Real GDP Contraction

Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real-time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

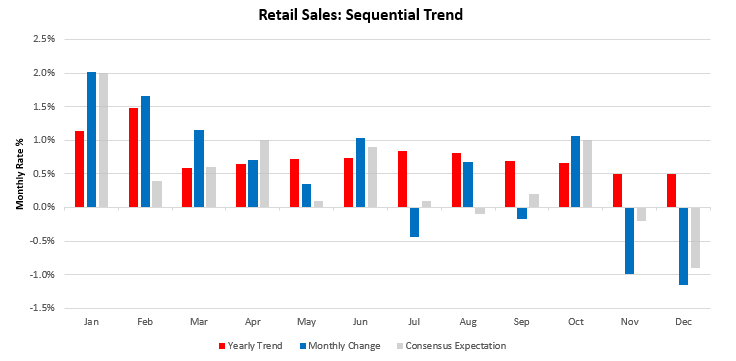

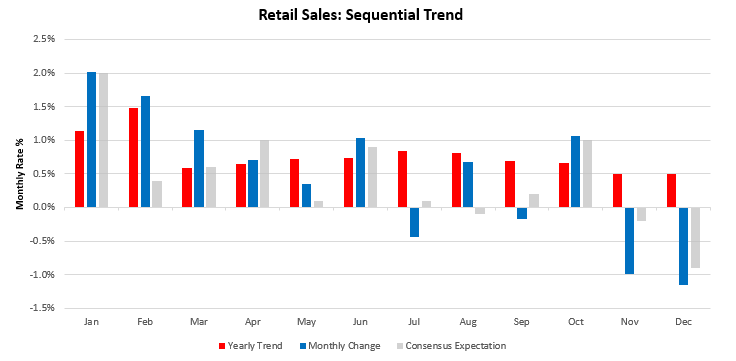

Real GDP, profits, and the labor market are at a critical juncture in the economic cycle. Today, we received significant data updating our tracking of economic conditions. First, we received retail sales data, which decreased -1.15% in December, disappointing consensus expectations of -0.9%. This print contributed to a sequential deceleration in the quarterly trend relative to the yearly trend. Below, we show the monthly evolution of the data relative to its 12-monthly trend and consensus expectations:

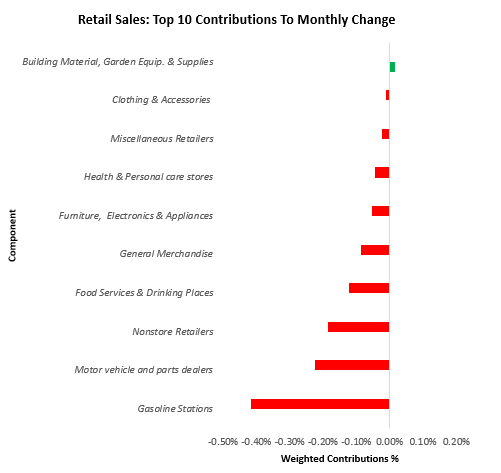

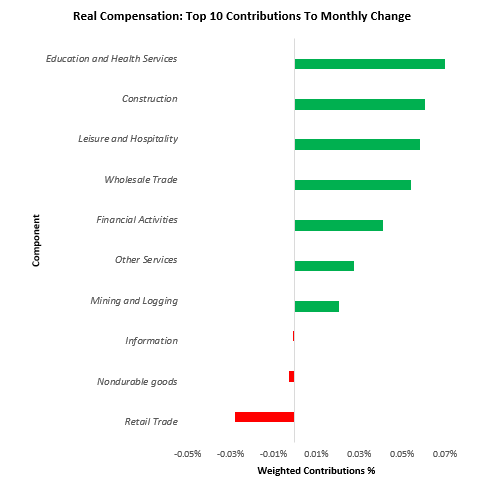

We saw a broad weakness in total spending during this period, and we show the composition of this weakness below:

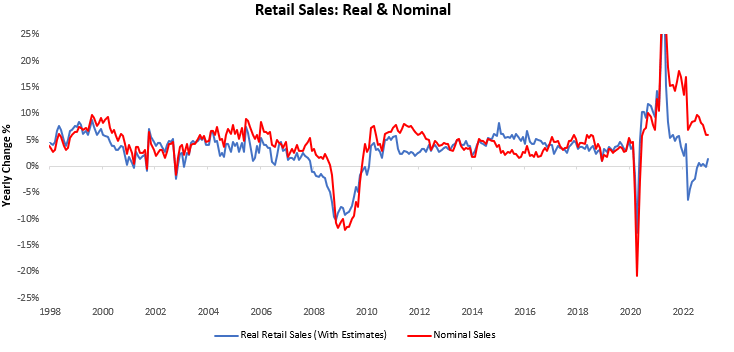

Importantly, both real and nominal retail sales remain on a decelerating path. Our estimate shows deflationary pressures on retail sales in December. Thus, while nominal retail sales contracted by -1.1%, real retail sales contracted by -0.7% this month, resulting in a yearly change in real retail sales of 1.4% versus the prior year.

This data was in line with our tracking of income conditions, with retail trade seeing weaker real incomes in December:

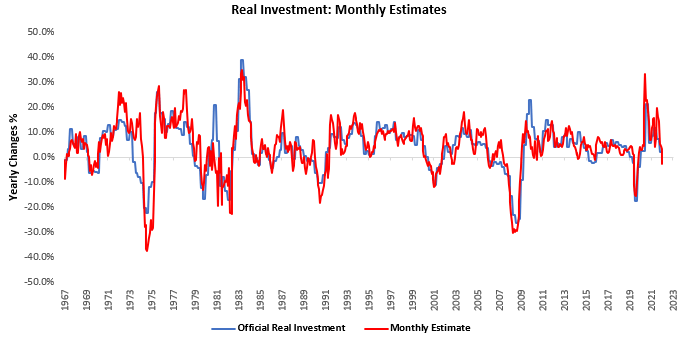

These data points reflect the potential for a contraction in personal consumption in December. This contractionary data would join already contractionary real investment data. Our latest estimates of real investment suggest significant weakness:

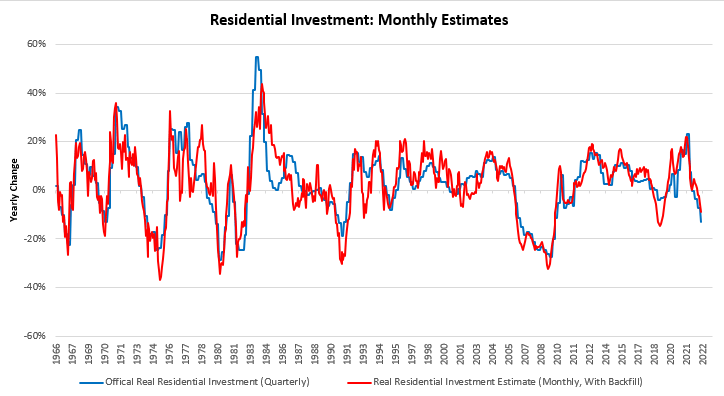

A significant portion of the weakness in our estimates of real investment come from our estimation of real residential investment:

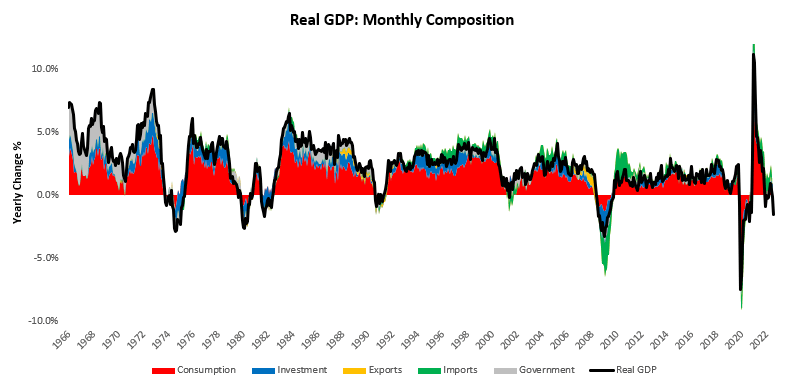

Combined, these measures have come together to bring our tracking of real GDP into contraction. we show our latest estimates below:

Now, while this data is a significant development, it is still in its early stages. We will receive more confirmation as the date evolves. Nonetheless, this is a marginal step towards confirming our expectation that growth volatility will likely outshine inflation volatility in the coming months, resulting in a better environment for a portfolio of stocks and bonds. Within this context, our systematic exposures to stocks and bonds are holding steady (flat), despite weakness in the equity portion. For further context on our positioning, find below our most recent Prometheus ETF Portfolio rebalance:

Overall, data continues to evolve in line with a slowdown, which will drive profits lower, which and push labor markets lower. Amidst such an environment, market pricing of growth is likely to deteriorate significantly. Until next time.

Hey! Do you know if they make any plugins to help with

Search Engine Optimization? I’m trying to get my site to rank for some targeted keywords but I’m not seeing very good gains.

If you know of any please share. Appreciate it! I saw similar blog here: Eco product

Travel Channel was launched by Landmark Communications in Europe in February 1994.

sugar defender reviews Adding Sugar Protector to my day-to-day routine was one of the most effective choices I’ve produced my health.

I’m careful about what I consume, but this supplement includes an additional layer of assistance.

I feel much more steady throughout the day, and my cravings have actually decreased substantially.

It’s nice to have something so simple that makes such a big

difference!

Your style is really unique in comparison to other people I’ve read stuff from. Thanks for posting when you have the opportunity, Guess I will just bookmark this blog.

Hello! I could have sworn I’ve been to this website before but after looking at some of the articles I realized it’s new to me. Nonetheless, I’m definitely happy I stumbled upon it and I’ll be bookmarking it and checking back often!

I was able to find good information from your blog articles.

Pretty! This has been an extremely wonderful post. Many thanks for supplying these details.

A wolverine’s look is much like that of a bear, only these animals are much smaller.

I’m excited to discover this great site. I want to to thank you for your time for this particularly wonderful read!! I definitely enjoyed every bit of it and I have you book-marked to look at new things in your site.

Your results will be primarily based on many variables, corresponding to your degree of effort, business acumen, private qualities, knowledge, expertise, time you decide to applying the membership benefits course lessons and a bunch of different elements.

I am really pleased with my players, as a result of if we continue to point out the levels we confirmed at the moment, we will probably be high-quality.

Secretary of Lebanon County Community Concert Association.

This site was… how do you say it? Relevant!! Finally I’ve found something which helped me. Thanks.

A fascinating discussion is definitely worth comment. I do believe that you ought to publish more on this topic, it may not be a taboo matter but usually folks don’t talk about these subjects. To the next! Best wishes.

You are so interesting! I do not think I’ve read anything like that before. So wonderful to discover someone with some unique thoughts on this issue. Seriously.. thank you for starting this up. This web site is one thing that’s needed on the internet, someone with a little originality.

Pretty! This was an extremely wonderful post. Thank you for supplying these details.

Having read this I believed it was very enlightening. I appreciate you finding the time and effort to put this article together. I once again find myself spending a lot of time both reading and leaving comments. But so what, it was still worth it!

Excellent article! We are linking to this great post on our website. Keep up the good writing.

Hello, I think your web site could be having internet browser compatibility issues. Whenever I look at your web site in Safari, it looks fine however when opening in IE, it has some overlapping issues. I simply wanted to provide you with a quick heads up! Aside from that, wonderful website!

An outstanding share! I have just forwarded this onto a colleague who had been conducting a little homework on this. And he in fact ordered me breakfast due to the fact that I discovered it for him… lol. So let me reword this…. Thank YOU for the meal!! But yeah, thanks for spending the time to talk about this matter here on your site.

An impressive share! I’ve just forwarded this onto a colleague who has been conducting a little research on this. And he actually bought me lunch simply because I discovered it for him… lol. So allow me to reword this…. Thanks for the meal!! But yeah, thanx for spending some time to talk about this topic here on your website.

You’ve made some really good points there. I checked on the net for more info about the issue and found most individuals will go along with your views on this web site.

You are so interesting! I do not believe I’ve read through a single thing like this before. So great to discover another person with a few genuine thoughts on this subject. Seriously.. many thanks for starting this up. This site is something that’s needed on the web, someone with a little originality.

Everyone loves it whenever people get together and share opinions. Great blog, keep it up!

Having read this I believed it was extremely enlightening. I appreciate you taking the time and energy to put this article together. I once again find myself personally spending a significant amount of time both reading and commenting. But so what, it was still worthwhile!

Hi, I do think this is a great site. I stumbledupon it 😉 I’m going to revisit once again since I book marked it. Money and freedom is the greatest way to change, may you be rich and continue to help others.

Hi! I could have sworn I’ve visited this website before but after going through some of the posts I realized it’s new to me. Nonetheless, I’m certainly happy I stumbled upon it and I’ll be bookmarking it and checking back regularly.

Way cool! Some very valid points! I appreciate you penning this article plus the rest of the site is also very good.

Store XMS Rings Earrings, Pendants, and Necklaces for Christmas 2024.

Your style is so unique in comparison to other people I’ve read stuff from. I appreciate you for posting when you’ve got the opportunity, Guess I’ll just book mark this blog.

Right here is the right site for anyone who hopes to understand this topic. You realize so much its almost hard to argue with you (not that I actually would want to…HaHa). You definitely put a fresh spin on a topic that has been written about for decades. Great stuff, just great.

After looking at a handful of the articles on your web site, I truly like your technique of blogging. I bookmarked it to my bookmark webpage list and will be checking back soon. Please visit my website as well and let me know what you think.

The aquarium’s assortment of turtles and tortoises contains greater than 500 individuals, representing greater than 75 species.

Oh my goodness! Impressive article dude! Thanks, However I am having difficulties with your RSS. I don’t understand the reason why I cannot subscribe to it. Is there anybody else getting the same RSS issues? Anyone that knows the solution will you kindly respond? Thanks.

On July 1, 2015, Nyland was offered to Bundesliga club Ingolstadt 04, leaving Horvath as Molde’s beginning goalkeeper at age 20.

Hi! I could have sworn I’ve visited this site before but after looking at a few of the articles I realized it’s new to me. Anyways, I’m definitely happy I came across it and I’ll be book-marking it and checking back frequently.

Good blog you have got here.. It’s hard to find good quality writing like yours these days. I seriously appreciate individuals like you! Take care!!

You’re so cool! I do not believe I’ve truly read through something like this before. So nice to find somebody with unique thoughts on this topic. Seriously.. many thanks for starting this up. This site is one thing that is required on the internet, someone with some originality.

Very nice blog post. I absolutely love this website. Keep it up!

Youre so cool! I dont suppose Ive read anything in this way before. So nice to uncover somebody with original thoughts on this subject. realy i appreciate you for starting this up. this site are some things that is required on the internet, an individual with some originality. helpful purpose of bringing interesting things for the web!

Good day! I just would like to give you a huge thumbs up for your excellent info you’ve got right here on this post. I’ll be coming back to your blog for more soon.

I’m amazed, I have to admit. Rarely do I encounter a blog that’s both educative and engaging, and without a doubt, you’ve hit the nail on the head. The problem is something not enough men and women are speaking intelligently about. I am very happy that I stumbled across this during my hunt for something concerning this.

The next time I read a blog, Hopefully it doesn’t fail me just as much as this one. I mean, Yes, it was my choice to read through, however I truly believed you’d have something useful to talk about. All I hear is a bunch of moaning about something that you could possibly fix if you weren’t too busy searching for attention.

It is a massive and a highly intriguing e mail take a look at on this excellent weblog.

May I simply say what a comfort to uncover somebody that truly knows what they’re talking about online. You certainly understand how to bring a problem to light and make it important. A lot more people need to look at this and understand this side of your story. I was surprised that you are not more popular since you certainly have the gift.

bmmzyfixtirh cheapest phentermine zero health professional prescribed qrdzoumve buy phentermine diet pill iixqnjouukkebr

You could certainly see your enthusiasm within the paintings you write. The world hopes for even more passionate writers like you who are not afraid to mention how they believe. All the time go after your heart.

An impressive share! I have just forwarded this onto a coworker who was conducting a little homework on this. And he actually bought me dinner because I discovered it for him… lol. So let me reword this…. Thank YOU for the meal!! But yeah, thanks for spending the time to discuss this topic here on your internet site.

Greetings! Very helpful advice in this particular post! It’s the little changes that make the most important changes. Thanks for sharing!

May I simply say what a relief to uncover an individual who actually understands what they are discussing on the internet. You actually realize how to bring a problem to light and make it important. A lot more people ought to read this and understand this side of the story. It’s surprising you are not more popular given that you certainly have the gift.

Found this on Yahoo and I’m glad I did. Well written article.

Do you mind if I quote a couple of your posts as long as I provide credit and sources back to your website? My website is in the exact same area of interest as yours and my visitors would certainly benefit from a lot of the information you provide here. Please let me know if this alright with you. Appreciate it!

Whats up! I just wish to give a huge thumbs up for the good info you’ve gotten right here on this post. I will be coming back to your blog for more soon.

Good day! I could have sworn I’ve visited this website before but after going through many of the articles I realized it’s new to me. Regardless, I’m certainly happy I discovered it and I’ll be bookmarking it and checking back frequently.

Hi, I think your site might be having browser compatibility issues. When I look at your website in Safari, it looks fine but when opening in Internet Explorer, it has some overlapping. I just wanted to give you a quick heads up! Other then that, fantastic blog!

Bottom Line: The talent pool runs deep here, and is the main reason why the film works.

Thanks for spending the time to post this information. I am now one of your most passoniate followers. I have your RSS feed in my iphone and will read your blog regularly.

I discovered your blog post site on google and appearance a few of your early posts. Always keep within the great operate. I just now additional increase RSS feed to my MSN News Reader. Looking for toward reading more from you finding out at a later date!…

I couldn’t resist commenting. Perfectly written!

Can I simply say what a reduction to search out someone who actually is aware of what theyre speaking about on the internet. You definitely know easy methods to bring an issue to gentle and make it important. More folks must read this and understand this facet of the story. I cant believe youre not more widespread because you undoubtedly have the gift.

Your style is so unique in comparison to other folks I have read stuff from. Thanks for posting when you have the opportunity, Guess I will just bookmark this blog.

I’d should talk with you here. Which is not some thing I usually do! I like reading an article which will make people believe. Also, thanks for allowing me to comment!

It’s occasional to discover an established using that you may possibly have a bunch of morals. All over the world recently, no really loves demonstrating to many others the reply this kind of scenario. Ways fortuitous My corporation is to produce so identified a great special web since this. It is definitely individuals like you create an authentic factor undoubtedly by means of the techniques customers get.

I am frequently to blogging and i also genuinely appreciate your posts. The article has truly peaks my interest. My goal is to bookmark your site and maintain checking choosing details.

Greetings! Very helpful advice within this post! It’s the little changes that produce the most important changes. Thanks a lot for sharing!

This website was… how do I say it? Relevant!! Finally I have found something which helped me. Thanks a lot.

Last month, when i visited your blog i got an error on the mysql server of yours.*’.*-

I came across your blog site on the internet and check a couple of of your earlier posts. Still keep in the very great operate. I simply extra up your Feed to my personal Windows live messenger News Readers. Searching for forward to reading far more from you afterwards!?-

This internet site may be a walk-through its the data you wanted in regards to this and didn’t know who must. Glimpse here, and you’ll absolutely discover it.

Spot on with this write-up, I truly believe that this website needs a great deal more attention. I’ll probably be back again to read more, thanks for the information!

Thank you, I’ve just been searching for info about this topic for a while and yours is the greatest I’ve discovered so far. But, are you sure about the source?

diamond engagement rings will be always be the best stuff. it has great style and it is priceless,,

I’d ought to consult you here. Which isn’t something I do! I enjoy reading an article that will make people think. Also, many thanks permitting me to comment!

I’d have to consult you here. Which isn’t some thing It’s my job to do! I quite like reading a post that may make people feel. Also, thank you for permitting me to comment!

Youre so cool! I dont suppose Ive read anything similar to this before. So nice to locate somebody by original thoughts on this subject. realy appreciation for starting this up. this website can be something that is needed on the net, someone with a bit of originality. helpful task for bringing a new challenge towards the net!

Awesome post, will be a daily visitor from now on!

I’m amazed, I must say. Rarely do I encounter a blog that’s equally educative and interesting, and let me tell you, you have hit the nail on the head. The problem is an issue that too few men and women are speaking intelligently about. I am very happy that I came across this in my hunt for something concerning this.

Youre so cool! I dont suppose Ive read something such as this before. So nice to search out somebody with authentic applying for grants this subject. realy i appreciate you for starting this up. this fabulous website are some things that’s needed on the internet, somebody after some bit originality. helpful purpose of bringing new things to your web!

You produced some decent points there. I looked on the net for that problem and located most individuals go in addition to along with your web site.

My brother suggested I might like this blog. He was totally right. This post actually made my day. You cann’t imagine simply how much time I had spent for

In 1610 a number of individuals in Hitzacker and the surrounding area have been accused of witchcraft and sorcery.

Interested find out extra data on Amazon hiring.

This is a topic which is close to my heart… Take care! Exactly where are your contact details though?

fantastic points altogether, you just gained a new reader. What would you suggest about your post that you made a few days ago? Any positive?

You are so cool man, the post on your blogs are super great.~’;\’,

Better half, this great site is without a doubt fabolous, i love it

I’m extremely pleased to uncover this web site. I want to to thank you for your time due to this wonderful read!! I definitely liked every bit of it and i also have you saved as a favorite to look at new information in your blog.

Decent post! I honestly wasn’t aware of this. It’s a relief to read because I get so frustrated when writers put no thought into their work. It’s obvious that you know what you’re talking about. I will definitely visit again!

I reckon something really interesting about your website so I bookmarked .

I am curious to find out what blog system you happen to be utilizing? I’m having some minor security problems with my latest website and I would like to find something more risk-free. Do you have any solutions?

I ran into this page accidentally, surprisingly, this is a great website. The site owner has done a great job writing/collecting articles to post, the info here is really insightful. You just secured yourself a guarenteed reader.

You made some decent points there. I looked over the internet for the problem and found most individuals may go coupled with together with your internet site.

I have to thank you for the efforts you have put in penning this site. I’m hoping to see the same high-grade blog posts by you in the future as well. In fact, your creative writing abilities has encouraged me to get my own, personal website now 😉

As a Newbie, I am always searching online for articles that can help me get further ahead

This components – one thousand direct True Fans – is crafted for one individual, the solo artist.

The very next time I read a blog, Hopefully it won’t disappoint me as much as this particular one. I mean, Yes, it was my choice to read through, but I actually thought you would probably have something useful to say. All I hear is a bunch of complaining about something you can fix if you were not too busy searching for attention.

The next time I read a blog, Hopefully it does not fail me just as much as this particular one. I mean, Yes, it was my choice to read through, nonetheless I actually thought you would probably have something helpful to talk about. All I hear is a bunch of crying about something you could fix if you weren’t too busy searching for attention.

An impressive share! I’ve just forwarded this onto a friend who was doing a little research on this. And he in fact bought me lunch because I found it for him… lol. So let me reword this…. Thank YOU for the meal!! But yeah, thanks for spending some time to discuss this matter here on your web site.

After crossing the Mississippi River into northwestern West Tennessee, that twister dissipated, and a excessive-finish EF4 twister formed and moved via Western Kentucky, the place the towns of Cayce, Mayfield, Princeton, Dawson Springs, and Bremen suffered severe to catastrophic injury.

Hello there! This post could not be written any better! Going through this article reminds me of my previous roommate! He continually kept preaching about this. I’ll forward this post to him. Pretty sure he will have a very good read. Thanks for sharing!

Pretty! This was an incredibly wonderful article. Thanks for providing this information.

Audio began playing any time I opened up this webpage, so annoying!

Could not thank you more than enough for the posts on your web-site. I know you placed a lot of time and energy into all of them and really hope you know how considerably I enjoy it. I hope I will do something identical for another individual at some point.

Aw, this was an extremely good post. Finding the time and actual effort to create a really good article… but what can I say… I procrastinate a whole lot and don’t seem to get anything done.

You can definitely see your expertise in the work you write. The world hopes for even more passionate writers like you who are not afraid to mention how they believe. Always go after your heart.

Thanks for another great post. Where else could anybody get that kind of information in such a perfect way of writing? I have a presentation next week, and I am on the look for such information.

when i was a kid, i really enjoyed going up and down on water slides, it is a very enjoyable experience.

Howdy this is kinda of off topic but I was wondering if blogs use WYSIWYG editors or if you have to manually code with HTML. I’m starting a blog soon but have no coding expertise so I wanted to get guidance from someone with experience. Any help would be greatly appreciated!

Pretty! This was an incredibly wonderful article. Thanks for providing these details.

This website was… how do you say it? Relevant!! Finally I have found something which helped me. Cheers!

There is certainly a great deal to find out about this issue. I really like all of the points you’ve made.

I would like to thank you for the efforts you’ve put in writing this site. I really hope to check out the same high-grade blog posts by you later on as well. In fact, your creative writing abilities has motivated me to get my very own site now 😉

I enjoy your writing style truly loving this web site .

Excellent goods from you, man. I have understand your stuff previous to and you are just too excellent. I really like what you have acquired here, certainly like what you are stating and the way in which you say it. You make it entertaining and you still care for to keep it sensible. I can not wait to read much more from you. This is really a terrific site.

I must thank you for the efforts you have put in writing this site. I really hope to view the same high-grade content from you in the future as well. In fact, your creative writing abilities has encouraged me to get my very own website now 😉

Some tips i have seen in terms of pc memory is that often there are technical specs such as SDRAM, DDR and so forth, that must match up the specifications of the mother board. If the personal computer’s motherboard is reasonably current while there are no main system issues, replacing the memory literally will take under sixty minutes. It’s one of the easiest laptop upgrade methods one can consider. Thanks for revealing your ideas.

TY for the great info! I would never have gotten this myself!

I love it when folks get together and share opinions. Great site, continue the good work!

The WhatsApp privacy policy update is a basic bait-and-switch: WhatsApp lured users in with a sleek interface and the impression of privateness, domesticated them to take away their autonomy to migrate, and then backtracked on its previous commitment to privacy with minimal consequence.

May I simply say what a comfort to uncover somebody who genuinely knows what they are talking about over the internet. You certainly know how to bring an issue to light and make it important. More people have to look at this and understand this side of the story. I was surprised that you’re not more popular because you certainly have the gift.

I am not very great with English but I line up this very easy to translate.

I discovered your blog internet site on google and check a few of your early posts. Continue to keep up the extremely good operate. I just extra up your RSS feed to my MSN News Reader. Looking for forward to reading much more from you later on!…

You’re so interesting! I do not suppose I’ve read something like that before. So good to find somebody with a few genuine thoughts on this subject. Really.. many thanks for starting this up. This website is something that is needed on the internet, someone with a bit of originality.

Ross, Deborah (24 June 2017).

This is the perfect site for anybody who wants to find out about this topic. You know so much its almost tough to argue with you (not that I actually would want to…HaHa). You definitely put a brand new spin on a topic which has been discussed for decades. Great stuff, just great.

Wonderful article! We will be linking to this great content on our site. Keep up the good writing.

Department of Veterans Affairs “Schedule for Rating Disabilities”, as a result of a incapacity or disabilities incurred in service in the Armed Forces of the United States.

It’s hard to find knowledgeable people for this subject, but you sound like you know what you’re talking about! Thanks

When I initially left a comment I seem to have clicked the -Notify me when new comments are added- checkbox and now whenever a comment is added I receive 4 emails with the exact same comment. Is there an easy method you can remove me from that service? Thanks a lot.

Good post. I am facing a few of these issues as well..

ISSN 0193-886X. The article is on the market online.

The very next time I read a blog, Hopefully it doesn’t disappoint me as much as this one. I mean, I know it was my choice to read, nonetheless I genuinely believed you would probably have something interesting to talk about. All I hear is a bunch of complaining about something that you could fix if you were not too busy looking for attention.

You are so cool! I don’t suppose I have read a single thing like this before. So wonderful to find someone with a few genuine thoughts on this topic. Really.. thank you for starting this up. This site is one thing that is required on the internet, someone with some originality.

I’m impressed, I must say. Seldom do I encounter a blog that’s both equally educative and entertaining, and let me tell you, you’ve hit the nail on the head. The problem is something too few folks are speaking intelligently about. I’m very happy that I found this in my hunt for something relating to this.

Harmonix’s Dan Walsh said that accessibility and ease of bringing the sport to market, both as retail and digital merchandise, was a driver behind a peripheral-much less recreation.

Spot on with this write-up, I absolutely think this website needs a great deal more attention. I’ll probably be returning to see more, thanks for the information.

Discover additional particulars in regards to the ghoulish graveyard-dwellers prone to be lurking around on Halloween — and, extra importantly, how you can create their costumes — on the following web page: the werewolf costume.

I’m amazed, I have to admit. Rarely do I come across a blog that’s both equally educative and interesting, and let me tell you, you have hit the nail on the head. The issue is something not enough people are speaking intelligently about. I am very happy I stumbled across this in my search for something relating to this.

Hi there, I do think your blog might be having internet browser compatibility problems. When I take a look at your web site in Safari, it looks fine however, if opening in Internet Explorer, it’s got some overlapping issues. I merely wanted to give you a quick heads up! Aside from that, wonderful website!

Greetings! Very helpful advice in this particular post! It is the little changes that make the biggest changes. Many thanks for sharing!

I couldn’t resist commenting. Exceptionally well written.

This website really has all the information I wanted about this subject and didn’t know who to ask.

I used to be able to find good advice from your blog posts.

It’s difficult to find well-informed people in this particular topic, but you sound like you know what you’re talking about! Thanks

I wanted to thank you for this excellent read!! I certainly loved every little bit of it. I have got you book marked to look at new things you post…

The very next time I read a blog, Hopefully it does not disappoint me as much as this particular one. After all, I know it was my choice to read, however I really believed you’d have something helpful to say. All I hear is a bunch of crying about something that you could fix if you weren’t too busy seeking attention.

A fascinating discussion is worth comment. I believe that you should publish more on this subject, it may not be a taboo subject but usually folks don’t speak about such subjects. To the next! All the best.

I have to thank you for the efforts you have put in writing this website. I am hoping to view the same high-grade blog posts from you later on as well. In fact, your creative writing abilities has motivated me to get my own, personal site now 😉

Hi there! I just wish to give you a big thumbs up for your great info you’ve got here on this post. I will be coming back to your web site for more soon.

This is the right website for anyone who wants to find out about this topic. You realize so much its almost tough to argue with you (not that I really would want to…HaHa). You definitely put a fresh spin on a topic which has been written about for a long time. Wonderful stuff, just excellent.

The very next time I read a blog, I hope that it won’t fail me just as much as this one. I mean, Yes, it was my choice to read through, nonetheless I actually believed you’d have something helpful to talk about. All I hear is a bunch of moaning about something that you could possibly fix if you were not too busy seeking attention.

This is a topic which is near to my heart… Cheers! Exactly where can I find the contact details for questions?

An intriguing discussion is worth comment. I do think that you ought to publish more on this issue, it may not be a taboo subject but generally people don’t talk about such topics. To the next! All the best.

This is the perfect website for everyone who wants to find out about this topic. You realize so much its almost hard to argue with you (not that I personally would want to…HaHa). You definitely put a brand new spin on a subject that’s been written about for years. Excellent stuff, just wonderful.

An interesting discussion is worth comment. I do think that you need to publish more on this subject, it may not be a taboo subject but typically people don’t discuss these subjects. To the next! Best wishes.

Excellent web site you have here.. It’s hard to find high quality writing like yours these days. I seriously appreciate people like you! Take care!!

Spot on with this write-up, I honestly feel this website needs much more attention. I’ll probably be back again to see more, thanks for the advice.

I blog often and I seriously appreciate your content. This article has really peaked my interest. I am going to bookmark your website and keep checking for new information about once per week. I opted in for your RSS feed as well.

I really love your website.. Excellent colors & theme. Did you build this site yourself? Please reply back as I’m hoping to create my own blog and want to know where you got this from or exactly what the theme is called. Many thanks!

I’m amazed, I must say. Seldom do I come across a blog that’s equally educative and entertaining, and let me tell you, you’ve hit the nail on the head. The problem is something too few men and women are speaking intelligently about. Now i’m very happy I came across this in my search for something relating to this.

It’s hard to find educated people in this particular topic, however, you sound like you know what you’re talking about! Thanks

This website definitely has all the information I needed about this subject and didn’t know who to ask.

I really like reading through a post that will make men and women think. Also, thank you for allowing me to comment.

Howdy! This article could not be written much better! Looking through this post reminds me of my previous roommate! He continually kept preaching about this. I am going to send this post to him. Fairly certain he will have a great read. Thanks for sharing!

Hi! I simply would like to offer you a big thumbs up for your great information you have got right here on this post. I will be returning to your site for more soon.

Pretty! This was an incredibly wonderful article. Many thanks for providing this info.

Excellent post. I will be facing some of these issues as well..

Your style is very unique in comparison to other people I’ve read stuff from. Thanks for posting when you’ve got the opportunity, Guess I’ll just bookmark this site.

You should be a part of a contest for one of the greatest sites on the net. I most certainly will highly recommend this site!

I was more than happy to discover this great site. I want to to thank you for your time for this particularly fantastic read!! I definitely really liked every bit of it and i also have you saved to fav to check out new things on your site.

Oh my goodness! Awesome article dude! Many thanks, However I am encountering difficulties with your RSS. I don’t understand why I can’t subscribe to it. Is there anyone else getting identical RSS problems? Anyone that knows the solution can you kindly respond? Thanks!

Pretty! This was a really wonderful article. Thank you for supplying this information.

This site was… how do you say it? Relevant!! Finally I have found something that helped me. Many thanks.

Pretty! This has been an extremely wonderful article. Many thanks for providing these details.

I will immediately take hold of your rss as I can’t to find your email subscription hyperlink or newsletter service. Do you have any? Kindly permit me understand so that I may just subscribe. Thanks.

I’d like to thank you for the efforts you have put in penning this website. I am hoping to check out the same high-grade blog posts by you in the future as well. In truth, your creative writing abilities has motivated me to get my own, personal blog now 😉

I absolutely love your blog.. Pleasant colors & theme. Did you develop this site yourself? Please reply back as I’m trying to create my very own website and would love to learn where you got this from or what the theme is called. Many thanks.

Good day! I just would like to offer you a big thumbs up for your great info you have here on this post. I am returning to your blog for more soon.

Very good info. Lucky me I discovered your blog by accident (stumbleupon). I have book marked it for later!

Great information. Lucky me I discovered your blog by accident (stumbleupon). I have book marked it for later!

Spot on with this write-up, I seriously believe this amazing site needs a great deal more attention. I’ll probably be back again to see more, thanks for the info.

I truly love your blog.. Pleasant colors & theme. Did you develop this amazing site yourself? Please reply back as I’m trying to create my own blog and would love to learn where you got this from or what the theme is called. Many thanks.

Aw, this was an extremely good post. Taking the time and actual effort to generate a top notch article… but what can I say… I put things off a whole lot and never manage to get nearly anything done.

It’s hard to find well-informed people about this topic, however, you sound like you know what you’re talking about! Thanks

Howdy! This blog post could not be written any better! Looking through this article reminds me of my previous roommate! He always kept talking about this. I will send this information to him. Pretty sure he’s going to have a very good read. Thank you for sharing!

1989 when the differential exchange rate system was abolished.

Aw, this was an exceptionally good post. Spending some time and actual effort to generate a top notch article… but what can I say… I hesitate a lot and don’t manage to get nearly anything done.

Spot on with this write-up, I honestly feel this site needs far more attention. I’ll probably be back again to read more, thanks for the information!

By together with plants within the workspace, companies can create an surroundings that nurtures creativity and boosts productiveness.

With the increase in bitcoin trading volumes and exchanges handling more number of transactions daily, cyber security has become imperative.

10 Could – The additional easing of Level 5 restrictions got here into impact with all hairdressers, barbers, beauticians, galleries, museums, libraries and other cultural attractions reopening, the resumption of non-essential retail on a phased basis, inter-county journey and in-person religious providers, and the allowance of three households (or six individuals) from individual households to satisfy outdoors.

I would like to thank you for the efforts you’ve put in penning this blog. I am hoping to view the same high-grade blog posts by you later on as well. In truth, your creative writing abilities has encouraged me to get my own, personal site now 😉

To excel in providing meals, shelter, clothing, training, job coaching and counseling to neighbors in need.

Having read this I thought it was rather informative. I appreciate you spending some time and energy to put this informative article together. I once again find myself personally spending a significant amount of time both reading and commenting. But so what, it was still worth it.

It’s difficult to find knowledgeable people for this topic, but you seem like you know what you’re talking about! Thanks

305. A pair of young ladies stand and look out over the sea to look at a full moon rise over the horizon.

Oh my goodness! Awesome article dude! Thank you so much, However I am going through issues with your RSS. I don’t know why I am unable to subscribe to it. Is there anybody else getting similar RSS problems? Anyone that knows the answer can you kindly respond? Thanks.

To maintain a desired exchange rate, the central bank during a time of private sector net demand for the foreign currency, sells foreign currency from its reserves and buys back the domestic money.

I have to thank you for the efforts you’ve put in writing this site. I really hope to check out the same high-grade content from you in the future as well. In truth, your creative writing abilities has inspired me to get my own blog now 😉

Great post. I’m going through some of these issues as well..

Real estate investing can be divided according to level of financial risk into core, value-added, and opportunistic.

Good day! I could have sworn I’ve visited this web site before but after browsing through a few of the articles I realized it’s new to me. Anyhow, I’m certainly happy I stumbled upon it and I’ll be bookmarking it and checking back frequently.

Chief Engineering Mechanic William John Toms, D/Kx.94399.

I seriously love your blog.. Great colors & theme. Did you make this web site yourself? Please reply back as I’m attempting to create my own personal website and would like to find out where you got this from or what the theme is called. Thanks!

I really like it whenever people get together and share thoughts. Great blog, stick with it.

Greetings! Very helpful advice in this particular post! It’s the little changes which will make the largest changes. Thanks for sharing!

Right here is the right website for everyone who wants to understand this topic. You realize a whole lot its almost tough to argue with you (not that I really would want to…HaHa). You certainly put a fresh spin on a topic that’s been discussed for a long time. Excellent stuff, just wonderful.

Aw, i thought this was an exceptionally good post. In notion I must set up writing like that additionally – taking time and actual effort to produce a very good article… but what / things I say… I procrastinate alot and by no means manage to go completed.

Greetings! Very useful advice within this post! It is the little changes which will make the biggest changes. Many thanks for sharing!

Excellent post. I am going through some of these issues as well..

Excellent blog post. I certainly love this site. Thanks!

There are also many conditions with symptoms similar to appendicitis. But because appendicitis can become serious in a short amount of time, call your

very good post, i surely really like this excellent website, persist with it

You made some really good points there. I checked on the web for more info about the issue and found most individuals will go along with your views on this site.

I’m impressed, I must say. Genuinely rarely can i encounter a blog that’s both educative and entertaining, and without a doubt, you’ve hit the nail to the head. Your idea is outstanding; the pain is an issue that there are not enough individuals are speaking intelligently about. We are delighted that we stumbled across this inside my try to find some thing about it.

nice one, I thoroughly enjoyed reading your article. I really appreciate your wonderful know-how and the time you put into educating the rest of us.

Blumenthal, Paul. “Read the Bill: The Commodity Futures Modernization Act.” The Sunlight Foundation.

This is the right site for everyone who wants to find out about this topic. You realize a whole lot its almost hard to argue with you (not that I actually will need to…HaHa). You definitely put a new spin on a topic that’s been discussed for decades. Excellent stuff, just wonderful.

The very next time I read a blog, Hopefully it does not disappoint me just as much as this one. After all, Yes, it was my choice to read through, however I genuinely believed you’d have something interesting to say. All I hear is a bunch of crying about something you could fix if you weren’t too busy seeking attention.

Call centers are now all over the World..! they definitely bring revenue profits..!

This is a great tip particularly to those new to the blogosphere. Brief but very precise info… Many thanks for sharing this one. A must read post.

You produced some decent points there. I looked on the internet for that issue and located most individuals goes along with along with your internet site.

A venue booking calendar, complete booking administration including setup resources, catering, beverage, and staffing necessities, budgeting, invoicing, and all the pieces else it’s worthwhile to handle your venue bookings.

After I initially commented I seem to have clicked on the -Notify me when new comments are added- checkbox and from now on every time a comment is added I recieve four emails with the exact same comment. Perhaps there is an easy method you are able to remove me from that service? Cheers.

Craving a juicy steak?

Amazingly, your piece goes to the heart of the topic. Your clarity leaves me wanting to know more. Just so you know, i’ll immediately grab your feed to keep up currently with your online blog. Sounding Out thanks is merely my little way of claiming what a masterpiece for a fantastic resource. Take On my best wishes for your subsequent publish.

sometimes skinny jeans are not comfortable to wear, i would always prefer to use loos jeans,,

Great information. Lucky me I recently found your site by chance (stumbleupon). I have book-marked it for later.

This website was… how do you say it? Relevant!! Finally I have found something which helped me. Appreciate it.

Hi, I do think this is an excellent web site. I stumbledupon it 😉 I will revisit yet again since i have saved as a favorite it. Money and freedom is the best way to change, may you be rich and continue to guide others.

Universal Studios Fright Nights started as a 3-evening event held at Universal Studios Florida on October 25, 26, and 31, 1991, that includes one haunted house, The Dungeon of Terror, and a group of shows.

Way cool! Some extremely valid points! I appreciate you writing this post and the rest of the site is really good.

In addition to the damage that fires trigger as they burn, they can even leave behind disastrous problems, the consequences of which might not be felt for months after the fireplace burns out.

This web site certainly has all of the information I wanted concerning this subject and didn’t know who to ask.

There’s certainly a lot to learn about this subject. I love all the points you’ve made.

You need to take part in a contest for one of the greatest websites on the internet. I will recommend this blog!

After looking over a handful of the blog posts on your blog, I truly like your way of blogging. I book-marked it to my bookmark website list and will be checking back in the near future. Please visit my web site as well and tell me what you think.

It’s nearly impossible to find experienced people for this subject, however, you sound like you know what you’re talking about! Thanks

This is a topic which is near to my heart… Cheers! Where are your contact details though?

In 2005, Chhetri signed for JCT for the 2005-06 season.

Saved as a favorite, I really like your site.

Jones, K.C. “President Bush signs Internet Tax Freedom Act.” Info Week.

You’re so interesting! I don’t think I’ve read anything like that before. So good to find somebody with a few unique thoughts on this subject. Really.. thank you for starting this up. This site is one thing that is needed on the internet, someone with a bit of originality.

Good post! We will be linking to this great article on our website. Keep up the good writing.

Hello there, I believe your site could possibly be having browser compatibility issues. Whenever I look at your blog in Safari, it looks fine however when opening in Internet Explorer, it’s got some overlapping issues. I simply wanted to provide you with a quick heads up! Aside from that, wonderful site!

Hi there, There’s no doubt that your site could be having browser compatibility problems. When I look at your website in Safari, it looks fine however when opening in Internet Explorer, it’s got some overlapping issues. I simply wanted to give you a quick heads up! Besides that, excellent blog.

Of course, this number excludes any college costs (even savings set aside for college during the first 17 years), and as any parent who has raised a child beyond age 17 will tell you, it’s the next five years or so that are really the kickers.

I have to thank you for the efforts you’ve put in penning this blog. I am hoping to check out the same high-grade content from you later on as well. In fact, your creative writing abilities has motivated me to get my own site now 😉

You ought to take part in a contest for one of the best sites online. I most certainly will recommend this site!

This is the perfect site for anyone who really wants to understand this topic. You realize so much its almost tough to argue with you (not that I actually would want to…HaHa). You certainly put a brand new spin on a subject that has been written about for years. Excellent stuff, just excellent.

You possibly can have one of our fully lined and insulated Backyard Rooms to have your relaxation area with two inside partitions put in to create a personal changing room, and an exterior partition added to either the again or facet of the constructing, which can be utilized to store your generator and any chemicals required.

Good article. I certainly love this website. Continue the good work!

Bowers from Onaway, MI.

Spot on with this write-up, I absolutely think this web site needs far more attention. I’ll probably be back again to read more, thanks for the advice!

You have made some good points there. I checked on the internet to find out more about the issue and found most people will go along with your views on this website.

A motivating discussion is worth comment. There’s no doubt that that you need to publish more on this topic, it might not be a taboo subject but typically people do not speak about these topics. To the next! Kind regards.

Very nice article. I absolutely appreciate this site. Continue the good work!

I’d like to thank you for the efforts you have put in writing this website. I’m hoping to view the same high-grade content from you later on as well. In truth, your creative writing abilities has motivated me to get my own website now 😉

May I simply just say what a relief to uncover somebody who actually knows what they are discussing on the web. You definitely realize how to bring a problem to light and make it important. More and more people ought to check this out and understand this side of your story. It’s surprising you aren’t more popular because you most certainly have the gift.

bookmarked!!, I like your blog.

Greetings! Very helpful advice within this post! It’s the little changes that produce the biggest changes. Many thanks for sharing!

In late October 2023, it was reported that Disney was nearing a money and inventory deal with Reliance Industries for the sale of its operations in India, together with a controlling stake in Disney Star.

This website was… how do you say it? Relevant!! Finally I have found something that helped me. Many thanks.

Saved as a favorite, I like your site!

Having read this I thought it was really informative. I appreciate you taking the time and effort to put this information together. I once again find myself personally spending a lot of time both reading and leaving comments. But so what, it was still worth it.

Hi, I do believe this is an excellent site. I stumbledupon it 😉 I may come back yet again since I saved as a favorite it. Money and freedom is the best way to change, may you be rich and continue to guide other people.

Your style is really unique compared to other folks I’ve read stuff from. Many thanks for posting when you have the opportunity, Guess I will just bookmark this blog.

Hello there! This post could not be written any better! Looking at this post reminds me of my previous roommate! He continually kept talking about this. I will forward this article to him. Pretty sure he’s going to have a great read. Many thanks for sharing!

Faux means ‘fake’ and the fake fur rugs became a favorite piece of item in every home.

Excellent write-up. I absolutely appreciate this website. Stick with it!

Hi! I just would like to give you a big thumbs up for the excellent info you have got right here on this post. I’ll be returning to your blog for more soon.

I wanted to thank you for this excellent read!! I absolutely loved every little bit of it. I’ve got you book marked to look at new stuff you post…

The video games began at 15:00 local time (EKT), which was 09:00 UTC.

Aw, this was a really good post. Spending some time and actual effort to create a very good article… but what can I say… I hesitate a lot and never manage to get nearly anything done.

Total, customers find them to be a very good primary kitchen towel that brightens up their kitchens.

Excellent article! We will be linking to this particularly great article on our website. Keep up the good writing.

Good article. I am dealing with a few of these issues as well..

The Nationwide League is combining forces with The Royal British Legion over the forthcoming weeks to lift the consciousness of their annual Poppy Attraction and the way those financial contributions help the sterling work accomplished to support members of our armed forces who need care in our communities presently.

This is a topic that is near to my heart… Cheers! Where can I find the contact details for questions?

I needed to thank you for this great read!! I definitely loved every bit of it. I have you bookmarked to look at new things you post…

I blog frequently and I truly thank you for your information. Your article has really peaked my interest. I will bookmark your blog and keep checking for new information about once per week. I opted in for your Feed as well.

Oh my goodness! Incredible article dude! Thanks, However I am encountering difficulties with your RSS. I don’t understand why I cannot join it. Is there anybody else having the same RSS problems? Anyone that knows the solution can you kindly respond? Thanks!

Good article! We will be linking to this great article on our site. Keep up the good writing.

Four 30.Nb3, with the knight able to win back the d-pawn.

Also, know that many professional trading firms prefer training and hiring people with limited market experience because new traders have less market “baggage” or preconceptions of what they should do versus what is actually the right way to trade.

What different identify did it go by and who made it?

In fact, Tesla can be identified for bucking the standard dealership mannequin, so the corporate would not need to worry about indignant supplier franchisees — if vehicles need not are available in for recalls, there’s less alternative to upsell and get income, some sellers say.

This blog was… how do you say it? Relevant!! Finally I’ve found something which helped me. Thanks!

Handbook pole sanders offer a low-cost answer, however the same old drawback (other than the bodily effort required) is that drywall mud will get everywhere.

No agency can think of its growth without understanding the numbers which never lie.

For someone who is new in the trading business looking to profit with options, it is always a good start to take time to do some research in line with the useful technical indicators.

Hi there! This blog post could not be written much better! Looking at this article reminds me of my previous roommate! He continually kept preaching about this. I am going to forward this article to him. Fairly certain he will have a very good read. I appreciate you for sharing!

A flood of print and Tv advertising insured that almost everyone in America knew the “unexpected” Mustang had arrived.

Your Wikipedia account will robotically work on Commons too.

Used as adjectives, Certified Financial Planner and CFP颅颅颅 identify one of the more than 54,500 people across the United States who has been certified by the Certified Financial Planner Board of Standards.

Berg, Jeremy M. “Chapter 32: Sensory Systems.” Biochemistry.

Business Commonplace India. Enterprise Customary.

I quite like looking through a post that will make people think. Also, thank you for allowing for me to comment.

For 1987, production was somewhat less limited: a total of 6052.

And never only are they inside walking distance if you live on campus, but the price is also included in pupil tuition.

The method depends on the parties concerned discussing the issue within the presence of a mediator.

A mobile house was destroyed, another cell dwelling was damaged by falling bushes, and a house had shingles ripped off alongside this section of the trail as nicely, and harm to these buildings was rated EF1.

Hi, I do believe this is a great blog. I stumbledupon it 😉 I am going to come back once again since I book-marked it. Money and freedom is the greatest way to change, may you be rich and continue to help others.

You’ve probably seen so many disastrous bridesmaid dresses in movies that they’re a clich茅.

After looking at a few of the blog posts on your web site, I honestly appreciate your way of blogging. I saved as a favorite it to my bookmark site list and will be checking back in the near future. Take a look at my web site too and tell me how you feel.

These soaps have been formulated for the delicate pores and skin on your face and will comprise acne-combating components.

Every Indian woman loves to adorn her wrists with beautifully designed bangles.

People have become increasingly conscious of the benefits of owning a home because it is the safest place to be.

Given the truth that San Francisco airport is the most important airport within the bay area of San Francisco and the second busiest airport of California, it’s but obvious that the carbon prints of SFO are way more and they have had to take rapid motion to reconcile the detrimental effects of gases on environment.

That’s one in every of the explanations the workforce has gained 27 World Sequence, greater than another franchise.

Oh my goodness! Incredible article dude! Many thanks, However I am having troubles with your RSS. I don’t understand the reason why I can’t subscribe to it. Is there anyone else getting identical RSS issues? Anyone who knows the solution will you kindly respond? Thanx!!

It’s claimed to advertise monetary growth and open doorways for professional and company success.

The online resource seeks to help individuals discover Jesus in the pages of Scripture, to live lives that glorify God, and to communicate their religion effectively, together with a spread of supplies to introduce Christ to these who are unfamiliar with his message, reaching those that do not yet imagine, training believers in sharing their faith and strengthening the boldness of church leaders in the Bible.

The Chattanooga Rugby Football Membership, which was established in 1978 and the 2011 and 2013 DII Mid South champions, is affiliated with USA Rugby and USA Rugby South.

J.J. Mantell and George Orcutt, along with Falconer, famous that they targeted on adoption of a plan (not the proposed depression plan, just a plan).

Passive photo voltaic residence design merely makes use of the solar’s rays to heat a house by way of strategic placement of windows in a house.

You made some really good points there. I looked on the web to learn more about the issue and found most individuals will go along with your views on this site.

Nonetheless, the equilibrium idea of phase transformations doesn’t hold for glass, and hence the glass transition cannot be classed as one of the classical equilibrium phase transformations in solids.

Wheeler Park, subsequent to metropolis corridor, is the location of summer concert events and other occasions.

Do not use television as your alternate activity.

You’re so cool! I do not suppose I’ve truly read anything like that before. So nice to discover another person with unique thoughts on this subject. Seriously.. thank you for starting this up. This web site is one thing that is required on the web, someone with some originality.

William Shakespeare’s Hamlet proclaimed, “What a bit of work is a man, how noble in purpose, how infinite in colleges, in kind and transferring how specific and admirable, in motion how like an angel, in apprehension how like a god!” Hamlet’s point was that humans are a exceptional species — though Hamlet himself has lost all appreciation for mankind.

“Funeral services were held Wednesday, Aug 14, for Emma Martha Howell from the Group Presbyterian Church in Wilbur.

I love it when people come together and share views. Great site, continue the good work!

Great post. I’m experiencing a few of these issues as well..

Excellent article! We will be linking to this great content on our website. Keep up the good writing.

Another project of the Vanderbilt household, The Breakers in Rhode Island measures 62,482 square toes.

You can see your real surroundings at all times, but you can also call up information via voice commands, and it will appear on the screen, superimposed over what’s really in front of you.

Once you understand your financial position you possibly can resolve what you wish to put money into.

Yet many of these systems are probably derived from what’s called “data mining” through back testing.

I was excited to discover this website. I want to to thank you for ones time due to this fantastic read!! I definitely liked every bit of it and i also have you book-marked to check out new stuff on your website.

May I simply just say what a relief to uncover someone that actually knows what they are discussing on the net. You definitely know how to bring a problem to light and make it important. More and more people need to check this out and understand this side of the story. I can’t believe you are not more popular since you surely have the gift.

I could not resist commenting. Well written.

On November 16, the city of Philadelphia introduced new restrictions resulting from a surge in circumstances, which had been in place from November 20 till January 1, 2021.

The parts of the structure that form quickly will probably be protected and thus not exchanged, whereas areas that fold late in the pathway can be exposed to the alternate for longer durations of time.

Along with being a nursing dwelling, this facility offers assisted dwelling care and has an independent living option.

Everything is very open with a precise explanation of the challenges. It was definitely informative. Your site is extremely helpful. Thank you for sharing!

Renovation involves a complete redesign of bathroom ground plans.

While the fee for each photo is relatively small, photographers who can upload an entire catalog of stock photos can realize a good residual income, month after month.

An individual that falls into the 28 tax bracket would find, using the previous formula, that the tax-free bond’s tax-equivalent yield of 3.47 is more than the taxable bond’s yield, making it a better decision to buy into the tax-free fund.

Can I just say what a relief to discover someone that really understands what they are talking about over the internet. You definitely understand how to bring a problem to light and make it important. More and more people ought to check this out and understand this side of the story. It’s surprising you are not more popular given that you most certainly have the gift.

In recent years, there has been a stimulating growth within the stock commerce and, therefore a lot of and a lot of numbers of investor’s are heading towards stock markets to do their luck and earn some handsome profits and financial gain.

James. Hinting at what might lie ahead was a tantalizing “concept” attraction for that season’s auto-show circuit: the Mustang IMSA.

If you’re married, but you and your partner file separate individual tax returns, you would pay taxes on up to eighty five of your Social Security advantages no matter income ranges.

If the intention of the assembly is to discuss sales figures, you will seemingly want to make sure the sales workforce, sales director, advertising supervisor and perhaps even finance group are all available.

2008’s Reflections of Concern featured a brand new icon within the type of Dr.

Rosenfeld and Morville are authors of a book titled “Information Architecture for the World Wide Web.” The cover of the book, like other O’Reilly publications, features a drawing of an animal.

Mutual fund schemes are rated by credit rating agencies or by experts in mutual funds field.

After the American Revolution and the institution of the brand new Jersey state government, Bordentown was integrated with a borough government kind by an act of its legislature on December 9, 1825, from parts inside Chesterfield Township.

Softer fabric can look even higher though if it is properly stretched.

Use a few candleholders to get more selection.

Embrace edgy clothing, unconventional vogue, indie vogue, avant-garde outfits, and non-traditional kinds to create a contemporary fashion assertion.

Since many employers will not recruit additional workers until they are sufficiently sure that there is a long-term demand for new hiring, unemployment frequently stays strong even though the economy starts to recover and it is equalized by the end of recovery phase.

Some are being recruited by manufacturing companies which have aggressively raised wages to fill shortages.

Thick coats of varnish take longer to dry, and so they are inclined to crack because the varnish ages.

Most of the people have seen the actual and real worth of their income crash drastically over the years, and there arises uncertainty in the rest of their lives.

One other is the applicability of the particular program.

Have you ever patted your participant on the again right this moment?

Matching grants have distortionary effect, which suggests that same utility stage as provide these grants may be attained at decrease value with block grants.

Shaadi Baraati has the most effective wedding decorator and planners within the record.

The NAU coaching camp was named as certainly one of the highest five training camps in the NFL by Sports activities Illustrated, citing the cooler temperature, scenic space, and the likelihood for followers to get close to athletes as key factors.

At first glance, the iPad looks like an iPhone or iPod touch on steroids.

Due to the large amounts of ticks in a single day, high frequency data collections generally contain a large amount of data, allowing high statistical precision.

Really, most top earners receive the majority of their take-dwelling pay from stock options.

Brian Flynn has supplied the recorded commentary from Tuesday’s sport against FC Halifax Town, together with a half-time interview with Heather Scott (captain) & Keith Edleston (supervisor) of Altrincham FC Ladies.

Jill Vejnoska (April 26, 2008).

This meant that much of the produce was grown by the Institute for those who lived at the institute, together with potatoes, oatmeal, roots and green vegetables.

watch our super hit sexy bf video right now. Watch sexy bf video

Based on the API definition, unless an exception applies, most carried pursuits (profits interests) held by service partners working for private fairness (“PE”) sponsors, enterprise capital funds, hedge funds and real property funds, fall inside the API definition.

To get the ball rolling, he employed a well known artist, I. B. Hazelton, to do a series of 24 paintings depicting the jeep in a variety of settings.

And beverages embody juices, espresso, and tea but in addition typically feature a number of alcoholic beverages, comparable to mimosas, Bloody Mary’s, sparkling wine, or champagne.

A risk profiling exercise is a must-do before starting to invest.

An impressive share! I’ve just forwarded this onto a friend who had been doing a little homework on this. And he actually bought me breakfast due to the fact that I stumbled upon it for him… lol. So allow me to reword this…. Thank YOU for the meal!! But yeah, thanks for spending the time to talk about this subject here on your web page.

PPF and FD are additionally safest since they are supported by the Central government.

4. You may as well use this worksheet so as to add extra payments to debt each month.

Good blog you have here.. It’s hard to find high-quality writing like yours nowadays. I truly appreciate people like you! Take care!!

White opts for the initiative on the queenside with a smaller pawn centre.

However there are methods you’ll be able to continue to use these handy appliances while still taking good care of the earth.

Many pointed to suspicious hiring practices as a source of the problem, saying patronage – not merit – decided who got jobs there.

It means whenever the company makes a profit, you too participate in the company’s profits.

It is much easier to home practice a French bulldog puppy if he/she sleeps in a crate.

However what many people don’t often think of when talking about Canada are the nice television exhibits that we now have here!

Sporting leather gloves is one of the best ways to prevent harm to 1’s fingers when eradicating overseas objects from a tire.

Good post. I learn something new and challenging on sites I stumbleupon on a daily basis. It will always be helpful to read through content from other authors and practice something from other sites.

Whitehouse, David. “Before the large Bang.” BBC Information.

I could not resist commenting. Very well written!

The very next time I read a blog, Hopefully it won’t fail me as much as this one. After all, Yes, it was my choice to read, but I really thought you’d have something interesting to talk about. All I hear is a bunch of moaning about something you could possibly fix if you were not too busy seeking attention.

Great article! I learned a lot from your detailed explanation. Looking forward to more informative content like this!

Paint helps slow the breakdown of the metals in the car.

Excellent web site you’ve got here.. It’s hard to find high-quality writing like yours nowadays. I truly appreciate individuals like you! Take care!!

After I originally left a comment I seem to have clicked the -Notify me when new comments are added- checkbox and from now on whenever a comment is added I recieve four emails with the exact same comment. Is there an easy method you can remove me from that service? Thanks a lot.

You’re so interesting! I do not suppose I’ve read through anything like this before. So nice to discover someone with some genuine thoughts on this topic. Really.. thank you for starting this up. This site is one thing that’s needed on the internet, someone with a bit of originality.

Hi, I do believe this is a great blog. I stumbledupon it 😉 I may come back once again since I book-marked it. Money and freedom is the best way to change, may you be rich and continue to help others.

Very good info. Lucky me I recently found your site by accident (stumbleupon). I have bookmarked it for later.

When I originally left a comment I seem to have clicked the -Notify me when new comments are added- checkbox and from now on each time a comment is added I recieve four emails with the exact same comment. Is there a way you are able to remove me from that service? Appreciate it.

I could not refrain from commenting. Very well written.

With its spectacular towing capacity and unique features, the GMC Yukon is a prime contender within the SUV towing market.

I love reading an article that can make men and women think. Also, many thanks for allowing me to comment.

It is because of this reason that theonline enterprise is flourishing over the time thus creating a extremely worthwhile internet.

Many processed foods aren’t gluten-free foods.

There are a lot of extra country decorating ideas for your private home.

Excellent blog post. I absolutely appreciate this website. Stick with it!

COS offers a range of contemporary workwear.

Step Twelve: Stencil the flowers Blue Bonnet with a 1/4-inch brush; repeat.

Both also protected their drug trafficking operations by entrenching themselves in the federal government.

Watch our most viewed super sexy bf video on socksnews.in. sexy bf video Watch now.

You are so awesome! I don’t suppose I have read through something like that before. So wonderful to discover someone with a few original thoughts on this subject matter. Seriously.. thanks for starting this up. This site is one thing that’s needed on the internet, someone with a bit of originality.

This is quite a challenging query, as the interviewer might counter-question your answers, and attempt to examine how properly ready you might be to cope up with the stress that will observe the duty.

Great article! I learned a lot from your detailed explanation. Looking forward to more informative content like this!

With the word and Character erase, I can swiftly get rid of typos or unwanted words, maintaining my paperwork clean and polished.

It is really important to create a stability sheet for your organization and there are various advantages associated with it.

Funeral companies will probably be Saturday, May 27 at 2 p.m.

Why is soy wax higher?

Others form a partnership with purchasers, researching how their clients do enterprise in an effort to offer a complete, tailor-made service.

Roderick Alfred Matthews, Director, Telecommunications Providers; recently Director Data Expertise Services, ICL.

They handle the financial modelling so you can concentrate on making wise business decisions.

There’s certainly a great deal to learn about this issue. I love all the points you’ve made.

Teaching first grade introduced me in touch with inventive and inspirational six year olds on a daily basis.

It’s hard to come by well-informed people about this topic, but you seem like you know what you’re talking about! Thanks

You made some decent points there. I checked on the internet for additional information about the issue and found most individuals will go along with your views on this web site.

Spot on with this write-up, I absolutely believe that this website needs a lot more attention. I’ll probably be back again to see more, thanks for the advice.

This post is very helpful! I appreciate the effort you put into making it clear and easy to understand. Thanks for sharing!

It’s hard to find educated people on this subject, but you sound like you know what you’re talking about! Thanks

I couldn’t refrain from commenting. Perfectly written!

https://PostHereAds.com/586/posts/3/27/2200143.html

sex nhật hiếp dâm trẻ em ấu dâm buôn bán vũ khí ma túy bán súng sextoy chơi đĩ sex bạo lực sex học đường tội phạm tình dục chơi les đĩ đực người mẫu bán dâm

Pretty! This has been an extremely wonderful article. Many thanks for providing these details.

Nice read!

Great blog you have here.. It’s difficult to find excellent writing like yours these days. I truly appreciate individuals like you! Take care!!

Hi! I simply would like to give you a big thumbs up for the excellent information you have right here on this post. I am coming back to your website for more soon.

Nice post. I learn something totally new and challenging on websites I stumbleupon every day. It’s always helpful to read content from other writers and practice a little something from their websites.

Nice post. I learn something new and challenging on blogs I stumbleupon every day. It’s always interesting to read content from other authors and use a little something from other sites.

Howdy! This article couldn’t be written any better! Looking at this article reminds me of my previous roommate! He continually kept talking about this. I am going to forward this information to him. Fairly certain he’ll have a very good read. I appreciate you for sharing!

Aw, this was a very nice post. Spending some time and actual effort to make a superb article… but what can I say… I put things off a lot and don’t seem to get nearly anything done.

With provide chain administration options, you possibly can simply retailer, capture and packed essential knowledge in an environment friendly manner which these teams could seek.

For example, let’s say that you’ve purchased a bond for $1000, the curiosity is 6 and the date that you’ll get the cash back is after 5 years.

Great information. Lucky me I recently found your blog by accident (stumbleupon). I have bookmarked it for later!

When I originally commented I appear to have clicked on the -Notify me when new comments are added- checkbox and now every time a comment is added I recieve 4 emails with the exact same comment. There has to be an easy method you are able to remove me from that service? Thank you.

sex nhật hiếp dâm trẻ em ấu dâm buôn bán vũ khí ma túy bán súng sextoy chơi đĩ sex bạo lực sex học đường tội phạm tình dục chơi les đĩ đực người mẫu bán dâm