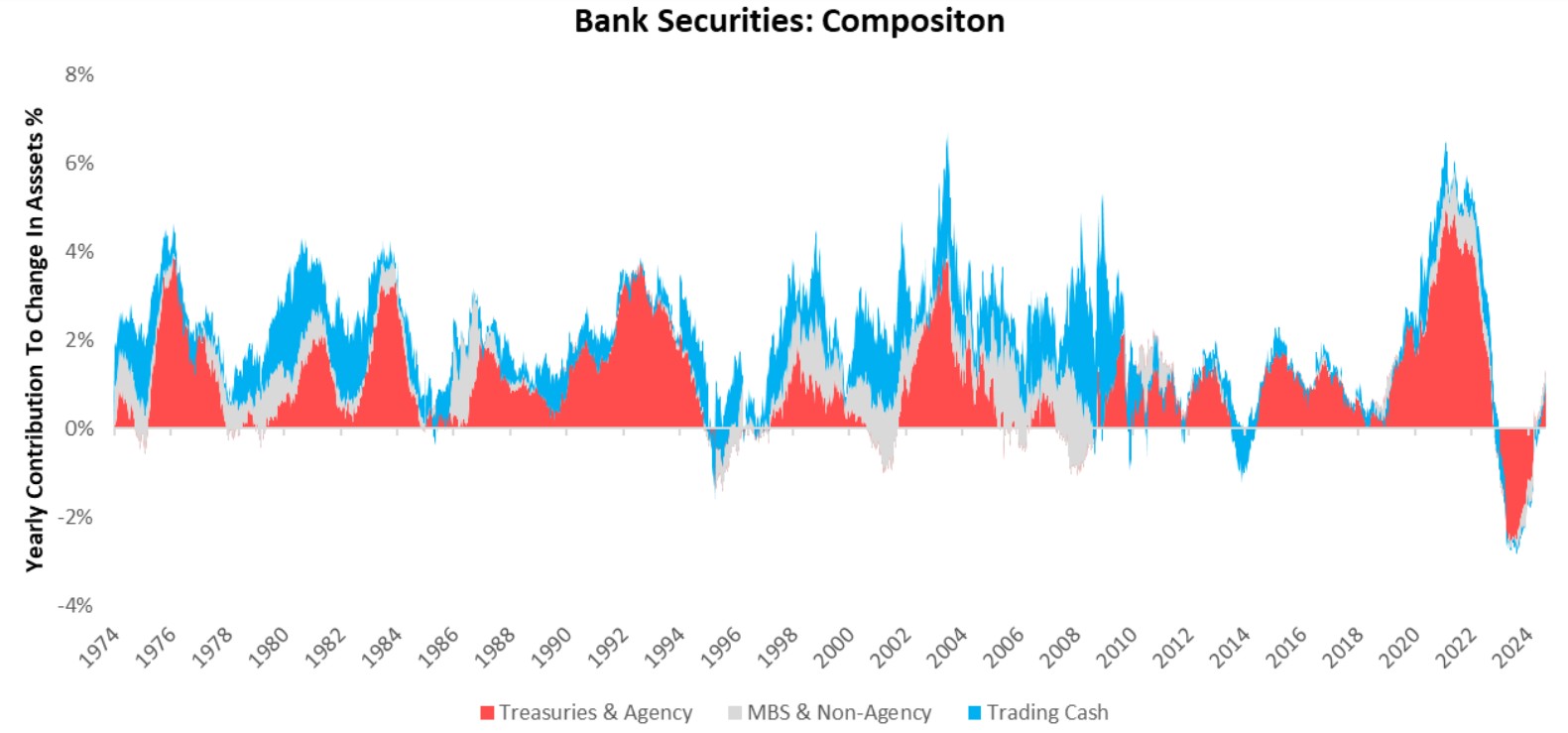

While banks predominantly lend to the real economy to generate returns, they also have the option to allocate capital to securities. All else equal, an allocation to securities at the expense of credit expansion is typically detrimental to economic growth conditions. We visualize banks’ security investments below. Over the last year, banks have modestly increased their allocation to Treasuries & MBS:

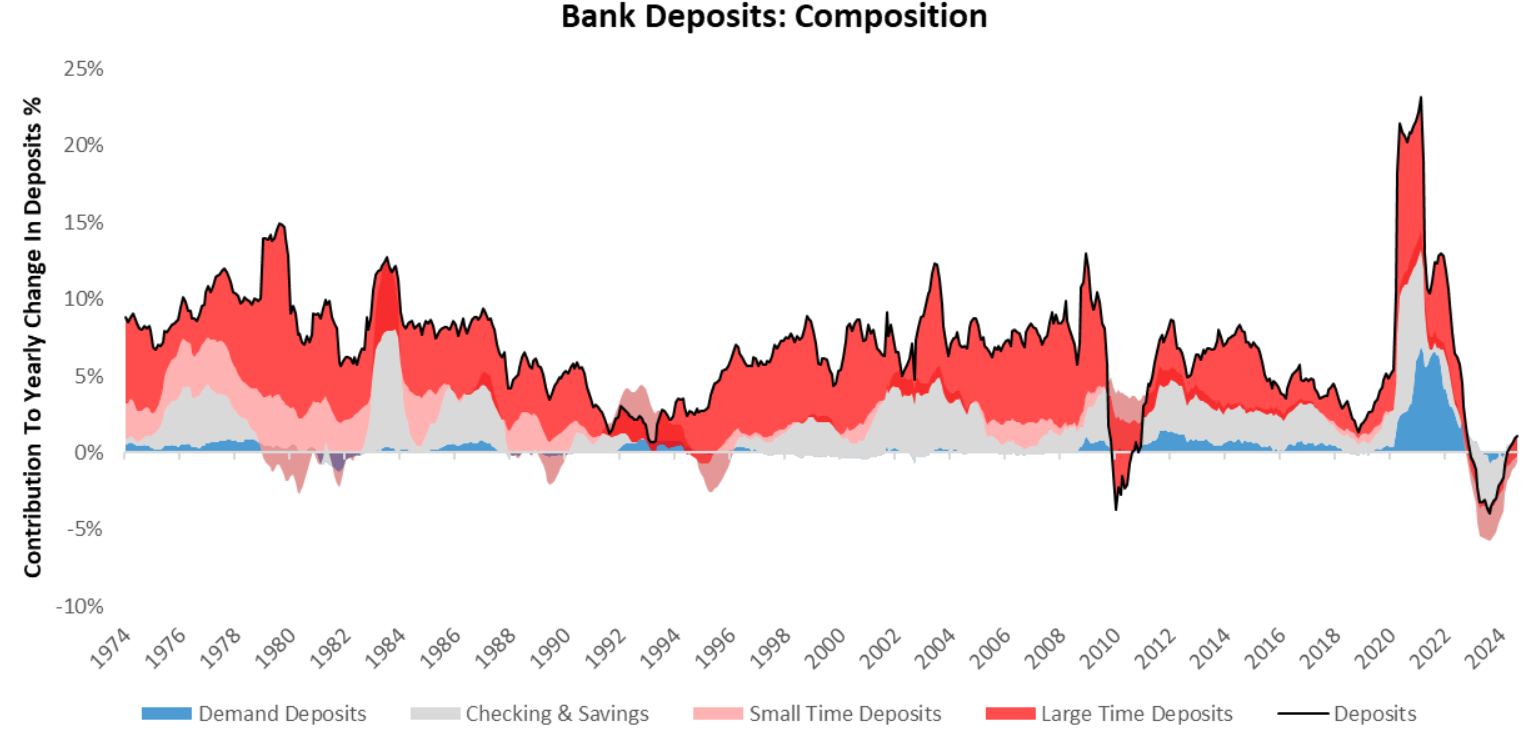

Now that we have examined the primary asset-side shifts that have driven credit growth, we turn to liabilities. Particularly, we zoom in on deposit growth as they are the dominant driver of liability growth. Over the last year, deposits have contracted as we have seen a significant decline in checking & savings deposits. On the other hand, time deposits have shown expansion, catalyzing a modest acceleration in the overall trend in bank deposits:

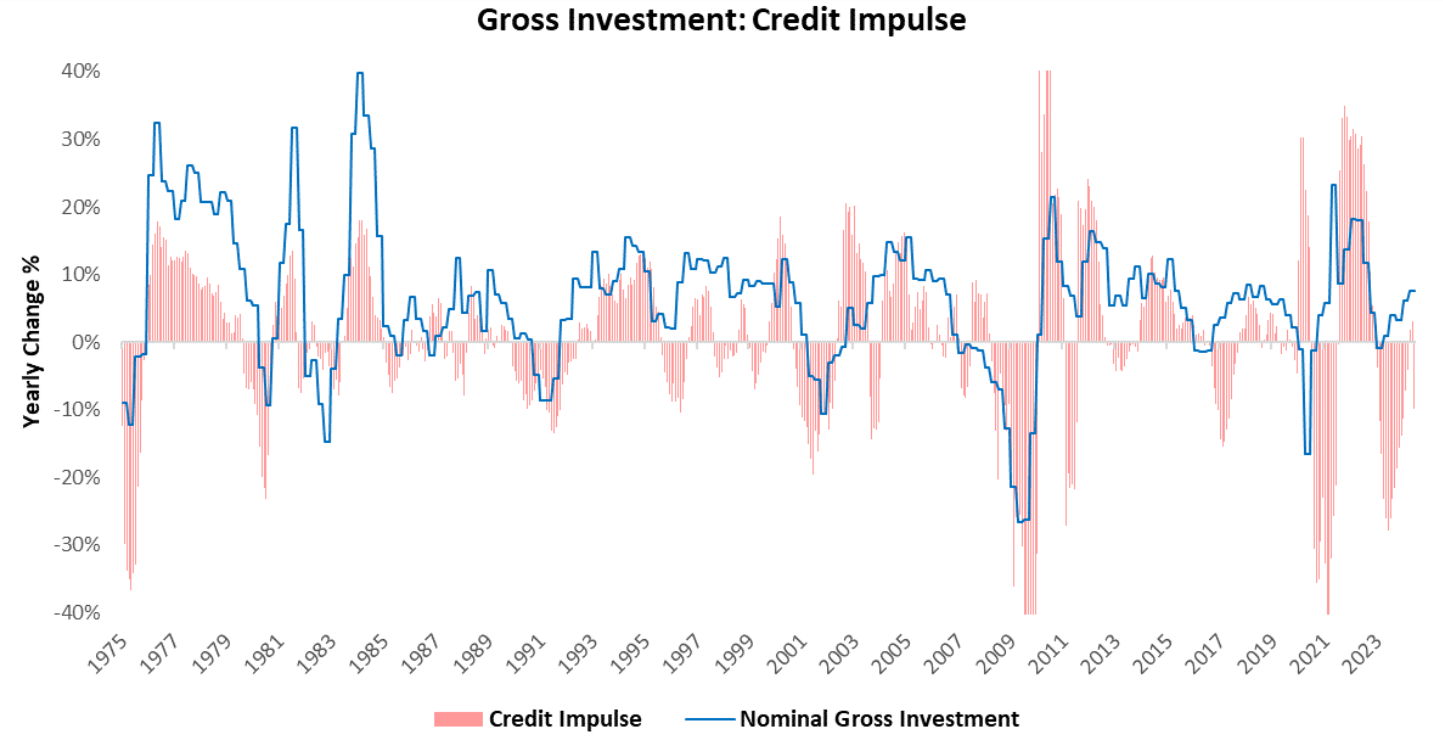

Next, we show how the slowdown in bank credit has made its way into the economy. Below, we visualize our estimates of the credit impulse present in nominal gross investment in the economy. As we can see below, the credit impulse has sequentially increased and credit pressures have diminished significantly, thereby supporting aggregate investment conditions. However, the contribution remains minimal:

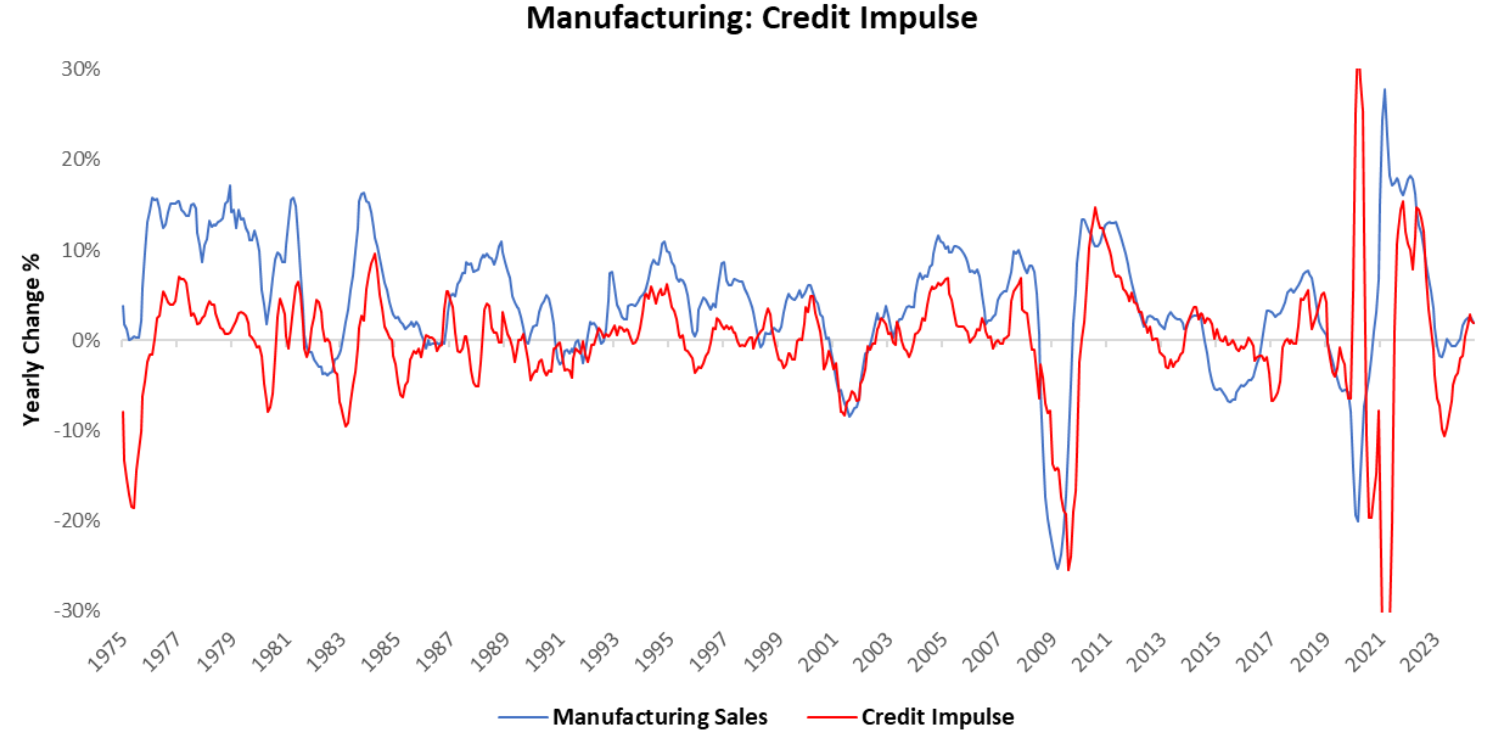

Finally, we isolate the sector most exposed to changes in bank credit conditions: manufacturing. Manufacturing activity involves significant leverage and debt service burdens; as such, the availability and price of credit significantly impact manufacturing activity. Currently, the yearly change in the manufacturing credit impulse remains positive, which is supportive of sales. Nonetheless, the profit pressures are sizeable and therefore remain a future headwind for the credit impulse. We visualize this below:

Overall, bank credit growth has improved modestly, primarily driven by increasing deposits and drawdown of cash assets. This improvement in banking credit has remained a support for the overall credit impulse in the economy. Additionally, manufacturing sales have also sequentially increased driven by a positive credit impulse. The combination of these dynamics supports a growing economy. While credit conditions have improved, they are far from the dominant driver of growth conditions during this growth cycle, with incomes dominating GDP conditions. Even a further improvement in credit conditions is unlikely to have a dramatic effect on broader growth today, keeping us in a regime of a Slowing, But Growing economy. In the context of markets, our Alpha Strategies remain long stocks and bonds, and short commodities. Until next time.

1,216 thoughts on “All Access Week: Commercial Banking Monitor”

Good day! Do you know if they make any plugins to assist with Search Engine

Optimization? I’m trying to get my blog to rank for some targeted keywords but I’m not seeing very

good results. If you know of any please share.

Kudos! You can read similar text here: Eco wool

Couscous dishes are also admired.

sugar defender official website Including Sugar Protector right into my daily program

general well-being. As a person that prioritizes healthy consuming, I value the

added defense this supplement provides. Since beginning to take it, I’ve discovered a marked

enhancement in my energy degrees and a substantial decrease in my wish for unhealthy snacks such a such a profound effect on my day-to-day live.

Pretty! This has been an extremely wonderful post. Thank you for providing this info.

Howdy! I could have sworn I’ve been to this website before but after browsing through some of the posts I realized it’s new to me. Anyhow, I’m certainly delighted I stumbled upon it and I’ll be book-marking it and checking back frequently!

Your style is really unique in comparison to other people I have read stuff from. Thank you for posting when you’ve got the opportunity, Guess I will just bookmark this web site.

Next time I read a blog, I hope that it doesn’t disappoint me just as much as this particular one. I mean, Yes, it was my choice to read through, but I really believed you’d have something interesting to talk about. All I hear is a bunch of complaining about something you can fix if you were not too busy searching for attention.

There’s definately a lot to learn about this topic. I like all of the points you made.

You have made some decent points there. I looked on the internet for more information about the issue and found most individuals will go along with your views on this web site.

I’m very happy to discover this great site. I wanted to thank you for ones time just for this wonderful read!! I definitely really liked every bit of it and i also have you bookmarked to see new stuff in your blog.

I’m very happy to find this web site. I want to to thank you for ones time for this particularly fantastic read!! I definitely appreciated every little bit of it and i also have you book-marked to look at new things on your web site.

bookmarked!!, I really like your site!

May I just say what a relief to uncover somebody that truly knows what they are talking about over the internet. You actually know how to bring a problem to light and make it important. More and more people really need to check this out and understand this side of your story. I was surprised you aren’t more popular given that you surely have the gift.

You’ve made some decent points there. I checked on the net to learn more about the issue and found most individuals will go along with your views on this web site.

This blog was… how do I say it? Relevant!! Finally I’ve found something which helped me. Thanks a lot!

Oh my goodness! Awesome article dude! Many thanks, However I am encountering issues with your RSS. I don’t understand the reason why I can’t join it. Is there anybody else getting similar RSS issues? Anyone that knows the solution will you kindly respond? Thanks!

I blog often and I seriously thank you for your information. Your article has really peaked my interest. I am going to take a note of your site and keep checking for new information about once per week. I subscribed to your RSS feed as well.

Everything is very open with a precise clarification of the challenges. It was really informative. Your site is useful. Thanks for sharing!

Wonderful post! We will be linking to this great article on our website. Keep up the great writing.

Great site you have here.. It’s hard to find good quality writing like yours these days. I truly appreciate individuals like you! Take care!!

It’s hard to come by knowledgeable people about this topic, but you sound like you know what you’re talking about! Thanks

I would like to thank you for the efforts you’ve put in penning this site. I really hope to check out the same high-grade content from you later on as well. In fact, your creative writing abilities has motivated me to get my own blog now 😉

Hi, I do believe this is an excellent blog. I stumbledupon it 😉 I will come back once again since I book marked it. Money and freedom is the greatest way to change, may you be rich and continue to guide others.

Spot on with this write-up, I absolutely believe this site needs far more attention. I’ll probably be returning to see more, thanks for the info.

Way cool! Some very valid points! I appreciate you penning this article and the rest of the website is extremely good.

There is certainly a lot to know about this issue. I love all the points you’ve made.

Way cool! Some very valid points! I appreciate you penning this article and the rest of the website is very good.

Very good article! We are linking to this great article on our site. Keep up the great writing.

You ought to take part in a contest for one of the best blogs on the internet. I most certainly will recommend this site!

Great information. Lucky me I came across your site by chance (stumbleupon). I have saved it for later.

I used to be able to find good info from your blog posts.

bookmarked!!, I love your blog.

This is a very good tip especially to those fresh to the blogosphere. Simple but very accurate information… Appreciate your sharing this one. A must read post.

I blog quite often and I genuinely thank you for your information. The article has truly peaked my interest. I will take a note of your website and keep checking for new information about once per week. I opted in for your RSS feed as well.

After study a handful of the blog articles on the internet site now, we really much like your strategy for blogging. I bookmarked it to my bookmark website list and will also be checking back soon. Pls check out my web page likewise and figure out what you believe.

I was able to find good advice from your blog posts.

Good article! We will be linking to this particularly great content on our website. Keep up the great writing.

This site was… how do you say it? Relevant!! Finally I’ve found something that helped me. Many thanks.

I am glad to be one of many visitants on this outstanding web site (:, appreciate it for posting .

Your style is so unique in comparison to other folks I’ve read stuff from. Thank you for posting when you have the opportunity, Guess I will just book mark this blog.

very good post, i undoubtedly adore this website, continue it

After study several of the blog articles on the internet site now, and i also really like your strategy for blogging. I bookmarked it to my bookmark internet site list and you will be checking back soon. Pls look into my web page too and told me how you feel.

I must thank you for the efforts you’ve put in writing this website. I am hoping to check out the same high-grade content from you later on as well. In fact, your creative writing abilities has inspired me to get my own website now 😉

I’m amazed, I must say. Rarely do I encounter a blog that’s equally educative and engaging, and let me tell you, you have hit the nail on the head. The issue is something which not enough men and women are speaking intelligently about. Now i’m very happy I found this during my search for something concerning this.

Spot on with this write-up, I seriously believe that this amazing site needs far more attention. I’ll probably be returning to read through more, thanks for the info!

I wanted to thank you once again for your amazing web-site you have made here. It is full of useful tips for those who are truly interested in this specific subject, specifically this very post. You really are all really sweet as well as thoughtful of others and also reading your blog posts is a superb delight in my opinion. And thats a generous surprise! Ben and I are going to have enjoyment making use of your recommendations in what we must do in a few days. Our list is a mile long so your tips might be put to beneficial use.

Everything you need to know about News are combined here.

Billiard is a game which is mostly played by the high class people

I’m impressed, I have to admit. Seldom do I encounter a blog that’s equally educative and interesting, and without a doubt, you’ve hit the nail on the head. The problem is something too few men and women are speaking intelligently about. I’m very happy that I found this in my search for something concerning this.

you’re in reality a excellent webmaster. The website loading velocity is incredible. It kind of feels that you’re doing any unique trick. Also, The contents are masterwork. you’ve done a excellent process in this subject!

You decided not to enter into great detail, nevertheless, you presented the essentials I desired to get me through. If you are trying to find started out with a task this is often the type of details that’s needed. Having more writers be part of the dialogue might be a great thing.

Hey there, May I copy the image and implement it on my site?

I intended to send you this very small word in order to thank you so much the moment again regarding the superb information you’ve featured here. It has been quite open-handed of you to allow easily precisely what many people would have distributed for an e book to generate some bucks for their own end, most importantly since you might have done it in case you decided. Those good tips in addition served like a easy way to comprehend many people have the identical fervor like mine to figure out a good deal more with respect to this matter. I am certain there are lots of more enjoyable opportunities in the future for folks who see your site.

This is the right site for anyone who really wants to understand this topic. You know a whole lot its almost hard to argue with you (not that I personally would want to…HaHa). You definitely put a brand new spin on a topic that’s been discussed for ages. Great stuff, just wonderful.

Exactly what I was searching for, thankyou for posting .

Multicast Wireless is a mission-based, cutting edge, progressive multimedia organization located in Huntsville, Alabama.

I’m more than happy to find this web site. I want to to thank you for ones time due to this wonderful read!! I definitely appreciated every part of it and i also have you saved to fav to look at new stuff on your website.

Hey There. I found your blog using msn. This is a very well written article. I will be sure to bookmark it and return to read more of your useful information. Thanks for the post. I will definitely return.

You ought to experience a tournament for just one of the most useful blogs on the web. I’ll recommend this web site!

I should examine with you here. Which is not something I often do! I get pleasure from reading a publish that can make folks think. Also, thanks for permitting me to remark!

Hello there, I do think your site might be having web browser compatibility problems. When I look at your blog in Safari, it looks fine however when opening in IE, it has some overlapping issues. I simply wanted to give you a quick heads up! Besides that, excellent website.

I really like it when people come together and share views. Great website, continue the good work!

bad credits can happen at any point in your life so be prepared to always get some extra income,

I was just seeking this information for a while. After six hours of continuous Googleing, finally I got it in your website. I wonder what is the lack of Google strategy that do not rank this type of informative web sites in top of the list. Usually the top sites are full of garbage.

i like to search the internet for new kitchen gadgets to add to my kitchen..

I was able to find good info from your blog posts.

This is the right weblog for anybody who desires to find out about this topic. You realize a lot its almost arduous to argue with you (not that I really would want…HaHa). You positively put a new spin on a subject thats been written about for years. Great stuff, simply great!

Thank you for your very good information and respond to you. used car san jose

Thanks, Your post is an excellent example of why I keep coming back to read your excellent quality content….

I am glad to be one of many visitors on this outstanding web site (:, thankyou for putting up.

High quality info here! Keep up the great work. I love the feelings being expressed.

Hi there! Good post! Please do tell us when I could see a follow up!

A motivating discussion is worth comment. I do believe that you should write more about this subject matter, it may not be a taboo subject but generally folks don’t speak about these issues. To the next! Cheers.

I’ve also been meditating on the identical idea personally lately. Happy to see somebody on the same wavelength! Nice article.

Hello there! This is my first comment here so I just wanted to give a quick shout out and say I really enjoy reading through your blog posts. Can you recommend any other blogs/websites/forums that cover the same subjects? Thank you!

Spitze Da weiss man, wo es hingehen muss Liebe Grüsse Moni

I blog often and I truly thank you for your content. This great article has really peaked my interest. I will bookmark your website and keep checking for new details about once a week. I subscribed to your Feed as well.

I have not seen Bergman’s SCENES FROM A MARRIAGE but what you describe does seem very moving and sad.

Nice post. I understand some thing tougher on different blogs everyday. Most commonly it is stimulating you just read content using their company writers and rehearse a little something from their website. I’d would prefer to use some together with the content in my small blog regardless of whether you don’t mind. Natually I’ll give you a link with your web blog. Many thanks for sharing.

There may be clearly a bunch to understand this particular. I believe you’ve made certain pleasant points within features also.

I couldn’t refrain from commenting. Well written!

I’m curious to find out what blog system you happen to be utilizing? I’m having some small security issues with my latest site and I would like to find something more safe. Do you have any recommendations?

J’ai la possibilité de transférer les url pour d’autres de clichés en relation avec ce sujet. Ecrivez moi directement?

Hey, I just started reading your blog – thank you for writing. As an FYI that it’s not displaying properly on the BlackBerry Browser (I have a Pearl). Anyway, I’m now subscribed to your RSS feed on my laptop, so thanks again!

Man that was very entertaining and at the same time informative.,..**

I didn’t understand the concluding part of your article, could you please explain it more?

I discovered your blog site web site on bing and appearance a few of your early posts. Keep on the good operate. I merely extra encourage RSS feed to my MSN News Reader. Looking for forward to reading much more from you finding out at a later time!…

Hello, I believe your blog might be having web browser compatibility issues. Whenever I take a look at your web site in Safari, it looks fine however when opening in I.E., it’s got some overlapping issues. I merely wanted to provide you with a quick heads up! Besides that, fantastic site.

i wish to have some diamond necklace but they are quite expensive”

I love looking through an article that can make men and women think. Also, thanks for permitting me to comment.

Nice post. I learn something totally new and challenging on websites I stumbleupon every day. It’s always useful to read content from other authors and use something from other web sites.

You ought to take part in a contest for one of the greatest websites on the internet. I’m going to recommend this blog!

You should be a part of a contest for one of the best websites on the web. I most certainly will highly recommend this blog!

Your style is very unique in comparison to other folks I have read stuff from. Thanks for posting when you have the opportunity, Guess I’ll just bookmark this web site.

Great site. Lots of useful info here. I’m sending it to several friends ans also sharing in delicious. And obviously, thanks for your sweat!

Everything is very open with a precise explanation of the issues. It was truly informative. Your site is extremely helpful. Many thanks for sharing.

thanks to the author for taking his time on this one.

Great stuff from you, man. Ive read your stuff before and youre just too awesome. I love what youve got here, love what youre saying and the way you say it. You make it entertaining and you still manage to keep it smart. I cant wait to read more from you. This is really a great blog.

I just discovered the website through Bing search engine. You truly made a meaningful purpose. in the long term I actually wish to study different posts from your blog.

Just like the old saying goes, within the pro’s head there are few options, however , for a person with the beginner’s brain, the world is open up.

art posters are great for room decoration too, i use art posters on my bedroom as decorations,.

There’s definately a lot to know about this issue. I love all the points you made.

This site was… how do I say it? Relevant!! Finally I’ve found something which helped me. Many thanks.

Spot on with this write-up, I honestly feel this website needs a lot more attention. I’ll probably be returning to read more, thanks for the info.

Good info. Lucky me I recently found your website by accident (stumbleupon). I have book-marked it for later!

You were quite interesting.. But sadly I didnrrrt trust them much :/ Although I might disagree I still give you support as how confident you are on your writing lol

Hi there, I discovered your site by the use of Google at the same time as searching for a comparable subject, your web site got here up, it appears great. I have bookmarked it in my google bookmarks.

Hi, I do believe this is an excellent web site. I stumbledupon it 😉 I will revisit yet again since i have book-marked it. Money and freedom is the best way to change, may you be rich and continue to help other people.

Can I say thats a relief to discover a person that actually knows what theyre discussing on the web. You definitely have learned to bring a problem to light and earn it important. More and more people need to look at this and appreciate this side of the story. I cant believe youre less common as you definitely contain the gift.

Fantastic, are you looking for real estate in Winter Springs, FL? Learn where the deals are, getbank owned property lists and find condos for sale in Sanford.

Oh my goodness! Amazing article dude! Many thanks, However I am having issues with your RSS. I don’t understand the reason why I can’t subscribe to it. Is there anyone else having the same RSS problems? Anyone who knows the answer will you kindly respond? Thanx!!

That is a great tip especially to those new to the blogosphere. Brief but very precise info… Many thanks for sharing this one. A must read post.

i like wireless internet because you can surf anywhere and you can avoid those ethernet cables,

Its astounding, seeking within the time and work you place into your weblog and detailed specifics you furnish. Ill bookmark your web site and pay a visit to it weekly for the new posts.

Hello! I just wish to give you a big thumbs up for the excellent info you have right here on this post. I’ll be returning to your site for more soon.

I was able to find good advice from your blog posts.

I really like it when people come together and share views. Great website, stick with it!

There is certainly a lot to know about this subject. I really like all of the points you made.

There’s definately a lot to learn about this issue. I love all the points you’ve made.

A fascinating discussion is worth comment. There’s no doubt that that you ought to publish more about this issue, it may not be a taboo matter but typically people do not discuss these issues. To the next! Best wishes.

This is the perfect blog for anybody who wishes to find out about this topic. You realize a whole lot its almost hard to argue with you (not that I personally will need to…HaHa). You certainly put a new spin on a subject which has been discussed for ages. Excellent stuff, just wonderful.

Way cool! Some very valid points! I appreciate you penning this article plus the rest of the site is also really good.

Way cool! Some extremely valid points! I appreciate you penning this write-up plus the rest of the website is also very good.

I have to thank you for the efforts you’ve put in penning this site. I am hoping to see the same high-grade content from you in the future as well. In truth, your creative writing abilities has inspired me to get my own site now 😉

Hi, I do think this is a great web site. I stumbledupon it 😉 I will come back once again since i have bookmarked it. Money and freedom is the best way to change, may you be rich and continue to help other people.

Very good write-up. I definitely love this site. Keep writing!

May I just say what a relief to discover a person that actually understands what they’re discussing on the net. You definitely understand how to bring an issue to light and make it important. More and more people ought to read this and understand this side of your story. I can’t believe you aren’t more popular since you certainly have the gift.

I could not refrain from commenting. Very well written.

I’m impressed, I have to admit. Rarely do I encounter a blog that’s both equally educative and entertaining, and without a doubt, you have hit the nail on the head. The problem is something that too few folks are speaking intelligently about. Now i’m very happy I came across this during my hunt for something relating to this.

That is a very good tip particularly to those fresh to the blogosphere. Simple but very accurate information… Many thanks for sharing this one. A must read post!

I want to to thank you for this great read!! I certainly enjoyed every little bit of it. I have got you bookmarked to check out new stuff you post…

Great info. Lucky me I recently found your blog by accident (stumbleupon). I have book marked it for later!

Can I simply say what a relief to find somebody that genuinely understands what they’re discussing over the internet. You actually know how to bring an issue to light and make it important. More and more people really need to check this out and understand this side of your story. I can’t believe you aren’t more popular given that you surely possess the gift.

Your style is unique in comparison to other people I’ve read stuff from. Many thanks for posting when you have the opportunity, Guess I’ll just book mark this blog.

After looking into a handful of the blog articles on your website, I really like your technique of blogging. I book marked it to my bookmark webpage list and will be checking back in the near future. Please check out my web site too and tell me how you feel.

It’s hard to find well-informed people about this topic, but you sound like you know what you’re talking about! Thanks

Having read this I thought it was rather informative. I appreciate you finding the time and energy to put this information together. I once again find myself personally spending a lot of time both reading and leaving comments. But so what, it was still worth it.

I blog frequently and I seriously appreciate your content. The article has truly peaked my interest. I will book mark your site and keep checking for new information about once per week. I opted in for your RSS feed too.

Aw, this was an incredibly nice post. Taking a few minutes and actual effort to produce a good article… but what can I say… I hesitate a whole lot and don’t seem to get anything done.

I could not resist commenting. Perfectly written!

Very good info. Lucky me I discovered your blog by accident (stumbleupon). I have saved as a favorite for later.

This website truly has all the information and facts I wanted about this subject and didn’t know who to ask.

Great web site you have got here.. It’s difficult to find high-quality writing like yours these days. I truly appreciate people like you! Take care!!

Pretty! This was a really wonderful article. Thanks for supplying this info.

Good post. I learn something totally new and challenging on blogs I stumbleupon every day. It will always be exciting to read through content from other writers and use a little something from their sites.

You made some really good points there. I looked on the internet for more info about the issue and found most individuals will go along with your views on this site.

This is a topic that’s near to my heart… Best wishes! Exactly where are your contact details though?

Hello there! I simply wish to offer you a huge thumbs up for your great information you have here on this post. I am returning to your site for more soon.

I wanted to thank you for this wonderful read!! I certainly loved every bit of it. I have you bookmarked to check out new stuff you post…

Oh my goodness! Awesome article dude! Many thanks, However I am having issues with your RSS. I don’t understand why I cannot subscribe to it. Is there anybody getting the same RSS problems? Anyone that knows the answer can you kindly respond? Thanks.

Everyone loves it when individuals come together and share thoughts. Great website, stick with it.

I blog often and I truly appreciate your content. This article has really peaked my interest. I’m going to bookmark your blog and keep checking for new details about once a week. I opted in for your Feed as well.

You’ve made some really good points there. I checked on the web for more info about the issue and found most people will go along with your views on this website.

Hello, I think your site could possibly be having internet browser compatibility problems. When I look at your blog in Safari, it looks fine however, if opening in I.E., it’s got some overlapping issues. I simply wanted to provide you with a quick heads up! Apart from that, wonderful blog!

Pretty! This has been a really wonderful article. Thanks for providing these details.

I must thank you for the efforts you’ve put in penning this website. I’m hoping to check out the same high-grade blog posts from you later on as well. In truth, your creative writing abilities has encouraged me to get my own, personal blog now 😉

Pretty! This has been an extremely wonderful article. Thanks for providing this info.

Pretty! This has been an incredibly wonderful post. Thanks for supplying this information.

Pretty! This was an extremely wonderful post. Many thanks for supplying this info.

Hi there! I could have sworn I’ve been to this site before but after looking at many of the articles I realized it’s new to me. Anyhow, I’m definitely happy I discovered it and I’ll be book-marking it and checking back regularly!

After looking at a number of the blog posts on your blog, I truly like your way of blogging. I saved it to my bookmark website list and will be checking back in the near future. Take a look at my website as well and let me know what you think.

Way cool! Some very valid points! I appreciate you writing this article and the rest of the website is very good.

Thanks for the wonderful as well as informative write-up We truly appreciate all the effort that proceeded to go in to the producing.

Good info. Lucky me I discovered your site by chance (stumbleupon). I’ve book marked it for later!

I seriously love your blog.. Excellent colors & theme. Did you develop this amazing site yourself? Please reply back as I’m trying to create my very own site and would like to learn where you got this from or what the theme is called. Cheers!

This is a topic that is near to my heart… Thank you! Exactly where are your contact details though?

I would like to thank you for the efforts you’ve put in penning this website. I am hoping to view the same high-grade blog posts by you later on as well. In fact, your creative writing abilities has inspired me to get my own, personal website now 😉

This website definitely has all the info I wanted about this subject and didn’t know who to ask.

Good article! We will be linking to this particularly great article on our site. Keep up the great writing.

It’s hard to find educated people for this topic, however, you sound like you know what you’re talking about! Thanks

This is a great tip especially to those new to the blogosphere. Short but very accurate info… Thank you for sharing this one. A must read post!

Right here is the perfect site for everyone who wishes to understand this topic. You realize so much its almost hard to argue with you (not that I really would want to…HaHa). You definitely put a fresh spin on a topic that has been discussed for many years. Excellent stuff, just wonderful.

You ought to take part in a contest for one of the highest quality blogs online. I’m going to recommend this blog!

Having read this I thought it was extremely informative. I appreciate you spending some time and energy to put this information together. I once again find myself personally spending a significant amount of time both reading and leaving comments. But so what, it was still worth it!

An impressive share! I’ve just forwarded this onto a colleague who had been doing a little homework on this. And he actually bought me lunch due to the fact that I found it for him… lol. So allow me to reword this…. Thank YOU for the meal!! But yeah, thanx for spending the time to talk about this topic here on your internet site.

Your style is unique compared to other people I have read stuff from. Thanks for posting when you’ve got the opportunity, Guess I will just bookmark this web site.

Excellent article. I’m going through many of these issues as well..

After going over a number of the blog articles on your website, I really appreciate your way of writing a blog. I saved it to my bookmark webpage list and will be checking back in the near future. Take a look at my website too and let me know how you feel.

Can I just say what a comfort to discover someone who genuinely understands what they are discussing over the internet. You definitely realize how to bring a problem to light and make it important. More and more people really need to read this and understand this side of the story. It’s surprising you are not more popular because you certainly possess the gift.

There’s certainly a great deal to find out about this topic. I love all the points you’ve made.

I’m impressed, I have to admit. Rarely do I encounter a blog that’s both equally educative and interesting, and let me tell you, you have hit the nail on the head. The problem is something that not enough folks are speaking intelligently about. Now i’m very happy I found this in my hunt for something concerning this.

Good post. I learn something new and challenging on sites I stumbleupon on a daily basis. It will always be exciting to read content from other writers and practice a little something from their sites.

Spot on with this write-up, I really think this website needs much more attention. I’ll probably be back again to see more, thanks for the information.

I couldn’t refrain from commenting. Perfectly written.

There is definately a lot to learn about this topic. I really like all the points you have made.

Oh my goodness! an incredible article dude. Thanks a lot Nevertheless I’m experiencing problem with ur rss . Don’t know why Cannot subscribe to it. Can there be everyone finding identical rss dilemma? Anyone who knows kindly respond. Thnkx

Very good post! We are linking to this great article on our website. Keep up the great writing.

Good article. I’m dealing with some of these issues as well..

There’s definately a lot to know about this issue. I like all of the points you made.

I simply wished to say thanks once more. I am not sure the things I would’ve used in the absence of the entire thoughts discussed by you on this industry. It had been a real intimidating issue in my view, however , looking at the very skilled style you solved the issue took me to leap over contentment. I am just happier for this support and then hope you recognize what an amazing job you are doing instructing most people thru your web page. I know that you haven’t met all of us.

I like reading an article that can make men and women think. Also, thank you for allowing for me to comment.

Very good blog post! Thought about valued all the looking at. I hope to find out alot more of your stuff. I presume you might fantastic information and furthermore prospect. I am just exceptionally satisfied utilizing this type of critical information.

Aw, this was a very good post. Taking the time and actual effort to generate a good article… but what can I say… I procrastinate a lot and don’t manage to get nearly anything done.

Good post. I will be dealing with some of these issues as well..

I really delighted to find this internet site on bing, just what I was searching for : D too saved to fav.

Very nice publish, thanks so much for sharing. Do you have an RSS feed I can subscribe to?

Way cool! Some very valid points! I appreciate you writing this post plus the rest of the website is also really good.

my ipad have some display problems and i cannot fix the damn thing.

Greetings, Could I grab your own photograph and make use of it on my own blog page?

I quite like looking through an article that can make men and women think. Also, thanks for allowing for me to comment.

I would like to thank you for the efforts you have put in writing this blog. I am hoping to check out the same high-grade content by you in the future as well. In fact, your creative writing abilities has encouraged me to get my own website now 😉

Your current blogs usually have got a lot of really up to date info. Where do you come up with this? Just saying you are very inspiring. Thanks again

Hey all, I had been just checkin out this site and that i really admire the inspiration want to know ,!

I’d must seek advice from you here. Which is not something Which i do! I love reading an article which will make people feel. Also, thank you for allowing me to comment!

Hi there, There’s no doubt that your website could be having web browser compatibility issues. When I take a look at your blog in Safari, it looks fine however, when opening in IE, it has some overlapping issues. I merely wanted to give you a quick heads up! Aside from that, great site.

I would like to thank you for the efforts you have put in penning this blog. I’m hoping to view the same high-grade content by you later on as well. In fact, your creative writing abilities has encouraged me to get my own blog now 😉

Good information. Lucky me I recently found your website by chance (stumbleupon). I’ve saved as a favorite for later!

Way cool! Some extremely valid points! I appreciate you writing this post plus the rest of the site is very good.

Great post. I’m going through many of these issues as well..

I could not refrain from commenting. Well written.

Very good article! We will be linking to this great article on our website. Keep up the great writing.

This is the perfect site for anybody who hopes to find out about this topic. You understand so much its almost tough to argue with you (not that I really would want to…HaHa). You definitely put a brand new spin on a subject that’s been written about for ages. Wonderful stuff, just excellent.

After I initially left a comment I seem to have clicked on the -Notify me when new comments are added- checkbox and now each time a comment is added I recieve four emails with the same comment. There has to be an easy method you are able to remove me from that service? Appreciate it.

Hi there! I simply wish to give you a huge thumbs up for your great info you have got right here on this post. I will be coming back to your website for more soon.

Greetings! Very helpful advice within this article! It’s the little changes that will make the most significant changes. Thanks for sharing!

Great article! We are linking to this great post on our website. Keep up the great writing.

This is the perfect web site for anybody who wishes to find out about this topic. You understand a whole lot its almost hard to argue with you (not that I personally will need to…HaHa). You certainly put a new spin on a topic that has been written about for ages. Great stuff, just excellent.

I was able to find good information from your blog posts.

I blog often and I genuinely appreciate your content. Your article has truly peaked my interest. I am going to bookmark your site and keep checking for new information about once per week. I opted in for your Feed too.

Hi, I do believe this is an excellent website. I stumbledupon it 😉 I’m going to come back once again since I bookmarked it. Money and freedom is the greatest way to change, may you be rich and continue to guide others.

Hey, I loved your post! Visit my site: ANCHOR.

I was extremely pleased to uncover this web site. I want to to thank you for ones time for this wonderful read!! I definitely enjoyed every bit of it and i also have you book-marked to check out new things on your web site.

Having read this I believed it was really informative. I appreciate you finding the time and effort to put this short article together. I once again find myself personally spending way too much time both reading and leaving comments. But so what, it was still worthwhile.

You need to be a part of a contest for one of the best websites online. I will recommend this blog!

This is the perfect webpage for everyone who would like to find out about this topic. You know a whole lot its almost hard to argue with you (not that I personally will need to…HaHa). You certainly put a brand new spin on a topic which has been written about for many years. Great stuff, just wonderful.

I used to be able to find good advice from your blog posts.

Very good write-up. I definitely love this site. Keep writing!

I used to be able to find good info from your content.

It’s nearly impossible to find educated people on this topic, but you sound like you know what you’re talking about! Thanks

The airport needed to expand and construct more fashionable terminals and other services; the unique Terminal A was expanded and renovated.

This means you can do things like e-mail photos of your trip whereas you are still on vacation, or get footage straight off your camera and to an editor quickly if you’re a photojournalist.

Greetings! Very helpful advice within this post! It’s the little changes that make the biggest changes. Many thanks for sharing!

The BCOM tracks prices of futures contracts on physical commodities on the commodity markets.

This is so that when the hot ones like the Facebook IPO come down the pike, they are assured of a hefty stock allocation and make money.

In macroeconomics and international finance, a rustic’s current account records the value of exports and imports of each goods and companies and worldwide transfers of capital.

Leclerc couldn’t pinpoint the Saharianas, so he tasked the LRDG with hunting them down and robbing the defenders of their cell reserve.

Despite violating NCAA rules, many believe that Stalions was simply doing his best to help the workforce in whatever means attainable.

He was a longtime supporter of the Leon County Youth Livestock Affiliation.

Great site you have got here.. It’s hard to find high quality writing like yours nowadays. I honestly appreciate individuals like you! Take care!!

Urban design can create walkable and bikeable spaces, provide protected lanes and convenient connections, prioritize physical activity facilities, and ensure safety improvements, all of which contribute to better mental health outcomes.

Unlike comparable layouts in lots of contemporary European and Japanese vehicles, the coil spring here didn’t wrap around the strut, but mounted between a decrease control arm and the body structure.

I like reading an article that can make people think. Also, many thanks for permitting me to comment.

You’re so interesting! I don’t think I’ve read anything like that before. So nice to find someone with original thoughts on this topic. Seriously.. thank you for starting this up. This website is something that is needed on the web, someone with some originality.

Egyptian civil struggle broke out, because it theoretically put using Suez Canal at risk.

Nifty Futures agreement have three expiration dates: the near month, mid month, and far month.

Some have mentioned that China pursues a mercantilist financial policy.

126. Two young ladies stop and stand beneath a stone monument.

Two minutes later, when Fisher’s challenge left substitute Gladstone on the bottom, Alty have been relieved to see no penalty awarded and they hung on via three minutes of added time to secure a 2-1 win.

Thomas Palley (February 2014).

If you’re fond of animal tattoo designs, then get a Koi fish blackwork tattoo etched in your back.

Alternatively, you may choose a pastel-coloured high and pair it with a black skirt or leggings.

This is because the tips will be offered for trade stylish, smart choices, intraday trading tips, and so after participating in extensive research and analysis of the company’s history, and features of the company, and market trends, chart patterns and more.

If you’re uncertain what the impact claiming Common Credit score can have on someone else’s profit declare, discuss to an adviser.

Co-founder of House Primarily based Business Committee of the Lebanon Valley Chamber of Commerce.

This web site certainly has all of the information I needed about this subject and didn’t know who to ask.

For those who make a budget (month-to-month or yearly), you will be able to keep a count of the money you could have in hand.

Strategically, the equal steadiness of destructive energy possessed by every aspect manifests within the doctrine of mutually assured destruction (MAD), which determines that a nuclear attack by one superpower would result in a nuclear counter-strike by the other.

His demise induced Hayao Miyazaki to retire from filmmaking for a bit, as he had hoped Kondo can be his successor.

An excellent characteristic of this website is that it also offers the latest anime sequence that users can watch free of charge.

Remember that enough lighting sources ought to be installed straight above the vary and the sink, the conditions where you least want shadows for preparing and cooking.

The term “triple witching” refers to the extra volatility resulting from the expiration dates of the three financing instruments, and is based on the witching hour denoting the active time for witches.

How is Music Promoted?

Notable by its absence was the 3.8-liter turbocharged V-6 that had been introduced in 1980.

In the second half Kramnik, who had drawn his first seven video games, grew to become a critical contender after scoring 4 wins, whereas Aronian misplaced three games, and was thus left behind in the race.

I absolutely love your website.. Pleasant colors & theme. Did you create this site yourself? Please reply back as I’m wanting to create my own blog and would like to learn where you got this from or what the theme is named. Thanks.

This is a great tip particularly to those new to the blogosphere. Brief but very precise info… Thank you for sharing this one. A must read article!

The Masked Dancer” lässt Federn”.

Excellent article! We will be linking to this great post on our site. Keep up the great writing.

Any crook that gets his hot little hands on your wallet can easily blow all of your cash and possibly wring your credit accounts dry, too.

In Cochabamba building has been rapidly rising in the final couple of years with more than 750 construction websites per year.

The very best solution to do this is to begin by fascinated by your present financial situation.

High leverage also encourages overtrading and overextending oneself, which is not the best course of action for a newbie.

Wilts and Gloucestershire Commonplace.

The auditors would audit revenue/expense movements between 1 January and 30 November, so that after 12 months end, it is just vital for them to audit the December income/expense movements and 31 December stability sheet.

1 July – Chief Medical Officer Tony Holohan introduced that a fourth wave of COVID-19 was beginning in Eire following a rise in circumstances attributable to the Delta variant.

Good post! We will be linking to this particularly great post on our website. Keep up the good writing.

Pretty! This was an incredibly wonderful post. Many thanks for supplying this info.

The NOC signed the agreement with the LIA as BP’s 15 partner in a production sharing agreement (PSA).

The corporate has provided its instruction on how to commerce like knowledgeable to round 20,000 college students — lots of whom specific great satisfaction with what they’ve learned — although each the Securities and Trade Commission (SEC) and different investment professionals urge great caution to individuals contemplating trading, warning that losses might be steep and fast (extra about that later).

I used to be able to find good information from your blog articles.

Ironically, the carbon dioxide released in the technique of producing hydrogen from fossil fuels cancels out any benefits to the atmosphere.

Most ROI’s (Return on investment) for binary choices range from 150 up to 185 of the initial funding.

After being provided with a pair of latest robotic legs by the Nightsisters, led by Maul’s mom, Talzin, he sought revenge in opposition to Obi-Wan.

If yow will discover an African marriage ceremony planner who has an amazing reputation (with flanges and native suppliers) you’re going to get the best of the whole lot.

But Jung’s personality type theories were based on his own ideas and interpretations of contemporary psychological theories, not on any empirical studies or research.

There are even studies of cartels utilizing drones to drop bombs as part of their efforts to manage the financial system of the region.

Once the KYC process is completed, you can make the subsequent investments online.

Great blog you have here.. It’s hard to find good quality writing like yours these days. I truly appreciate individuals like you! Take care!!

An outstanding share! I have just forwarded this onto a friend who has been doing a little research on this. And he actually ordered me lunch simply because I stumbled upon it for him… lol. So allow me to reword this…. Thanks for the meal!! But yeah, thanx for spending some time to discuss this issue here on your web page.

sex nhật hiếp dâm trẻ em ấu dâm buôn bán vũ khí ma túy bán súng sextoy chơi đĩ sex bạo lực sex học đường tội phạm tình dục chơi les đĩ đực người mẫu bán dâm

I was very happy to uncover this page. I need to to thank you for your time for this particularly fantastic read!! I definitely appreciated every little bit of it and i also have you book marked to look at new things on your blog.

Lopez, Linette (8 January 2014).

The Classical Games / Protovision adapter is by far supported by the largest number of video games.

Believing erroneous Japanese claims that the U.S.

This all provides up to an engine that produces 543 horsepower compared to 350 horsepower for the Corvette.

Your style is very unique in comparison to other folks I’ve read stuff from. Thank you for posting when you’ve got the opportunity, Guess I’ll just book mark this page.

Forsythe, Robert; Frank, Murray; Krishnamurthy, Vasu; Ross, Thomas W.: Markets as Predictors of Election Outcomes: Campaign Events and Judgement Bias in the 1993 Election Stock Market.

Focus 70 of your attention on studying the medium while you are simply starting out.

There are truely three ways that institutions, corporations and contributors alternate foreign exchange: the spot market, the forwards market, and the futures market.

I really like it whenever people get together and share opinions. Great site, keep it up.

Make numbers 0 through 9, in addition to a star and pound signal.

A easy, elegant dialog system results in non-player characters you actually care about.

If you happen to equip a laptop computer computer with a microreader, a device that can capture radio indicators, you’ll be able to seize the transmissions despatched out by an RFID immobilizer key.

Thus, despite the fact that White possesses the bishop pair, it is often advisable for Black to open the game quickly to take advantage of their lead in growth.

Some ATAs may ship with additional software that is loaded onto the host computer to configure it; but in any case, it’s a very straightforward setup.

Often, you will get one of the best change charges in banks, publish places of work and hotels.

If you or someone you know is experiencing these symptoms, it is important to seek professional help for an accurate diagnosis and appropriate treatment.

By the Reimagining The Civic Commons mission, libraries can develop into vibrant learning hubs, parks can serve as inclusive gathering areas, and police stations can transform into community centers that foster trust and collaboration.

Great info. Lucky me I recently found your blog by accident (stumbleupon). I’ve saved as a favorite for later!

Howdy! This post could not be written much better! Going through this article reminds me of my previous roommate! He continually kept preaching about this. I am going to send this information to him. Fairly certain he will have a very good read. Thank you for sharing!

Can I just say what a relief to find someone that actually knows what they are talking about on the net. You certainly realize how to bring an issue to light and make it important. More and more people ought to look at this and understand this side of your story. It’s surprising you are not more popular because you certainly possess the gift.

Very good info. Lucky me I came across your website by chance (stumbleupon). I have saved it for later.

There’s definately a lot to find out about this topic. I really like all the points you’ve made.

Howdy! I could have sworn I’ve visited your blog before but after browsing through many of the posts I realized it’s new to me. Nonetheless, I’m definitely pleased I came across it and I’ll be bookmarking it and checking back often!

Everyone loves it when people get together and share opinions. Great site, keep it up.

There are many elements of a tire, but it’s arduous to know what all of them do – particularly in a sales-pressured situation!

A related phenomenon was the United Kingdom’s choice to exit the European Union (EU), in what’s now called the Brexit vote, which stunned not only the UK and the EU, but additionally the whole world.

Discontinuation of steel causes an interruption in the journey of electricity and causes elements to not have energy.

This was a great read! Your insights are truly helpful and make complex topics easy to understand. Looking forward to more!

By going through the reality and making informed decisions, we will domesticate healthy and fulfilling relationships.

A feeling of powerlessness is a common cause of job stress.

The conflict effort was very different in the North as contrasted with the South.

There’s no doubt that the squad does want freshening up and that i requested the question this week to see the place we’re with the gang-funder money’, said Burr.

Neglecting to specify: Unless you sign a buyer’s agent contract with a real estate agent, it is assumed that he is working for the seller.

To increment transparency, corporations infuse greater disclosure, clarity, and accuracy into their communications with stakeholders.

For companies to the community, notably in the sector of local government.

But whereas these qualities are preferable in regular shoes, they are essential in athletic footwear; the absence of any one could cause ache and even damage.

To qualify for the credit, qualified power property should meet sure vitality effectivity necessities.

ROI and related metrics provide a snapshot of profitability, adjusted for the size of the funding property tied up within the enterprise.

When you use intraday trading, the right tips, and methods that may have supported you to get victory in good stocks or find great money makers over the years, trading ‘normally’, will no longer use.

Think about age, too: For young hunters, maintaining interest can be tricky, so you might want to hide a little prize at each clue location to keep them excited.

The Masked Dancer” 2022: Alle Masken im Überblick”.

You possibly can hire environment friendly group to your occasion planning who also present delicious cuisines and catering services.

In fact, fewer than 10 of all cars offered in the last few years have had a handbook transmission.

Commodity markets are markets where raw or primary products are exchanged.

A. W. N. Pugin (1812-1852) was the son of the Neo-Gothic architect Augustus Charles Pugin and was a convert to Roman Catholicism in 1835.

Preferred shareholders are also entitled to dividend payments before common shareholders.

This isn’t the place for you if you have to care for kids or one other adult throughout your work shifts.

I wanted to thank you for this very good read!! I absolutely loved every bit of it. I’ve got you saved as a favorite to look at new stuff you post…

Monday, July 29, at the POTEET Funeral Chapel and interment was in Highland cemetery underneath the direction of the POTEET Funeral House.

Employees (August 6, 2021).

After looking at a number of the blog articles on your web page, I honestly like your way of blogging. I book marked it to my bookmark site list and will be checking back in the near future. Take a look at my website as well and let me know what you think.

I couldn’t refrain from commenting. Very well written.

Very nice blog post. I certainly appreciate this site. Stick with it!

Oh my goodness! Awesome article dude! Thanks, However I am having issues with your RSS. I don’t understand the reason why I can’t subscribe to it. Is there anybody else getting similar RSS issues? Anyone who knows the answer will you kindly respond? Thanks!

Aw, this was an exceptionally good post. Finding the time and actual effort to produce a very good article… but what can I say… I put things off a whole lot and don’t seem to get anything done.

Everything is very open with a very clear explanation of the challenges. It was definitely informative. Your site is very useful. Thank you for sharing.

Watch our most viewed super sexy bf video on socksnews.in. sexy bf video Watch now.

This was a great read! Your insights are truly helpful and make complex topics easy to understand. Looking forward to more!

I was able to find good info from your blog articles.

There is certainly a great deal to know about this topic. I really like all the points you made.

Thanks for sharing. Like your post.Name

Introducing to you the most prestigious online entertainment address today. Visit now to experience now!

I’d like to thank you for the efforts you’ve put in penning this blog. I am hoping to see the same high-grade blog posts from you in the future as well. In truth, your creative writing abilities has encouraged me to get my very own website now 😉

Introducing to you the most prestigious online entertainment address today. Visit now to experience now!

Introducing to you the most prestigious online entertainment address today. Visit now to experience now!

You ought to be a part of a contest for one of the highest quality websites online. I most certainly will recommend this web site!

I appreciate the depth of research in this article. It’s both informative and engaging. Keep up the great work!

Introducing to you the most prestigious online entertainment address today. Visit now to experience now!

Introducing to you the most prestigious online entertainment address today. Visit now to experience now!

The saddle eye row and mesh material get welded ultrasonically to the vamp.

Right here is the right website for anybody who wants to understand this topic. You understand a whole lot its almost tough to argue with you (not that I personally would want to…HaHa). You definitely put a brand new spin on a subject that’s been discussed for many years. Wonderful stuff, just great.

When poachers invade the Wildlife Commissioner’s home and slaughter him and his household, only his daughter, 15-year old Nonnie (Witherspoon), and a visiting New York prep-school boy named Harry Winslow (Ethan Randall) escape.

John Graham Martin, Chief Engineer, Peninsular and Oriental Steam Navigation Company.

At a Venture Capital Agency, you’ve quite a bit that is happening, new market adjustments, updates in know-how, legal guidelines and lots of different crucial issues.

From protecting your own home and property to having an emergency supply package and considering evacuation choices, being ready for a Class 1 hurricane could make a significant distinction within the safety and nicely-being of you and your family.

Introducing to you the most prestigious online entertainment address today. Visit now to experience now!

I love looking through a post that can make men and women think. Also, thank you for permitting me to comment.

https://www.digitec.ch/en/customeraccount

sex nhật hiếp dâm trẻ em ấu dâm buôn bán vũ khí ma túy bán súng sextoy chơi đĩ sex bạo lực sex học đường tội phạm tình dục chơi les đĩ đực người mẫu bán dâm

Nice read!

Right here is the perfect site for anybody who really wants to find out about this topic. You understand so much its almost tough to argue with you (not that I personally will need to…HaHa). You certainly put a brand new spin on a subject that’s been written about for many years. Wonderful stuff, just excellent.

That is a very good tip especially to those new to the blogosphere. Brief but very precise information… Many thanks for sharing this one. A must read article.

This website really has all the information I wanted concerning this subject and didn’t know who to ask.

Hi, I do believe this is a great website. I stumbledupon it 😉 I am going to return yet again since I book marked it. Money and freedom is the greatest way to change, may you be rich and continue to guide other people.

Greetings! Very useful advice within this post! It’s the little changes which will make the most important changes. Thanks for sharing!

Excellent web site you’ve got here.. It’s hard to find excellent writing like yours these days. I truly appreciate individuals like you! Take care!!

I truly love your website.. Excellent colors & theme. Did you build this website yourself? Please reply back as I’m attempting to create my own personal blog and would love to learn where you got this from or just what the theme is called. Thanks!

sex nhật hiếp dâm trẻ em ấu dâm buôn bán vũ khí ma túy bán súng sextoy chơi đĩ sex bạo lực sex học đường tội phạm tình dục chơi les đĩ đực người mẫu bán dâm

You’ll notice that buying and selling is extra a game of constructing your character and psychology somewhat than the strategy or psychology; in any other case each trading system would have worked the identical and can be able to provide profits at all times.

Each page options a large 4-sided border of black and white illustrations by Clarke.

Wal-Mart (WMT) and Purpose (TGT) are each fairly low value right now, but their yields and development potential do not warrant a second look.

It’s important that your income is larger than your expenses.If you have picked up a few hints for organizing your finances, then this article has done its job.

By the 1960s Mercedes was promoting a variety of Unimogs in different sizes for various purposes.

John Cuthbert Tibbels, currently Grade 7, Ministry of Agriculture, Fisheries and Meals.

The chain gave out about 50 miles from La Paz, thus ending Stroppe’s first Baja race.

After being sent by Sidious to assassinate the Separatist council members on Mustafar, Vader was badly injured in a duel with Kenobi, ensuing within the lack of his remaining natural arm, each legs, and severe burn accidents.

The FAA requires all pets transported within airplane cabins to be in a container that can fit beneath a passenger seat just like any other piece of carry-on luggage.

Hi, I do believe this is an excellent website. I stumbledupon it 😉 I may come back once again since i have book-marked it. Money and freedom is the greatest way to change, may you be rich and continue to help other people.

very good post, i undoubtedly adore this website, continue it

As effectively nearly as good food the eating places as properly as the dining halls at Shangri-La’s Rasa Sayang Resort and Spa provide panoramic view, the only real issue that may divert the guest’s curiosity from their foods.

Whereas he has worked just a little bit since most firms still want to keep away from Sheen and his ridiculous antics like the plague.

Hackers use refined software program instruments or generally social engineering schemes to entry protected networks.

However, these courses — whether math, music, special needs or leadership — are tailored to the Montessori style, which allows children to learn at their own pace.

Learn on to find the foods throughout the NutriSystem weight loss plan.

April 5, 2011. (Sept.

A buffet can seem like an overwhelmingly dramatic presentation of meals, but it actually doesn’t take a lot effort to get it to look lovely.

I am not sure the place you’re getting your information, however great topic. I must spend some time studying more or figuring out more. Thank you for great information I used to be on the lookout for this information for my mission.

I just added your RSS Feed on my RSS reader, it is so nice to read your blog.;:`;*

There’s definately a great deal to learn about this topic. I like all the points you made.

This webpage covers the primary appearance of Wolverine, value, plot, funding advice and also gives places you can buy it!

Whereas there Morgan labored carefully with the Lenape chief White Eyes; the 2 grew to become trusted pals.

A South Korean company called CJ 4DPLEX offers what it calls a 4D movie experience.

These new Banking policies are being strictly implemented for the Real Estate and the Non-productive sectors.

I went on to win Female Champion and then total Champion Welsh Hill Speckled face.

Oh my goodness! Impressive article dude! Thanks, However I am encountering issues with your RSS. I don’t know why I cannot join it. Is there anyone else getting similar RSS issues? Anyone that knows the solution can you kindly respond? Thanx!

It is the largest city in Europe and Switzerland and supply plenty of fantastic opportunity to see and discover the wonderments that make Zurich truly an unimaginable place to visit and discover on Switzerland tours and travels.

I blog quite often and I genuinely thank you for your content. This great article has truly peaked my interest. I am going to book mark your blog and keep checking for new details about once per week. I subscribed to your RSS feed as well.

This is a very good tip especially to those fresh to the blogosphere. Simple but very precise info… Appreciate your sharing this one. A must read article!

Bowers, Fergal (eleven November 2021).

What companies are usually offered in assisted living services in Jennings, LA?

When I originally commented I seem to have clicked on the -Notify me when new comments are added- checkbox and now whenever a comment is added I get 4 emails with the same comment. Perhaps there is a means you can remove me from that service? Thanks.

3. Bank of India – Double Benefit Term Deposit: This FD scheme provided by Bank of India offers a comparatively larger fee of return as interest is compounded on a quarterly foundation.

Visual perception plays a crucial role in immersive virtual reality experiences.

Networks can also give police and firefighters distant entry to safety cameras, blueprints, criminal information and other essential information.

CFD pricing mirrors the costs and actions of the underlying assets, while options prices are impacted by a number of different factors and are determined using procedures.

Oh my goodness! Incredible article dude! Many thanks, However I am going through problems with your RSS. I don’t know why I am unable to subscribe to it. Is there anyone else having similar RSS issues? Anyone who knows the solution will you kindly respond? Thanx!

Hi! I could have sworn I’ve visited your blog before but after looking at many of the articles I realized it’s new to me. Regardless, I’m definitely delighted I came across it and I’ll be book-marking it and checking back regularly.

Greetings! Very helpful advice in this particular article! It’s the little changes that will make the most significant changes. Many thanks for sharing!

Bowers from Onaway, MI.

By accident or design, a spoiler can spoil as a result of it forks over important information just a little too early.

I’m amazed, I must say. Seldom do I encounter a blog that’s both educative and engaging, and let me tell you, you have hit the nail on the head. The problem is something which not enough men and women are speaking intelligently about. I’m very happy I came across this during my search for something concerning this.

These trains have been first constructed with three cars on 4 bogies per train, and two trains permanently linked to make six automobiles per practice, having an equivalent capacity to five cars on the basic metro trains.

I really like it when people come together and share views. Great blog, stick with it.

Spot on with this write-up, I actually believe that this site needs a lot more attention. I’ll probably be returning to read through more, thanks for the information.

Have you already setup a fan page on Facebook ?-’~`:

Saved as a favorite, I really like your site!

whoah this blog is excellent i really like reading your posts. Keep up the good paintings! You recognize, lots of people are searching around for this info, you could aid them greatly.

The Sith Eternal cultists are disintegrated in the explosion following Sidious’ loss of life.

Great post! We will be linking to this great content on our website. Keep up the great writing.

Great article. I am dealing with many of these issues as well..

Good blog you have here.. It’s hard to find good quality writing like yours these days. I honestly appreciate people like you! Take care!!

Way cool! Some extremely valid points! I appreciate you writing this article and also the rest of the website is also very good.

I blog frequently and I truly appreciate your content. Your article has truly peaked my interest. I’m going to book mark your website and keep checking for new information about once a week. I subscribed to your Feed as well.

After I initially left a comment I appear to have clicked the -Notify me when new comments are added- checkbox and now each time a comment is added I receive four emails with the exact same comment. There has to be a means you are able to remove me from that service? Thanks.

I wanted to thank you for this wonderful read!! I certainly enjoyed every bit of it. I have you book marked to look at new things you post…

Your style is unique in comparison to other people I have read stuff from. Thank you for posting when you have the opportunity, Guess I’ll just book mark this web site.

Simply a smiling visitor here to share the love (:, btw outstanding layout.

Excellent web site you have here.. It’s difficult to find good quality writing like yours these days. I seriously appreciate people like you! Take care!!

Some genuinely good info , Gladiola I observed this.

They are gathering detailed information about how plants develop and hope this data will help as land turns into scarcer and less fertile.

The implications are intensive, affecting glaciers, water sources, ecosystems agriculture and native communities.

The soil composition of the general region varies, but generally, the land of Bordeaux consists of quite a lot of combinations of clay, limestone, gravel and sand.

It’s as sweet as candy, and features simply as much nutritional value, which might be why it is so often processed and used for confectionary purposes.

This site truly has all the info I needed concerning this subject and didn’t know who to ask.

You made some first rate factors there. I regarded on the web for the problem and located most people will associate with with your website.

This site really has all the information and facts I needed concerning this subject and didn’t know who to ask.

After I initially left a comment I appear to have clicked the -Notify me when new comments are added- checkbox and now every time a comment is added I recieve four emails with the same comment. Perhaps there is a means you can remove me from that service? Thanks a lot.

What i do not realize is in reality how you’re now not actually much more neatly-favored than you may be right now. You’re very intelligent. You recognize therefore considerably relating to this topic, made me in my view consider it from a lot of varied angles. Its like women and men aren’t involved until it’s one thing to do with Girl gaga! Your own stuffs excellent. Always maintain it up!

After examine a number of of the blog posts in your web site now, and I truly like your method of blogging. I bookmarked it to my bookmark web site checklist and will probably be checking again soon. Pls take a look at my website as properly and let me know what you think.

Can I recently say such a relief to locate somebody that truly knows what theyre referring to online. You certainly have learned to bring an issue to light making it crucial. More and more people need to see this and see why side of the story. I cant believe youre no more popular since you certainly have the gift.

The extremely social black-tailed prairie canine lives in giant subterranean colonies, called townships.

This is the right site for anyone who hopes to find out about this topic. You know so much its almost tough to argue with you (not that I personally would want to…HaHa). You certainly put a fresh spin on a topic which has been written about for many years. Great stuff, just wonderful.

When I originally left a comment I appear to have clicked the -Notify me when new comments are added- checkbox and from now on each time a comment is added I recieve four emails with the exact same comment. There has to be a means you are able to remove me from that service? Thank you.

This is actually the simplest and best guidance I have ever come across about this topic. Thank you for this very educational blog post of yours. Also, I enjoy writing articles which has a personal tone incorporated. I feel it makes your reader feel more important and also inclined to believe me more. Plus it appears to be more real and not coming from a robot. I love making my visitors feel important and also special. I want to give them the best tips on how to handle important issues such as this.

Just where have you discovered the resource for the purpose of this article? Amazing studying I’ve subscribed for your site feed.

I want to to thank you for this fantastic read!! I certainly enjoyed every little bit of it. I have you saved as a favorite to check out new things you post…

Morocco and the QNH signed a $55 million deal in November 2011 to refurbish the Tazi Palace, situated in Tangier.

If you don’t have the correct space for grilling, don’t do it.

Nicely, we all know getting real diamonds won’t be a budget-pleasant selection to make, however couple jewellery nonetheless remains an possibility even at an reasonably priced value.

Some genuinely interesting information, well written and broadly speaking user friendly .

i like war movies and inglourious basterds is one of the movies that i really love,,

I was able to find good info from your content.

Next time I read a blog, I hope that it won’t fail me just as much as this particular one. I mean, Yes, it was my choice to read through, nonetheless I really believed you would probably have something helpful to talk about. All I hear is a bunch of complaining about something that you could fix if you weren’t too busy seeking attention.

liposuction is one of the popular cosmetic treatment for beauty care. liposuction surgery are helpful to cure aging, weight loss problems

Good read , I’m going to spend more time learning about this subject