If you haven’t already, make sure to check out our first podcast! For our first episode, our Founder, Aahan Menon, is joined by a very special guest: Darius Dale, Founder & CEO of 42 Macro. Darius is one of the best quantitative macro minds out there and runs one of the best macro research firms in the business. The conversation covered a wide variety of topics, from the underlying mechanics of a systematic macro approach to the current outlook on markets.

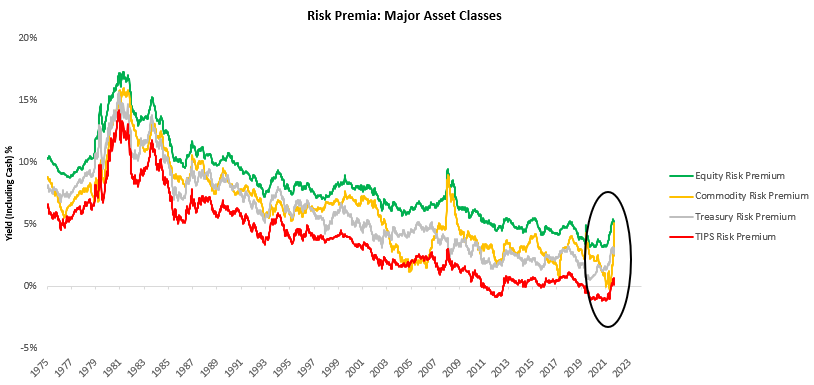

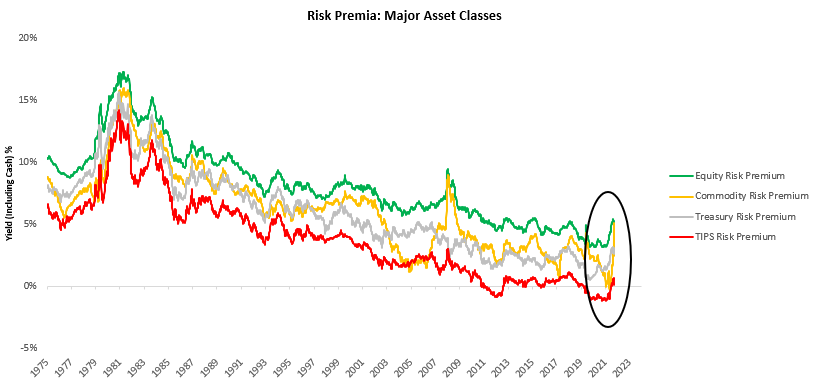

Last week, risk assets struggled, with the dollar showing strength while commodities sold off. As liquidity from the Federal Reserve and the Treasury tighten, we continue to witness an elevation in risk premia. We offer our estimates of major asset class risk premia below:

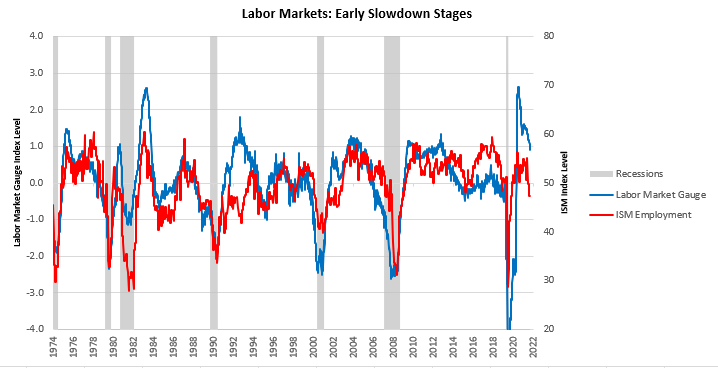

Of particular note is the widening of our estimates of the commodity risk premium. As markets move to price slowing inflationary pressures & liquidity conditions, the premium required for investing in commodities continues to rise. We saw a similar dynamic during the unwind of the commodity bull market in 2008. We are witnessing the first leg of liquidity tightening, i.e., primarily from higher discounting of cash flows and some degree of fiscal tightness. As the Treasury moves to increase its cash balance further and Quantitative Tightening picks up further pace, the effects in both financial markets and the real economy are likely to be acute. This tightening has significant ramifications for the state of the labor market. Currently, we are seeing a robust labor market. However, early indications of cyclical weakness are beginning to shine through. We show our gauge of this below:

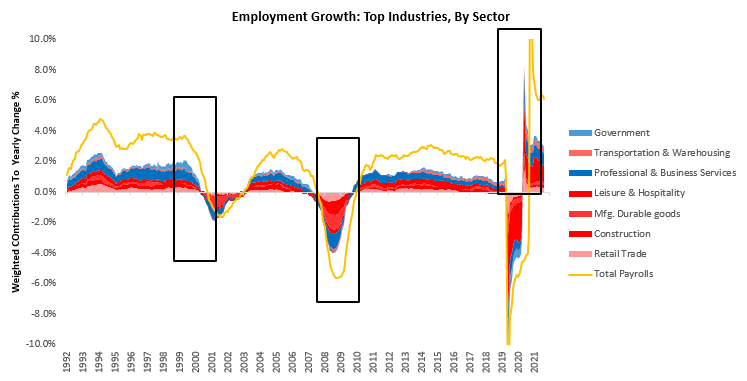

Of particular note is that labor markets are currently highly exposed to cyclicality, while aggregate wages are less. This dynamic is because employment growth is currently being driven by areas of the economy that are cyclically sensitive. At the same time, nominal aggregate wages are concentrated in more resilient areas of the economy. Below, we show the top contributors to labor market growth and colour the cyclically sensitive areas in shades of red and resilient areas in shades of blue:

Further, we highlight how these cyclical areas (retail trade, leisure, hospitality, etc.) typically tend to lead other parts of the economy at inflection points, i.e., these incomes accelerate and deteriorate before others. These incomes will likely decline further as real investment declines as corporate profitability begins to drag. We already see the early sign of reduced demand from businesses:

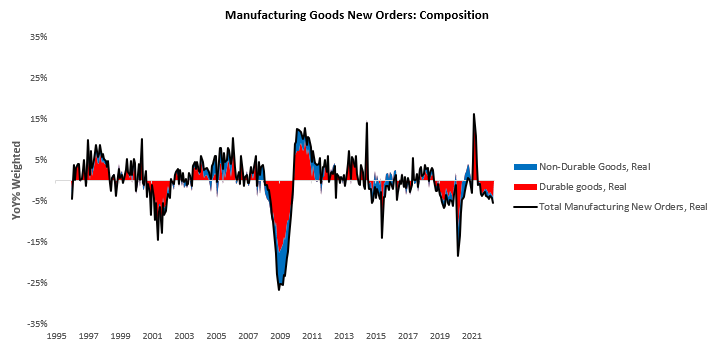

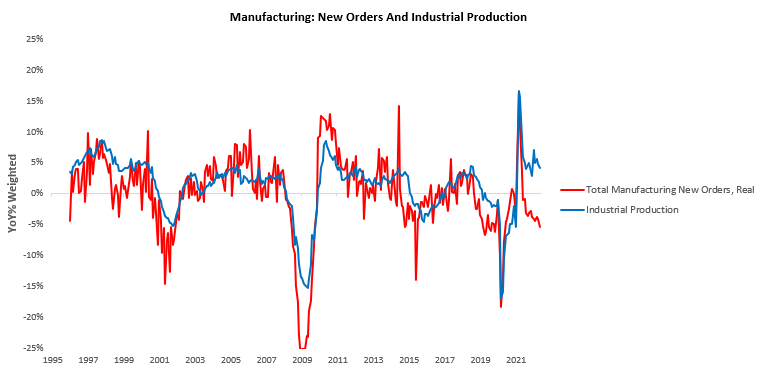

On a real basis, we estimate that total manufacturing new orders have decreased by 5.33% versus one year ago, with durable goods orders driving the majority of this decline (4%). Manufacturing new orders have a strong relationship with industrial production, as new orders facilitate the demand for production. However, manufacturing new orders is currently at odds with industrial production, telling us there is pressure on industrial production to fall.

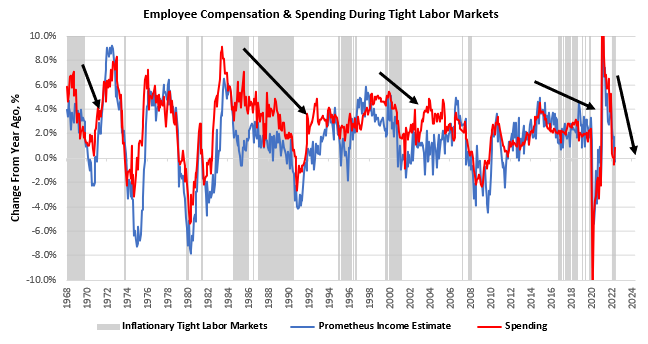

Therefore, we continue to see the tight labor markets as a self-limiting factor, i.e., robust nominal growth driven by inflation tends to cause its own downfall. Below we show these periods of “inflationary-tight labor markets” tend to result in declining incomes & spending on a real basis:

Therefore, while the labor market is tight, we continue to look at the nature of this tightness to be a net negative.

Turning to next week, we receive a slew of inflation data. We show the data relevant to our systematic process below:

-

Monday: N/A

-

Tuesday: NFIB Small Business, Nonfarm Productivity

-

Wednesday: MBA Mortgage Apps, Average Hourly Earnings, CPI

-

Thursday: Claims, PPI

-

Friday: University of Michigan Surveys

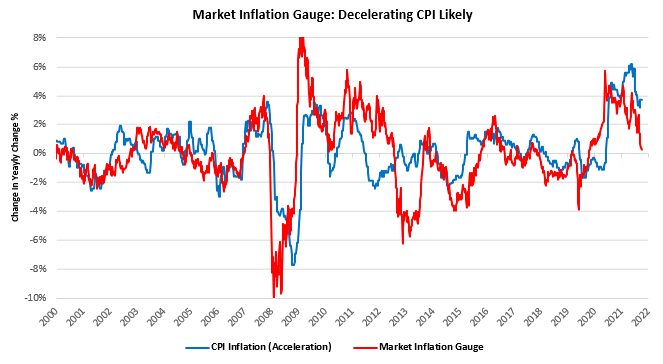

Markets are highly likely to anchor on inflation data. For our part, we expect the declaration in CPI to begin over the next few prints. However, there is a strong autocorrelation component to inflation prints, i.e., high monthly inflation begets more inflation in subsequent months. We will offer more information on this front prior to the print. However, from a strategic perspective, we continue to expect the acceleration in CPI to reverse. This decline will likely be a function of commodity price declines, which pass through to goods prices and services. We show some of our gauges below:

Our market inflation gauge has generally been a strong predictor of inflation acceleration and tells us the path is likely lower.

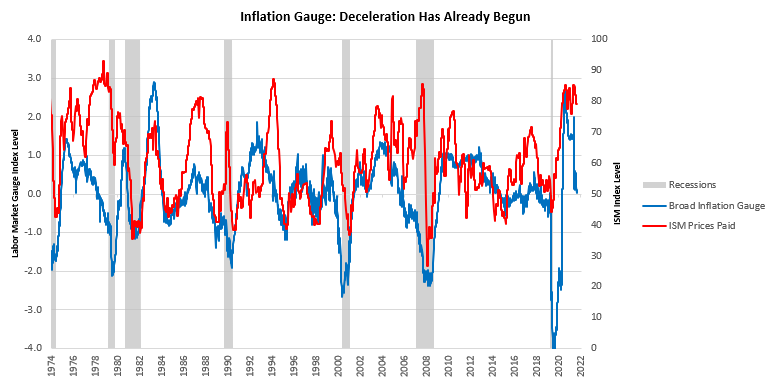

Our broad inflation gauge has also been a strong indicator of the inflation impulse and tells us that we are likely headed lower.

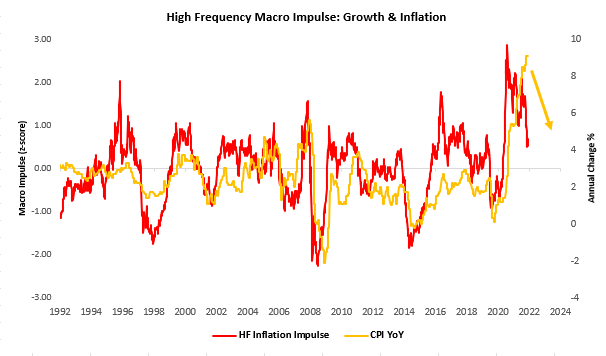

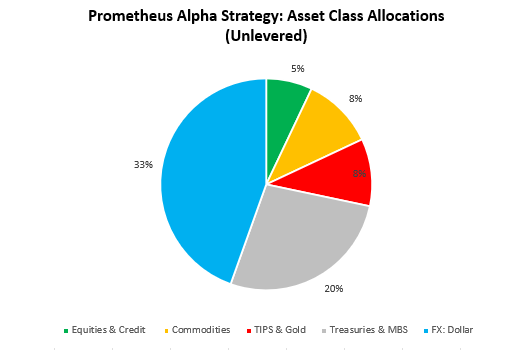

Finally, we show our high-frequency impulse gauge, which paints a similar picture. Therefore, our systems are aligning to show that the pressures for inflation to decelerate are gathering and are incrementally moving to benefit from these moves. Our systems are, therefore, extremely defensive in their posture now and are primarily allocated to the dollar and treasuries. We show the asset allocation for our Alpha Strategy below:

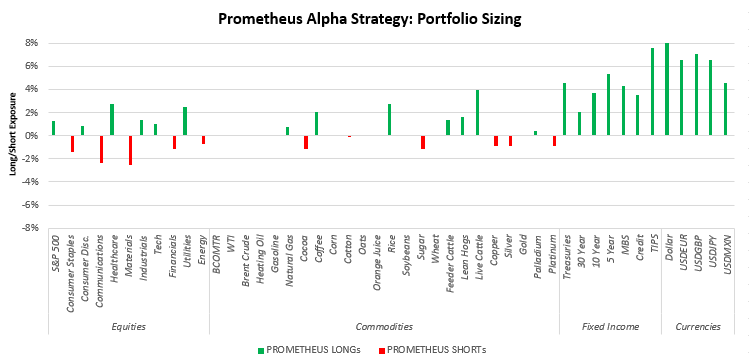

At the security level, we show how the Alpha Strategy is positioned below:

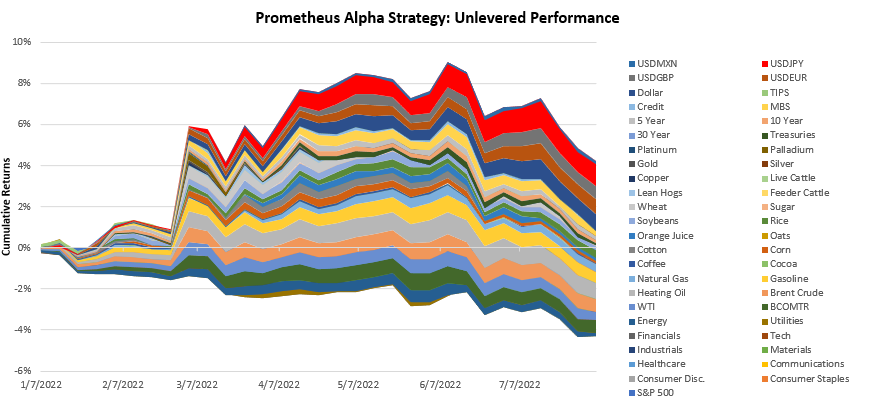

Additionally, we show the cumulative un-levered year-to-date returns on the strategy below:

Stay defensive.