Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of both the economy and financial markets in real-time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

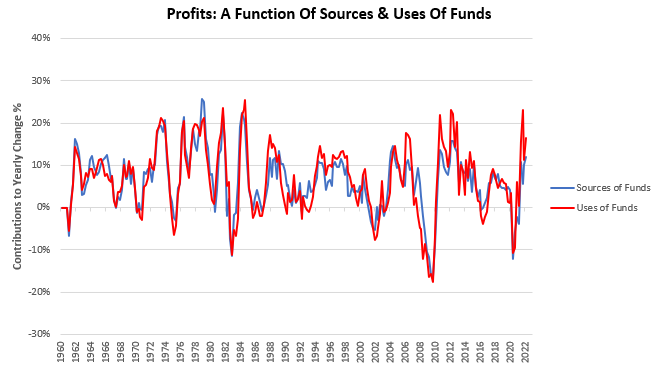

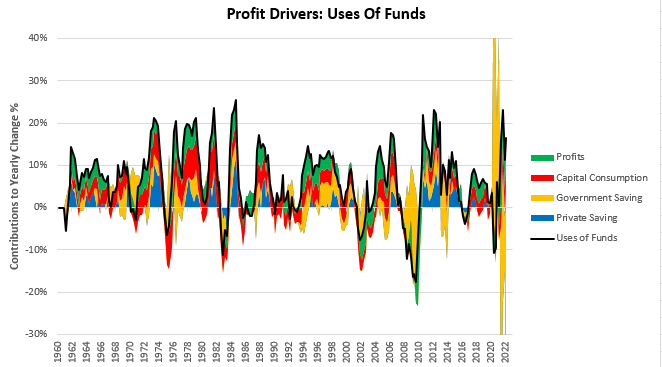

i. Fiscal tightness will continue to pressure profits. Profitability in the macroeconomy is the residual of investment in the economy relative to the amount of savings. The primary driver of corporate profitability is fixed investments into the economy because real investment creates revenue for businesses over time without incurring costs other than depreciation. Conversely, the most significant drain on profitability is increased savings by households & the government. We can categorize these items (and others) into sources or uses of profits. The vital thing to note here is these reflect offsetting accounts, i.e., the sources of funds must equal the uses. We illustrate this below:

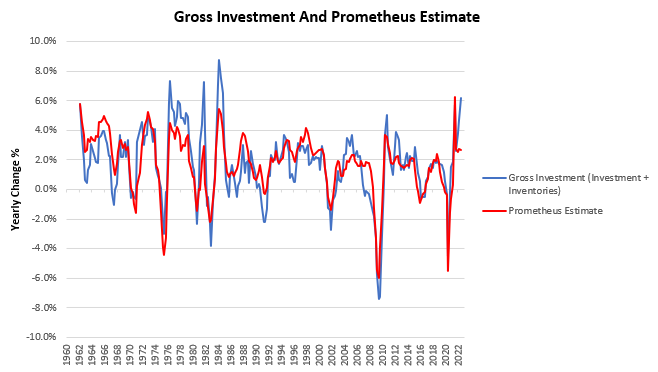

This approach allows us to dissect all the moving parts that drive corporate profitability granularly. Currently, we continue to see elevated nominal investment levels, which provide support for corporate profitability. We show below how gross investment remains a strong source of profitability:

We also show hour our models still show nominal gross investment (including inventory build), holding up for now:

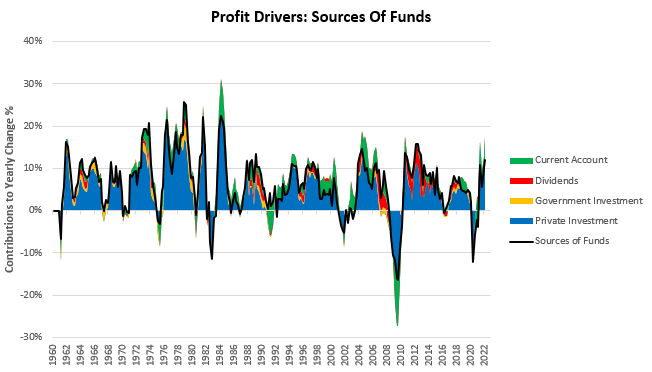

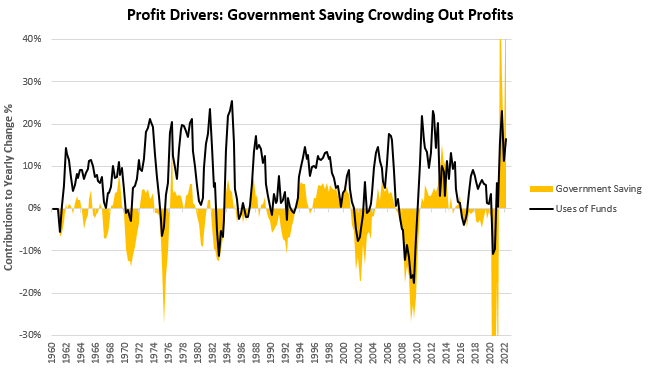

However, 43% of this gross investment growth has come from inventory build-up, which does not bode well for future profitability. The drain on profits from fiscal withdrawal remains of particular concern. Historically, the US government has been willing to dissave (deficit spend), which has supported corporate profitability significantly. We show the drains on profitability alongside profits over time below:

However, we are now in a different environment, where government savings is now crowding out the potential for corporate profitability:

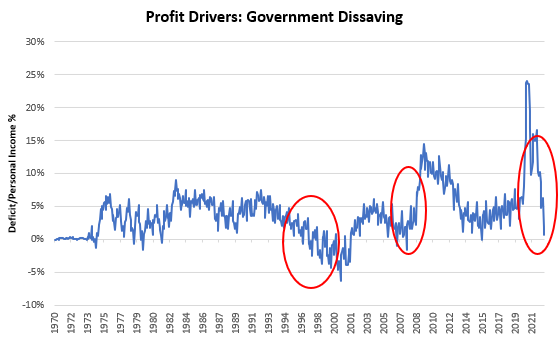

The US Treasury remains on a far more frugal path than recent past, and this fiscal tightening will impact create further headwinds for profitability:

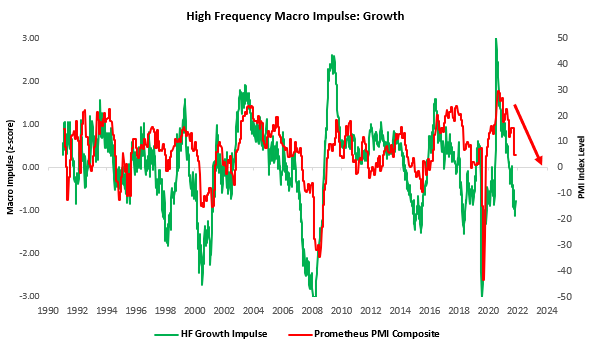

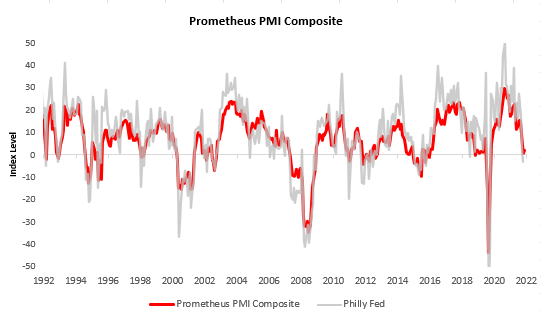

ii. PMIs will likely continue to deteriorate as the outlook for profitability weakens. Our high-frequency impulse tracker continues to the growth impulse deteriorating. We expect this to continue to show in PMI data:

This information means that pressure will remain on Philly Fed data later this week to soften. Our PMI composite, which aggregates PMI data across the US, tells us that the trend remains a weakening one:

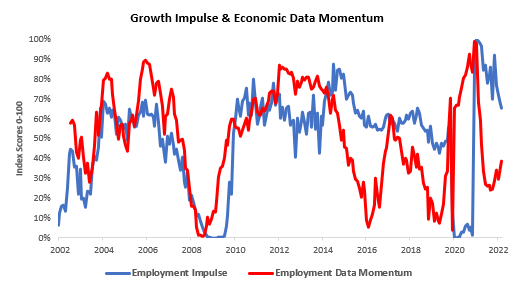

iii. Income and employment data will confirm the next leg down. On a secular basis, labor markets remain extremely tight. However, on a cyclical basis and relative to expectations, labor markets have weakened. Labor market data began to disappoint many months ago, but we are starting to see the initial stages of a cyclical deterioration in labor markets. Below, we show both the momentum in labor market data relative to expectations, alongside the cyclical change in labor markets (growth impulse):

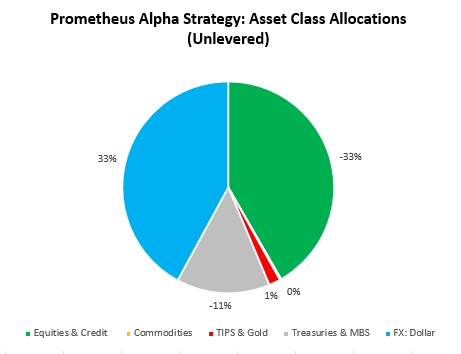

There remains much room for labor market deterioration, and pressures continue to build. Our systems are designed to be incremental and continue to adjust as the data changes. We continue to expect further slowdown in both the real economy and asset markets. Our systems net the signals from the above analyses and continue to point us in the same direction they have for the last few months: stay short equities & credit and long the dollar or cash. We show how our systematic Alpha Strategy is positioned at the asset class level:

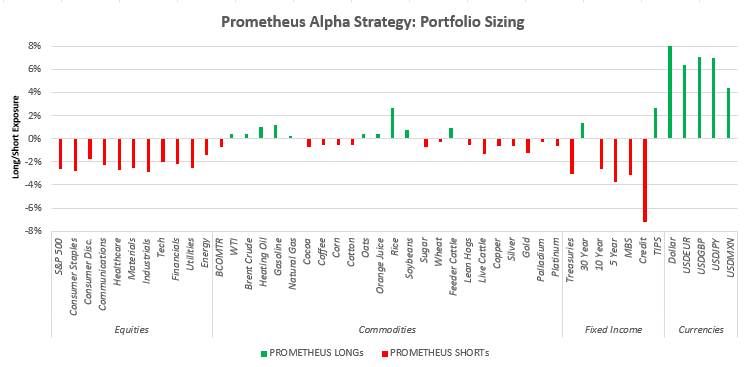

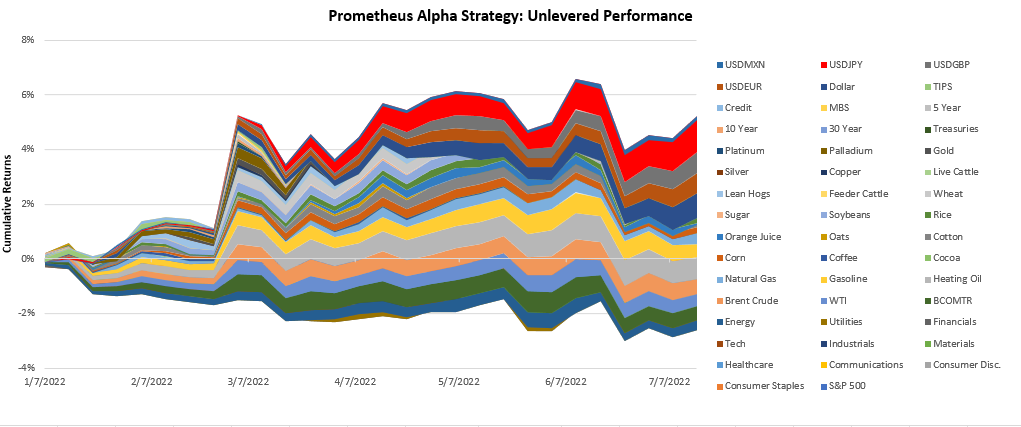

Additionally, we also have a net short treasury position. However, the systems remain long at the long end of the Treasury curve. We show our positioning at the security level below, along with the year-to-date cumulative returns of the strategy:

Year-to-date system returns:

Stay nimble.

Muchas gracias. ?Como puedo iniciar sesion?