Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real-time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

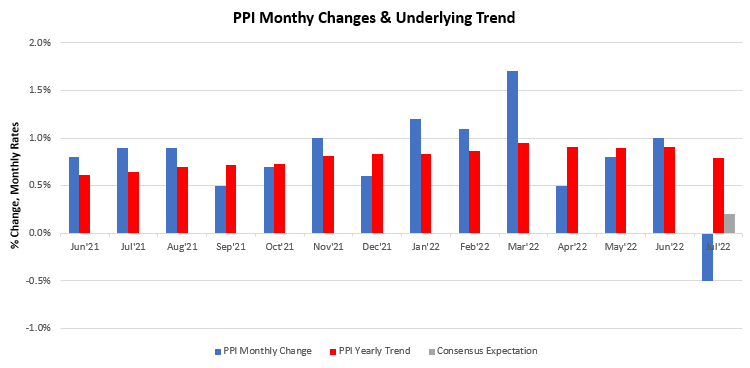

i. PPI data confirmed CPI data, i.e., that weaker energy prices found their way into inflation measures. PPI data came in showing a monthly decrease of -0.5%, leading to a 9.5% change versus a year ago, disappointing consensus expectations. We show this below:

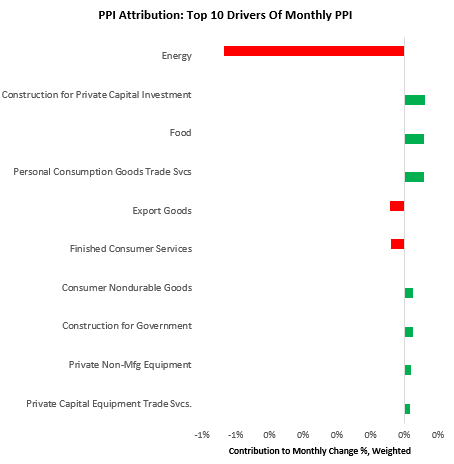

The primary driver of thus move was a significant decline in energy prices. Below, we show the contributions of the top 10 drivers of this PPI print:

This reading was a sequential deceleration within an accelerating trend 12-month trend. Energy, Personal Consumption Goods Trade Svcs, Food, Private Capital Equipment Trade Svcs., and Transportation & Warehousing of Goods for Final Demand have exerted the largest influence on PPI over the last twelve months.

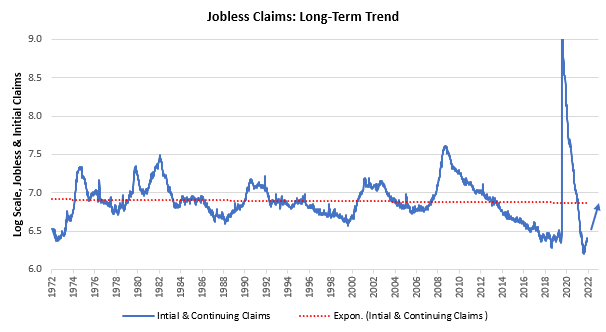

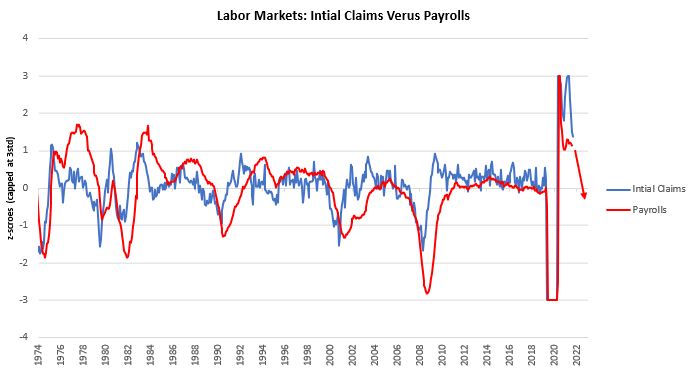

ii. Labor market data continues to deteriorate. Initial claims data came in lower than expected, but continuing claims came in higher. Nonetheless, unemployment is broadly below trend. We a combined measure of initial and continuing claims below, relative to its full-sample trend:

As we can see, the labor market remains extremely tight. However, on a rate of change basis, we are in the early stages of a decline:

iii. The full pace of quantitative tightening has not even begun. We recently received data from the Treasury, telling us that they are, in fact, likely to increase their cash balance at the Federal Reserve, i.e., reducing bank reserves while keeping cash at the Fed. We are not at the full pace of Quantitative Tightening, and the mechanical impacts of these changes are yet to be felt in markets. We show our projections for the impact of QT on reserve balances below:

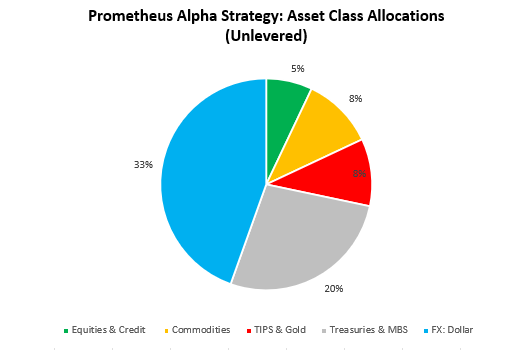

Tightening liquidity conditions create a tough environment for all assets, and we are moving into one of the fastest liquidity tightening in history. Therefore, our Alpha Strategy maintains exposure to the dollar and treasuries while primarily playing for long/short opportunities within other assets. We show the current asset allocation for our Alpha Strategy below:

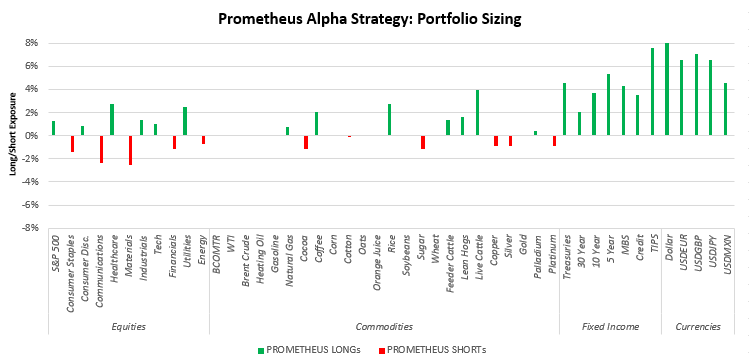

At the security level, we show how the Alpha Strategy is positioned below:

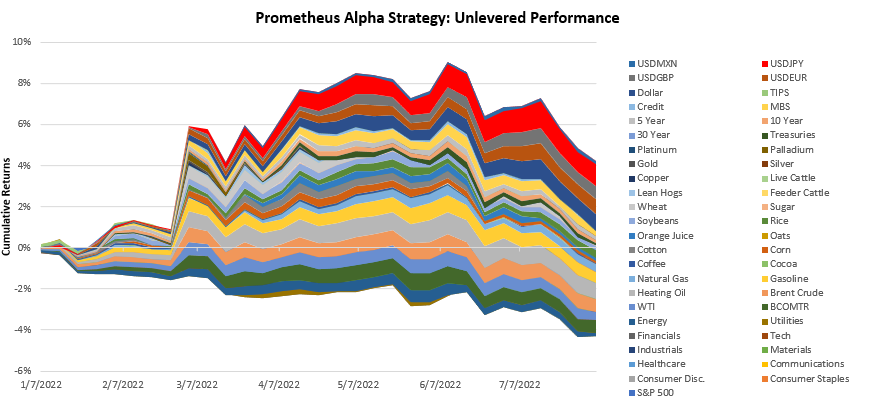

Additionally, we offer the cumulative un-levered year-to-date returns on the strategy below:

Stay defensive.