Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real-time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

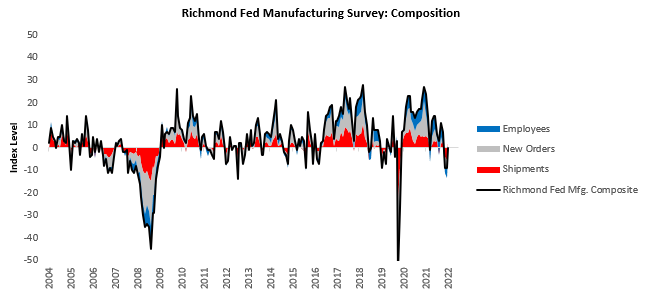

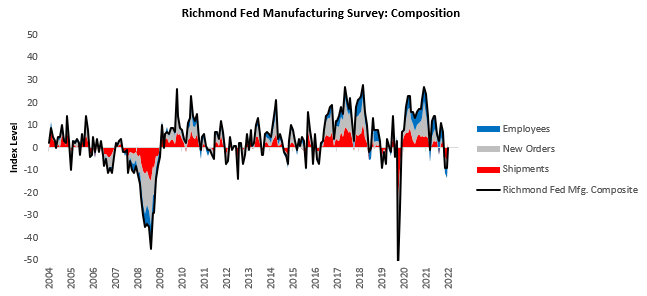

i. The latest PMI data showed some amelioration in downwards pressures. Nonetheless, the trend remains lower. We offer the latest PMI data from the Richmond Fed. The latest Richmond Fed manufacturing survey data showed a contractionary reading of 0, implying 5% YoY earnings for the S&P 500. We offer the composition of this data below:

This reading was a sequential acceleration within a decelerating trend. The largest gaining segment was Shipments, and the largest slowdown was in Employees. We show this in tabular form below:

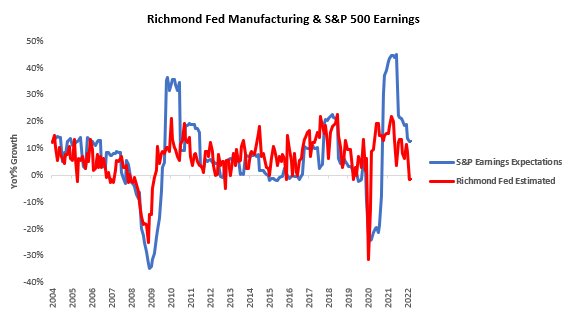

This recent counter-trend move marginally improves the earnings outlook, but minimally so. We show this below:

The pressure remains on earnings.

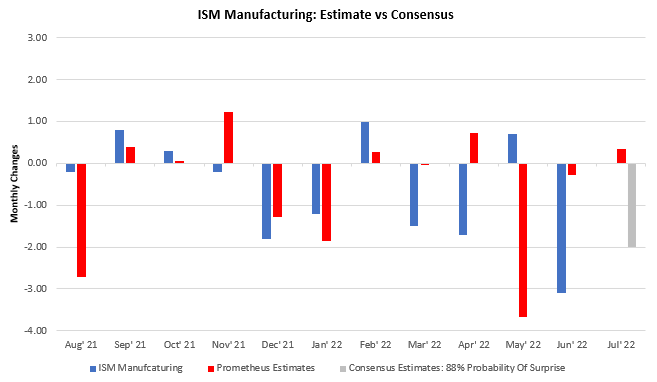

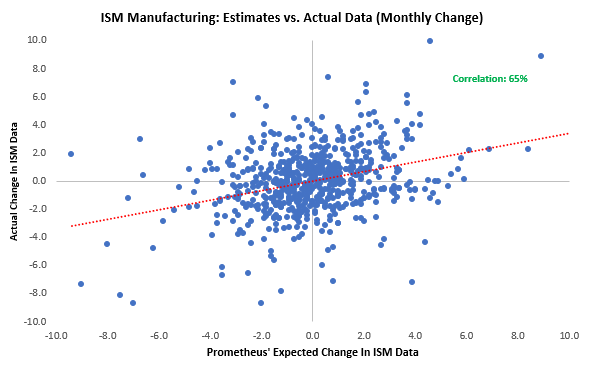

ii. ISM manufacturing data will likely surprise consensus expectations to the upside. Consensus expectations for ISM manufacturing data are for them to decline, and our systems tell us that economic forces continue to pressure PMIs lower. Nonetheless, our signals also tell us there is potential for a counter-trend surprise in the latest ISM print. Below, we show Prometheus’ estimates relative to realized data and consensus:

Our estimates imply a high chance for a data surprise; based on our ISM estimates, consensus expectations, and the typical error around our estimates. Our forecasts have typically been a decent gauge of changes in the level of ISM Manufacturing; we show this below:

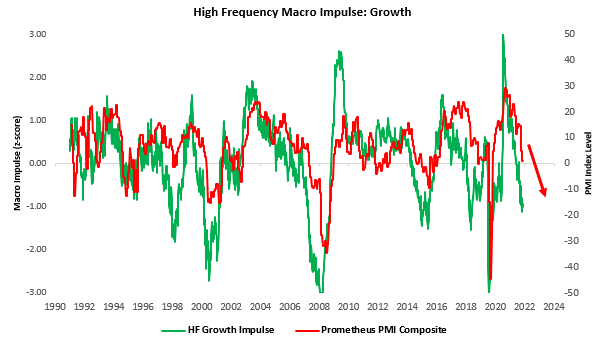

These forecasts offer insight into the print-by-print action; however, our systems take action based on longer trends that are more informative of the economic cycle. Our proprietary high-frequency impulse measures continue to tell us that the US PMIs will deteriorate. We show this gauge versus our PMI Composite below:

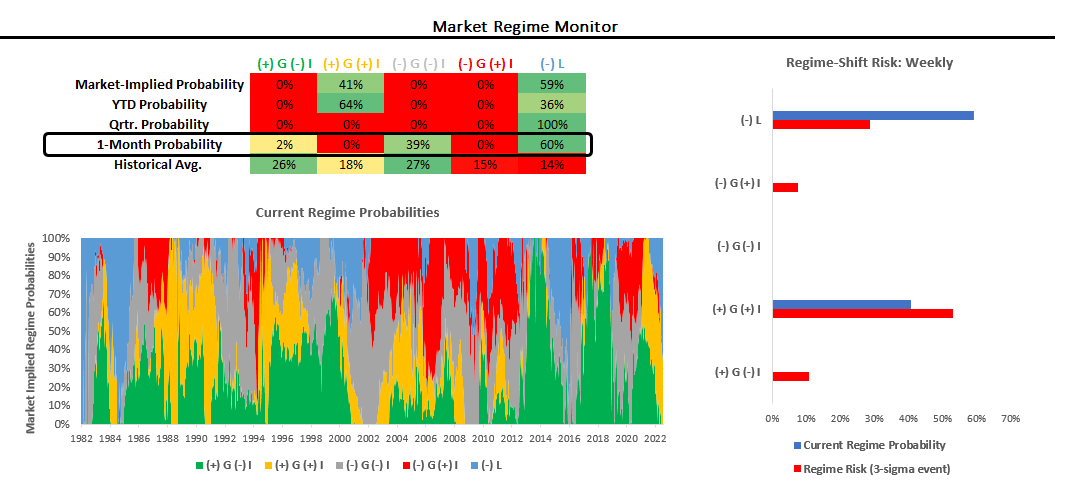

iii. As tightening liquidity pushes us closer to deflation, Treasuries will likely catch a bid. The odds of a disinflationary market regime are beginning to take hold of the market, simultaneously tightening liquidity as monetary and fiscal policy contracts.

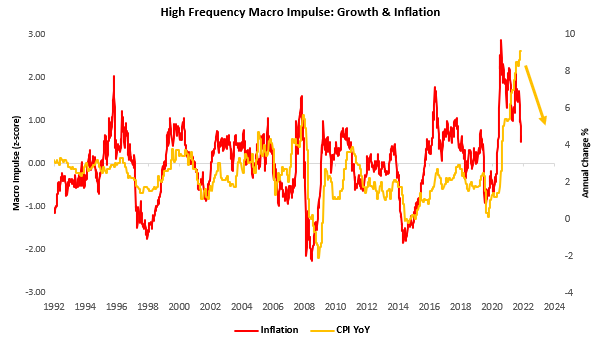

Tightening liquidity over time reduces the potential for inflationary pressures, and our gauges of inflationary pressure show abatement:

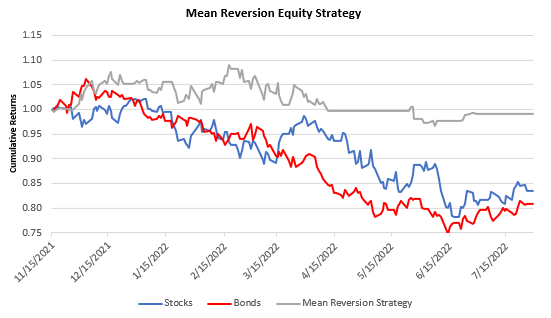

The moves in treasuries on a year-to-date basis have potentiated future returns on Treasuries. These losses have potentiated future returns, but they don’t necessarily catalyze them. However, weaker growth will likely be the primary driver of equity and bond returns as the inflation impulse fades. This dynamic creates increased “choppiness” in markets, as stocks and bonds have opposing biases. When growth becomes the primary driver of markets & stock-bond correlations are negative, we start to see an increasing amount of up-and-down movement on a daily and weekly basis in stocks as investors move to rebalance their exposures. Shorting gets more tactical in this environment. We show a simple strategy based on the phenomenon below. After sitting out the market for a long period of time, the strategy once again received signals to start trading yesterday:

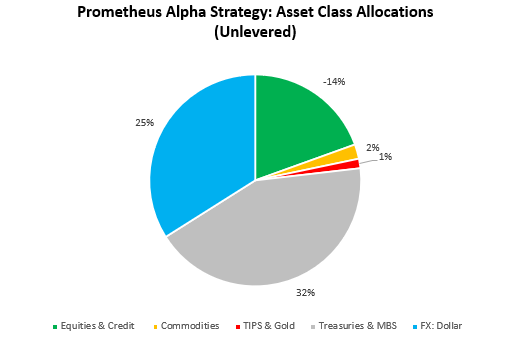

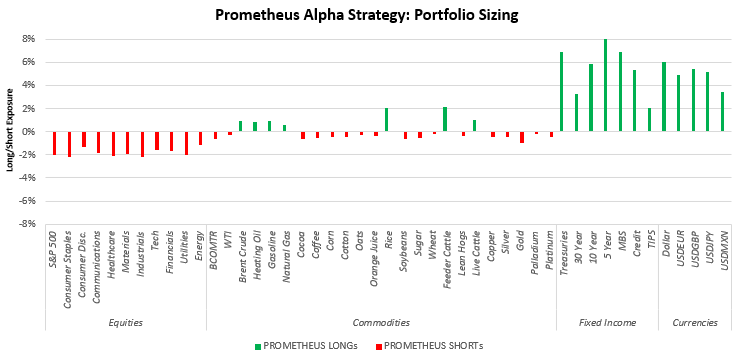

Equities and bonds are again moving in offsetting directions, creating a harder environment for shorts. Tactical shorting remains key to risk management. Nonetheless, our systems continue to hold equity shorts as the economic environment warrants these exposures. We show our Alpha Strategy positioning below:

Stay nimble.

Hello there! Do you know if they make any plugins to assist with

SEO? I’m trying to get my site to rank for some targeted keywords

but I’m not seeing very good results. If you know of any please share.

Appreciate it! I saw similar article here: Bij nl

Hey! Do you know if they make any plugins to assist with SEO?

I’m trying to get my website to rank for some targeted keywords but I’m

not seeing very good gains. If you know of any please share.

Cheers! I saw similar article here: Coaching

I’m really impressed with your writing talents as

smartly as with the structure to your weblog. Is this a paid topic or did you customize it yourself?

Anyway stay up the nice high quality writing, it is uncommon to look a great weblog like this one nowadays.

HeyGen!

I’m really impressed together with your writing talents and also with the structure for your weblog. Is that this a paid theme or did you modify it yourself? Either way keep up the excellent high quality writing, it is rare to look a great blog like this one these days. I like prometheus-research.com ! Mine is: Stan Store alternatives

I am extremely inspired with your writing skills and also with the layout

for your blog. Is that this a paid topic or did you customize it yourself?

Anyway keep up the nice quality writing, it’s rare to look a great weblog like this one these days.

Blaze ai!

Thanks for sharing. I read many of your blog posts, cool, your blog is very good.

Thank you for your sharing. I am worried that I lack creative ideas. It is your article that makes me full of hope. Thank you. But, I have a question, can you help me?