Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real-time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

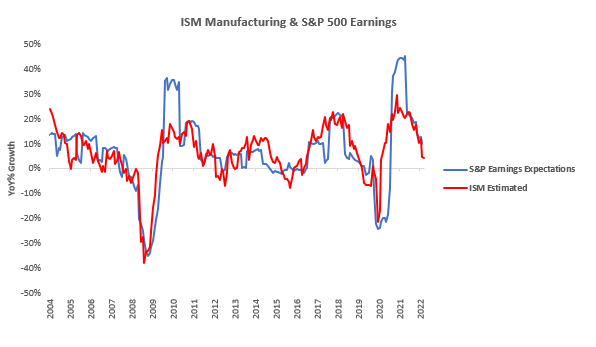

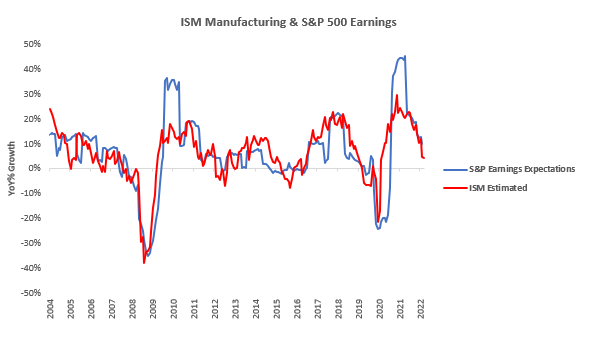

i. ISM Manufacturing data surprised expectations, as estimated by our models. The latest ISM Manufacturing data showed an expansionary reading of 52.8, implying a 5% YoY change in earnings estimates for the S&P 500.

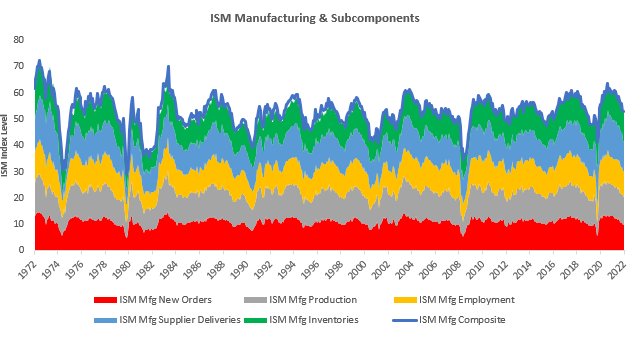

This reading was a sequential deceleration within a decelerating trend. The largest gaining segment was Inventories, and the most significant slowdown was in New Orders. These readings continue to spell trouble for both the economic outlook and future ISM data- New Orders typically decline as manufacturers expected demand weakens, and inventories rise as realized demand weakens. We show the composition of this print below:

We show the same in tabular form:

Despite this counter-trend print in ISM (which our system nailed), Prometheus’ systems continue to tell us that the fundamental economic trend is lower. We stay defensive.

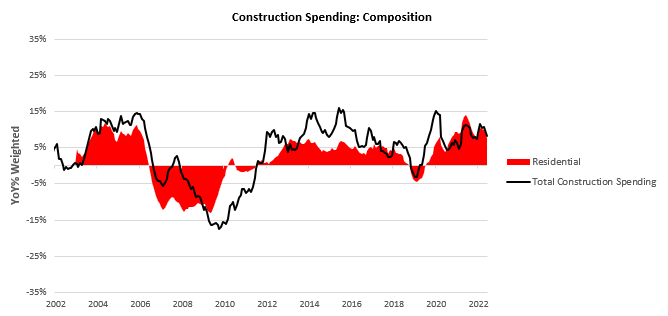

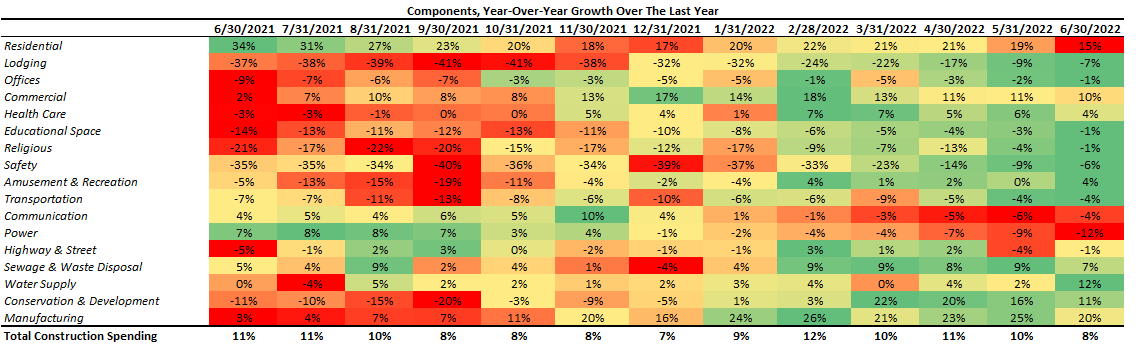

ii. Nominal construction spending remains elevated. Construction Spending came in at 8.3%, a sequential deceleration from the last print. This print disappointed expectations with a monthly charge of -1.1% versus expectations of 0.1%.

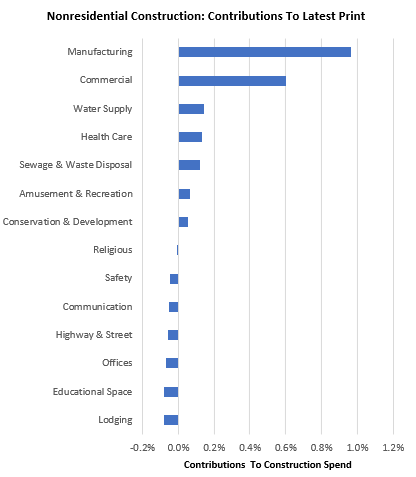

Residential construction (as is typical) has been the largest contributor to these moves, with a weighted year-over-year growth of 7.7%. Within the non-residential space, manufacturing continues to be the driver of nominal spending, with lodging dragging on nonresidential spending:

Over the last year, Construction Spending has been in an uptrend, and the latest values confirm this trend. We show the full composition of construction spending below:

While nominal construction spending remains strong, we must remember that real construction spending is much lower, i.e., a large portion of these increased expenditures are from elevated prices. As nominal labor income decline, as has already begun, the potential for these gains become more and more muted. Furthermore, fixed investment typically moves well after consumption has declined; therefore, we continue to see late-cycle dynamics at play.

iii. We have seen a brief respite in Quantitative Tightening, but there is much more to come. The primary driver of the improved level of reserve balances was the decrease in the Treasury general account last month, i.e., the Treasury injected cash into the private sector. However, the outlook for liquidity conditions remains bleak, and we show our forecasts for reserve balances below:

Our forecasts take into account the pace of QT, the estimated path of the Treasury & the ensuing level of reverse repo usage. As we can see above, the likely path for reserve balances is much lower. The level of reserve balances is critical to the financial systems; all else equal, a heightened level of reserve balances reduces the cost of capital to the private sector. This reduction takes place through the US government’s maturity-weighted interest profile becoming significantly lower, upon which private borrowing is priced.

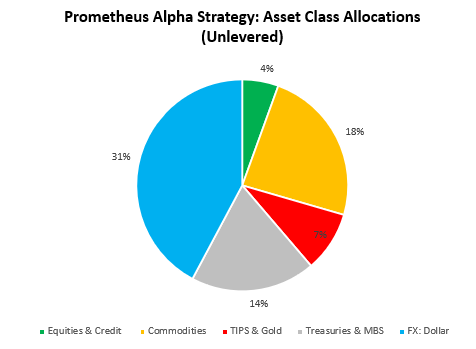

Our systems combine the underlying principles in our analysis into rules-based portfolio construction and continue to tell us to remain defensive in our exposures after being aggressively short equities & credit. Our systems estimate that the worst of the inflation shock is behind us. These dynamics create an environment where generating alpha via equity shorts becomes more challenging, but bond beta becomes easier to harvest. Resultantly, our systems are now significantly allocated to deflationary & tightening liquidity assets (Treasuries, MBS, Dollar, & Cash). However, our risk mitigation signals have also moved us towards marginally higher exposure to commodities. We show our Alpha Strategy asset class allocations below:

Stay nimble.