Equity markets continued their descent last week; however, commodities and treasuries sold off alongside equities. Our systematic lenses qualify these moves as indications of tightening liquidity, i.e., an environment where cash outperforms risk assets. Consistent with this fundamental thinking, the dollar was the best performing macro asset last week. These moves took place alongside the Federal Reserve moving to hike interest rates by 75 basis points, an incremental tightening whose size we haven’t seen in decades. We examine these events through our systematic lenses below.

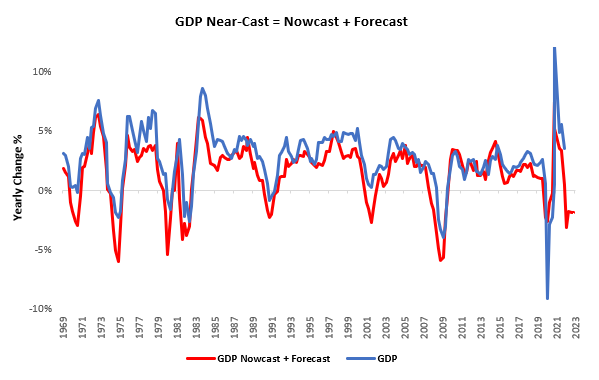

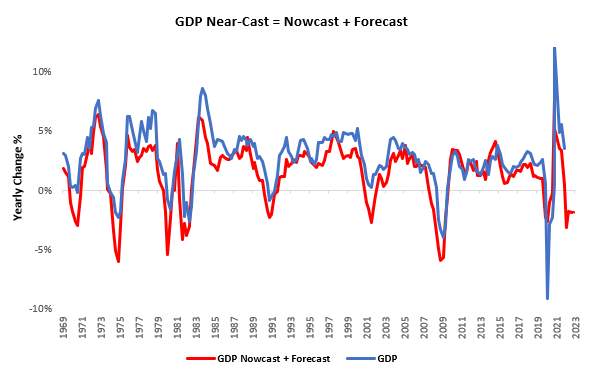

i. Growth continues to decelerate and is likely to get worse. Our GDP nowcasts estimate GDP Growth of approximately 0.5%-0.9%, a further determination in growth rates. Furthermore, our systematic forecasts point to further deceleration in the cards. We show our “Near-Cast,” which combines a GDP Nowcast plus a systematic forecast for GDP below.

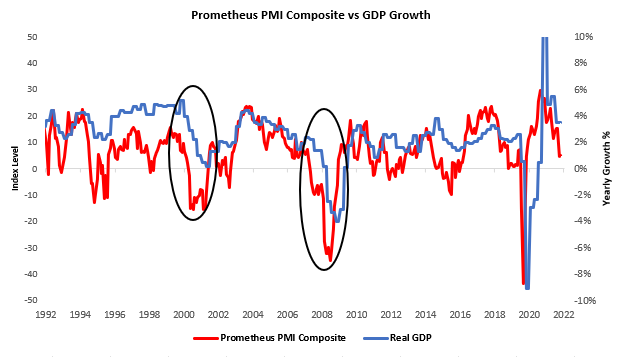

Our tracking of PMI data corroborates these forecasts. We aggregate PMIs across the US into a single composite PMI gauge, allowing us to get a better sense of what the sum of all survey data is telling us about the current state of the economy. PMI data tends to be more cyclically sensitive and move ahead of official GDP data. We show how our PMI Composite typically leads GDP cycles below:

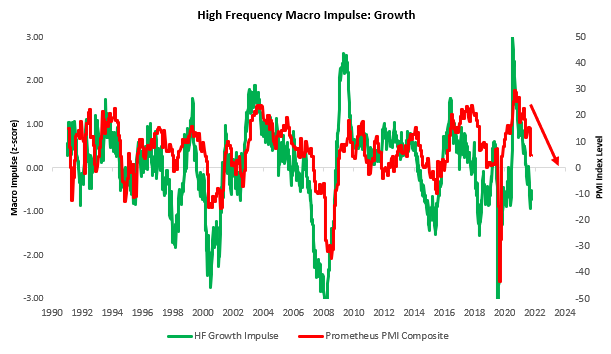

Additionally, our proprietary High-Frequency measures of economic growth tell us that PMIs are likely to move lower:

Putting all these measures together, our systems find it highly likely that economic growth will continue to deteriorate. For the time being, economic activity remains upheld by an extremely tight labor market. However, low unemployment rates create the conditions necessary for spiking unemployment, especially when real wage growth remains negative. We continue to monitor labor incomes and other dynamics to confirm slowdown conditions further.

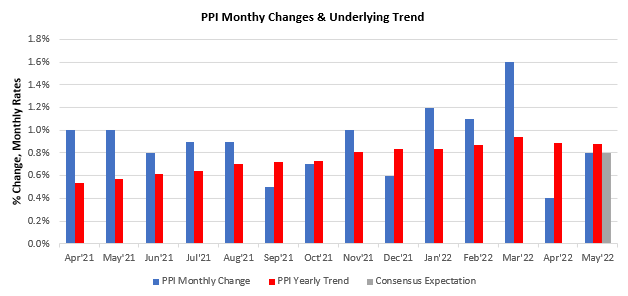

ii. Inflationary pressures remain elevated and are spreading to “sticky” areas. What started with energy costs is now migrating to consumer services. Most recently, PPI data showed a monthly increase of 0.8%, leading to a 10.5% change versus a year ago, in line with consensus expectations. This reading was a sequential deceleration within an accelerating trend 12-month trend.

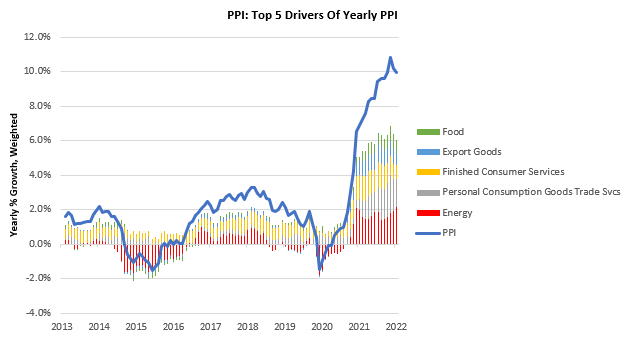

Food & personal consumption goods and services are major contributors to ongoing price increases.

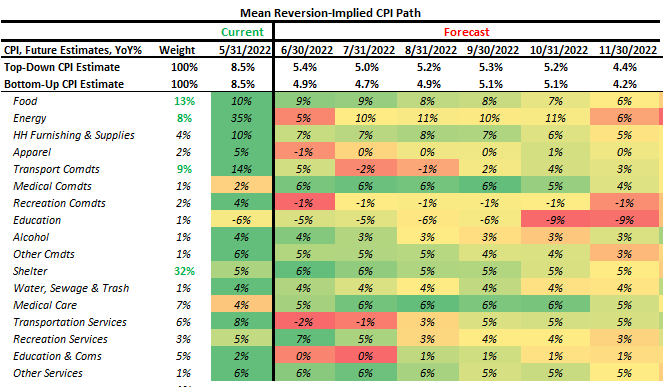

This broad-based price increase is consistent with what we see in CPI. Even if we strip out energy from the latest PPI print, we still have PPI at approximately 7.5%, suggesting that price increases are now widespread. Furthermore, when we actually dig down into CPI on an item-by-item basis and then forecast a reversion to a slower rate of inflation, we still find CPI at greater than 4%. This forecast is consistent whether we forecast CPI by itself or if we forecast each item from the bottom-up:

Aggregating this information, our systems continue to tell us we are in an inflationary environment and will likely remain so for the next few months. We continue to allocate to hedge this substantially underpriced risk.

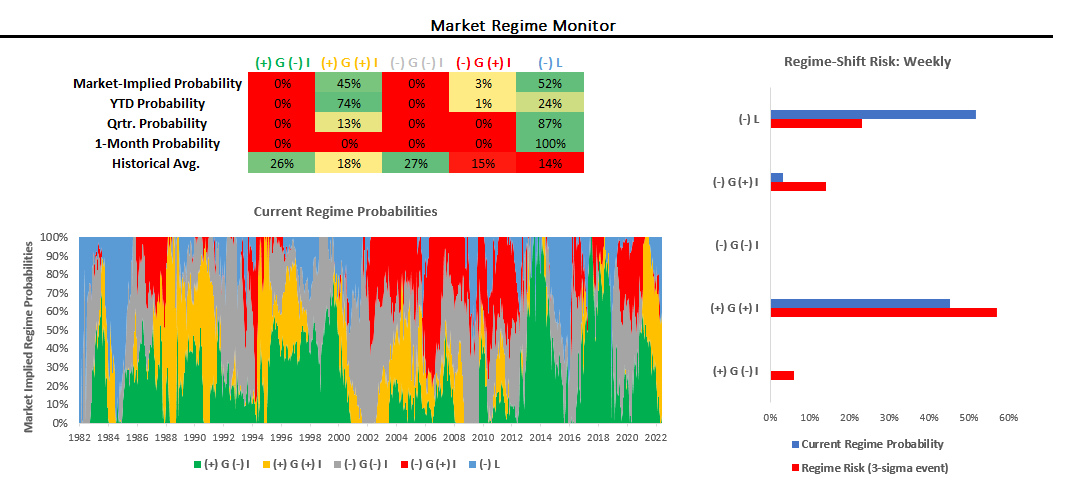

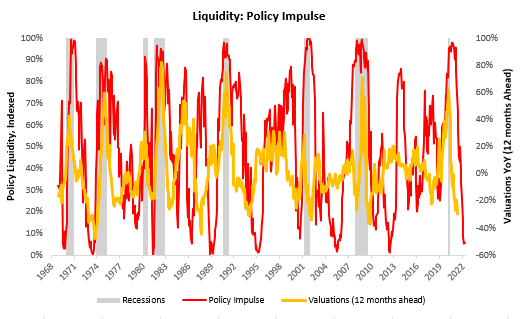

iii. Markets have moved to price tightening liquidity conditions, i.e., kryptonite for risk assets. We show our market regime monitors below:

Our market monitors use our understanding of market-implied moves to assess the current market environment. Most recent market moves have confirmed that markets are dominantly pricing tightening liquidity conditions, though stagflationary growth remains in the picture. Environments of tightening liquidity have historically been extremely tough on equity markets through the channel of contracting valuations. We show this below:

Liquidity conditions tend to lead the market cycle by approximately twelve months, and with liquidity conditions remaining bleak, we think there remains room for asset markets to deteriorate further. This dynamic can only be reversed by either an increase in fiscal expenditures (i.e., more inflation) or a reversal in the monetary policy path. We find this unlikely and therefore continue to position for stagflation and tightening liquidity.

Turning to the week ahead in economic data:

-

Tuesday: Existing Home Sales

-

Wednesday: Powell Testimony

-

Thursday: Initial Jobless Claims, Fed Powell, Crude Oil Invt

-

Friday: New Home Sales, Markit Composite PMI

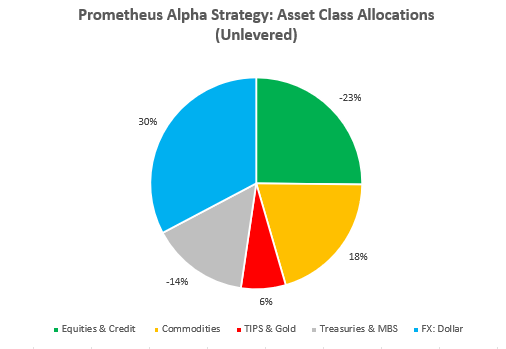

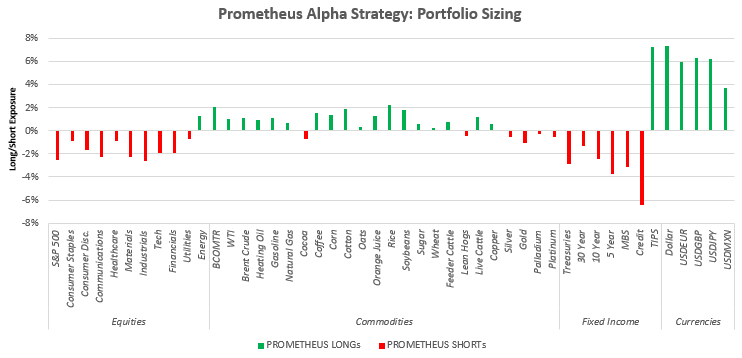

Our systems continue to expect PMIs to deteriorate. Further, we will monitor labor market data carefully to better assess the consumer’s status. Heading into next week, here’s how our systems have positioned our Alpha Strategy at the asset class level:

Our systems algorithmically combine the principles underlying our analysis of economic and market conditions to create rules-based investment portfolios. Today, we find ourselves at a unique junction in modern history, one where Treasuries have not acted as a haven during a period of tightening liquidity. We attribute this to rampantly high inflation, which we expect can remain elevated far longer than most traditional asset allocations can stay solvent. Whether or not Treasury performance will converge to historical norms remains in question. However, our systems continue to think that the fundamental backdrop and existing market environment favor fixed-income shorts. There will come a time when Treasury assets return to their typical price behavior, but that will likely take place only once inflation has been tamed in the eyes of the markets. However, the current regime has proven far more resilient than market participants expected, and our bias remains to stay with the current regime, especially when it remains well supported.

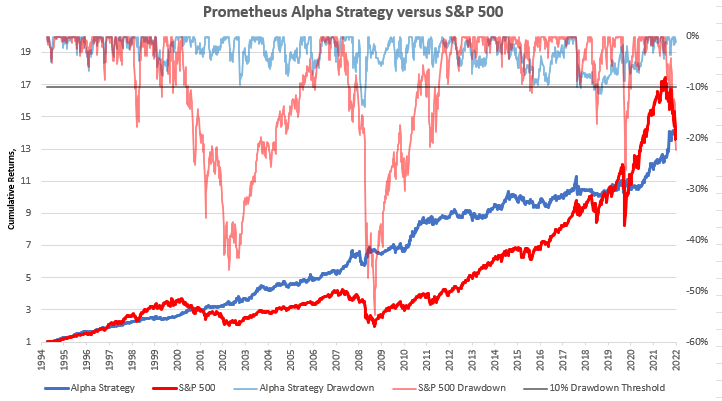

Below, we show the Alpha Strategy’s cumulative performance after considering transaction & leverage costs. The Strategy dynamically uses leverage to target volatility of approximately 10% and is currently leveraged to 1.77x and continues to perform well in this environment.

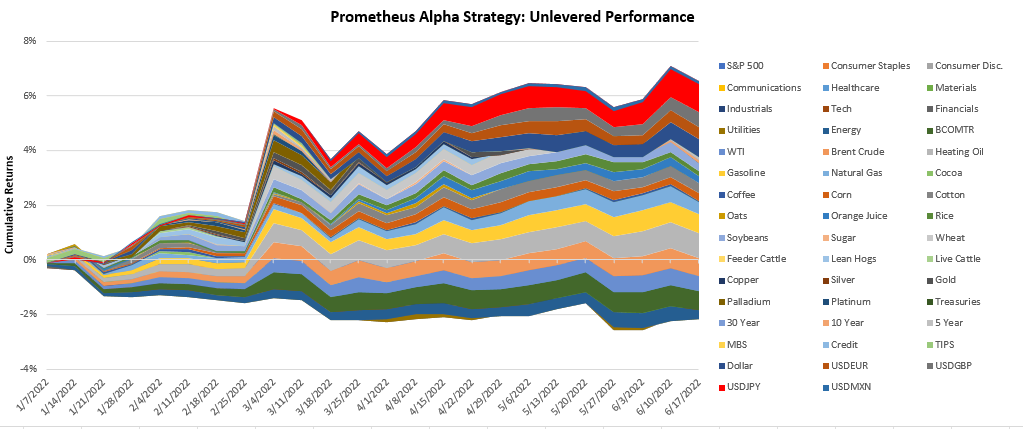

On a year-to-date basis, the Strategy has returned strong relative returns on a levered and un-levered basis. We show the year-to-date performance of the strategy below:

Here is how our systems are positioned heading into this week:

Remember, this is a time for capital preservation and active shorting. There will come a time when we will need to reverse our positions and purchase risk assets in earnest. However, we need to manage portfolio drawdowns in the interim. Stay nimble!