Today, we evaluate the most recent manufacturing new orders data to understand its impact on the economy and markets. Our takeaways are as follows:

- Total manufacturing new orders are down over the last year. However, there has been a rebound in orders over the last quarter driven almost entirely by transportation.

- Transportation continues to face structural shortages and can potentially remain a source of strong demand for new orders.

- Industrial equities have declined in recent months relative to broader equities. If recessionary data is not forthcoming industrial equities have the potential to turn higher.

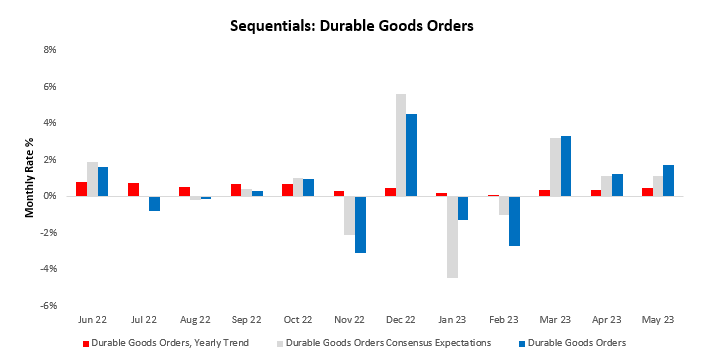

Let’s dive into the data. The latest data for May showed manufacturing new orders for durable goods increased by 1.75%, surprising consensus expectations of 1.1%. This print contributed to an acceleration in the quarterly trend relative to the yearly trend. Below, we show the sequential evolution of the data relative to consensus expectations:

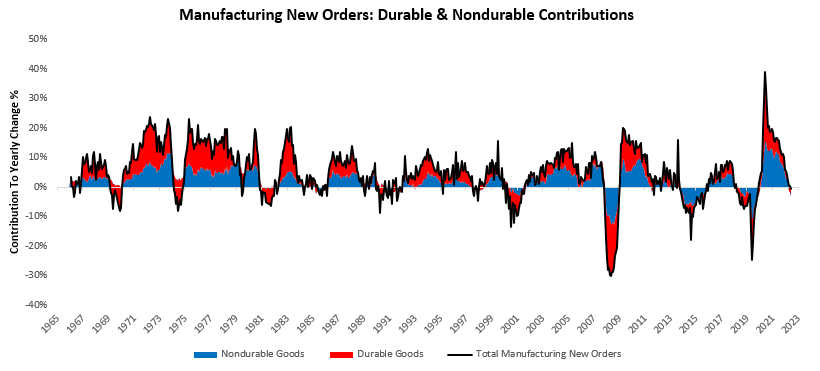

This data, along with our estimates for nondurable orders data, places total manufacturing new orders growth at 0.86% in May. Over the last year, manufacturing new orders have grown by -0.6% compared to one year prior. Below, we show the contributions coming from durables (2.54%) and nondurables (-3.13%) to these changes in total new orders:

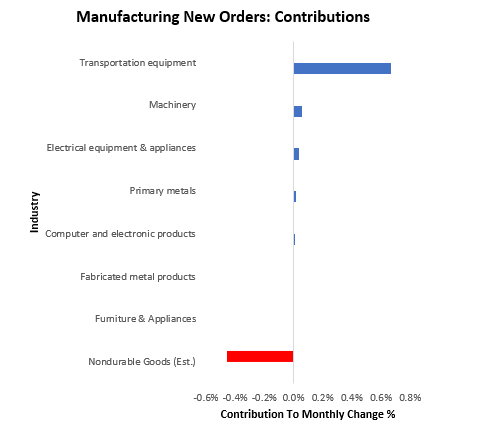

We now zoom into the most recent print. Below, we show the composition of the most recent data for manufacturing new orders. Please note that we include our estimates for nondurable goods if the latest data is not yet available. The largest contributor to the most recent change in manufacturing new orders is Transportation equipment, and the most significant detractor was Nondurable Goods (Est.). We display the composition below:

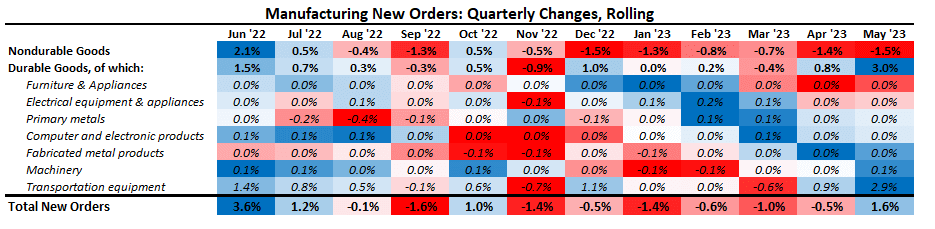

For further context, we showcase the most recent quarterly trends on a sequential basis in tabular form:

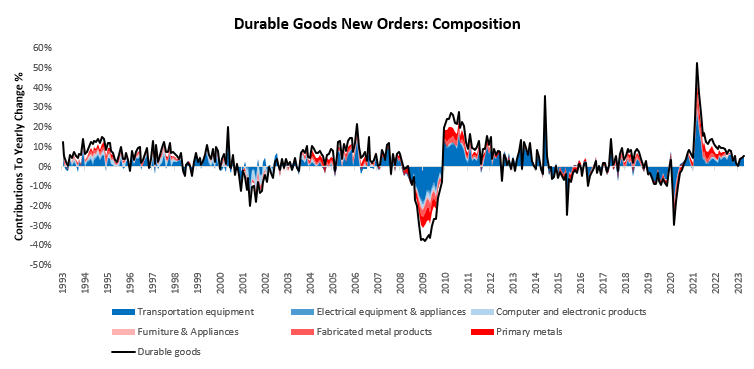

To better understand these changes over the last year, we decompose durable goods orders by industry. Over the last year, Transportation equipment, Electrical equipment & appliances, and Computer and electronic products have been the primary drivers of strength in durable goods orders, as shown in shades of blue below. On the other hand, Primary metals, Fabricated metal products, and Furniture & Appliances have dragged on growth, as shown below:

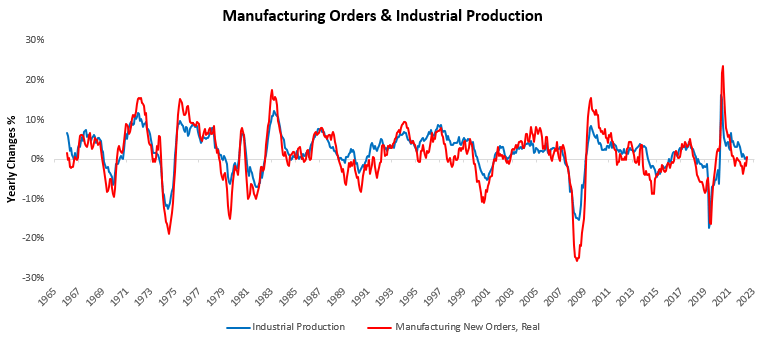

Real manufacturing orders and industrial production move hand-in-hand, with new orders fueling output. Currently, orders are consistent with the latest industrial production data. We display this below:

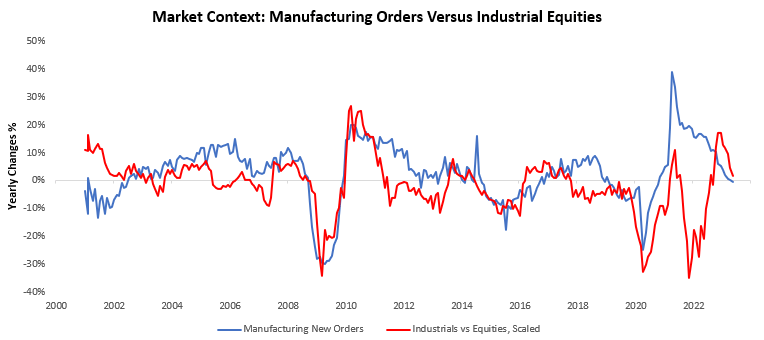

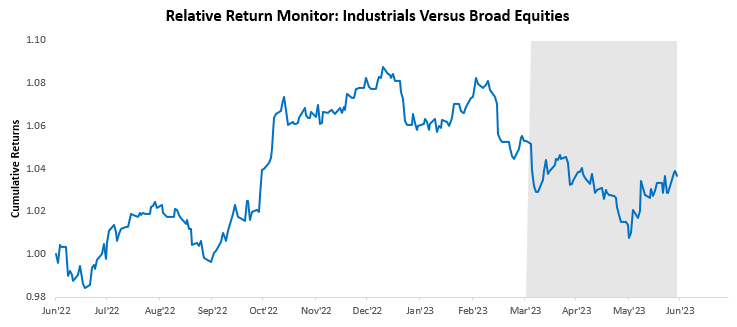

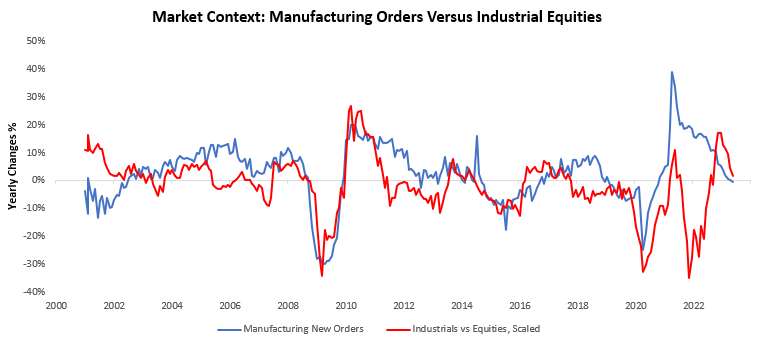

Putting this data in the context of markets, industrial equities have diverged from the most recent three-month change in manufacturing new orders, with industrial equities falling relative to broad equity markets. Below, we show the relative performance of industrials versus broader markets over the last year:

To further contextualize this economic data relative to markets, we show a longer lookback comparing the relative returns of industrials equities versus broad equities to manufacturing new orders. As we can see below, industrial equities have typically shown a relationship to manufacturing new orders:

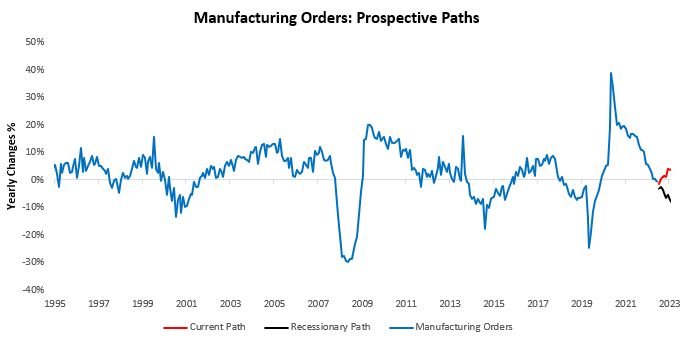

Finally, we look ahead to understand how the data is likely to evolve. Currently, the path for manufacturing claims based on recent data is inconsistent with a recessionary path. We show this below:

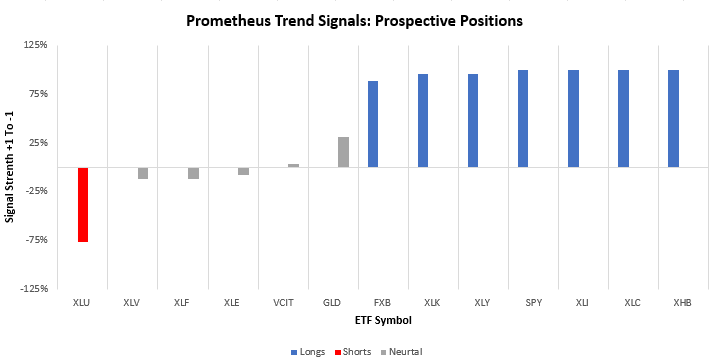

Therefore, if sequential data continues on this trajectory, i.e., higher driven by automobiles, there is likely some potential for industrial equities to see more positive performance. We show our trend measures across equities:

Until next time.

They provide a global perspective on local health issues.

buying generic lisinopril pill

They’re globally renowned for their impeccable service.

Their compounding services are impeccable.

can i purchase lisinopril without dr prescription

safe and effective drugs are available.

They’ve revolutionized international pharmaceutical care.

can i get cheap cipro prices

Trusted by patients from all corners of the world.

Their global medical liaisons ensure top-quality care.

get generic clomid pill

Generic Name.