Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real-time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

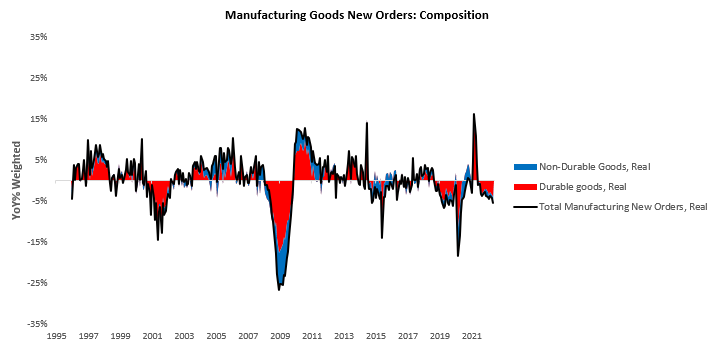

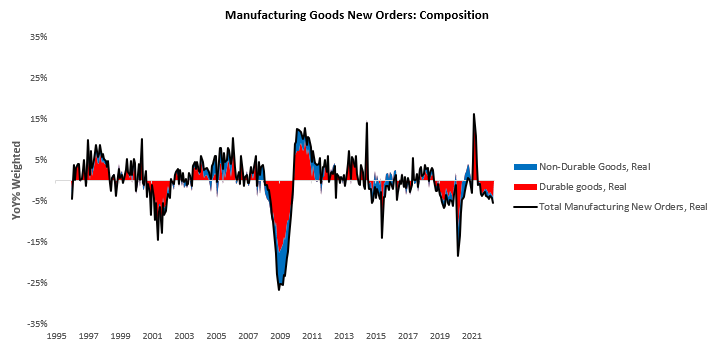

i. Manufacturing new orders came in stronger than expected on a nominal basis but weakened further on a real basis. Nominal manufacturing new orders increased by 1.95%, with durable goods and non-durable goods contributing 0.96% and 0.99%, respectively. However, in inflation-adjusted terms, we see a different picture. We show the relative contributions to yearly changes in real durable goods orders below:

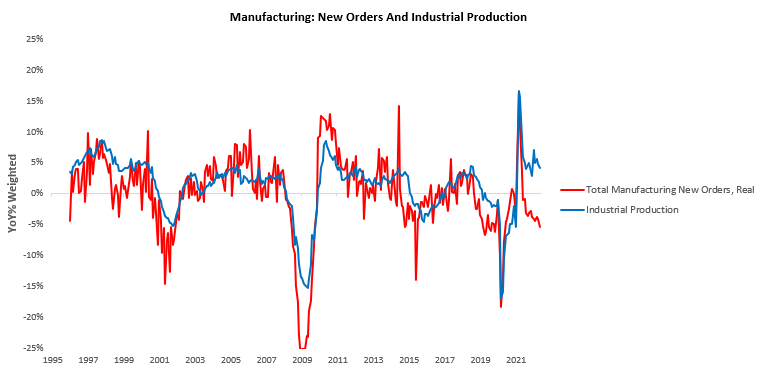

On a real basis, we estimate that total manufacturing new orders have decreased by 5.33% versus one year ago, with durable goods orders driving the majority of this decline (4%). Manufacturing new orders have a strong relationship with industrial production, as new orders facilitate the demand for production. However, manufacturing new orders is currently at odds with industrial production, telling us there is pressure on industrial production to fall.

As real demand continues to wane and production slows, private fixed investment will likely suffer, creating a further headwind for corporate profits. This headwind comes amidst an already tightening liquidity impulse from the US government, further eroding profitability.

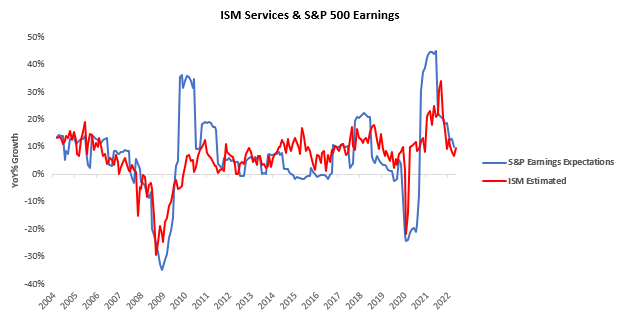

ii. ISM Services PMIs surprised expectations but remain in a downtrend. The latest ISM Services data showed an expansionary reading of 56.7, implying a 10% YoY change in earnings expectations for the S&P 500. This reading surprised expectations with a reading of 56.7 versus the expected 53.5.

This datapoint was a sequential acceleration within a decelerating trend. The largest gaining segment was Deliveries, and the most significant slowdown was in Employment. We show this in tabular form below:

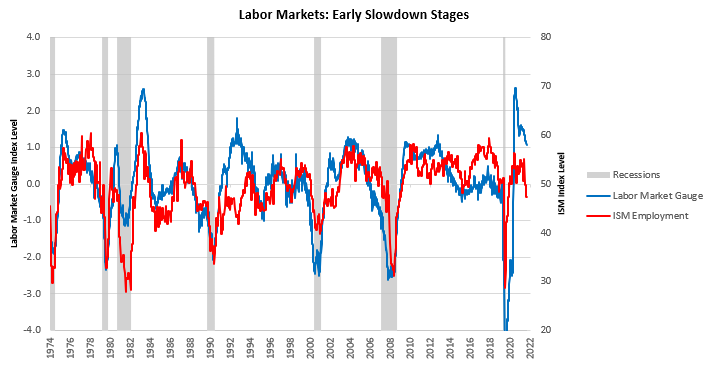

Of particular note in this print was the sustained weakness in the employment sub-component. This data, combined with ISM Manufacturing employment data, alongside our labor market gauge, continues to paint a picture of a deteriorating labor impulse:

On Friday, we will receive further incremental evidence on the labor market status this week in the form of nonfarm payrolls. The labor market remains the foundation upon which nominal spending is built, and we will need to see a deterioration here for nominal spending to decline.

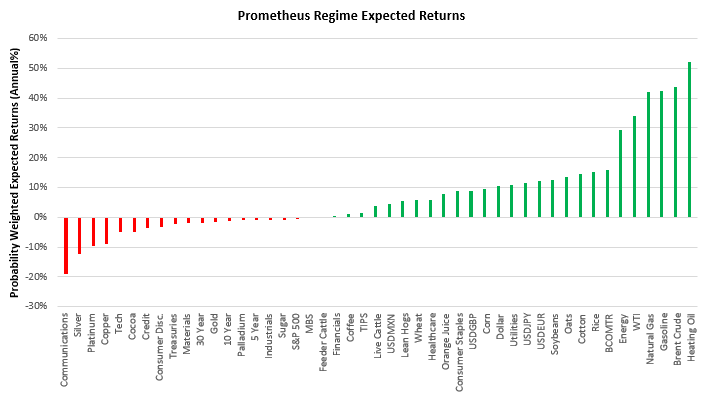

iii. History does not favor equities and credit in the current environment. Below we show our regime-expected return measures:

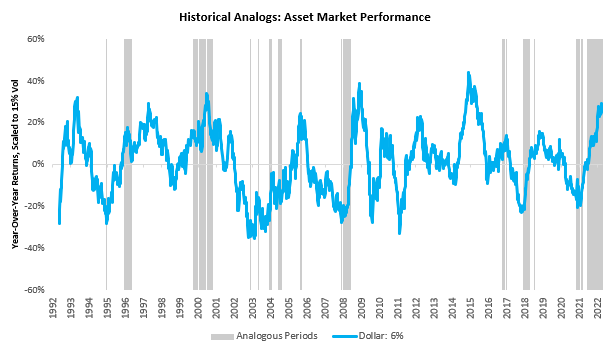

Our measures blend the current context and historical information to estimate the type of returns we can expect in a given environment. As we can see above, markets simply do not favor equity or credit exposure at this junction. Therefore, we continue to allocate defensively. Furthermore, tightening policy liquidity does not favor asset markets and will likely express itself with a higher dollar. Systematically looking at analogous periods, we find that markets tend to support the dollar:

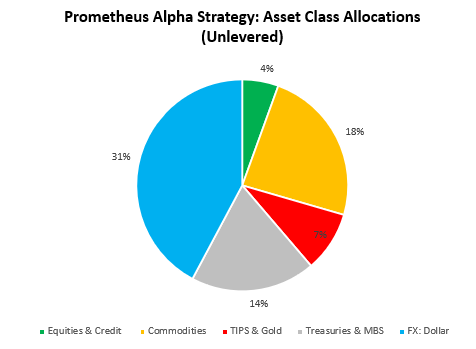

Overall, the combination of these factors continues to suggest we stay defensive. Our systems combine the underlying principles in our analysis into rules-based portfolio construction and continue to tell us to remain defensive in our exposures after being aggressively short equities & credit. Our systems estimate that the worst of the inflation shock is behind us. These dynamics create an environment where generating alpha via equity shorts becomes more challenging, but bond beta becomes easier to harvest. Resultantly, our systems are now significantly allocated to deflationary & tightening liquidity assets (Treasuries, MBS, Dollar, & Cash). However, our risk mitigation signals have also moved us towards marginally higher exposure to commodities. We show our Alpha Strategy asset class allocations below:

There will likely again be opportunities to generate outperformance on the short Quantitative Tightening accelerates, and we will wait for our systems to guide us. Stay nimble.