Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real-time. We are currently on the road with client meetings; hence, this week’s coverage may be slightly less comprehensive than usual. Nonetheless, our Week Ahead this weekend will resume regular coverage.

Today, we will provide updates on our ETF Strategy. Our ETF Strategy algorithmically employs our systematic analysis of the US economy and financial markets to create a rules-based, quantitative portfolio. We use fundamental economic and high-frequency financial data to best understand the macroeconomic environments and codify how to best trade markets. This process creates a robust portfolio solution that attempts to provide high return/risk characteristics and high percentage positive ratios at the portfolio level, regardless of the economic environment. Subscribe below so that you never miss out on our systematic insights into markets and portfolio strategy:

Markets have moved to price tightening liquidity conditions, with ramifications showing across stocks, fixed income & commodities. During tightening liquidity environments, no single risk asset is safe, and long/short exposure is crucial, either via cross-asset long/short exposure or through the dollar. This year has been one where capital preservation has been paramount, and with tightening liquidity being priced into markets, this will become even more important.

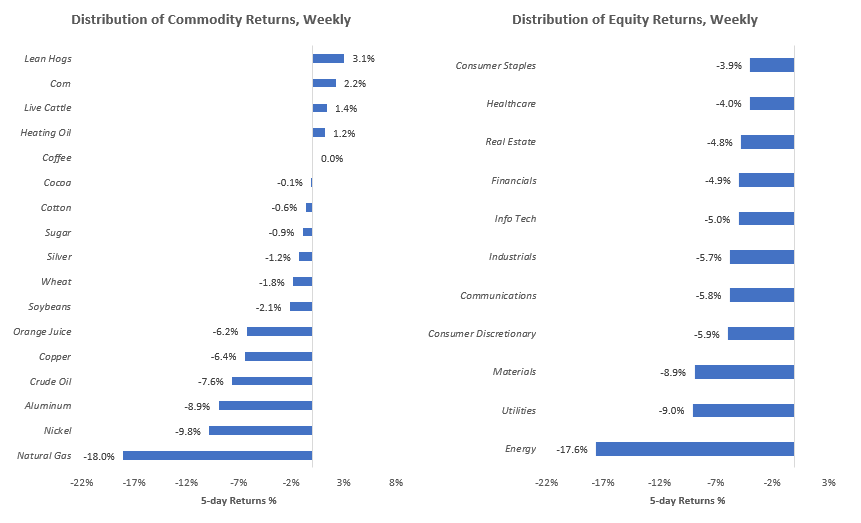

These dynamics showed themselves in both commodity and equity space, with significant downside moves. In particular, energy and energy commodities saw significant headwinds:

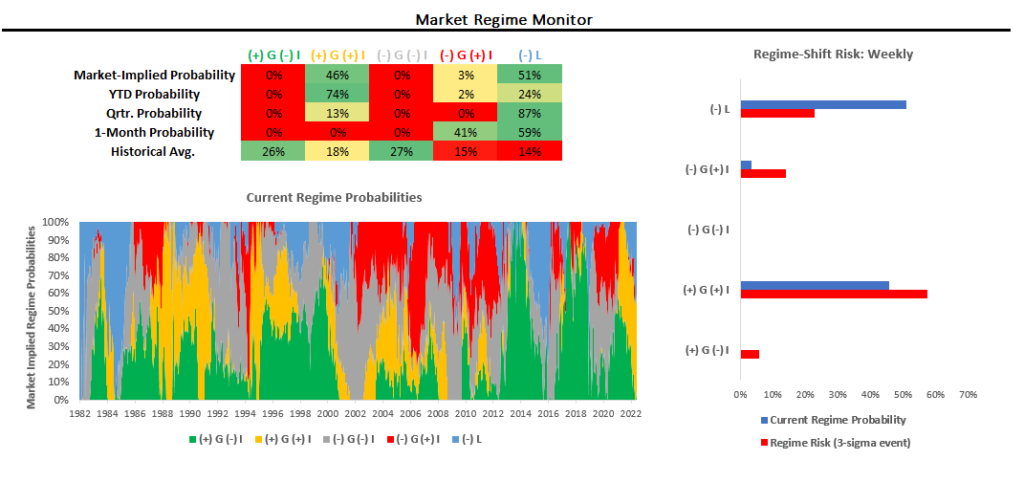

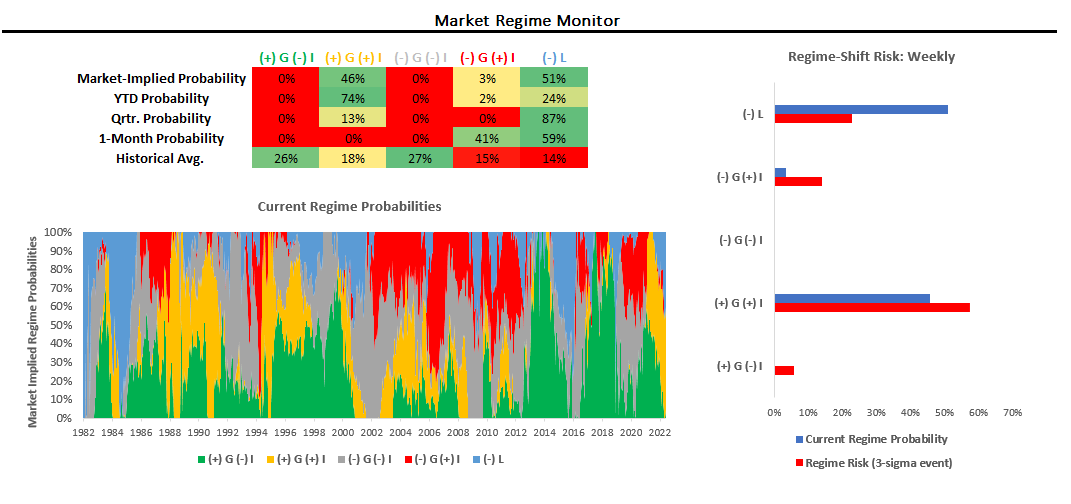

These dynamics are to be expected as tightening liquidity takes hold. Commodities operate through risk transfer markets and have higher volatility and less stable return characteristics relative to capital formation markets like stocks and fixed income. Nonetheless, one week does not make a trend, and our systems continue to tell us we are in an environment of stagflationary nominal growth. In this context, we show our systems gauges of return/risk based on market regime, trend, volatility, & correlation:

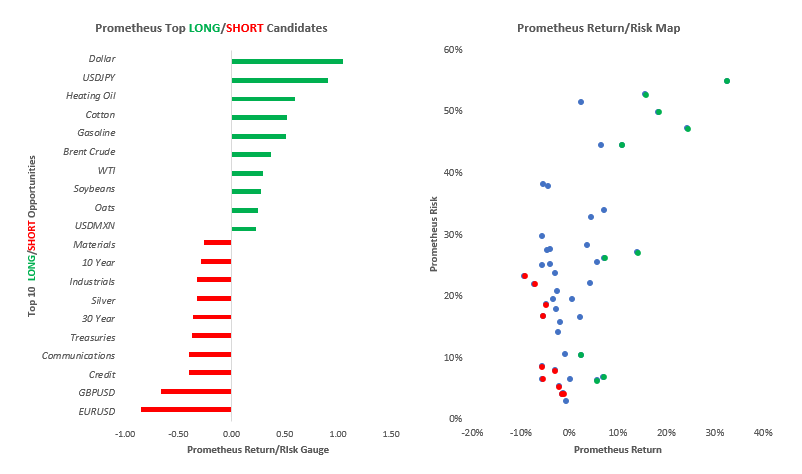

Based on the previously mentioned factors, our systems estimate that the best return/risk characteristics are LONG: Dollar & USDJPY and SHORT: EURUSD & GBPUSD. These positions are dollar positions, reflecting the tightening liquidity regime dynamics. Historically, tightening liquidity conditions tend to be brief but extremely painful, as evidenced by the last ten days of trading.

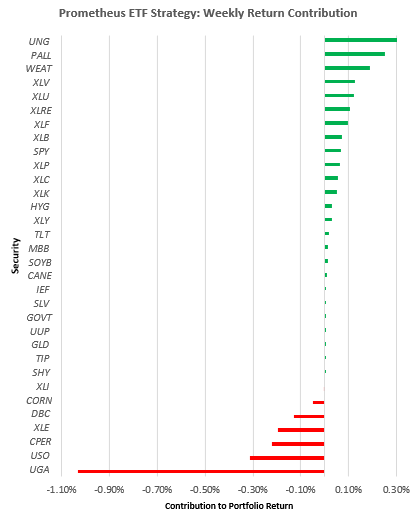

In this environment, our ETF Strategy remained well-positioned this week. However, the outsized moves in Natural Gas (UNG) weighed on the portfolio, creating an unlevered loss at the portfolio level of 1%. Nonetheless, 75% of portfolio positions were in the green this week, telling us that our systems remain well-suited to handle the turbulence of current market dynamics. We show the weekly contributions to portfolio performance below:

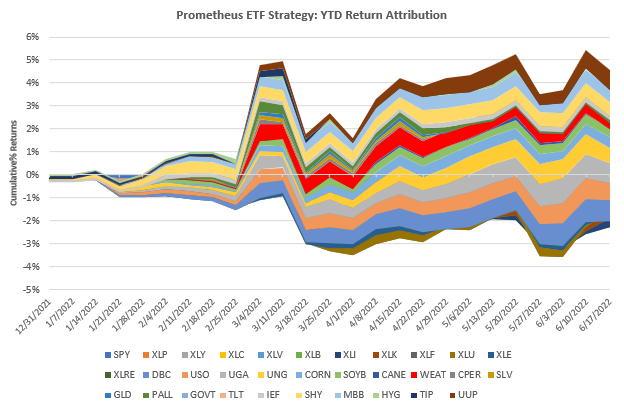

Additionally, we show the year-to-date portfolio performance below:

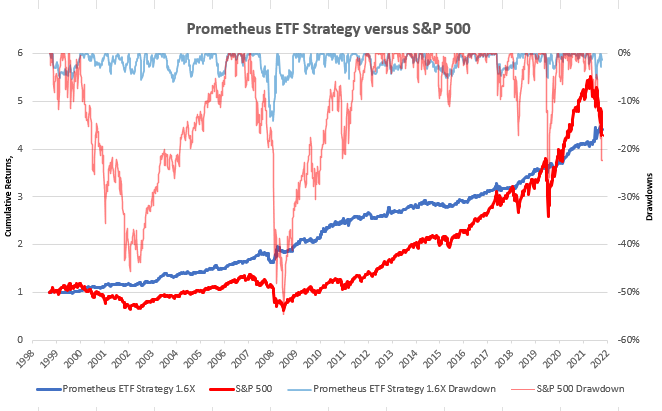

Additionally, we show the full-sample performance of the ETF Strategy, including leverage for illustrative purposes:

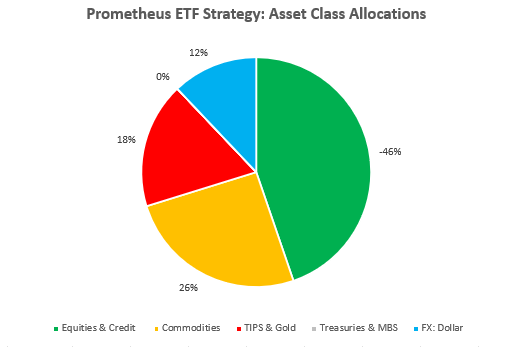

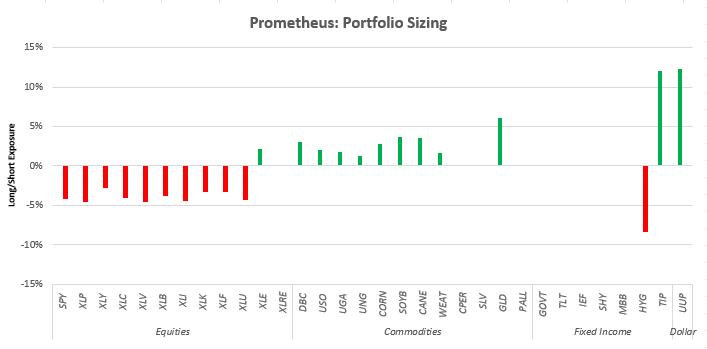

Turning to next week, here is how our systems are positioning the ETF Strategy at the asset class level:

As we can see above, our systems continue to be aggressive short equities & credit while remaining long inflation beneficiaries & the dollar. At the security level, here’s how our systems are looking to position (keep in mind there is still time until the end of the day, so this may change):

-

Stocks: SPY (-5%), XLP (-5%), XLY (-3%), XLC (-5%), XLV (-5%), XLB (-4%), XLI (-5%), XLK (-4%), XLF (-4%), XLU (-5%), XLE (3%)

-

Commodities: DBC (4%), USO (3%), UGA (2%), UNG (2%), CORN(3%), SOYB(4%), CANE(4%), WEAT(2%), GLD (7%),

-

Fixed Income: HYG (-9%), TIP (12%)

-

Dollar: UUP (13%)

We show this graphically below:

Remember, avoiding drawdowns during tightening liquidity environments is the priority, especially when limited to ETFs. Long/short exposure will continue to add performance. We highly recommend active shorting, i.e., actively managing short exposures throughout the week to best crystallize gains. Markets are getting tougher. Stay nimble.

Disclaimer: No information provided by Prometheus should be construed as investment advice.