Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

If you haven’t already, check out Episode 3 of the Prometheus Podcast! For this episode, we have a formidable guest- Mr. Blonde. Mr. Blonde is an independent macro strategist who chooses to remain anonymous. With significant experience on both the buy-side & sell-side- his equity-centric research is timely, precise, and pragmatic. This year, he’s done an excellent job expecting the bear market in stocks & the ensuing bear market rally. In a wide-ranging discussion, our Founder, Aahan Menon, helps Mr. Blonde take you through a masterclass in macro-equity investing. This episode is a must-listen for anyone investing or trading equities actively. Enjoy!

Prometheus Podcast: Mr. Blonde

Below are the top observations coming from our systematic tracking of economic conditions:

Below are the top observations coming from our systematic tracking of economic conditions:

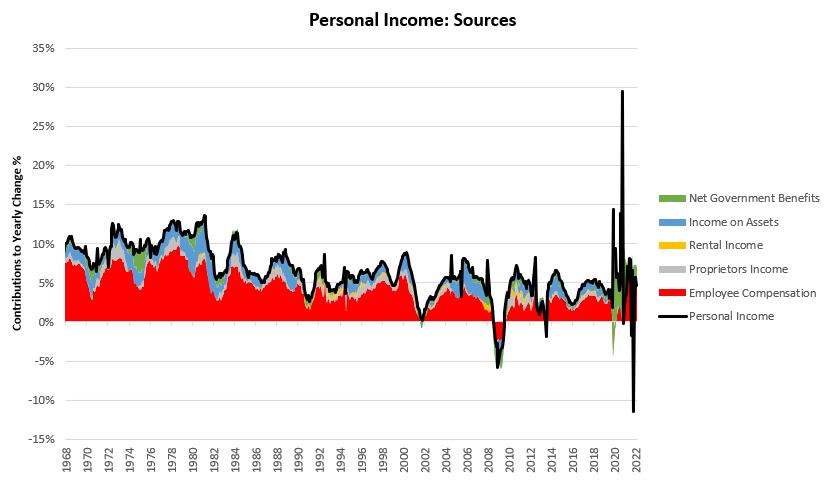

i. Nominal personal income remains elevated but is translating into lower real spending, which creates a self-reinforcing dynamic for lower real economic activity. Inflationary spending cannot sustain itself indefinitely and requires a real output component to match nominal spending. As we show below, personal income remains elevated on a nominal basis:

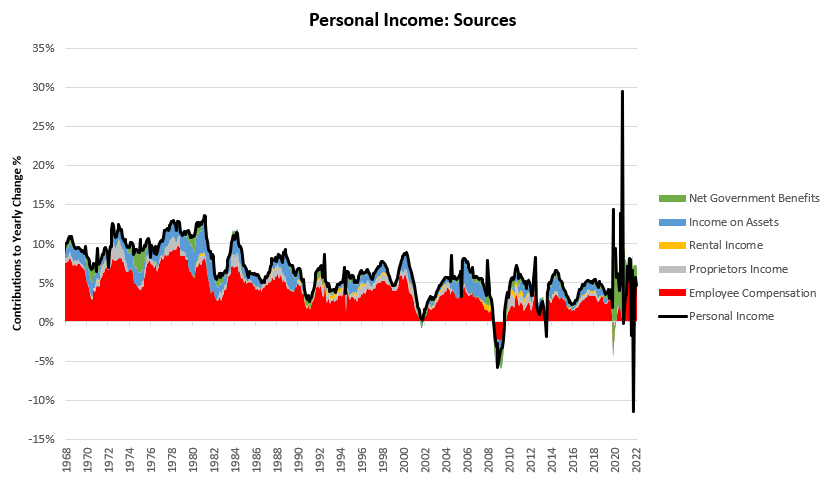

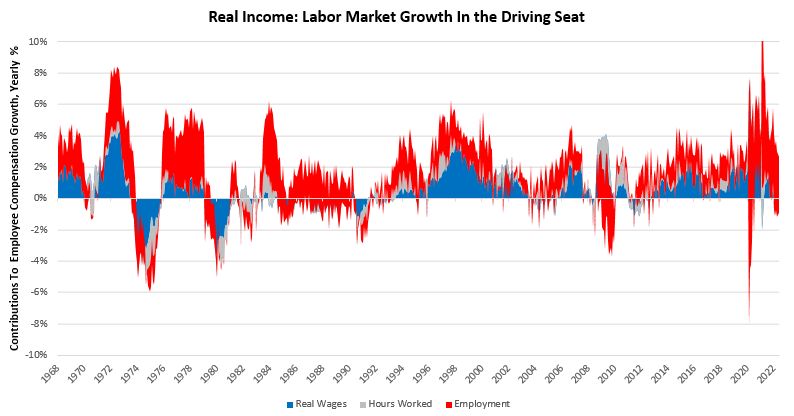

Driving these income changes is broad-based support for nominal employee compensation, accounting for all the growth in personal income. Below, we show our estimates of the primary drivers of employee compensation:

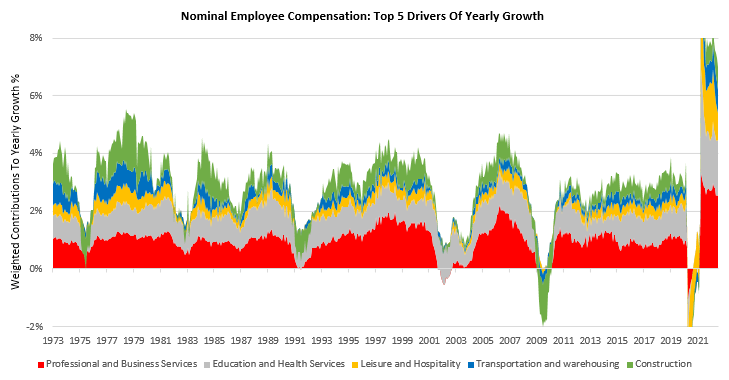

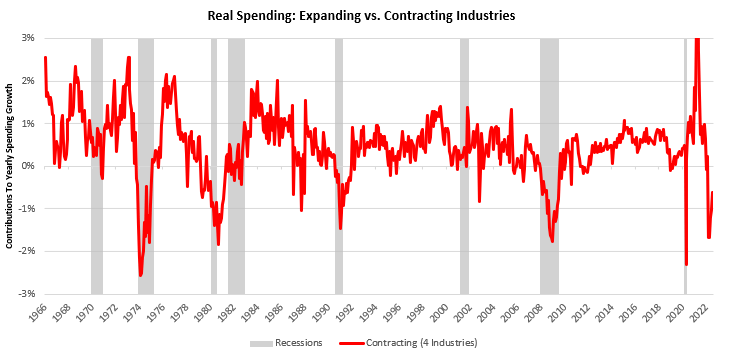

Now, while these nominal wages remain elevated, the concern continues to pass through in spending- where these wages increasingly buy less goods and services. Below, we show the current composition of real personal spending, grouped into industries receiving positive levels of spending and those receiving negative levels of real spending:

We now zoom in on those industries with contracting levels of real spending, i.e., Motor Vehicles & Parts, Furnishings & Durable Household Equip., Food & Beverages, & Gasoline & Energy Goods. These industries are highly cyclical parts of the economy, which tend to be sensitive to changing economic conditions, suggesting that cyclical conditions are weakening:

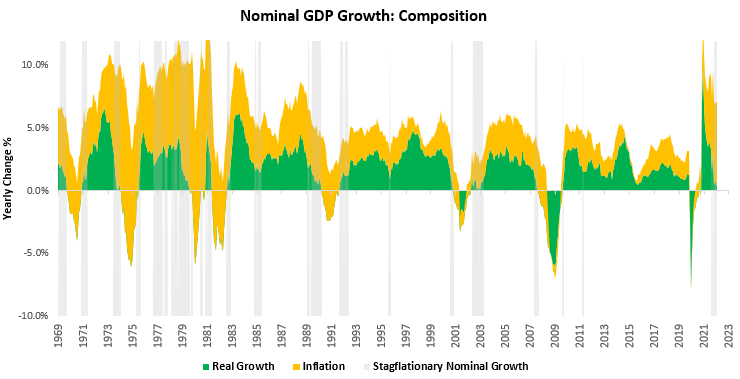

The combination of these factors is creating an environment where inflation remains the dominant driver of nominal GDP growth, which we show below:

The issue with this type of growth is that it is rarely self-sustaining. As nominal incomes remain elevated and real spending weakens, output begins to decline as each nominal dollar invested into the economy yields lower real output- which eventually results in lower nominal income. Now, it can take a significant period of time for nominal incomes to come in line with real output, and during this adjustment period, we experience dynamics like today. In our view, the only way to cause a swift recalibration is via the labor market, and the Fed will have to be willing to tolerate a significant amount of labor market weakness to happen. Alternatively, the only other readily available lever is taxation, i.e., using a higher tax policy to drain liquidity from the private sector. However, given political dynamics, we expect labor to be the lever that adjusts.

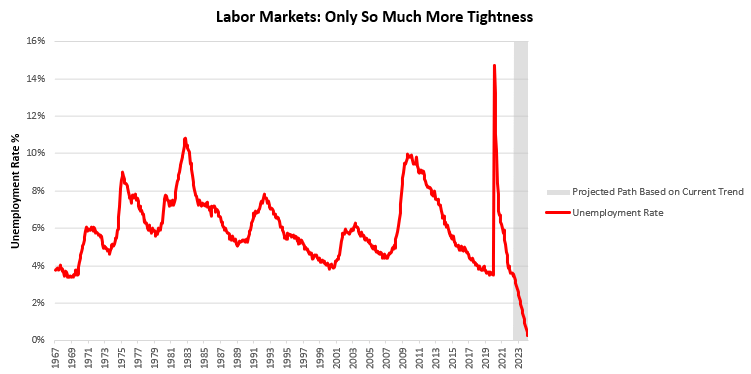

ii. Labor markets only have so much more to give. At the current trajectory, we will hit a 2% unemployment rate by Q1 2023 and a 0% unemployment rate by 2024- and we find this path unlikely. Below, we show the projected path for unemployment based on the current trend in growth for employment and the labor force:

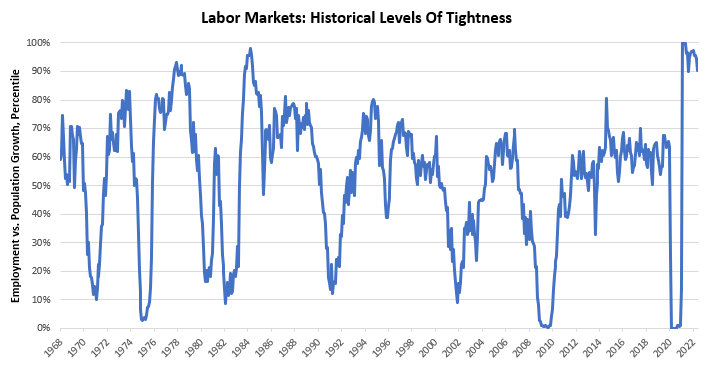

This level of tightness is at a historical extreme, and this has a self-limiting function built in. At some point, labor markets will not be able to tighten relative to the population, and the growth in labor markets will likely decelerate in the near future: We show the historically elevated rate of employment growth relative population growth:

This dynamic is particularly important in today’s context, where labor market are the primary driver of real income growth:

Therefore, as labor markets slow which they likely will real incomes will begin o contract. On a year-over-year basis, we would require a 2.7% annualized deceleration in employment growth to generate a negative print in real incomes. This kind of deceleration is well within historical precedent, and given existing pressures, we could see these moves materialize over the next six months. Therefore, we continue to monitor labor markets carefully.

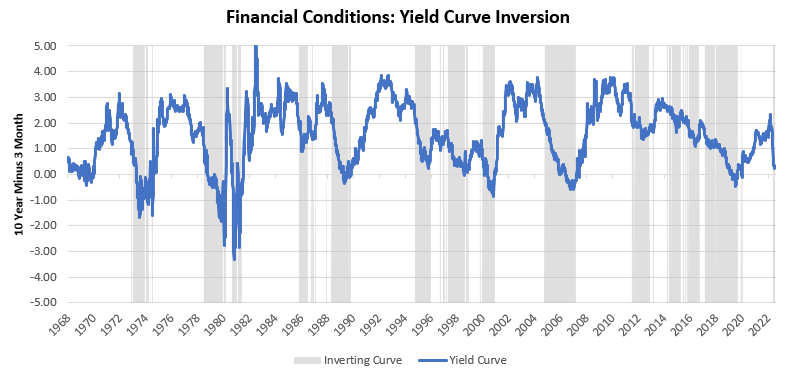

iii. Financial conditions continue to tighten, creating a challenging environment for credit creation. Our systems flag both yield curves inverting on their current path and credit risk widening via spiking credit spreads. Both these conditions create significant pressures on the economy. We show the yield curve below:

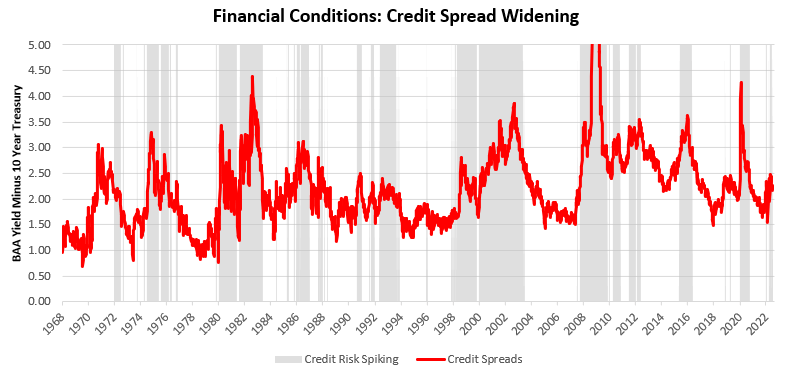

Yield curve inversion is a difficult environment for all economic activity, as it shows a mismatch between demand for safe assets at the long end of the treasury curve relative to the short end, resulting in long-duration and short-duration assets having similar yields. This dynamic is inconsistent with the time-value of money; wherein longer-dated assets should command a premium over short-dated ones and is rarely sustainable (unless largely government-sponsored). Inverted yield curves disincentivize longer-dated lending to the Treasury and have cross-asset ramifications as Treasury securities form the base at which risk assets are priced. Coincident with yield curve inversion, our systems have flagged spiking credit spreads. We show this below:

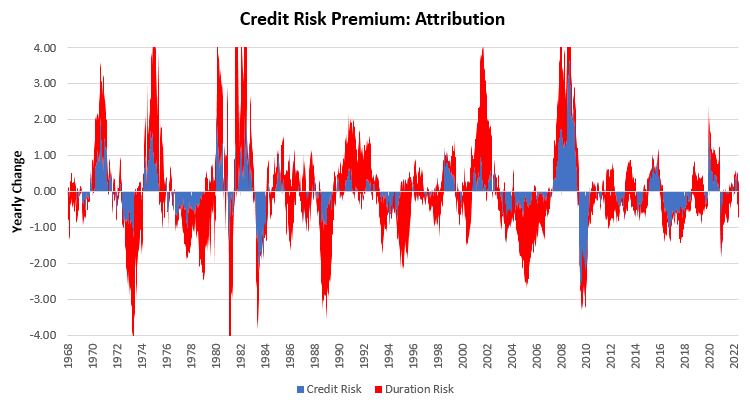

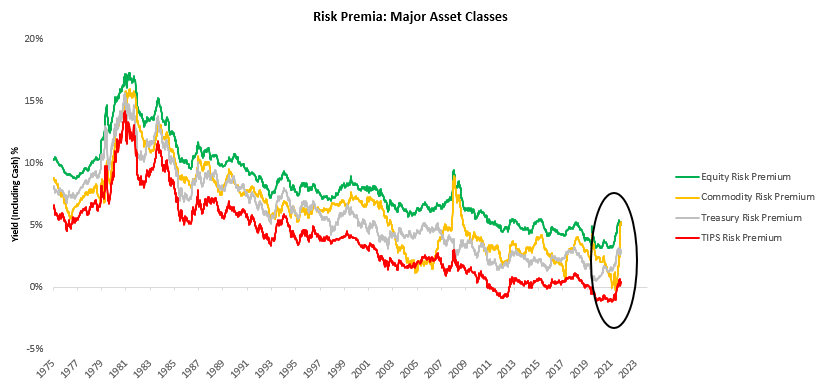

Credit & Equities will always command a risk premium over Treasuries as they have embedded default risk in their price. However, during times of stress, this premium rises significantly, reflecting the increased risk of defaults and a higher cost of borrowing. When investors purchase an asset, they are purchasing the combined package of these components in exchange for cash, i.e., they are purchasing a combination of duration and credit risk, and the current mix of factors simply repackages this premium to create riskier security relative to cash:

The result of these dynamics is a wide elevation in expected returns (risk premia +cash rate) across asset classes, largely driven by higher discount rates:

Keep in mind that while expected returns potentiate future returns, they do not catalyze them. In fact, they are generally the mirror image of current returns. Overall, the liquidity environment continues to create a difficult environment for borrowing via these channels, and it’s only likely to worsen as the Fed continues to raise interest rates.

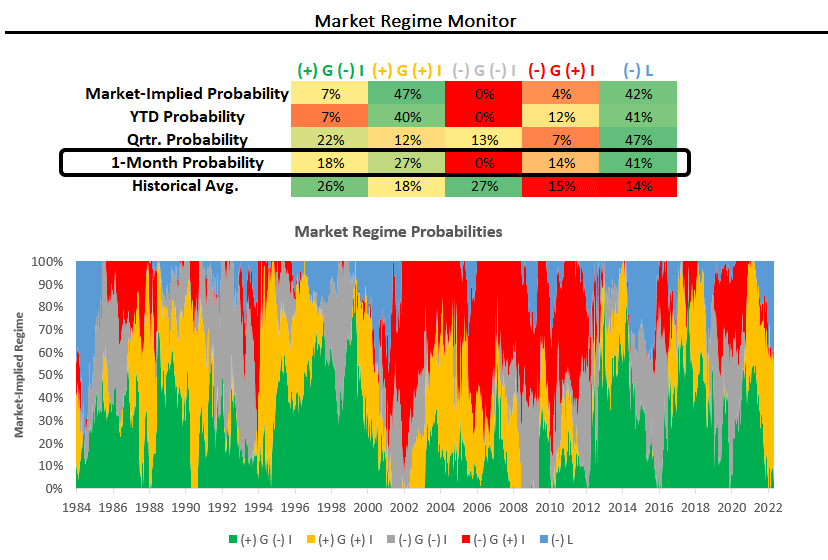

Our systems continue to show that we are in a stagflationary nominal growth environment with tightening liquidity conditions. Nominal growth dynamics remain resilient as the economy works through monetary excesses built through joint monetary and fiscal support. During the COVID-19 crisis, government authorities created large amounts of liquidity in both financial markets and in the real economy. While the Fed is moving to drain some of this in markets via quantitative tightening, the fiscal authority can only drain its liquidity creation via taxation. Without higher taxation, it is extremely hard to destroy policy liquidity, as it is essentially cash, i.e., government liabilities have almost no risk of default and therefore can’t be written down significantly. Inflation is an organic result of this phenomenon, where liquid assets exceed the economy’s capacity, and the only way to mechanically correct these imbalances is to erode the currency’s value. Resultantly, markets continue to price these dynamics:

This environment doesn’t favor treasuries & doesn’t favor equities (selectively). This is further reinforced by our regime-expected returns that account for the economic environment and are a much better pro-cyclical gauge of the returns we can expect in a given environment:

Resultantly our systems are net short equities & credit once again, alongside shorting treasuries. We have paired this with inflation hedges and long-dollar positions, creating a portfolio that will likely benefit from stagflationary dynamics and tighter liquidity conditions:

Our systematic approach has proven a strong guide this year, with our strategies In positive territory despite a difficult year for stocks & bonds. We continue to expect our strategies to harvest returns over the cycle:

We will eventually reach a point when self-reinforcing dynamics of weakening growth will tip us into a deflationary environment, but we simply aren’t there yet. In the meantime, stay nimble.