Long Stocks, Cash & Bonds

Welcome to our official publication of the Prometheus ETF Portfolio. The Prometheus ETF portfolio systematically combines our knowledge of macro & markets to create an active portfolio that aims to offer high risk-adjusted returns, durable performance, & low drawdowns. Given its systematic nature, we have tested the Prometheus ETF Portfolio through decades of history and have shown its durability. For those of you who are unacquainted with our systematic process, we offer a detailed explanation here:

In this publication, we will discuss the performance, positioning, & risks of the Prometheus ETF Portfolio and it will be published every week on Fridays to help investors understand how our systematic process is navigating through markets. Before diving into our ETF Portfolio positions, we think it is important for subscribers to understand the context within which our systems choose their exposures. Below, we offer our latest Month In Macro note, which contains the conceptual underpinnings of our systematic process within the context of the latest economic data:

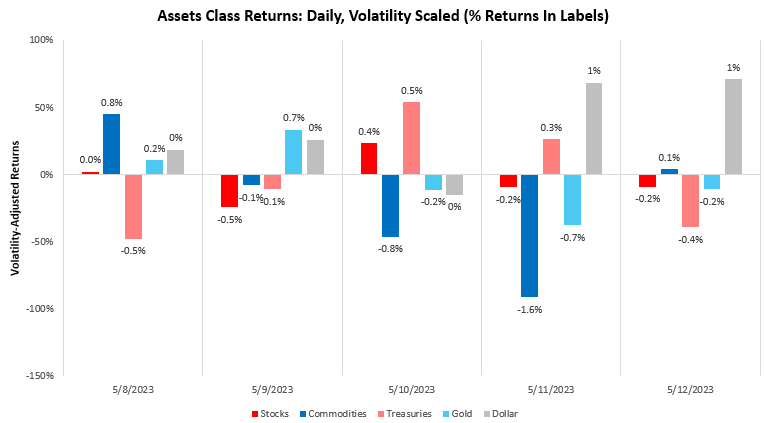

Last week proved to be a challenging week for markets as assets across the board declined. The only safe haven last week was in the form of cash and the dollar. We show the evaluation of markets over the last week below:

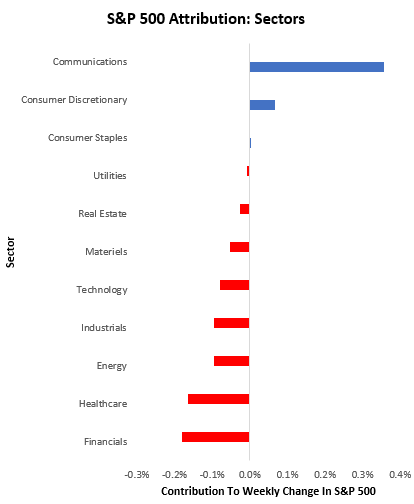

Digging a little deeper, weakness in the equity market was broad-based, with 8 out of 11 sectors down. Financials and healthcare dragged the index lower, while communications and consumer discretionary tried to push the index higher. Below, we show the weighted impact of these sector returns on S&P 500 total returns:

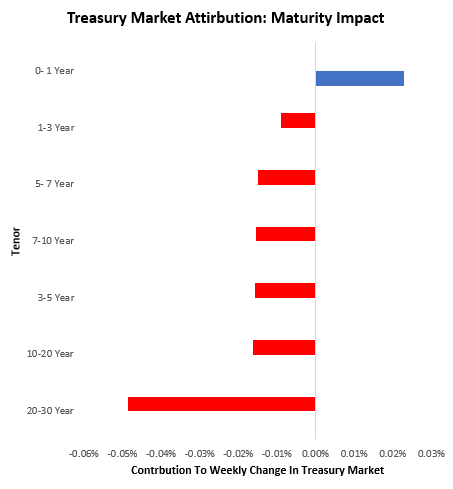

Alongside this weakness in equity markets, we also saw broad-based weakness across the Treasury market. We show the compositions of this weakness below:

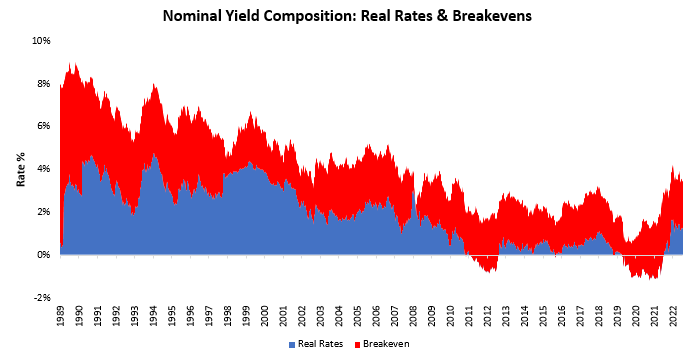

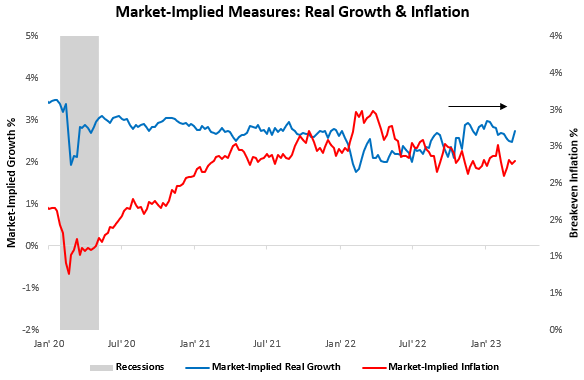

As we can see, the weakness of Treasuries was broad-based as well. These moves were driven less by inflation expectations in the form of breakevens and more by incremental expectations of policy tightening via higher real rates. We zoom out to show the big picture for these drivers below:

These moves came alongside economic data that suggest resilient inflation and potential moderating real growth, which implies the Fed has more tightening to do. This price action roughly squares with the theme we have seen throughout this year, with markets pricing flat nominal growth outcomes in markets:

Overall, market action remains contained as economic data does not paint a decisive picture. Within this context, opportunities remain meager until more decisive economic data shows. Our bias is that we are likely to see a transition into a stagflationary contraction in H2 of 2022. In this context, we turn to our Prometheus ETF Portfolio.

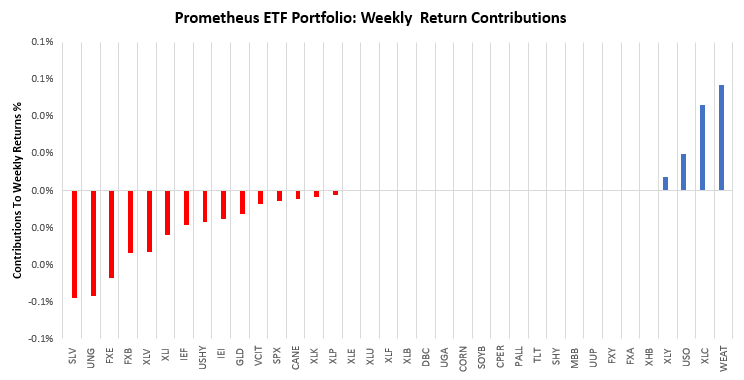

Over the last week, the Prometheus ETF Portfolio was down by -0.17%. This loss was well within expected parameters, and we see little cause for concern here. Below, we show the contributions to this portfolio performance across securities:

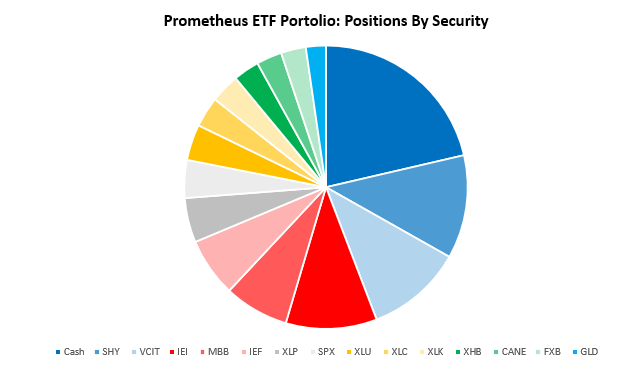

Turning to next week, our systems are looking to position the Prometheus ETF Portfolio, as shown below. The portfolio contains 15 positions heading into next week. We show these below:

POSITIONS: Cash: 21.37% SHY : 11.81% VCIT: 11.01% IEI : 10.4% MBB : 7.38% IEF : 6.72% XLP : 5.09% SPX : 4.32% XLU : 4.1% XLC : 3.46% XLK : 3.33% XHB : 2.97% CANE: 2.91% FXB : 2.85% GLD : 2.28% . Please note if the cash position is negative, it implies leverage.

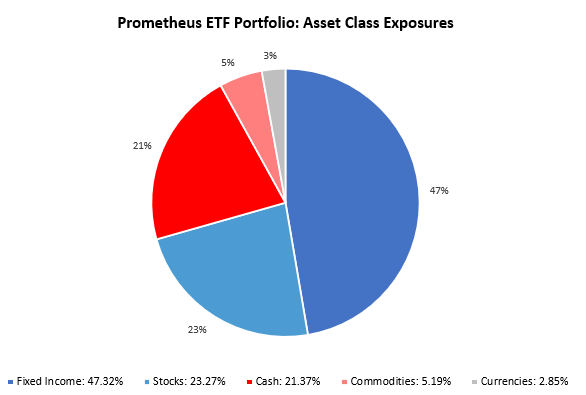

Additionally, we show these positions aggregated into asset class allocations below:

The portfolio has a net exposure (ex-cash) of 78.63%, with a gross exposure (ex-cash) of 78.63%, i.e., it is long-only. This allocation has an expected volatility of 4.99%, with maximum expected volatility of 10%. Given the disinflationary tilt of the portfolio, we think there is a modest risk of achieving maximum expected volatility from downside moves. Next week, we will have retail sales, industrial production, and housing data if these prints point to a stronger-than-expected economy, we are likely to move towards pricing further tightness by the Federal Reserve. We think the likelihood of strong retail sales and industrial production (barring an automobile surge) is limited but significant for housing data, so we will be watching closely. This remains a time for capital preservation. We continue to navigate the turn. Until next week.

cost generic clomiphene pills clomid rx for men can you get clomid without insurance get generic clomid online can you buy clomiphene prices where to buy clomiphene no prescription buy cheap clomiphene without dr prescription

The thoroughness in this piece is noteworthy.

I’ll certainly carry back to be familiar with more.

azithromycin 500mg canada – purchase azithromycin online order metronidazole 400mg without prescription

buy rybelsus 14mg without prescription – cyproheptadine 4 mg without prescription buy cyproheptadine online

motilium cost – brand motilium 10mg flexeril 15mg brand

purchase inderal generic – methotrexate where to buy buy methotrexate 10mg without prescription

amoxicillin for sale online – valsartan usa oral ipratropium 100mcg

anabolika und hgh kaufen

steroid medicine side effects