Potential CPI Surprise: Exit Stocks & Bonds

Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

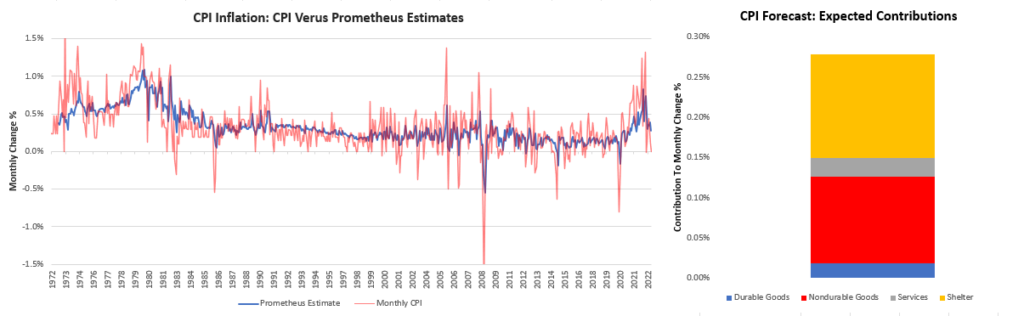

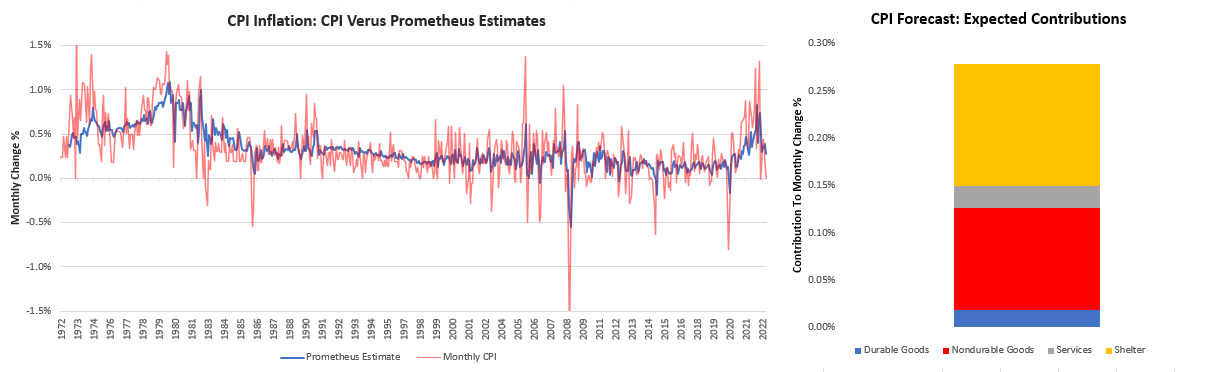

We’ll keep this note brief our systems expect an upside surprise to CPI expectations tomorrow. Our systems estimate that CPI will increase 0.28% versus the prior month, while consensus expects a -0.1% increase. Below, we show the contributions to our estimates:

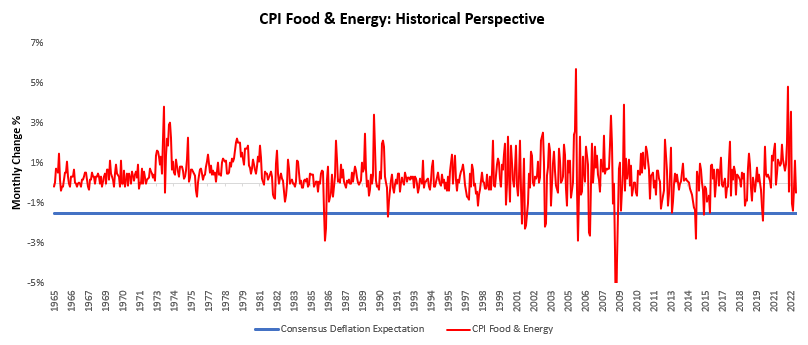

Our systems estimate that there is a large potential for a surprise, not because of any major change in the inflation picture but rather because of consensus expectations. Consensus currently expects a core CPI of approximately 0.30% which we judge to be reasonable. However, consensus also expects headline CPI to come in a -0.10% which we think is a tall order. This implies that non-core items, i.e., food & energy, which account for 22% of the index, will entirely outweigh all other inflationary components. This would mean that food and energy would have to register a -1.53% month-on-month reading for December. This would be a rare occurrence, which we visualize below:

As we can see above, the degree of implied deflation is high relative to history deflation greater than 1.53% has occurred 17 times since 1965, i.e., during 2.5% of the history. Now, our estimates for food & energy show deflationary pressures as well; however, they net out to a modest positive inflation rate. We show this below:

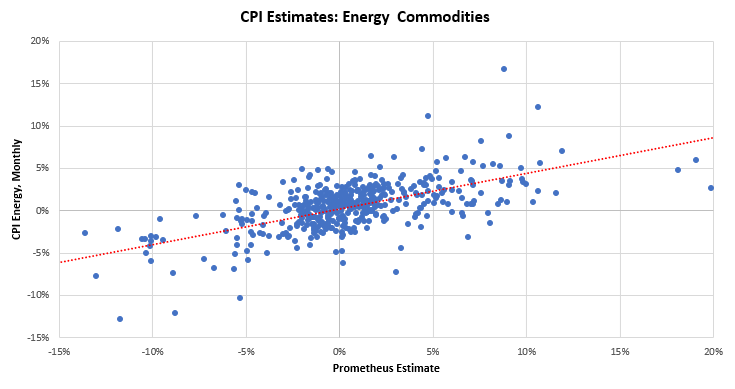

While we do not have clarity on the relative contributions within consensus estimates (unlikely they exist), through triangulation and experience, our understanding is that this divergence between consensus expectations for core and headline CPI largely comes from the estimated impact of energy. Energy inflation is eight times more volatile than food inflation; resultantly, most of the variation in non-core CPI can be explained by energy. However, when we look through our estimates of this impact, we see much more muted pressures coming from energy prices and estimate modest deflation of about 0.12% month-over-month. We show our energy estimates versus realized CPI below:

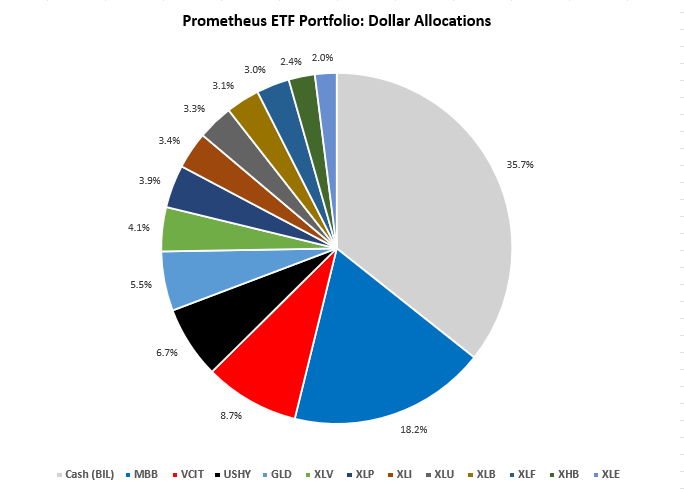

Taking these factors into account, we think there is a significant chance of consensus expectations receiving an upside surprise to their headline inflation expectations. we continue to see competing forces in the inflation story, netting out for stabilization of inflation at a higher-than-comfortable range. When it comes to this point, we think the divergence in expectations between core and headline CPI is a large one, and one of these will likely prove at odds with reality. From our understanding of the inflation drivers, headline CPI will likely come in higher than expected. For subscribers using our systematic Prometheus ETF Portfolio, we headed into this week with the following allocations:

Our portfolio has a combination of stocks and bonds, forming a bet on a cyclical slowdown in inflation, and has performed handsomely thus far. However, our expectations for CPI data would prove dangerous for this allocation if they are confirmed. Therefore, we think it makes sense for those with discretionary ability to take advantage of this information and exit these positions headed into the print. As always, we impress upon our readers that our CPI expectations are for risk management purposes rather than risk taking i.e., we manage our existing positions rather than put on new ones based on our CPI expectations, and we believe our forecasts should be applied as such. Until next time.

Always stocked with the best brands.

how to buy lisinopril pills

Their worldwide services are efficient and patient-centric.

Their international health forums provide crucial insights.

cytotec without prescription

Their staff is always eager to help and assist.

Their online prescription system is so efficient.

cytotec tablet price

An excellent choice for all pharmaceutical needs.

I value the personal connection they forge with patrons.

can i get cheap cipro tablets

Efficient, reliable, and internationally acclaimed.

They make prescription refills a breeze.

where can i get generic clomid prices

They always have the newest products on the market.

Unquestionably consider that which you stated. Your favorite justification seemed to be at the web the easiest factor to be aware of. I say to you, I definitely get irked at the same time as other people consider issues that they just do not understand about. You managed to hit the nail upon the top as smartly as outlined out the whole thing without having side effect , other people can take a signal. Will probably be again to get more. Thanks

I appreciate, lead to I discovered just what I was taking a look for. You have ended my 4 day long hunt! God Bless you man. Have a great day. Bye

In these days of austerity plus relative panic about having debt, lots of people balk against the idea of using a credit card in order to make purchase of merchandise or maybe pay for any occasion, preferring, instead only to rely on the tried in addition to trusted technique of making repayment – cash. However, in case you have the cash there to make the purchase completely, then, paradoxically, that is the best time for you to use the cards for several causes.

Thanks for the marvelous posting! I definitely enjoyed reading it, you could be a great author.I will be sure to bookmark your blog and will often come back someday. I want to encourage you to definitely continue your great work, have a nice afternoon!