Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of both the economy and financial markets in real-time. Here are the top developments that stand out to us:

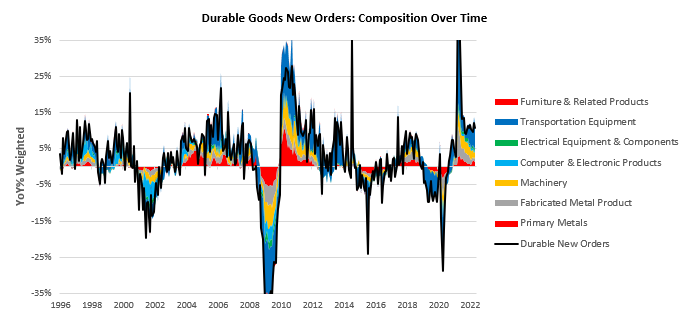

i. New Orders data suggest sustained business demand for manufacturing but also reflects inflationary pressures. Durable goods orders are often seen as a leading indicator of economic activity, as the private sector increases demand for durable goods when the economic outlook is strong. However, during heightened inflation uncertainty, consumers and businesses may front-load expenditures if they expect prices to increase over time. The result is heightened nominal demand but isn’t necessarily a healthy indication. Digging into the data, Manufacturers New-Orders for Durable Goods came in at 10.7%, a sequential deceleration from the last print. This print surprised expectations with a monthly change of 0.7% versus expectations of 0.1%. We show the composition of the trend in the data below:

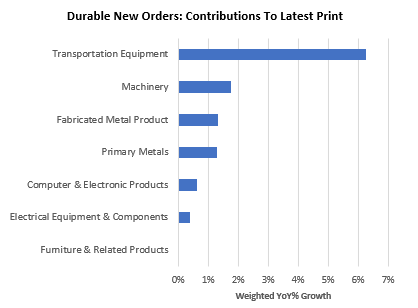

Transportation Equipment has been the largest contributor to these moves, with a weighted year-over-year growth of 6.3%. We show the weighted contributions of significant categories to the headline number below:

Over the last year, Durable Goods New Orders have been in a downtrend, and the latest values confirm this trend. Below, we show in tabular form how different areas have contributed to durable goods orders:

Overall, this data, while often interpreted by popular media as a sign of real growth, is likely more indicative of a high level of nominal demand.

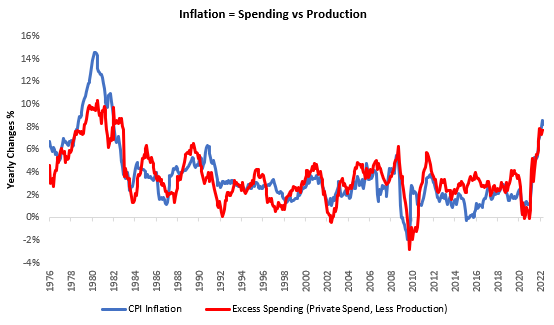

ii. Taming of inflation will come through curbing nominal demand, not increased production. This demand reduction will weigh on equities further. At a high level, inflation is a function of total spending relative to the output level. Currently, we are witnessing a high level of nominal expenditure, with production accelerating to match demand but falling behind. Spending in excess of production constraints creates inflationary pressures and can only be reconciled through higher or lower expenditures. We show our gauge of excess spending relative to production alongside CPI inflation below:

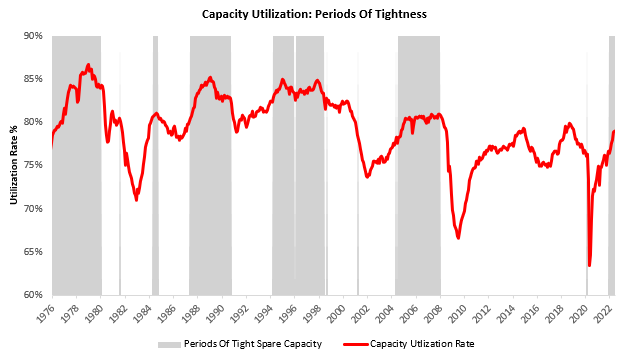

As we can see above, an elevated level of nominal spending, combined with lagging production, has resulted in significant inflationary pressures. There are only two ways this dynamic changes: reduced private sector demand (lower consumption, orders, etc.) or much higher production levels. Production of goods is much like employment in that physical constraints limit it, and therefore there are limits to which production can respond to demand shocks. Production growth is determined by the degree of capacity utilization in the economy, and relative to recent history, capacity utilization is elevated, i.e., spare capacity is tight:

Therefore, the likely resolution to inflationary pressures would be through decreased private sector demand. This dynamic would continue to weigh on equities, which are already struggling during a time of high inflation volatility.

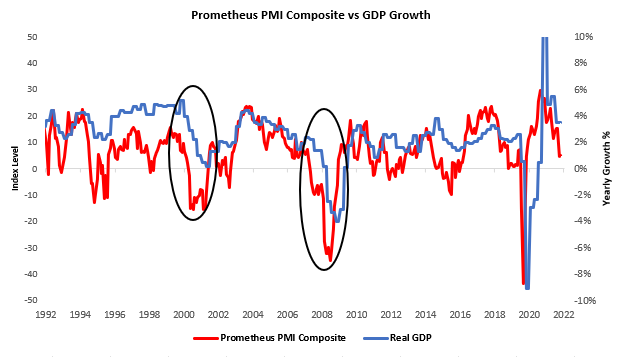

iii. The latest PMI data continue to advocate for a slowdown in economic growth. The latest PMI data from the Dallas Fed moved our PMI composite even lower. As we have shown previously, the PMI composite offers insight into the future path of economic activity; we show this below:

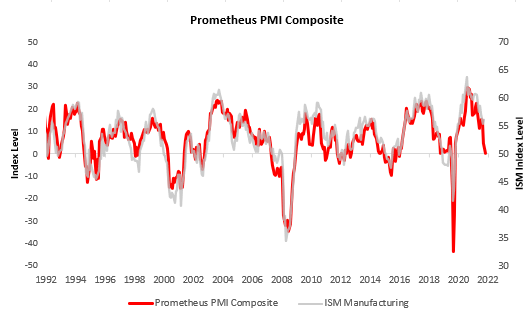

Furthermore, our PMI composite suggests there is significant pressure on the ISM PMI to head lower later this week:

The outlook for real economic growth remains weak; allocate accordingly.

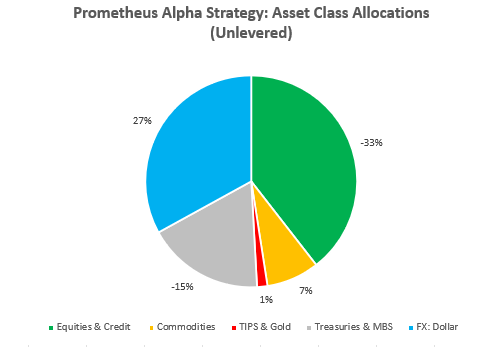

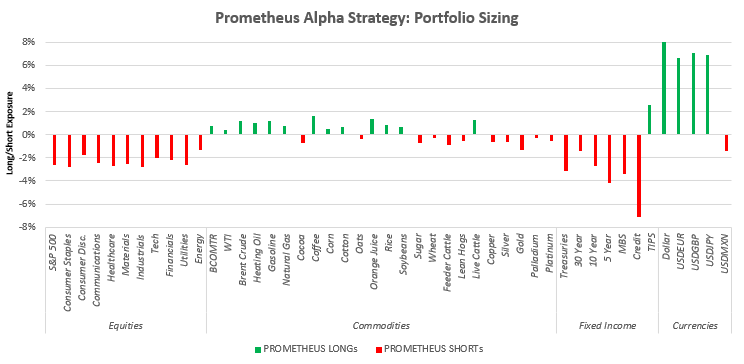

Our systems consider the principles that underly our economic and market analysis to create rules-based portfolios. Currently, our systems remain short assets that prefer stable or falling inflation, i.e., stocks, treasuries, and credit. This positioning is despite markets pricing elevated odds of tightening liquidity conditions. Tightening liquidity conditions are a difficult period for all assets and, in the past, has resulted in outsized returns on Treasuries. However, we are in a different variation of tightening liquidity, i.e., one where inflationary pressures remain resolute. This dynamic highlights the importance of having a rules-based process that is not only informed by historical performance but also understands the mechanics driving historical performance. There will come a time for us to pivot on our Treasury positions, and we are getting closer to that point, but we aren’t there yet. Here’s how our Alpha Strategy is positioned in this context, at the asset class level:

Here are the positions at the security level:

Stay nimble.