Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real-time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

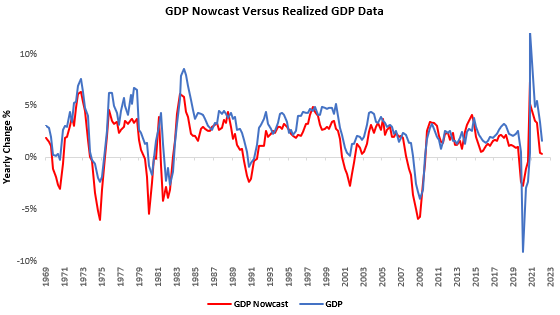

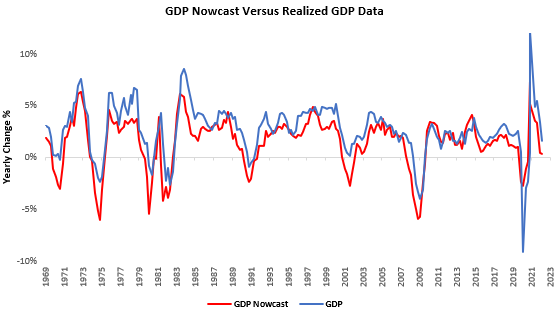

i. The latest GDP data came out in line with our estimated trajectory, i.e., on a downwards path. We show our GDP Nowcast relative to realized GDP data below:

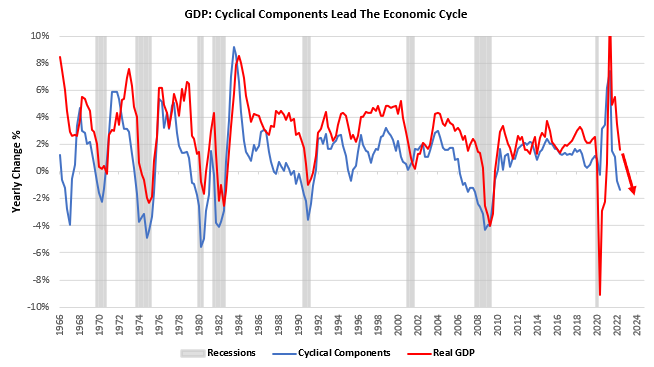

As we can see, GDP data remains on a downwards trajectory, and our systems estimate there is more weakness to come. Under the surface of this GDP print, we focus on real spending in areas highly procyclical, levered, and engender future spending as they typically move ahead of the rest of the GDP data. These cyclical components of GDP continue to paint a picture of economic deterioration in the future. We show this below:

There maybe be a debate on whether we are currently in a recession; however, we expect that the further weakening of economic data will likely resolve this debate.

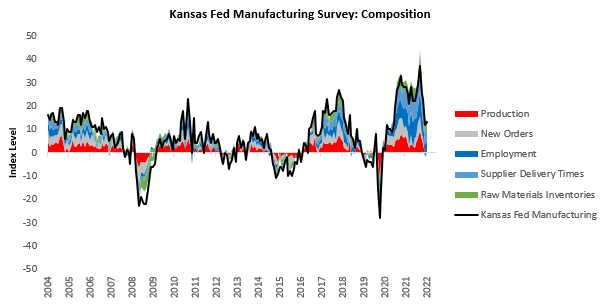

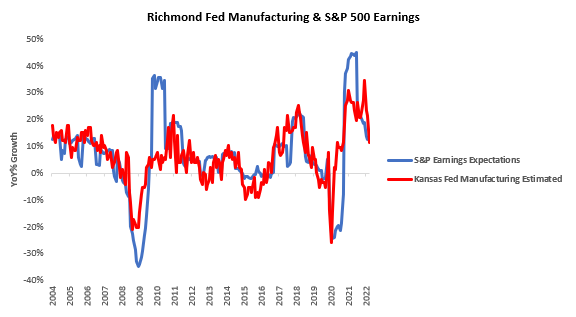

ii. Kansas Fed PMIs showed more support for a potential bounce in ISM Manufacturing data next week. The latest Richmond Fed manufacturing survey data showed an expansionary reading of 13, implying 13% YoY earnings for the S&P 500 (significantly higher than suggested by other PMI surveys). We offer the latest data below:

This reading was a sequential acceleration within a decelerating trend. The largest gaining segment was production, and the most significant slowdown was in employment. This confirms recent PMI data from the Richmond Fed, where we also saw weak sequential momentum in employment. We show the composition of the Kansas Fed composite below:

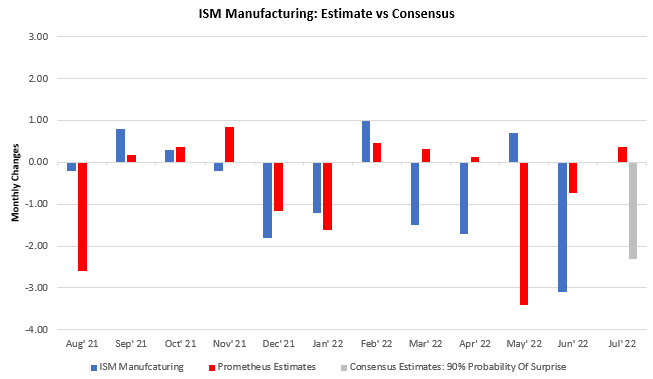

Aggregating this data into our forecasts, our systems show a high likelihood of an upside surprise in ISM Manufacturing data next week:

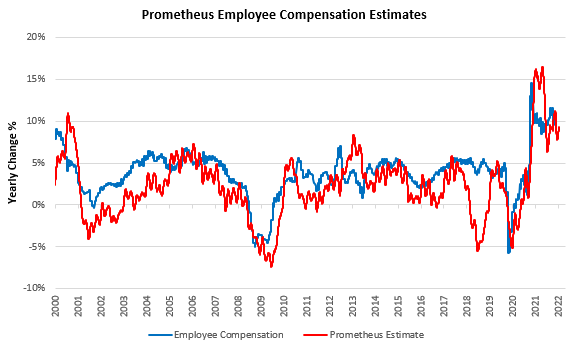

iii. Labor markets remain tight, keeping nominal income elevated. However, labor market growth has already inflected, suggesting headwinds on the horizon. Below, we show our high-frequency tracking of nominal employee incomes:

It is essential to note this data is no longer accelerating and has begun its descent. Furthermore, we see a similar dynamic in our labor market gauges, which also tell us that nominal incomes are going to face headwinds:

Our labor market gauge aggregates US employment and unemployment data into a single aggregate, allowing us to view the impulse in employment data. As we can see above, we are in the early stages of a slowdown. These risks will likely show themselves in markets, and our systems continue to position our portfolios to benefit from them.

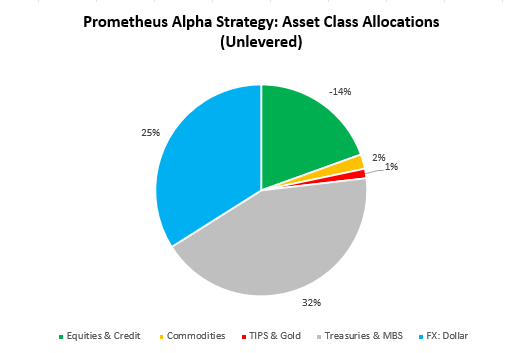

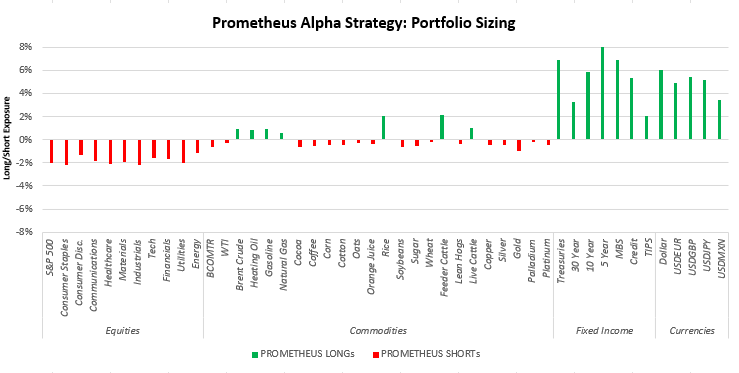

Our systems consider our economic and market analysis principles to create rules-based portfolios. Our portfolios have recently shifted towards Treasuries on the back of slowing inflation and deteriorating growth. They continue to remain long the dollar, short equities & credit. We show our asset class positioning below:

We show our security-level positioning as well:

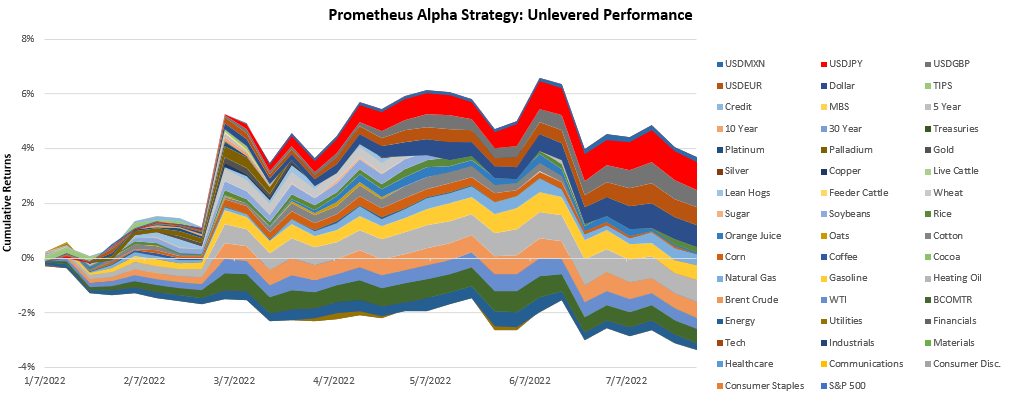

Finally, we show the year-to-date performance of the Alpha Strategy:

GDP data has weakened significantly, but there remains considerable room for further weakness. Stay nimble.

Hi there! Do you know if they make any plugins to assist with SEO?

I’m trying to get my blog to rank for some

targeted keywords but I’m not seeing very good gains. If you know of any please share.

Appreciate it! I saw similar blog here: Wool product

Howdy! Do you know if they make any plugins to help with Search Engine Optimization? I’m trying to get my site to rank

for some targeted keywords but I’m not seeing very good results.

If you know of any please share. Cheers! You can read similar text here: Coaching

I am really inspired along with your writing abilities as neatly

as with the structure in your weblog. Is this a paid

theme or did you customize it yourself? Either way stay up the

nice quality writing, it is uncommon to look a great weblog like

this one nowadays. HeyGen!

I am really inspired together with your writing abilities and also with

the format in your weblog. Is this a paid topic or did you modify it your self?

Either way stay up the nice quality writing, it’s uncommon to peer a great blog

like this one these days. Stan Store alternatives!

I am extremely impressed along with your writing abilities as neatly as with the format on your blog. Is that this a paid topic or did you modify it your self? Anyway keep up the nice high quality writing, it is rare to look a nice weblog like this one nowadays. I like prometheus-research.com ! Mine is: Tools For Creators

I’m really inspired with your writing skills and also with the format

for your weblog. Is that this a paid theme or did you modify it your self?

Anyway stay up the nice quality writing, it is uncommon to look a great weblog like this one nowadays.

HeyGen!

I don’t think the title of your article matches the content lol. Just kidding, mainly because I had some doubts after reading the article. https://accounts.binance.com/register?ref=P9L9FQKY