Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real-time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

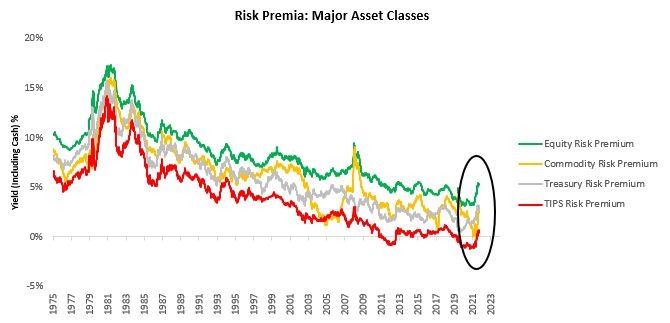

i. The Fed remains on the path to an aggressive tightening of financial conditions, sending expected returns higher. Expected returns are a function of the interest rate available on cash, plus a risk premium specific to each asset. Currently, expected returns are being propelled higher by monetary policy (interest rate hikes + QT). We show our gauges of these expected returns below:

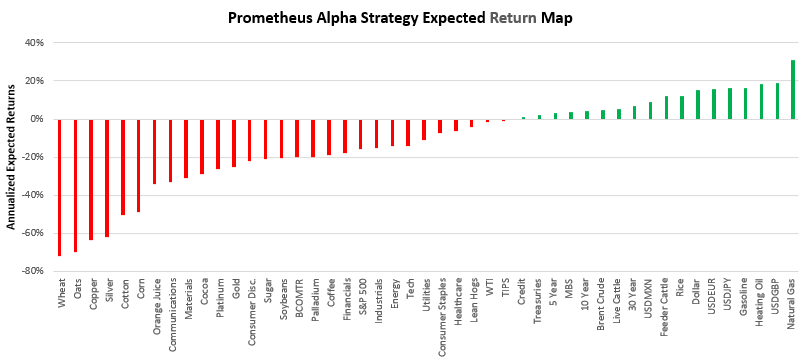

Expected returns potentiate future returns; however, they do not catalyze them. Our regime-expected returns account for the market environment and are a much better pro-cyclical gauge of the returns we can expect in a given environment. We show this below:

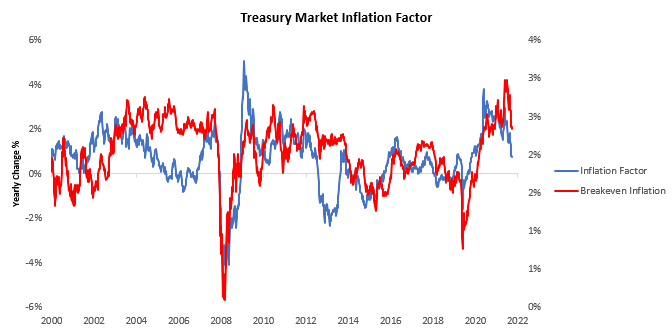

Our regime-expected return gauges take into account both current and historical dynamics to asses potential returns on an asset in a given environment. As we can see above, most asset classes are likely to perform poorly in the current regime. This dynamic will only reverse when the Fed changes its monetary policy stance. However, the tide looks to be turning for Treasuries, mainly on the back of a slowing inflation impulse. We show how our treasury market inflation factor, which measures the pricing of inflation within the treasury market, has declined significantly:

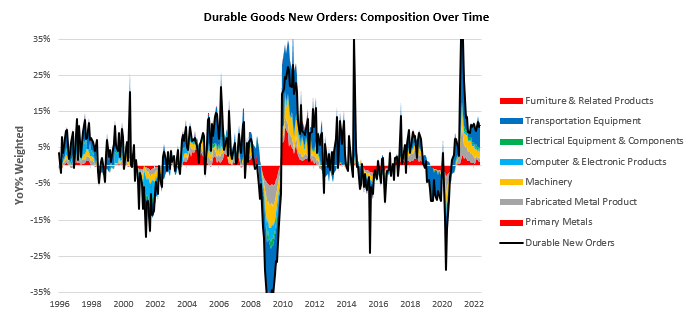

ii. Durable good new orders data showed sustained nominal demand. New Orders for Durable Goods came in at 10.9%, a sequential acceleration from the last print. This print surprised expectations with a monthly change of 1.9% versus expectations of -0.4%. We show the composition of this print below:

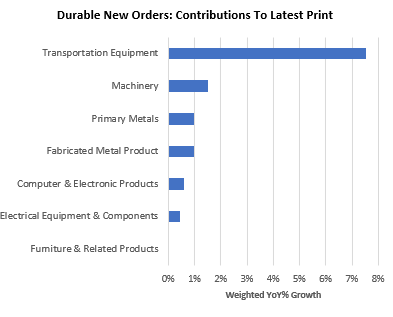

Transportation Equipment has been the most significant contributor to these moves, with a weighted year-over-year growth of 7.6%. We show this below:

Remember, inventory build is less penalized during inflationary periods, and we are seeing acute inflationary pressures in the transportation sector. Consumer demand for transportation and vehicles has not confirmed this data. Over the last year, Durable Goods New Orders have been in a downtrend though the latest print breaks this trend. We show the trend in the data below:

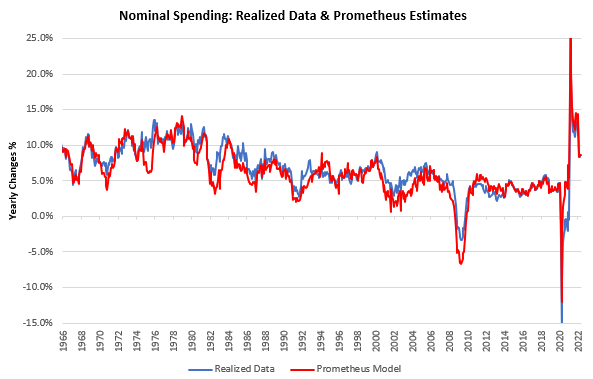

iii. Nominal Personal consumption expenditures are likely to accelerate tomorrow. Our systematic tracking of economic factors leads our systems to believe that nominal spending will remain stable this week. However, we continue to be in a decelerating trend. We show our model versus realized personal consumption data below:

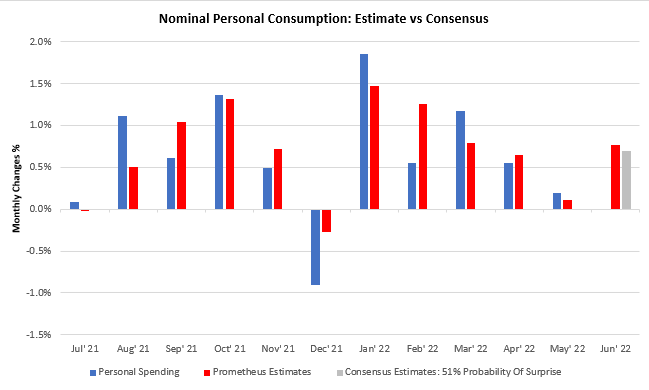

We also show the recent sequential forecasts relative to realized data:

Consensus expectations on personal spending tend to be quite accurate, and our models are roughly in line with these expectations. Therefore, we do not expect a significant surprise here.

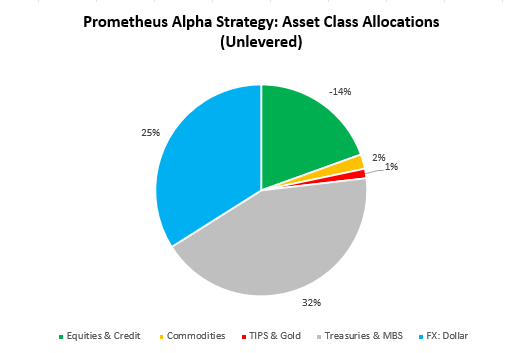

Our systems consider the principles underlying our economic and market analysis to create rules-based portfolios. Our portfolios have recently shifted towards Treasuries on the back of slowing inflation and deteriorating growth. They continue to remain long the dollar, short equities & credit. We show our asset class positioning below:

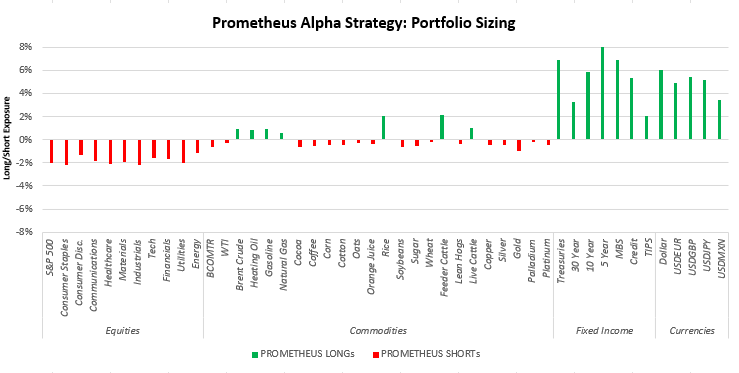

We show our security-level positioning as well:

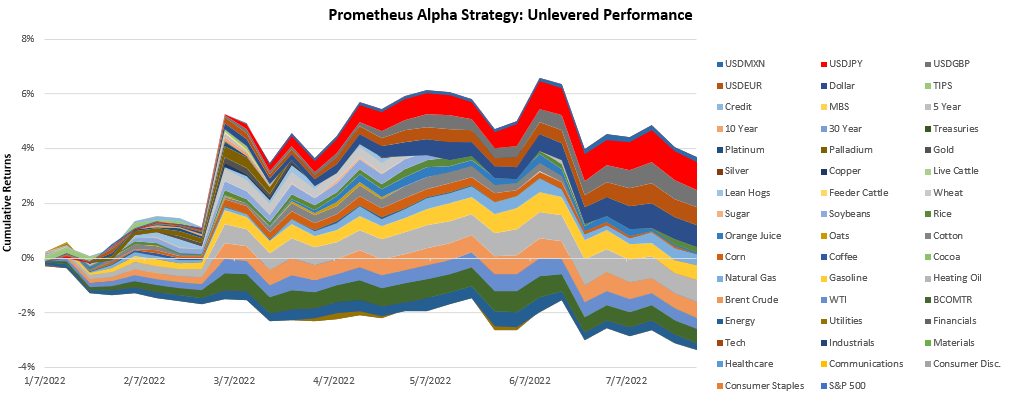

Finally, we show the year-to-date performance of the Alpha Strategy:

Markets are now turning to price growth slowdown dynamics relative to inflation surprises; shorting gets harder here, but Treasury beta likely gets easier. Stay nimble.