CPI Review: Slowdown Pressures Manifesting

Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real-time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

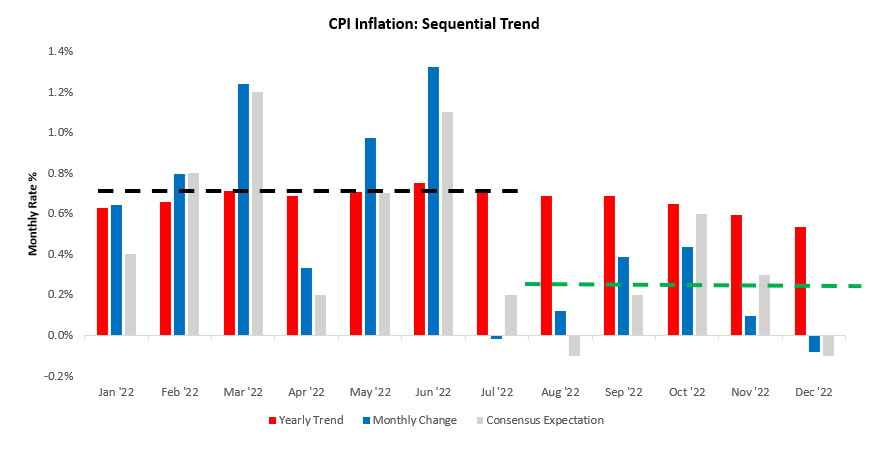

CPI inflation came in line with consensus expectations but counter to our forecasts. CPI Inflation decreased -0.08% in December. This print contributed to a sequential deceleration in the quarterly trend relative to the yearly trend. Below, we show the monthly evolution of the data relative to its 12-monthly trend and consensus expectations:

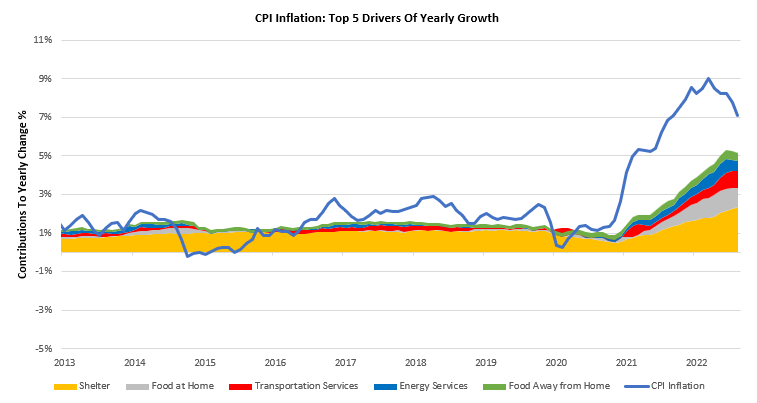

Over the last year, Food at Home (1%), Food Away from Home (0.43%), Energy Services (0.55%), Shelter (2.46%), & Transportation Services (0.88%). have been the primary drivers of the 6.42% CPI inflation. We show the contributions of these items to yearly changes in total spending below:

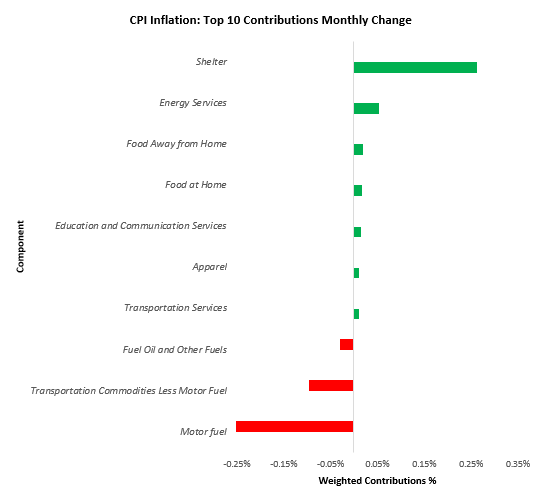

Of particular note in this release was the severity of energy deflation. Additionally, we saw extremely strong pressure coming from transportation commodities, ex-motor fuel:

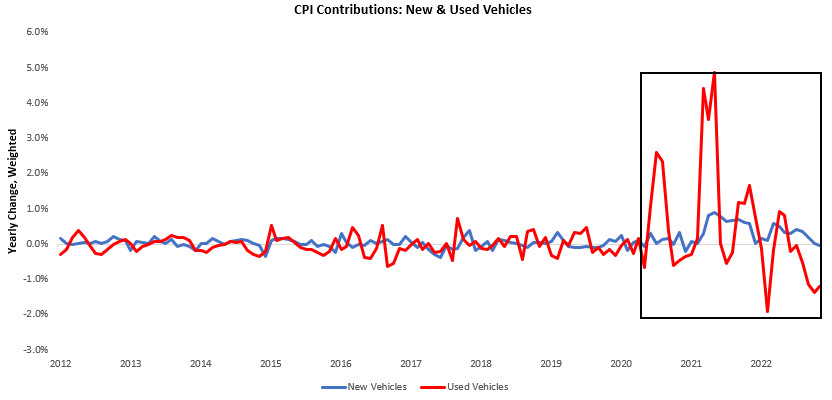

Within this category, used cars continue to be the primary driver of declines; however, new cars have also now slipped into deflation. We show this below:

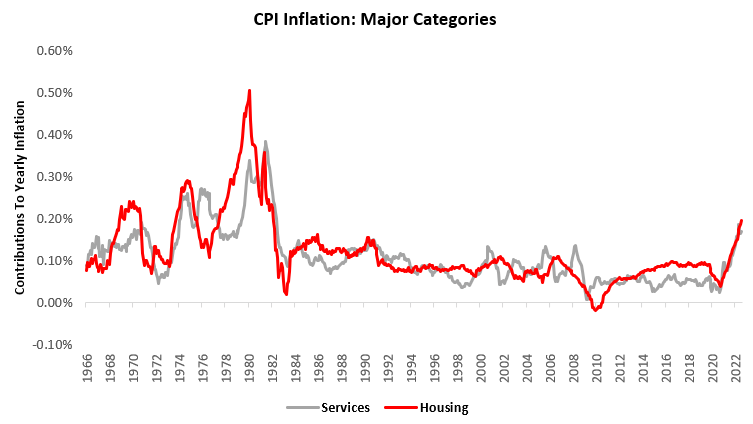

The themes we highlighted in our Month In Macro report remain intact, i.e., divergences between the goods and services economy continue to persist. Below, we show the yearly change in services inflation:

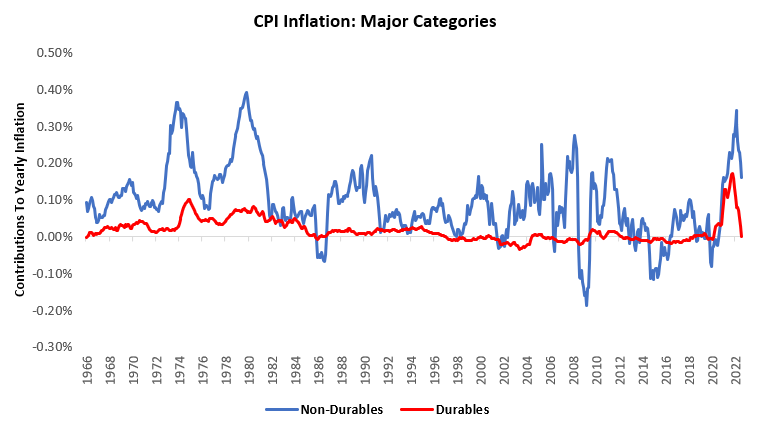

In contrast, the goods economy continues down a deflationary path:

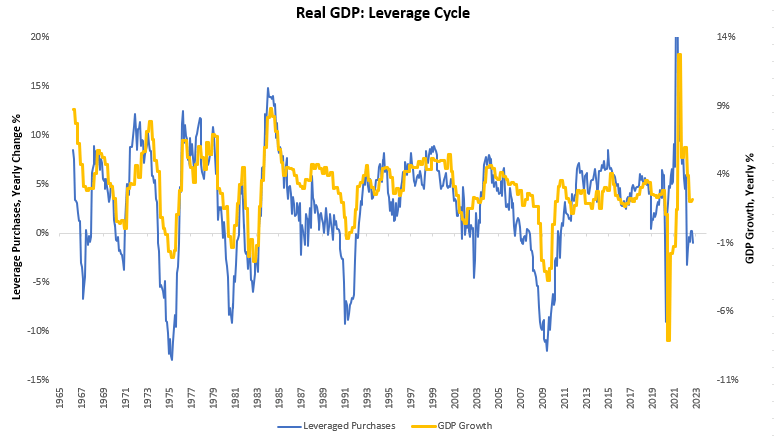

This divergent rate of inflation is largely a function of the slowdown elicited by Federal Reserve policy. We are seeing the cyclically sensitive, leveraged sector of the economy weakening faster than the service-oriented, income-sensitive sectors. We see this in our tracking of the leveraged sectors of the economy:

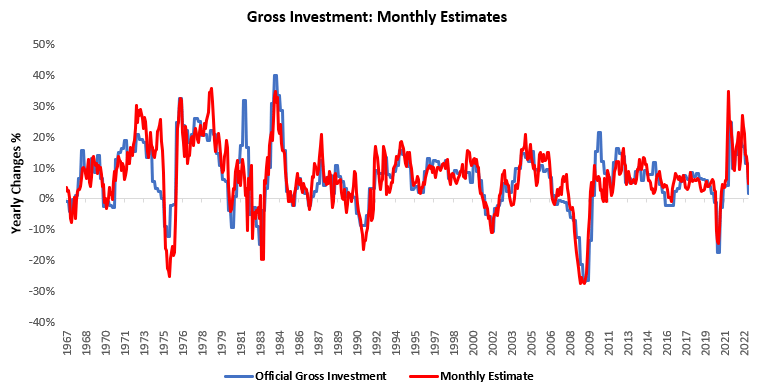

We see this further in our tracking of nominal investment, which is primarily driven by real estate & equipment investment:

Overall, the cyclical slowing of the economy via tighter liquidity conditions continues to pressure nominal and real activity, creating deflationary pressures. These exist alongside inflationary pressures in the services economy. The combination of these competing forces continues to force of stabilization of inflation at a high level. The next stage of the cycle will be determined by whether the recessionary & deflationary pressures in the goods economy will be enough to bring down nominal income and spending on services. This is another step forward in the slowdown. Until tomorrow.

They provide a world of health solutions.

can you get generic lisinopril for sale

An unmatched titan in the world of international pharmacies.

Their global medical liaisons ensure top-quality care.

how to buy generic lisinopril online

They always offer alternatives and suggestions.

They provide peace of mind with their secure international deliveries.

gabapentin 300 mg and weight gain

Their international shipment tracking system is top-notch.

The team always keeps patient safety at the forefront.

buy cipro pill

I’m impressed with their commitment to customer care.

Making global healthcare accessible and affordable.

gabapentin vicodin high

They consistently go above and beyond for their customers.

You could definitely see your skills in the work you write. The world hopes for even more passionate writers like you who aren’t afraid to say how they believe. Always follow your heart.

Hello my friend! I wish to say that this post is amazing, nice written and include approximately all significant infos. I would like to see more posts like this.

hi!,I love your writing so a lot! percentage we communicate extra about your article on AOL? I need a specialist on this house to resolve my problem. May be that is you! Having a look ahead to look you.

Hi, Neat post. There’s an issue with your site in internet explorer, could check this? IE nonetheless is the marketplace chief and a huge element of other people will pass over your fantastic writing because of this problem.

Whats up very cool web site!! Guy .. Beautiful .. Wonderful .. I will bookmark your website and take the feeds additionally?I’m glad to find a lot of useful info here within the put up, we’d like develop more strategies on this regard, thanks for sharing. . . . . .

Excellent read, I just passed this onto a friend who was doing a little research on that. And he just bought me lunch as I found it for him smile So let me rephrase that: Thanks for lunch!

I know this if off topic but I’m looking into starting my own blog and was wondering what all is required to get setup? I’m assuming having a blog like yours would cost a pretty penny? I’m not very internet savvy so I’m not 100 sure. Any suggestions or advice would be greatly appreciated. Thank you

Through my observation, shopping for gadgets online may be easily expensive, nevertheless there are some tips and tricks that you can use to obtain the best bargains. There are often ways to obtain discount bargains that could help to make one to have the best electronics products at the lowest prices. Thanks for your blog post.