Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of both the economy and financial markets in real-time. Here are the top developments that stand out to us:

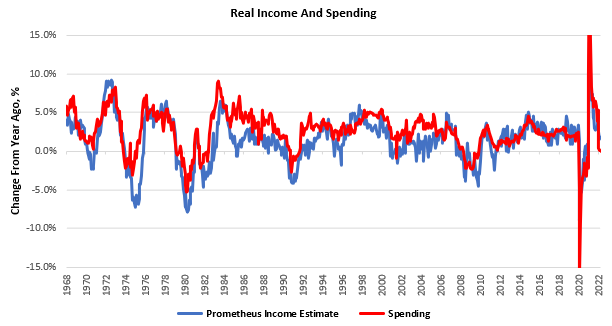

i. Personal income data showed households increased their savings in May, bringing down personal spending. Income and spending are two sides of the same coin, with one person’s spending powering another person’s income. However, this relationship between income and spending isn’t necessarily 1:1, as consumers can save income to purchase financial or invest in tangible assets. Nonetheless, the pass-through from income to spending is typically very high, and we show our tracking of income versus spending below:

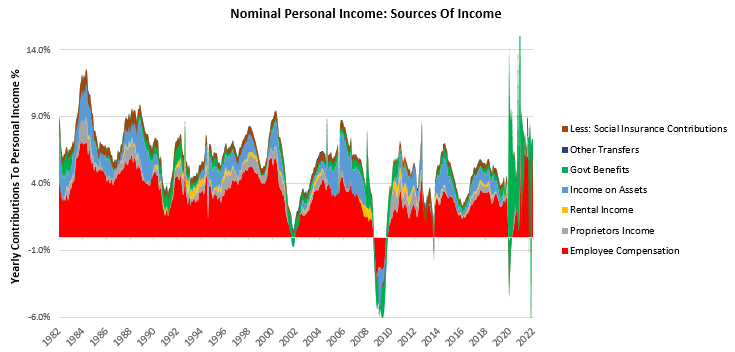

Currently, aggregate income remains supported by a high level of nominal wages and heightened employment. We see this in today’s economic data, where nominal personal income grew primarily as a function of increasing employee compensation:

Most recently, employee compensation accounted for 51% of monthly income growth, which remains in line with its one-year trend. On an annual basis, employee compensation continues to power nominal income growth, and the drop-off in government benefits continues to drag on growth:

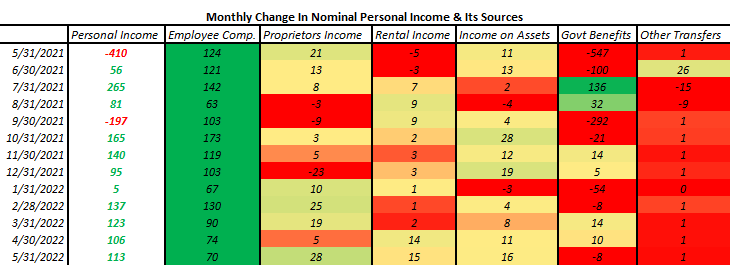

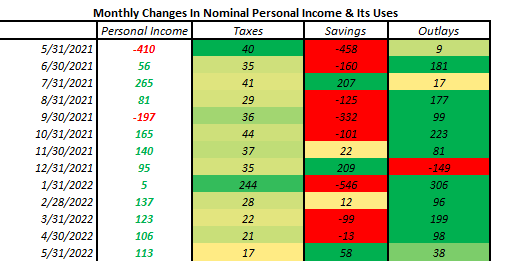

However, these marginal increases in income were not allocated to spending but rather saved. We show the composition of the monthly change in income and its uses:

In May, 51% of income increases were saved by consumers, effectively canceling out the growth in employee compensation. This increased savings doesn’t mean these funds are necessarily allocated to cash but may go towards other assets. Nonetheless, the impact of these increased savings was a decline in monthly outlays, i.e., a drag on personal spending.

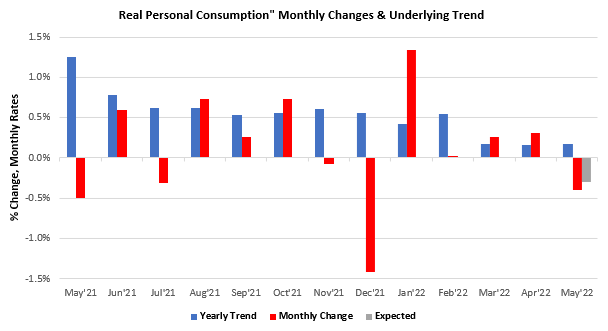

ii. Real personal consumption expenditures declined in May, with 60% of sub-categories turning lower. Real Personal Consumption came in at 2.06% versus the prior year, a sequential acceleration from the last print. Over the last year, Real Consumption has been in a downtrend though the latest print breaks this trend. This sequential acceleration was due to the drop-off of last May’s data, which showed a decline of -0.5%. We offer the monthly trend in personal consumption below:

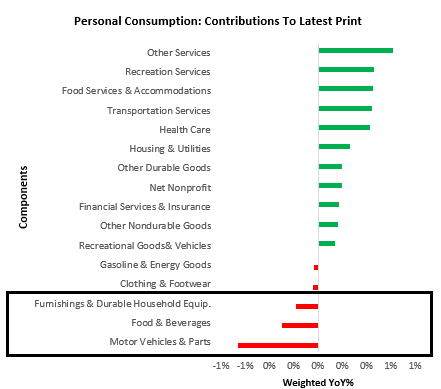

This print disappointed expectations with a monthly change of -0.4% versus expectations of -0.3%. Motor Vehicles & Parts has been the most significant driver of these moves with a weighted year-over-year growth of -8.3%. Below, we show the composition of yearly changes in real personal spending:

We highlight above those areas of spending typically the most pro-cyclical, i.e., motor vehicle and durable household goods spending, dragging aggregate expenditure. These areas of the economy tend to be highly responsive to the business cycle, i.e., they swing ahead of major inflections in the business cycle. Overall, personal income remains supported by employment and high nominal wages- but cyclically sensitive areas of the economy are beginning to show weakness.

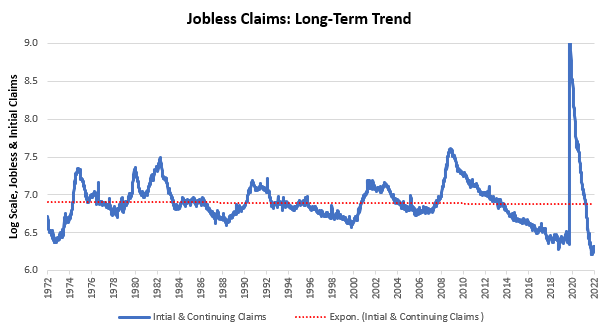

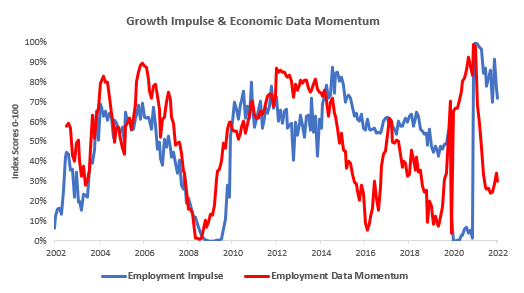

iii. Unemployment remains below its long-term trend; however, the data consistently disappoint expectations. As we can see below, the labor market remains extremely tight:

As described previously, this is the current source of strong consumer incomes. However, this has a built-in self-limiting factor: tight labor markets mean there is very little room for employment and income to expand. Additionally, labor market data continues to disappoint expectations. Below, we show the rate of change of our labor market aggregate versus the degree of economic data surprise (economic momentum):

At this stage of the economic cycle, labor markets will decreasingly be a source of incremental income gains. Employment is always the last shoe to drop in the economic process, and by the time employment bottoms, the economic recovery is usually underway. Our systems were designed with these principles in mind and continue to guide the way through these turbulent times.

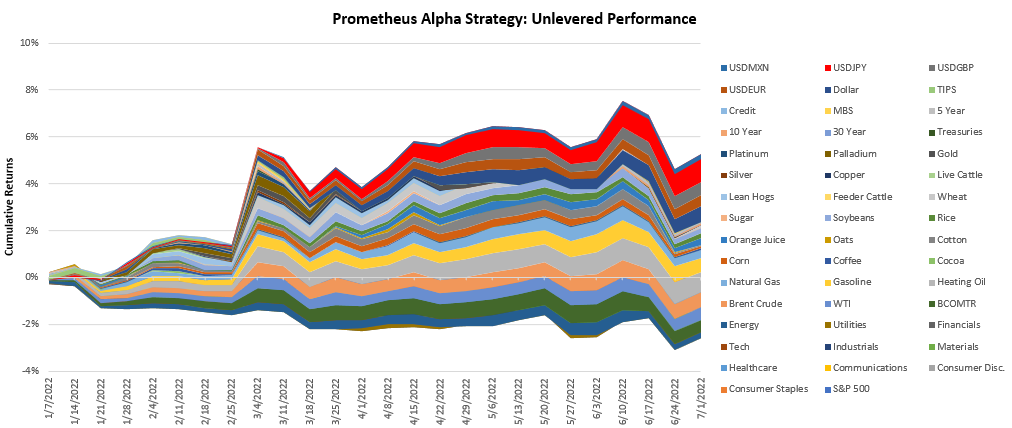

Given these late-cycle dynamics, our Alpha Strategy remains short equities, credit, and fixed income. Week-to-date, this positioning has fared well, with our Alpha Strategy running net-short at the portfolio level across asset classes. We show the cumulative year-to-date performance attribution below:

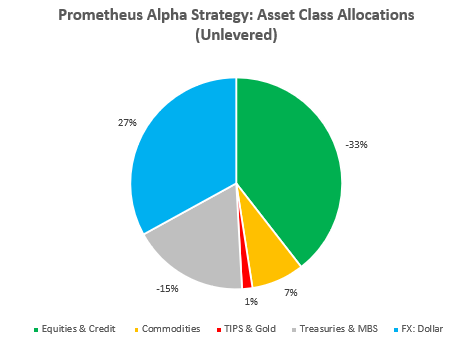

We show the unlevered asset class exposure of the Alpha Strategy below:

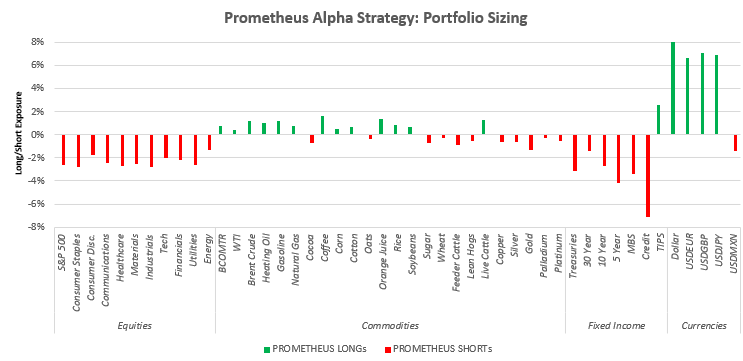

Finally, we offer the security-wise positions of the portfolio below:

Remember, we are in an environment of tightening liquidity, i.e., the dry powder available to fund assets and risk is being depleted. During these times, all asset markets suffer. These periods tend to be short but extremely painful, and managing drawdowns on your portfolio is what matters. Protect your capital so that you have the opportunity to buy assets when the tide turns. Stay nimble.