A Simple Long-Only Strategy To Combat Stagflation

Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real-time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

Our research aims to offer a granular and comprehensive understanding of current economic conditions and how they will likely evolve- to help investors navigate markets through the economic cycle. To augment the research and analysis, we have developed Prometheus Cycle Strategies- which use our cyclical expectations to trade markets. These Cycle Strategies reflect the understanding that particular points in the economic cycle offer an asymmetrically positive return on risk, either long or short assets. Using our systematic process, we attempt to forecast these points to harvest these attractive return-to-risk characteristics.

Typically, in macro, we focus on alpha generation via going long and short a variety of assets, often relative to one another. While fruitful, some of these approaches are often complex and require significant monitoring and management, making them out of reach for the everyday investor. At Prometheus, we’re trying to help the broadest possible population using our systematic tools. Therefore, today we will share a simple strategy aimed at helping a somewhat passive investor navigate today’s challenging macroeconomic landscape. We offer a simple approach that leverages our systematic macro forecasting process to risk-manage an equal-weighted portfolio of stocks and bonds. If we receive significant interest in this note, we will begin providing guidance on this front regularly, so let us know in the comments below or subscribe to let us know:

The performance of stocks and bonds is tied to the future outcomes for growth and inflation, and as active investors, we try to use our expectations for these variables to time our exposure to these markets. For a long-only, largely passive investor, we think the biggest benefit our process offers is to allow you to side-step the worst drawdowns in these asset classes.

Recessions are the primary risk to stocks as nominal spending collapses. At the same time, inflationary episodes are the primary risk to bonds as their fixed interest rate becomes less attractive relative to other nominal assets. Inflation also impacts stocks, through eventually higher costs and interest rates. Therefore, for a long-only investor, it makes sense to seek to exit stocks before an impending recession and exit both stocks and bonds during inflationary periods.

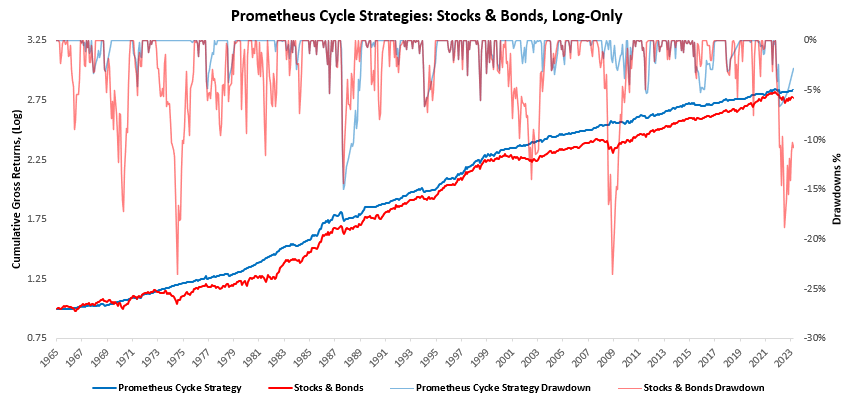

With these objectives in mind, our systems use a wide range of economic and market data to protect long-only, largely passive investors from material drawdowns driven by macroeconomic factors. We use a simple strategy that rotates between stocks, bonds, and cash. Below, we show how this modestly active strategy has performed relative to a passive stock & bond portfolio:

As shown above, our Prometheus Cycle Strategy outperforms static passive exposure to stocks and bonds while delivering significantly reduced drawdowns. Importantly, it does with relatively few trades (excluding the monthly rebalance for both strategies). The system has traded less than twice a year on average versus the benchmark. For further context, we show some summary statistics for the strategy:

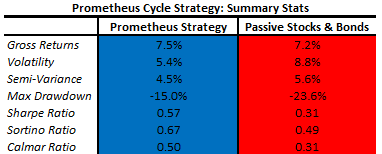

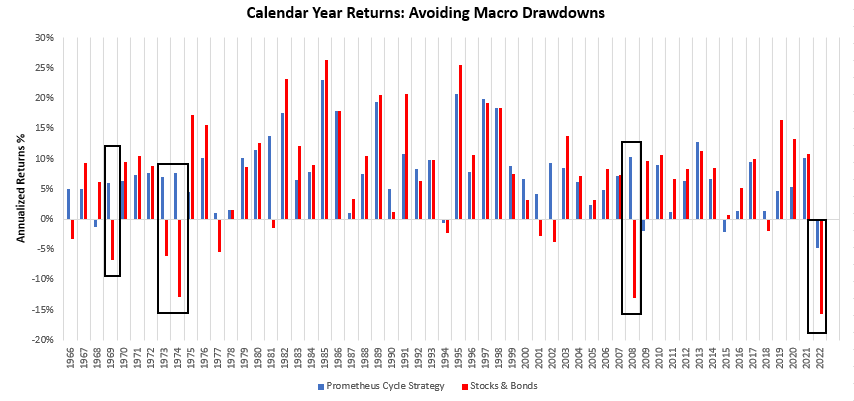

As shown above, our Prometheus Cycle strategy outperforms the passive portfolio on all measures. To display the consistency of this strategy, we also offer the calendar year returns of the strategy relative to the passive portfolio:

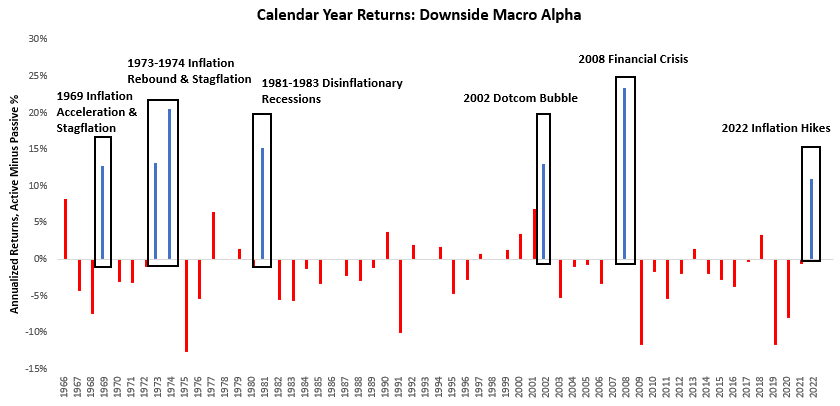

Additionally, we show the relative performance of our strategy versus the passive portfolio to showcase that the portfolio generates its outperformance for protecting against macroeconomic tail events. While calendar year returns are not the best way to gauge a return stream’s variability, they help us contextualize changes over time. To enhance this contextualization, we highlight how the strategy’s alpha primarily comes from protecting against macroeconomic shocks from growth & inflation. We do so by annotating several important macroeconomic events and the corresponding returns during these periods:

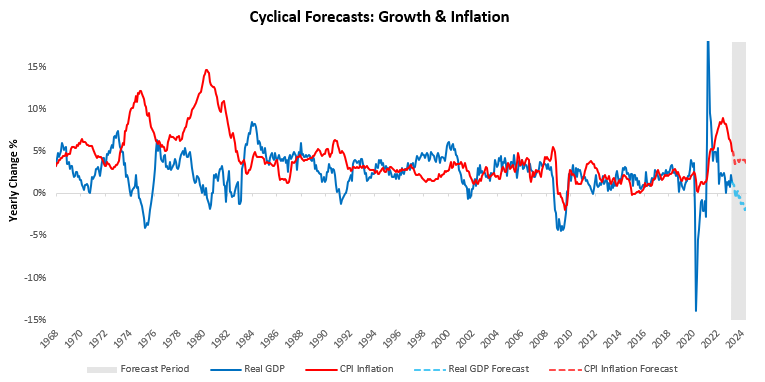

Our systems have generally proven reliable in flagging significant potential drawdowns in a portfolio of stocks and bonds, allowing us to attempt to side-step these drawdowns. To protect our edge in markets, we don’t share how our strategies are constructed. However, we offer a range of research that provides the intuitions and logic driving our systematic process. Next week, we will share a deep dive into our views in our Month in Macro report. Today, we share the high-level views coming from this systematic process. Our process tells us that we are likely headed towards a stagflationary environment, i.e., with growth contracting and inflation likely to be persistent. We show these estimates below:

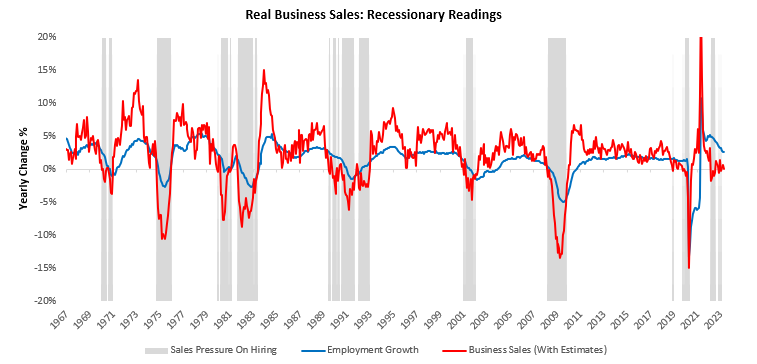

We think it is essential to recognize that stagflation tends to be one of the worst environments for passive investors. Inflation erodes the value of stocks and bonds; further, if inflation persists amidst a profit contraction, policymakers’ hands are tied in cutting interest rates to re-stimulate the economy. Looking at the growth outlook, we see it as likely that recessionary conditions are near. Below, we show some essential measures. We start with real business sales:

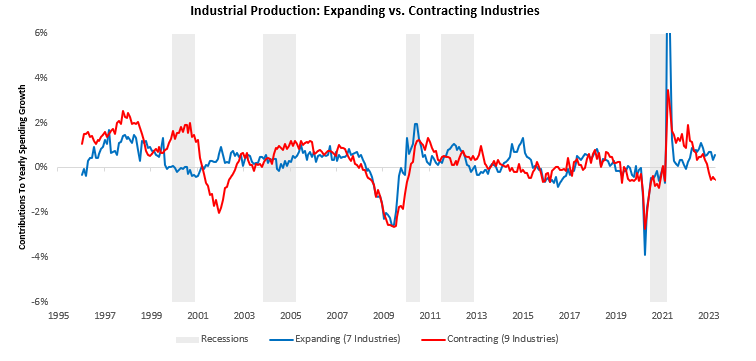

Next, we show the weakness in breath in industrial production:

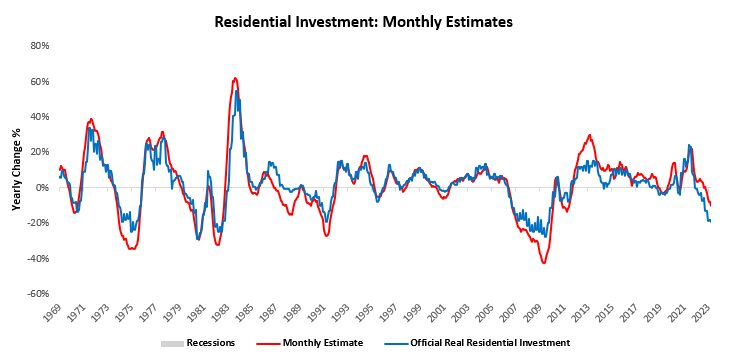

Finally, we show the weakness in residential investment:

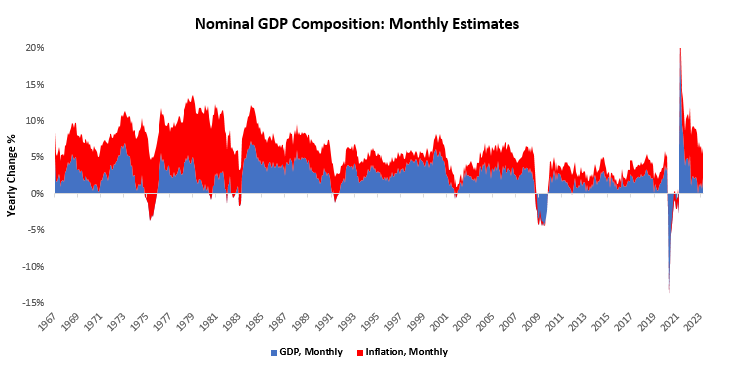

While real activity may contract soon, nominal activity remains elevated, and debt services costs remain low relative to this activity, and labor markets remain secularly tight. First, we show our latest tracking of nominal GDP, which remains extremely high relative to recent history:

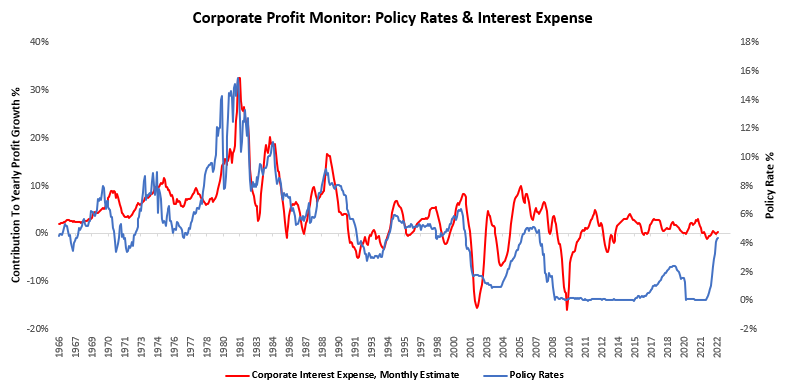

Next, we show how little impact interest rate hikes have had on corporate interest expense below:

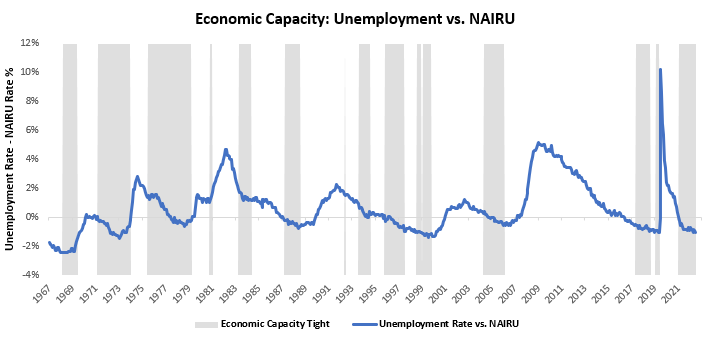

Finally, we show how labor markets remain extremely tight relative to measures of capacity:

The combination of these factors suggests that a recession is likely in the cards, with inflation still elevated. These dynamics will force policy to remain tighter for longer than is currently priced in bond markets and growth to come in lower than is currently priced by equity markets. To summarize our assessment of current conditions- the probability of a future recession is significant, and inflation is likely to be resilient. The macroeconomic setup does not favor stocks or bonds over the next 12 months. Cash likely outperforms assets. Until next time.