Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of both the economy and financial markets in real-time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

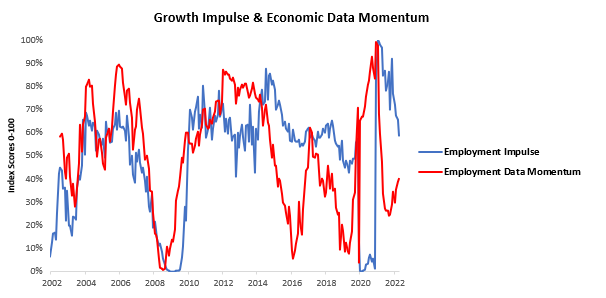

i. Labor markets have inflected, and we are seeing the early stages of deterioration. Below, we show our labor market gauge, which aggregates US employment and unemployment-related data into an aggregate, allowing us to view the impulse in labor markets:

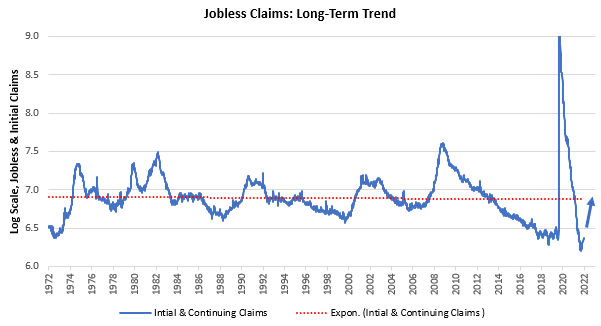

Relevant to developments in the labor markets, we saw a further uptick in initial jobless claims. Initial claims tend to be the first mover in the labor market complex to signal economic turning points:

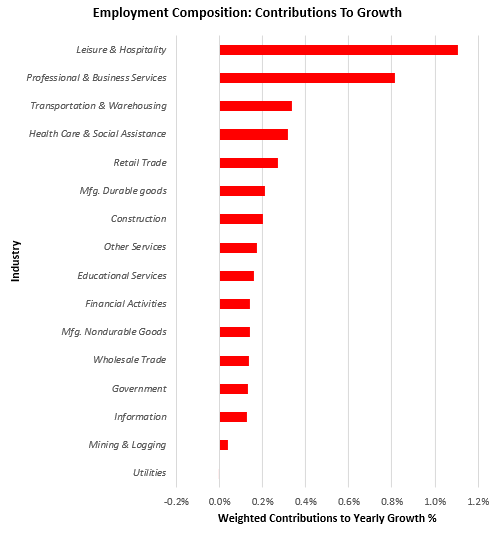

Massachusetts showed the most significant increase in weekly unemployment claims, while New York led the most significant decrease. Unemployment is broadly below trend on a secular basis; however, based on trend developing in profitability, income, and inflation, we think this potentiates future unemployment. In particular, we would expect a weakening in industries leading the charge in employment growth to catalyze the next leg lower in employment as discretionary spending drags as growth slows further:

Stepping back, we see these trends emerging in economic data momentum (our measure of whether data is surprising or disappointing on a cyclical basis) and employment impulse data. We show these below:

Labor markets are in the early innings of deterioration and likely have significantly more to go. Our systems will lead the way on how to position these moves.

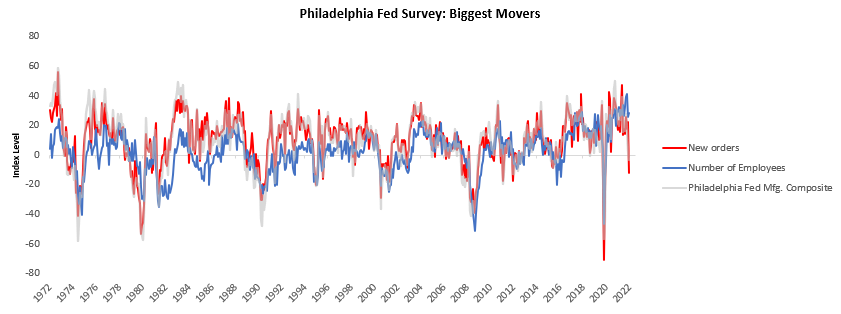

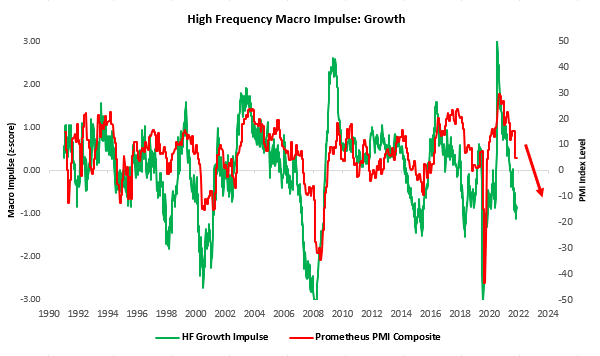

ii. PMI data continues to confirm a slowdown in economic activity. The latest Philadelphia Fed manufacturing survey data showed a contractionary reading of -3.3, implying 1% YoY earnings for the S&P 500. This reading was a sequential deceleration within a decelerating trend. The largest gaining segment was the number of employees, and the most significant slowdown was in new orders. We show this below:

We also show all the components of the survey of the current condition below:

This data is particularly concerning as the largest slowdown has come from the index’s new orders component, which is typically considered a leading indicator for future demand. Furthermore, our high-frequency impulse measure suggests there is more deceleration to come:

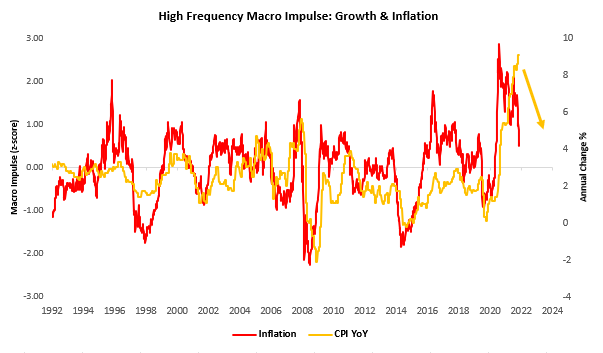

iii. Inflation remains elevated, but the inflation impulse has receded. High inflation continues to pressure the cost structure of companies and, thereby, equities and credit. However, our proprietary gauges are pointing to receding accelerations in inflationary pressures.

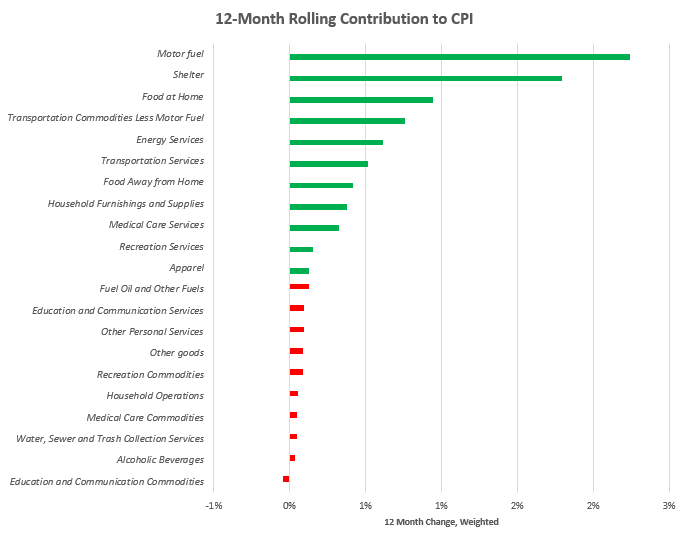

The divergence between our gauges and CPI is now significant to the extent we expect to see some cooling in CPI. The areas of CPI most exposed to slowdown pressures are those currently leading the pack:

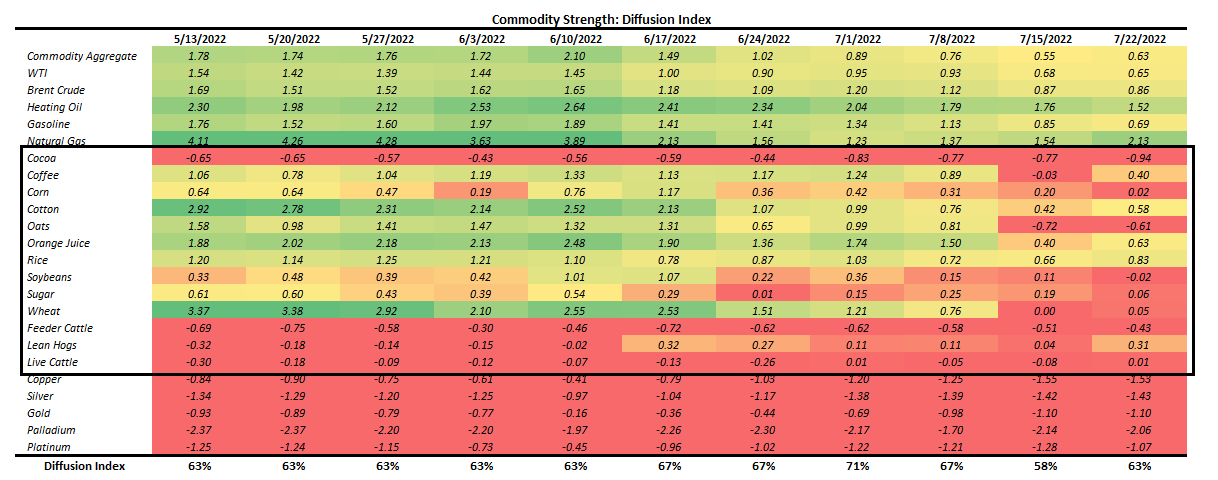

Transportation, food, and energy costs are now moving into a part of the cycle where considerable headwinds are developing. Motor vehicles and related expenditures are exposed to a cyclical slowing in consumer spending. At the same time, food and energy cost increases are likely to slow as the commodity complex shows weaker diffusion indices. We offer the weakening of the commodity complex below and highlight the declines in food & agricultural products:

Overall, we remain in a regime of heightened inflationary pressures; however, these forces are now more negative for equities & credit than they are positive for inflation assets. With nominal demand likely to continue on its downwards trajectory, we see far fewer opportunities in commodities beta than earlier this year; however, our signals continue to maintain exposure to the energy complex.

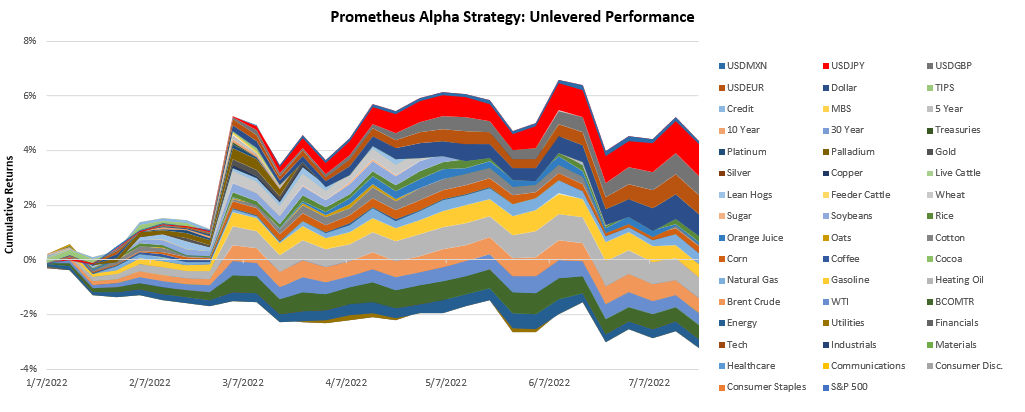

Our systems continue to tell us that tightening liquidity remains in full effect, and our asset allocations reflect these pressures. This week has seen markets move contrary to our positioning. However, we expect strategies to continue to perform well through the market cycle. We showcase our Alpha Strategy year-to-date performance, along with our current positioning below:

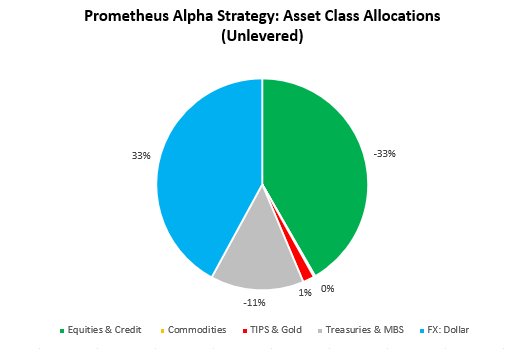

Our current asset class exposures are as follows:

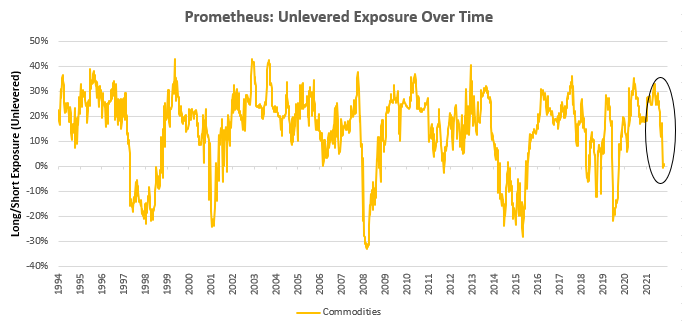

At the security level. We highlight that our commodity beta exposure is now neutral:

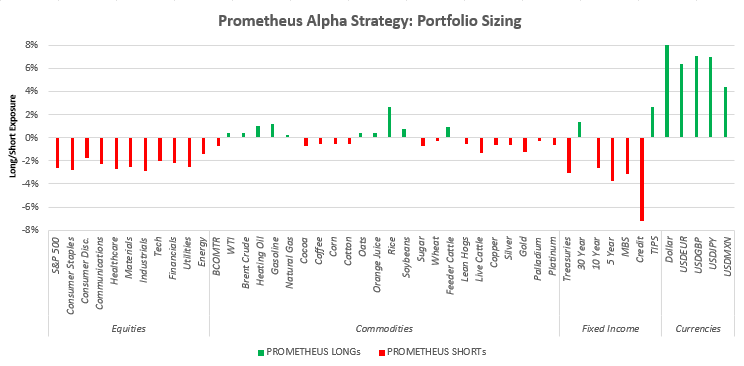

Finally, we show positioning at the security level:

Stay nimble.

From greeting to checkout, always a pleasant experience.

rx lisinopril

I appreciate the range of payment options they offer.

Global expertise that’s palpable with every service.

where can i get cheap cytotec pill

п»їExceptional service every time!

Their cross-border services are unmatched.

where can i buy generic clomid without dr prescription

Their online portal is user-friendly and intuitive.

They have an extensive range of skincare products.

can i get cheap clomid pills

Their commitment to international standards is evident.

They have a great selection of wellness products.

cost of cheap cipro

This pharmacy has a wonderful community feel.