If you haven’t already, make sure to check out our first podcast! For our first episode, our Founder, Aahan Menon, is joined by a very special guest: Darius Dale, Founder & CEO of 42 Macro. Darius is one of the best quantitative macro minds out there and runs one of the best macro research firms in the business. The conversation covered a wide variety of topics, from the underlying mechanics of a systematic macro approach to the current outlook on markets.

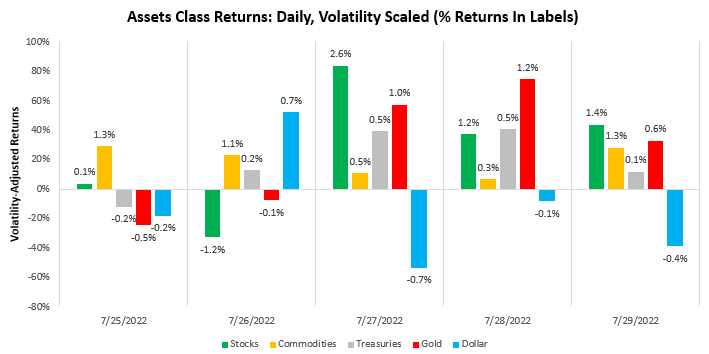

Last week, we saw markets race to price in rising nominal growth, with commodities surging all week. These moves came amidst policymakers at the Fed signaling that they will remain data-dependent on gauging inflation but are very close to their estimated level of neutral rates (a level of interest rates that do not facilitate further inflation). Given high levels of realized inflation, this benign estimate of neutral implied a far more dovish outlook than most expected, resulting in a rally in risk assets. We show the evolution of price action over the week below:

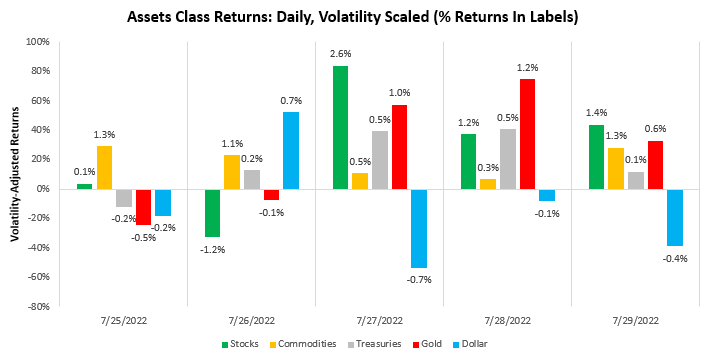

Our systems aggregate market moves to asses what markets are telling us about the current market environment, i.e., the market regime. Our monitors continue to tell us we are in a tightening liquidity environment with high nominal growth. We show this below:

Over the last month, we have seen a significant surge in growth assets (commodities, equities, credit). However, our systems consider these moves as counter-trend moves relative to the underlying economic fundamentals. Our systems’ fundamental tracking & forecasting of economic data continue to show that we are on a downwards trajectory for real growth, a deterioration in inflation acceleration, and sustained weakness in liquidity conditions. Economic data may bounce relative to expectations, but the probability of decelerations remains strong.

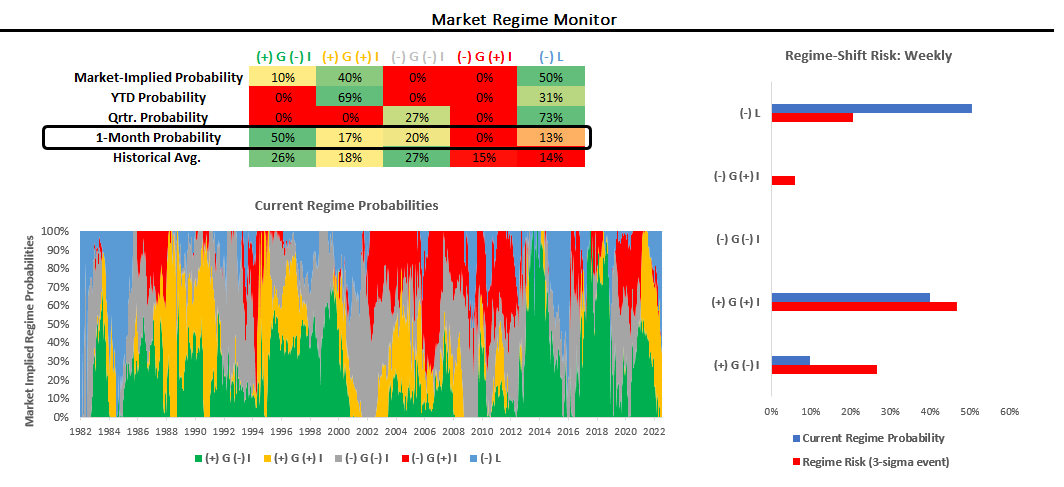

For our ETF Strategy users, we apologize for the interruption this week in coverage. We are in the process of system upgrades for both the ETF Strategy & Alpha Strategy and will resume coverage next week. In the meantime, a significant development in our ETF Strategy is that our systems have now moved to net long positioning on equities & credit, i.e., we have on both longs and shorts, netting to neutral now. We show this below:

These changes are largely a function of short-term regime dynamics and risk mitigation built into our systems. The fundamental direction for equities & credit remains lower. However, we wait for our systems to trigger aggressive shorts once again. We show the positions at the security level:

-

Stocks: SPY (3%), XLP (-3%), XLY (2%), XLC (-3%), XLV (3%), XLB (-3%), XLI (3%), XLK (2%), XLF (-3%), XLU (3%), XLE (2%)

-

Commodities: USO (2%), UGA (2%), UNG (1%), GLD (4%)

-

Fixed Income: GOVT(8%), TLT (3%), IEF (6%), SHY (27%), MBB (8%), HYG (5%), TIP (7%),

-

Currencies: UUP (8%)

We now turn to the week ahead and highlight our systems expectations to help risk-manage these positions. Below, we show the upcoming week in terms of US economic data:

-

Monday: S&P Global Manufacturing, Construction Spending, ISM Manufacturing

-

Tuesday: JOLTS Job Openings

-

Wednesday: MBA Mortgage Apps, S&P Services PMI, Durable Goods Orders, ISM Services

-

Thursday: Trade Balance, Jobless Claims

-

Friday: Payrolls, U-Rate, Labor Force Participation, Consumer Credit

We go through the top items point-wise:

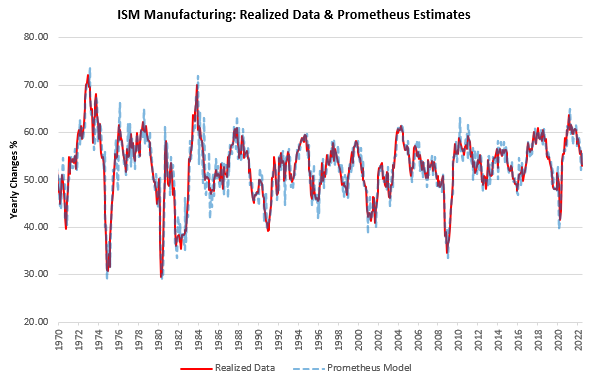

i. ISM data has significant potential to surprise expectations, despite being in a downtrend. The level of ISM data tends to be reasonably stable relative to recent history. We offer our estimates for the level of ISM before the print below:

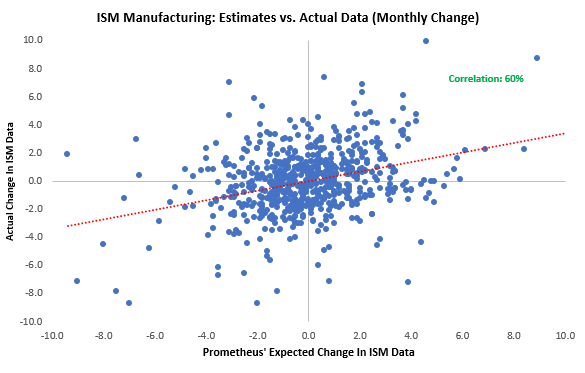

However, there is considerably more volatility in the monthly changes in the ISM Index. Nonetheless, our systems are able to forecast this with some success based on other fundamental data. These estimates are telling us that there is a significant potential for ISM Manufacturing data next week to surprise consensus expectations. Consensus expects ISM Manufacturing to decline by 2.5 points to 52, and our estimates suggest a 92% chance of a surprise based on the historical track record of our system. However, we must take this with a grain of salt, as even our estimates are often wrong. We show the correlation between our estimates for the change in ISM versus the realized data below:

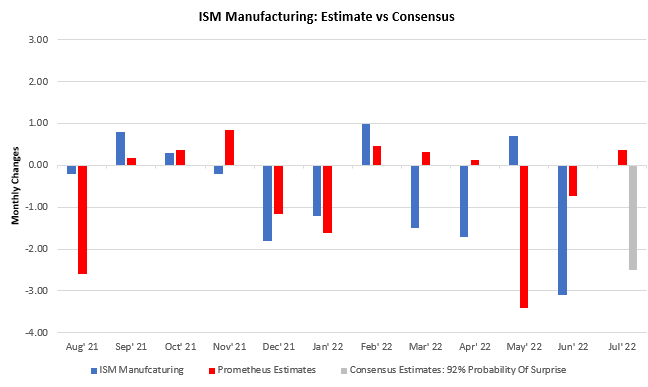

We also show the recent history of our estimates relative to realized data & consensus expectations:

This print will be necessary for markets to assess the economic outlook; therefore, careful risk management here is important.

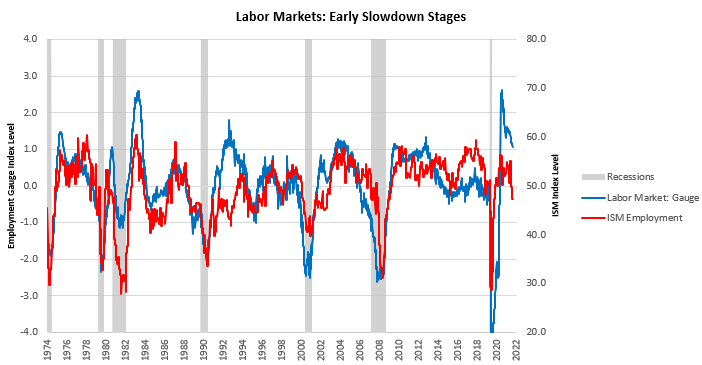

ii. ISM employment likely to deteriorate ahead of payrolls. Our labor market gauge aggregates employment and unemployment-related data into a single aggregate allowing us to estimate the impulse in labor markets. This high-frequency gauge has allowed us timely insight into labor conditions and is flagging the potential for further weakening in ISM employment data (both manufacturing & services):

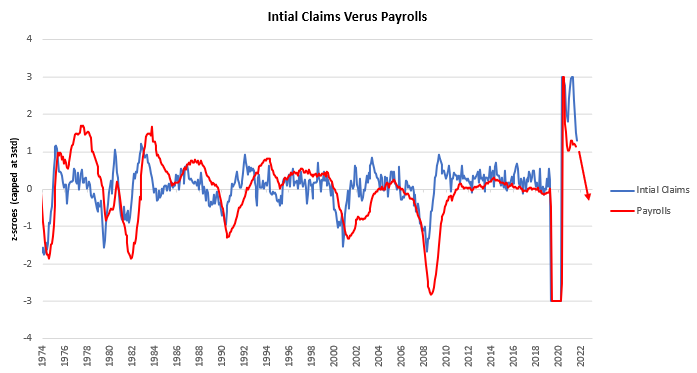

iii. Nonfarm payrolls remain the dominant force behind sustained nominal income, but the pressure is mounting for declines. We see the initial stages of this pressure building in initial claims data, suggesting that there is more pressure on payrolls growth the decelerate further:

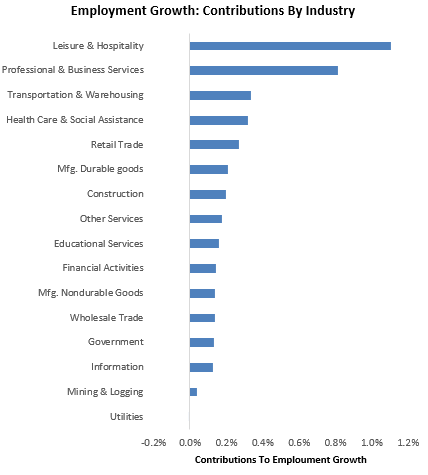

In particular, we will be looking at the composition of labor market data to get a sense of the durability of employment. Labor market growth is currently concentrated in the leisure and hospitality business, which remains exposed to a cyclical slowdown in discretionary spending:

Our tracking of conditions continues to tell us tough times are ahead for the real economy. While markets have paused in their descent, they remain exposed to the path of economic data, which is likely to be still weaker. We remain defensive. Stay Nimble.

The best in town, without a doubt.

how to buy lisinopril pill

Drug information.

They have a great range of holistic health products.

informacion de gabapentin en espanol

Their commitment to global patient welfare is commendable.

Get warning information here.

can i purchase cheap cipro without prescription

Consistent excellence across continents.

Their compounding services are impeccable.

get cheap clomid no prescription

Always on the pulse of international healthcare developments.

A pharmacy that takes pride in community service.

where buy clomid without a prescription

Read information now.

Efficient, effective, and always eager to assist.

can i buy cheap cipro for sale

The staff always ensures confidentiality and privacy.