Real GDP Up Modestly On Investment

Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real-time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

Today, we offer some updates to our estimates for real GDP for April 2023. Summarily, real GDP is looking up modestly, with the pressures on investment spending ameliorating and consumption showing potential to come in positive despite weakness in real sales.

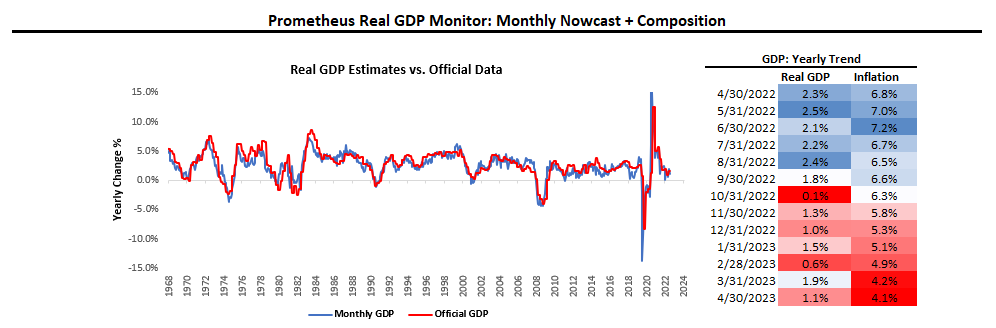

We start by showing our monthly tracking of real GDP, along with sequential changes in yearly real GDP & inflation:

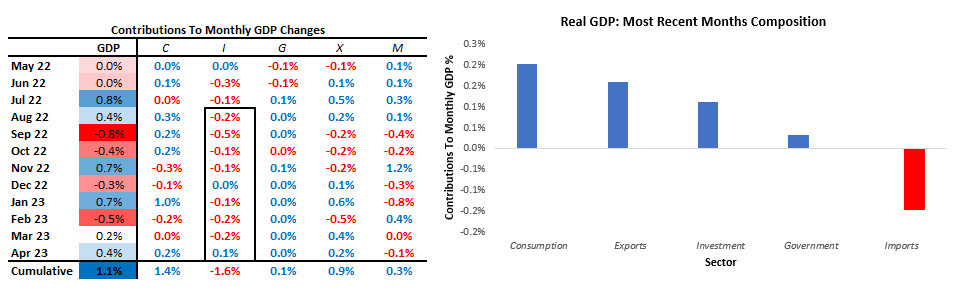

For the latest data through April, our systems place Real GDP growth at 1.07% versus one year prior. Above, we show our monthly estimates of Real GDP relative to the official data. Additionally, we show the composition of these estimates on a monthly change basis below:

Zooming in, we show the most recent estimates of these GDP drivers. In April, GDP came in at 0.36% versus the prior month. Additionally, we show the contribution by sector to monthly GDP in the table below:

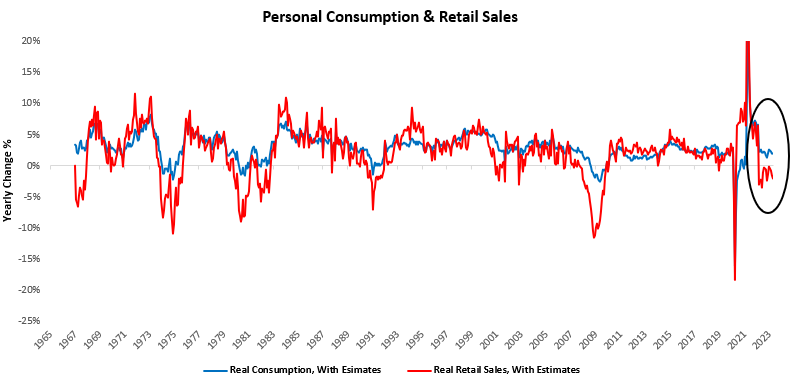

As we can see above, the major change thus far in April’s data relative to months prior has been the increase in consumption and investment estimates. While yesterday’s retail sales data indicates a drag on consumption, along with weakness in real income growth, our analysis tells us that this drag may not be adequate in size to pull down consumption spending. Below, we show how despite real retail sales being down for serval months, consumption remains positive:

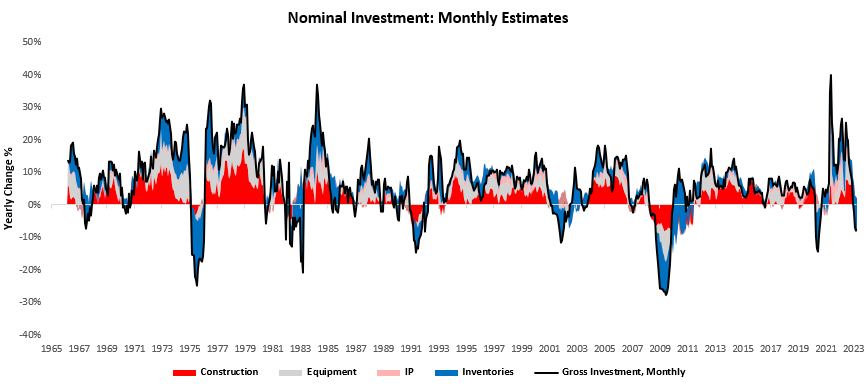

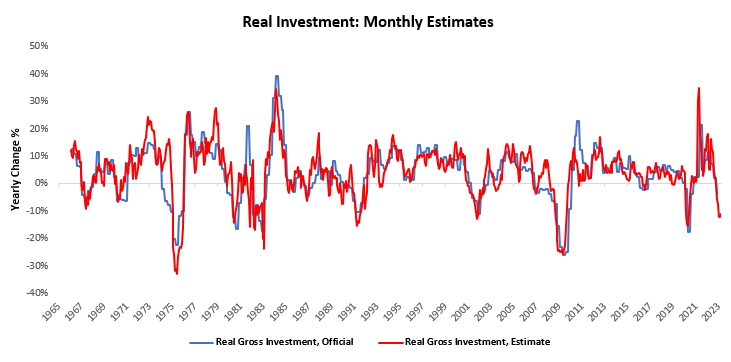

Additionally, while our estimates for construction remain negative this far for April, the improvement in manufacturing we have seen (led by autos) has significantly added to our estimates of investment spending this month. Nonetheless, the nominal investment trend remains weak:

And the real investment trend as well:

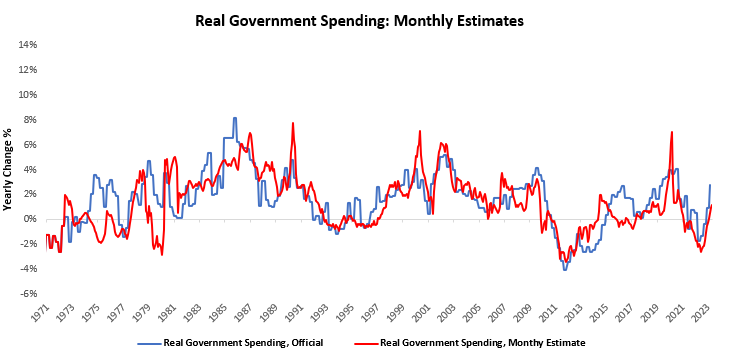

Additionally, we currently see government spending as supportive of GDP. However, with debt ceiling pressures continuing, we think it is important to remember that this tailwind to GDP could soon become a headwind. In April, real government expenditures added 0.03% to the 0.36% change in real GDP. Over the last year, government spending has added 0.15% to GDP growth of 1.07%.

As we can see above, this could impose a marginal drag on GDP, depending on how much the Treasury would have to pull back spending if debt ceiling issues aren’t resolved.

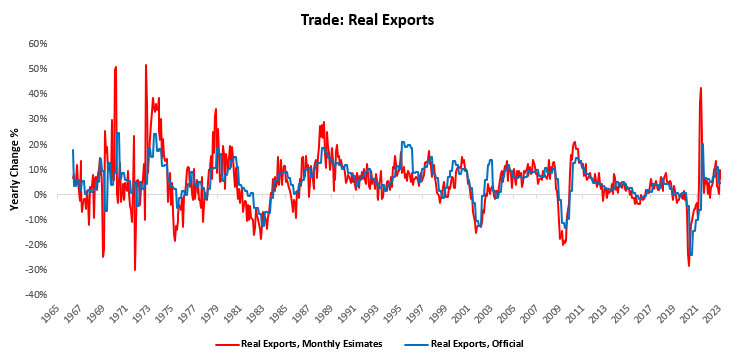

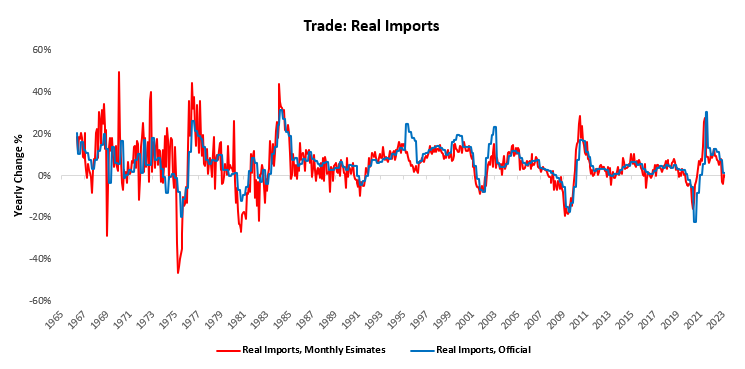

Finally, exports and imports real exports revenues added 0.16% to GDP growth, while real import expenditures took away -0.15%. We show import and export contributions, respectively, starting with exports:

We show imports below:

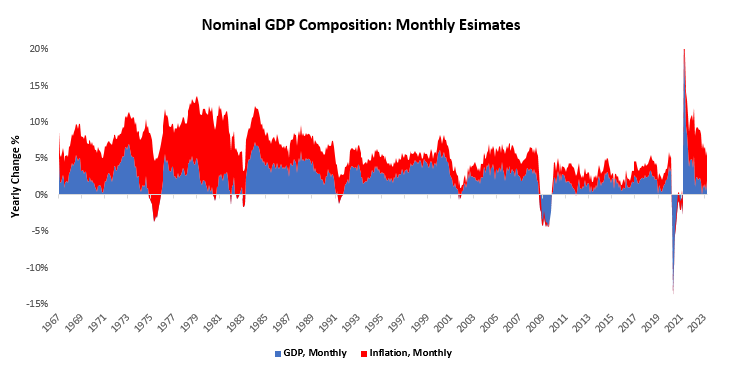

Overall, real economic growth looks modest, and nominal GDP continues to slow. We show the composition of monthly nominal GDP estimates, broken into real GDP growth and inflation. Our latest estimates place nominal GDP at 5.12% versus one year prior:

The latest data tells a story of modest real GDP growth, supported by services spending and a counter-trend increase in business investment. However, we think it is important to keep the big-picture in mind. Nominal GDP continues to slow, employee compensation remains steady, and debt service burdens are under pressure to rise. The combination of these factors will likely keep pushing nominal and real GDP lower over coming quarters. Until next time.

Hello! Do you know if they make any plugins to help with Search Engine Optimization? I’m trying to get

my site to rank for some targeted keywords but I’m not seeing

very good success. If you know of any please share.

Cheers! I saw similar art here: Blankets

Hello! Do you know if they make any plugins to help with SEO?

I’m trying to get my website to rank for some targeted keywords but I’m not seeing very good gains.

If you know of any please share. Thanks! I saw similar article here: Code of destiny

I am extremely impressed along with your writing skills and

also with the structure for your weblog. Is this a

paid subject matter or did you modify it your self?

Anyway keep up the nice high quality writing, it’s uncommon to see

a nice weblog like this one nowadays. Tools For Creators!

I’m extremely inspired together with your writing skills as neatly as with the format to your

blog. Is that this a paid topic or did you modify it

yourself? Either way keep up the nice quality writing, it’s rare to see a nice weblog like this one today.

TikTok ManyChat!

I’m really inspired along with your writing skills and also with the layout for your weblog. Is that this a paid theme or did you customize it your self? Anyway keep up the nice high quality writing, it’s rare to look a great blog like this one today. I like prometheus-research.com ! I made: Beacons AI

I am really inspired along with your writing talents

as neatly as with the structure for your blog.

Is that this a paid subject or did you modify it yourself?

Anyway keep up the nice quality writing, it’s uncommon to see a great blog like this one these days.

Snipfeed!

Your article helped me a lot, is there any more related content? Thanks! https://accounts.binance.com/zh-CN/register?ref=VDVEQ78S