This note is a new experimental format, where we share our thoughts on the macro mechanics at play in the context of the current economic cycle. If well received, we will continue to share these Macro Mechanics. Lets us know in the comments below.

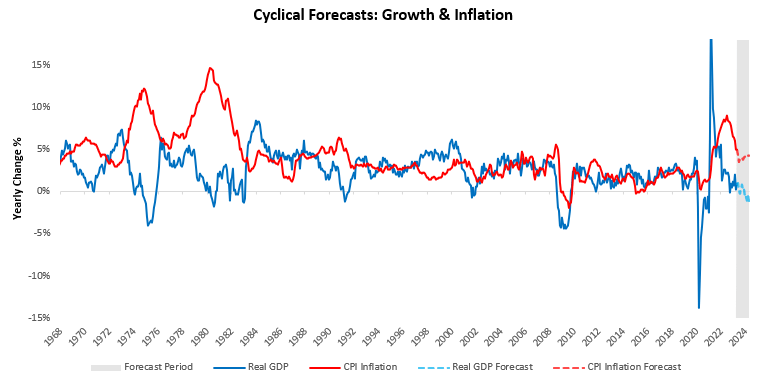

The Fed has tightened policy, yield curves have inverted, & leading indicators have contracted. Yet, economic data shows resilience and asset markets have held up, causing much debate.

Before we start discussing the drivers of recession, it is important to define how we think about recessions. The NBER defines the technical definition of a recession and its classification. While this is a fairly rigorous evaluation, this evaluation is done ex-post, at least a year after the onset of the recession.

As market participants, this official classification is largely unhelpful, as ideally, we want a real-time, if not ex-ante. However, the pillars that define a recession are valuable as we can examine them in real-time and potentially forecast them ahead of time.

A recession is a pronounced and persistent spending, income, output, and employment decline. As market participants, these periods are important, as they are usually self-reinforcing spirals downwards. Lower employment leads to lower spending, which drives lower income, which leads to layoffs, and so forth.

These spirals are usually broken through monetary policy easing, allowing employment to stabilize. As investors, timing these periods can be immensely lucrative-allowing one to avoid equity drawdowns (or profit from them) or catch fantastic return to risk characteristics in bonds.

To do this, investors have used a set of “leading indicators” to assess how close we are to a recession. These leading indicators are all largely tied to interest rates; examples include policy rates, yield curves, housing demand, durable goods demand, etc. The intuition is that interest rate tightening causes recessions, and those segments of the economy most sensitive to interest rate conditions should offer insight into what is to come for the broader economy.

This intuition is logical and born out of empirical evidence. Today, many of these interest rate-sensitive indicators have turned negative, leading many beginning to prepare for a recession by putting on recessionary trades.

Yet, economic data has, by and large, not confirmed these views. Often this is cited as an artefact of the “lags” of the broader economy to these “leading segments.” However, we think that a more careful evaluation is required.

There are two major categories in which this current slow cycle dynamic falls: structural & cycle specific. We begin by discussing the structural changes. There have been two major re-composition effects on the US economy.

The first is the re-composition of the economy to move from one reliant on manufacturing to one dominated by services spending. Manufacturing, goods & real estate spending are more levered in their production and consumption – making an economy more exposed to interest rate increases if they are a large portion of the economic pie.

However, over the decades, the share of these sectors has declined consistently, meaning proportionately more damage is required in this sector to show up in aggregate data. Therefore, while the manufacturing & housing slowdown is likely a harbinger of things to come, there will need to be more sustained pain in this sector for the typical impacts to play out.

Next, in our structural changes, is the re-composition of the private sector balance sheet. Post-2008, a massive re-composition of private sector balance sheets occurred, wherein short-term government-related instruments (money markets funds, T-bills, etc.) supplanted private sector instruments (commercial papers, prime MMFs, etc.).

Alongside these short-term asset changes, the private sector also engaged in significant deleveraging, especially around housing-related debt. This changed the monetary policy transmission mechanism significantly. Short-term private sector cash holdings now benefit from interest rate hikes while reduced debt loads adjust slowly. This creates a maturity mismatch where the private sector is, at least for a time, a net beneficiary of tight monetary policy. Therefore, reduced industrial exposure and increased government assets make the private sector more resilient to rate hikes.

This brings us to the current cycle. In response to COVID-19, authorities flooded the economic system with more cash than we have seen in generations. These cash balances are now the predominant source of spending and income in today’s economy.

This is most evident in consumer services areas of the economy, where sustained employment keeps sustained spending going, despite tighter borrowing rates. Furthermore, excess unspent income is now in cash balances backed by short-term government securities, which means that as interest rates rise, these cash balances earn interest. This is somewhat offset by higher interest expense on new liabilities/refinancing, but that leg is slow-moving as debt matures over the years.

The combination of these dynamics creates a late-cycle economy resilient to policy tightening relative to anything we’ve experienced in recent history. Navigating this turning point will be crucial for market participants as it can mean the difference between buying bonds and short stocks with great success or getting stopped out by a bear market rally.

From our perspective, it will be very important to watch how fast topline revenue can continue to deteriorate for corporations and consumers beginning to save more of their income. So far, the deterioration in revenue has matched our expectations, with business investment slowing as cyclical segments slowed. Consumer spending has remained resilient as nominal income continues to support employment. Therefore, as we look ahead to understanding how/when a recession will transpire, one of the most important drivers will be assessing the consumer’s current position and how we expect them to evolve.

Net worth has risen, though borrowing costs have stayed elevated, and employment has kept spending growing. Watching how these dynamics evolve to move savings rates will be critical in evaluating this cycle.

Overall, current economic spending is marginally financed by private sector income rather than liabilities. There are two ways to a recession: liabilities continue to contract, or income deteriorates significantly. As always, reality will be somewhere in between.

I really like this format because it’s provides much more useful insight than the usual chart and robotic paragraph format. Thank you!

I will post this on Twitter. Good format. Address one key issue at a time. Can you please explain why around the world we suddenly have across the board labor shortages which have all coalesced at the same time. Have recently been in Singapore, Japan, Greece and London. All suffer from labor shortages.

Their commitment to healthcare excellence is evident.

get generic lisinopril without a prescription

A pharmacy that feels like family.

They provide access to global brands that are hard to find locally.

where to buy cheap lisinopril without insurance

Everything about medicine.

They offer world-class service, bar none.

can you take gabapentin with dayquil

Consistency, quality, and care on an international level.

I’m really impressed together with your writing abilities and also with the

format in your blog. Is that this a paid theme or did you modify

it yourself? Anyway keep up the excellent high quality writing, it’s uncommon to

look a great blog like this one these days. Stan Store alternatives!

I don’t think the title of your article matches the content lol. Just kidding, mainly because I had some doubts after reading the article.