Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

If you haven’t already, check out Episode 3 of the Prometheus Podcast! For this episode, we have a formidable guest- Mr. Blonde. Mr. Blonde is an independent macro strategist who chooses to remain anonymous. With significant experience on both the buy-side & sell-side- his equity-centric research is timely, precise, and pragmatic. This year, he’s done an excellent job expecting the bear market in stocks & the ensuing bear market rally. In a wide-ranging discussion, our Founder, Aahan Menon, helps Mr. Blonde take you through a masterclass in macro-equity investing. This episode is a must-listen for anyone investing or trading equities actively. Enjoy!

Below are the top observations coming from our systematic tracking of economic conditions:

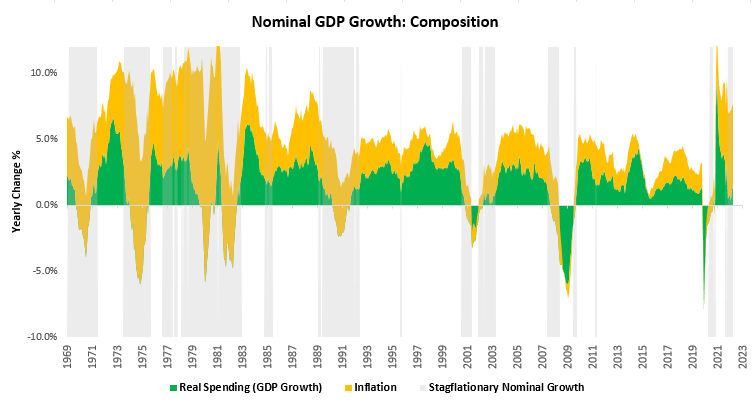

i. Real incomes remain weak, while production remains elevated. The latest estimates of our GDP Nowcast place real GDP growth at 1.6% versus a year ago. This real GDP growth is a relatively small portion of nominal GDP growth, i.e., we continue to be in a stagflationary nominal growth environment. Below, we show our estimates of the current composition of nominal GDP growth:

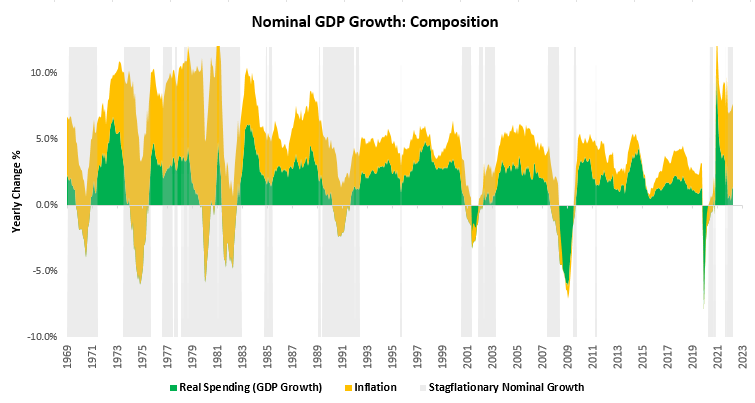

Additionally, we highlight the above periods that resemble today’s nominal growth profile of stagflationary nominal growth. As can be seen above, these periods tend to be periods of declining nominal and real growth. This is primarily a function of the fact that inflationary spending cannot sustain itself, unlike real growth. Furthermore, excessive levels of inflation are corrosive to real growth. Below, we show how periods of stagflationary nominal growth typically result in sharp slowdowns in real production and spending:

During periods of stagflationary nominal growth, income gains are not as valuable as in previous periods. When companies distribute incomes to employees, their real consumption power does not improve,i.e., they cannot demand as many goods and services. Additionally, when companies choose to reinvest profits, these profits cannot increase production as much as before. Thus, as inflation occupies more of the nominal income pie, it continues to pressure real and nominal growth. This creates a self-reinforcing spiral lower, which can only be halted by an improvement in output per dollar deployed (productivity) or a decrease in the availability of cash and credit powering demand. Based on the current dynamics, it looks highly likely that production and reinvestment will trend lower as the Fed tries to generate an adequate contraction in credit. However, these dynamics could take a while to play out, suggesting we could be in this environment for a while.

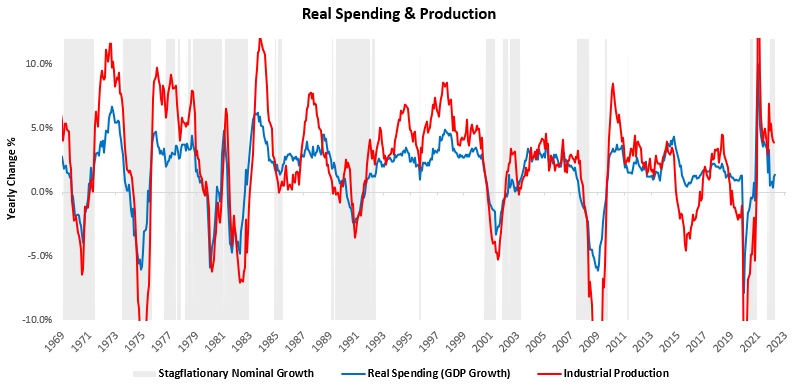

ii. The trend in PMI data remains weaker, despite an upside surprise in ISM. While ISM Data may have surprised expectations, the reading was very much in line with the deceleration we have seen in PMI data. ISM data showed an expansionary reading of 52.8, surprising consensus expectations of 51.9. This reading maintained the decelerating trend in ISM, staying more or less unchanged from the last print. We show the composition of the print below:

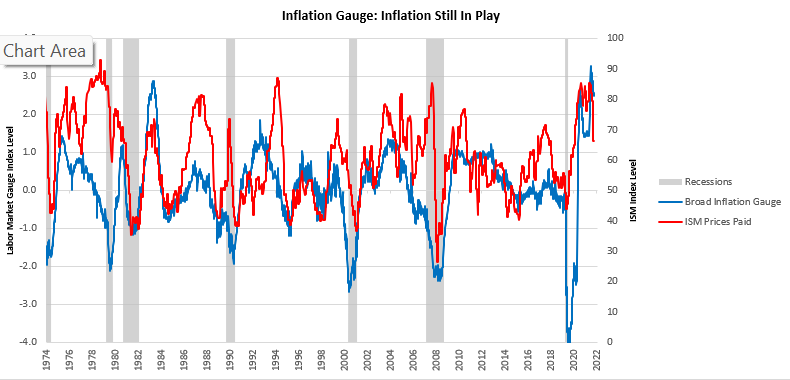

This ISM Manufacturing data implies a 5% YoY change in earnings estimates for the S&P 500. The largest gaining segment was Deliveries, and the largest slowdown was in Production. Of particular note, however, was the decline in ISM Prices paid. This data remains at odds with the hard economic data going into our revised broad inflation impulse gauge. (For those of you following our work regularly, we have recently revised our methodology for this gauge, resulting in higher readings):

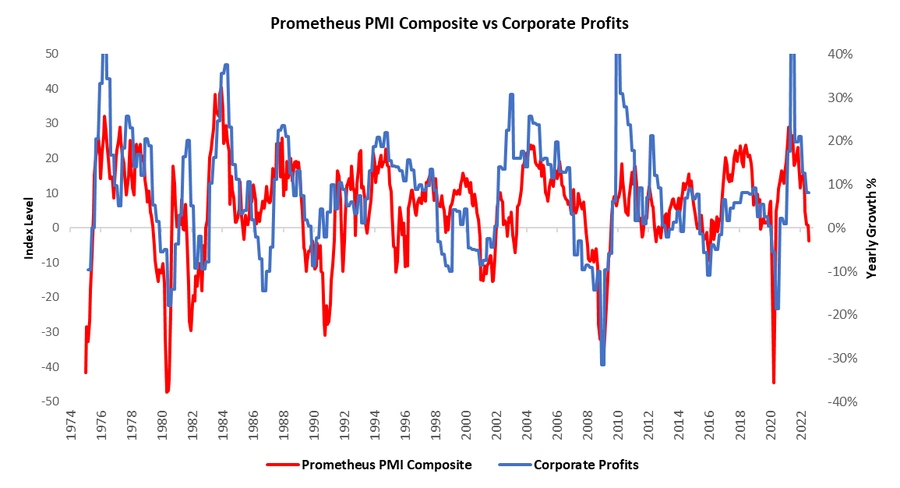

Furthermore, our PMI Composite, which aggregates PMIs and therefore offers a more broad-based insight into cyclical activity, continues to tell us that the pressure remains on profits to weaken cyclically:

With PMIs flagging a deterioration in cyclical activity, production under pressure due to nominal growth dynamics, inventories at extremely elevated growth rates, & the fiscal impulse tightening our systems continue to estimate the outlook for profitability remains weak. Our systems remain short equities and credit.

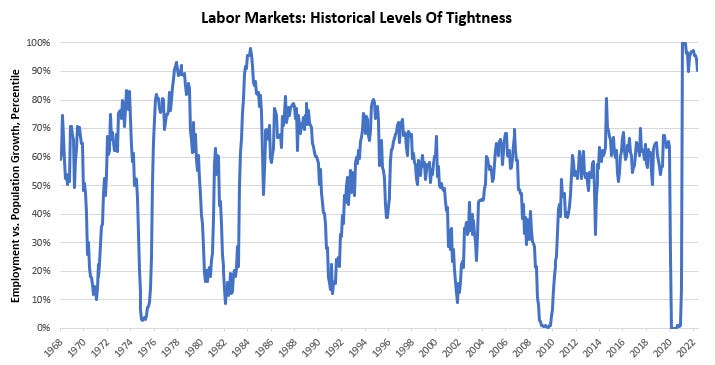

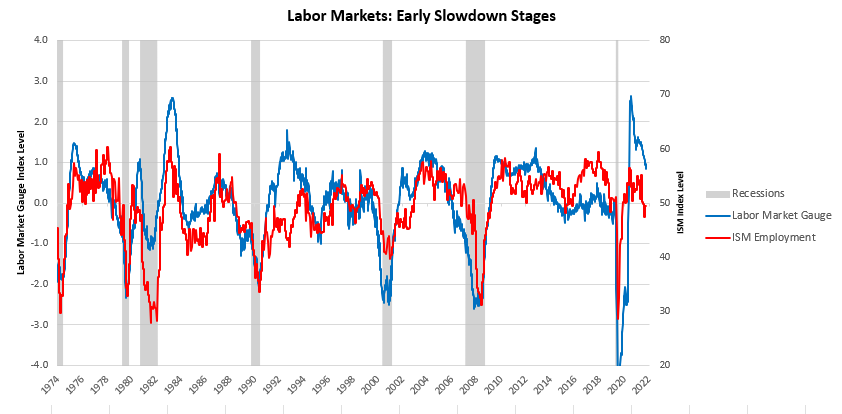

iii. Labor markets remain at historical levels of tightness. We show below the tightness of labor markets relative to historywe are in one of the tightest labor markets on record.

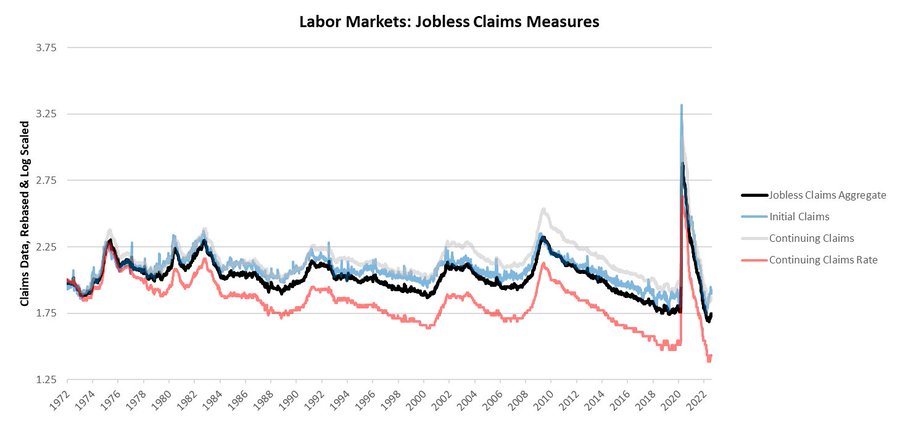

The tightness of this labor market continues to feed services inflation, and as yet, we have only seen the most nascent signs of a turning point here. Jobless claims data continued to paint a picture of expansion. Today’s Initial Claims disappointed expectations coming in at 232 versus the expected 247.5 while Continuing Claims surprised expectations coming in at 1438 versus the expected 1437. Below, we show these measures, along with the Continuing Claims Rate:

Additionally, we show the recent evolution of Jobless Claims Data over the last twelve weeks. Our tracking of Jobless Claims currently tells us that we are a ways off from recessionary territory:

However, our labor market gauges have begun to turn, and when these enter negative territory, we expect markets to price significant changes to the growth outlook:

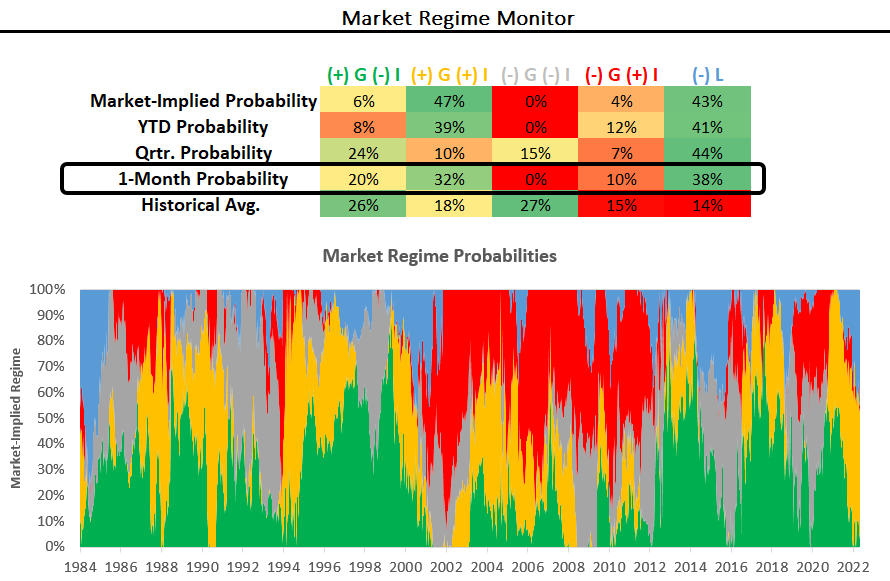

Our systems continue to show that we are in a stagflationary nominal growth environment with tightening liquidity conditions. Nominal growth dynamics remain resilient as the economy works through monetary excesses built through joint monetary and fiscal support. During the COVID-19 crisis, government authorities created large amounts of liquidity in both financial markets and in the real economy. While the Fed is moving to drain some of this in markets via quantitative tightening, the fiscal authority can only drain its liquidity creation via taxation. Without higher taxation, it is extremely hard to destroy policy liquidity, as it is essentially cash, i.e., government liabilities have almost no risk of default and therefore can’t be written down significantly. Inflation is an organic result of this phenomenon, where liquid assets exceed the economy’s capacity, and the only way to mechanically correct these imbalances is to erode the currency’s value. Resultantly, markets continue to price these dynamics:

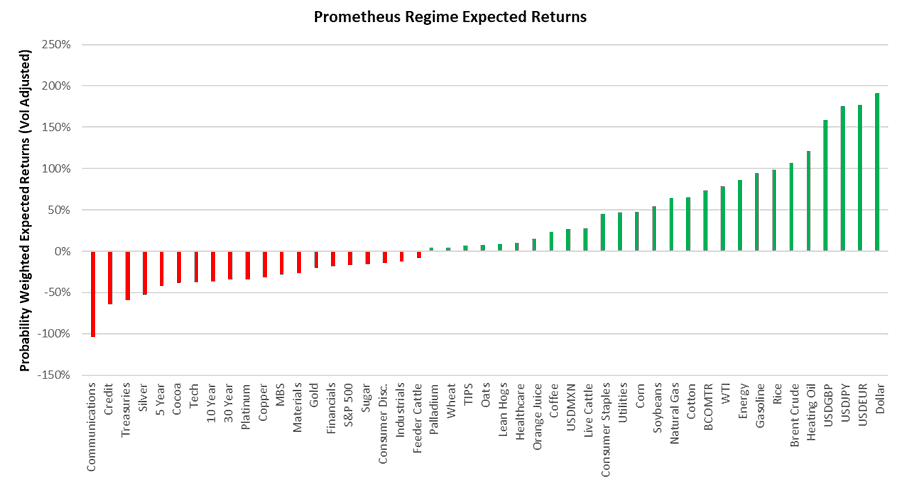

This environment doesn’t favor treasuries & doesn’t favor equities (selectively). This is further reinforced by our regime-expected returns that account for the economic environment and are a much better pro-cyclical gauge of the returns we can expect in a given environment:

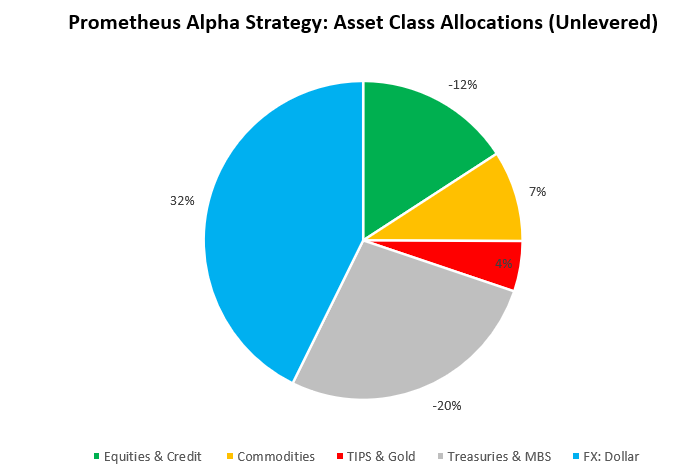

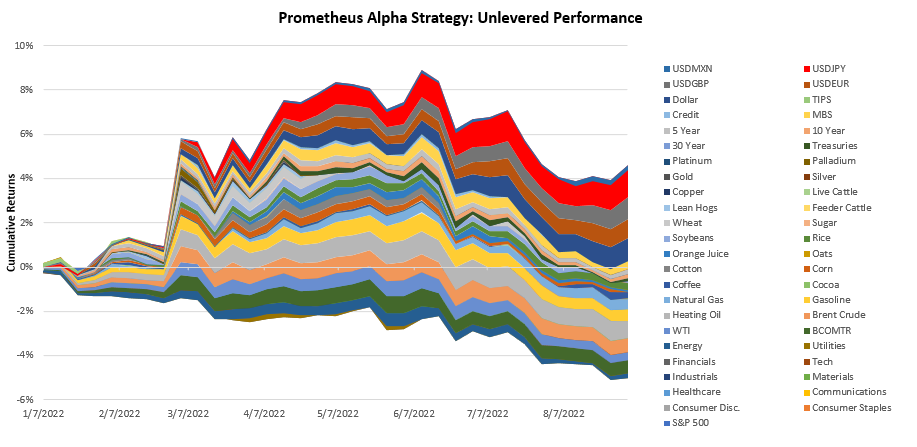

Resultantly our systems are net short equities & credit once again, alongside shorting treasuries. We have paired this with inflation hedges and long-dollar positions, creating a portfolio that will likely benefit from stagflationary dynamics and tighter liquidity conditions:

Our systematic approach has proven a strong guide this year, with our strategies In positive territory despite a difficult year for stocks & bonds. We continue to expect our strategies to harvest returns over the cycle:

We will eventually reach a point when self-reinforcing dynamics of weakening growth will tip us into a deflationary environment, but we simply aren’t there yet. In the meantime, stay nimble.