Recession On The Horizon: Fixed Income, Gold, & Commodities

Welcome to our official publication of the Prometheus ETF Portfolio. The Prometheus ETF portfolio systematically combines our knowledge of macro & markets to create an active portfolio that aims to offer high risk-adjusted returns, durable performance, & low drawdowns. Given its systematic nature, we have tested the Prometheus ETF Portfolio through decades of history and have shown its durability. For those of you who are unacquainted with our systematic process, we offer a detailed explanation here:

In this publication, we will discuss the performance, positioning, & risks of the Prometheus ETF Portfolio and it will be published every week on Fridays to help investors understand how our systematic process is navigating through markets. Before we dive into our ETF Portfolio positions, we think it is important for subscribers to understand the context within which our systems are choosing their exposures. Below, we offer our detailed Month In Macro note, which contains the conceptual underpinnings of our systematic process within the context of the latest economic data:

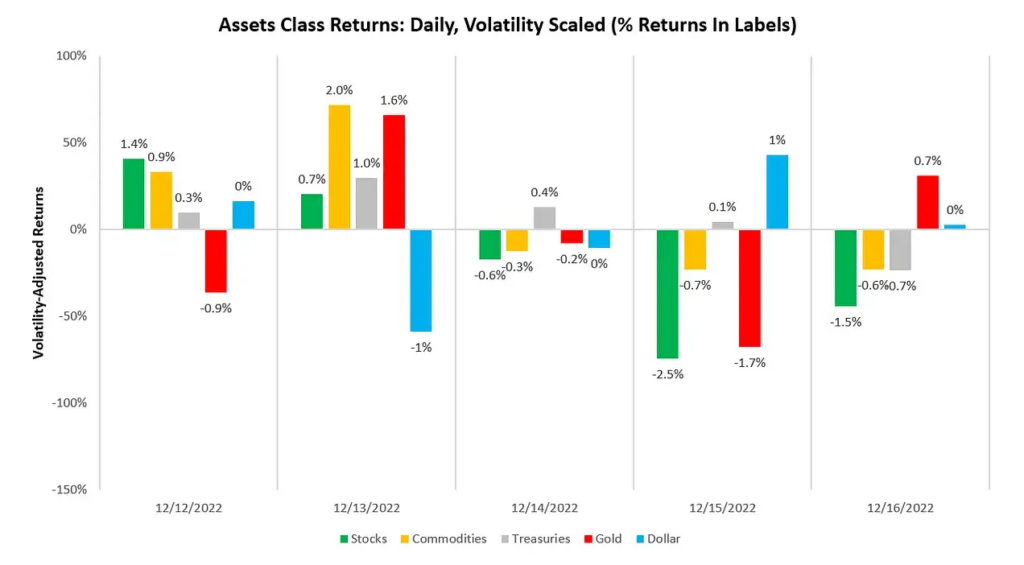

Turning to the week that was asset markets have moved to reflect the initial stages of a nascent turning point one where the principal driver of market moves transitions from inflation volatility to growth volatility. To elaborate: volatility in economies and markets creates conditions whereby future conditions are less likely to be like the recent past. These dynamics, while intuitively understandable, are hard to visualize and quantitatively account for. As a result, consensus expectations in markets are primarily a function of extrapolating the most recent past into the future. When we enter periods of high volatility (in growth, inflation, liquidity, etc.), the potential for economic surprises widens. As markets are discounting machines, unexpected events create significant moves. 2022 was a case in point market expectations of inflation were persistently shocked due to extreme inflation volatility created by both cyclical and idiosyncratic factors, causing a historic sell-off in fixed income.

In today’s context, our tracking of conditions continues to show that conflicting economic pressures are ameliorating inflationary pressures today. Continuing down the path will suggest an inflation trend of 3.5% to 4.5%. Crucially, resilient segments of the services economy are likely to support inflation, while weaker areas of the goods economy are likely to detract from inflation. The combination of these factors creates an environment where inflationary pressures are likely to be muted relative to those we have witnessed in H1 2022. However, the evolution of economic conditions increasingly suggests both a profit recession and, now, a GDP recession are incoming. Within this context, we entered the Prometheus ETF Portfolio long fixed income, gold, silver, and select agricultural commodities. Below, we show the evolution of asset classes over the last week:

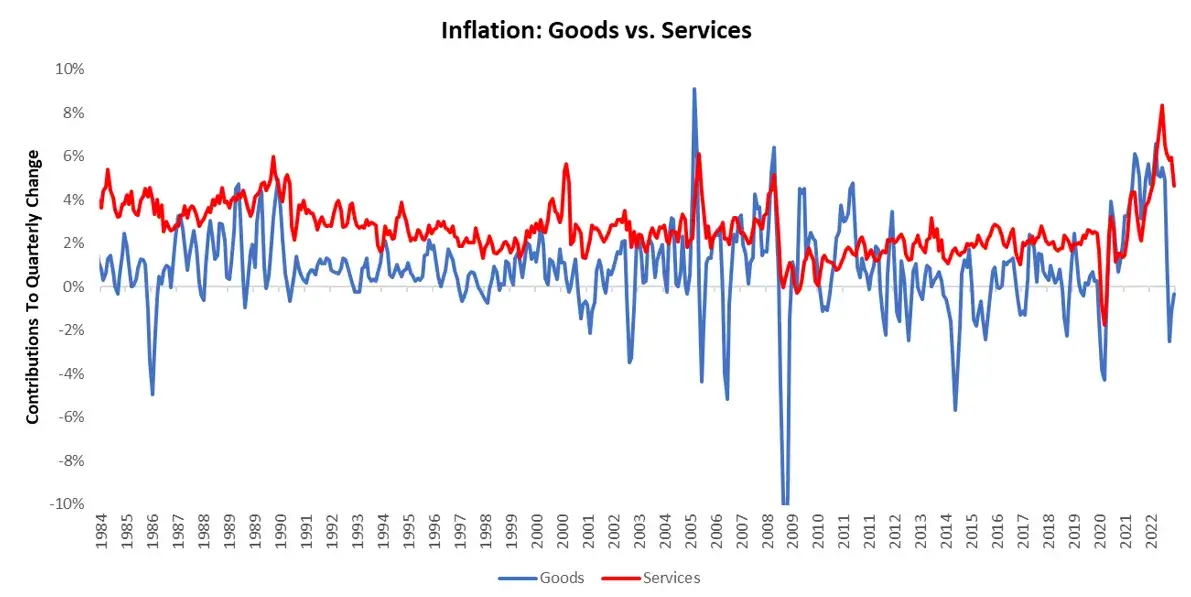

Consistent with our expectations of the inflation trend, we entered the week with a view that CPI would come in at 0.39% on Tuesday higher than expected by consensus. Our models proved incorrect in this expectation. CPI came in significantly lower than our expectations and those of consensus. The primary driver of this divergence was unexpected services deflation, primarily coming from Medical Care and Energy Services. Housing, durable goods, and nondurable goods were within the range of expected outcomes and consistent with broader pressures. The goods economy continues to feel pressure, with the potential for this pressure to spread to the broader economy. We show Goods vs. Services inflation below:

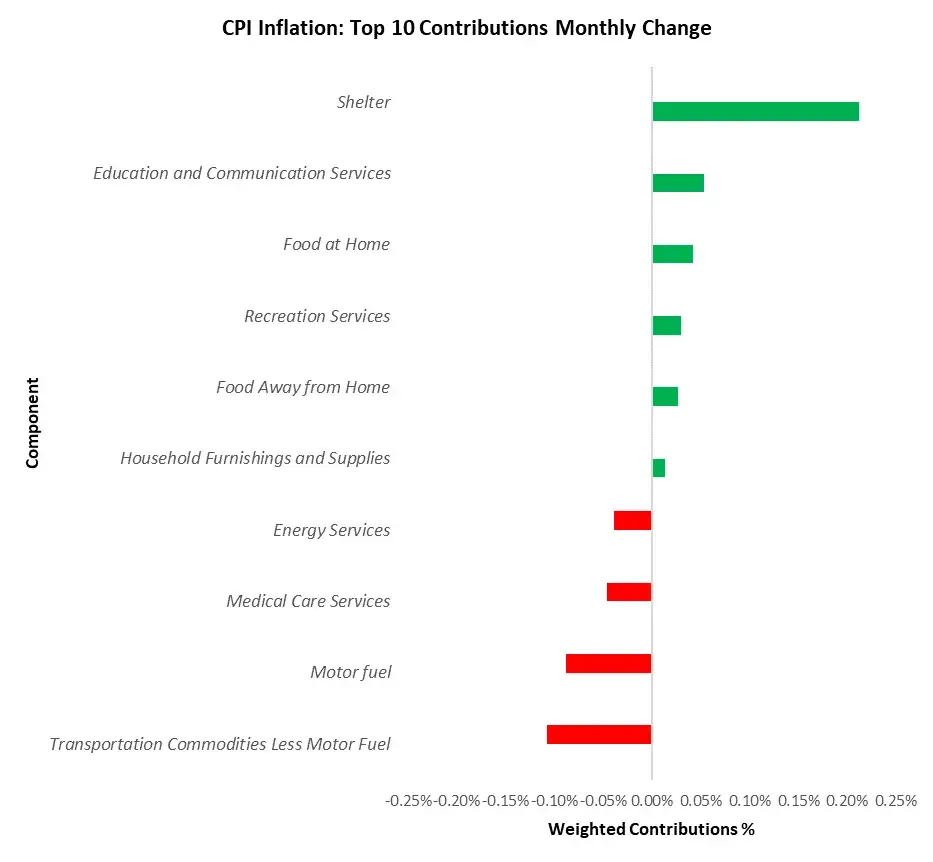

The primary drivers of this print were Motor fuel (-0.09%), Transportation Commodities Less Motor Fuel (-0.11%), Shelter (0.21%), Medical Care Services (-0.05%), & Education and Communication Services (0.05%). Below, we show the top 10 drivers of the monthly change:

We guided those with discretionary ability to trade the event to reduce exposure. While this proved less than maintaining exposure consistent with the systematic construction ex-ante, we think it remained prudent to provide this information.

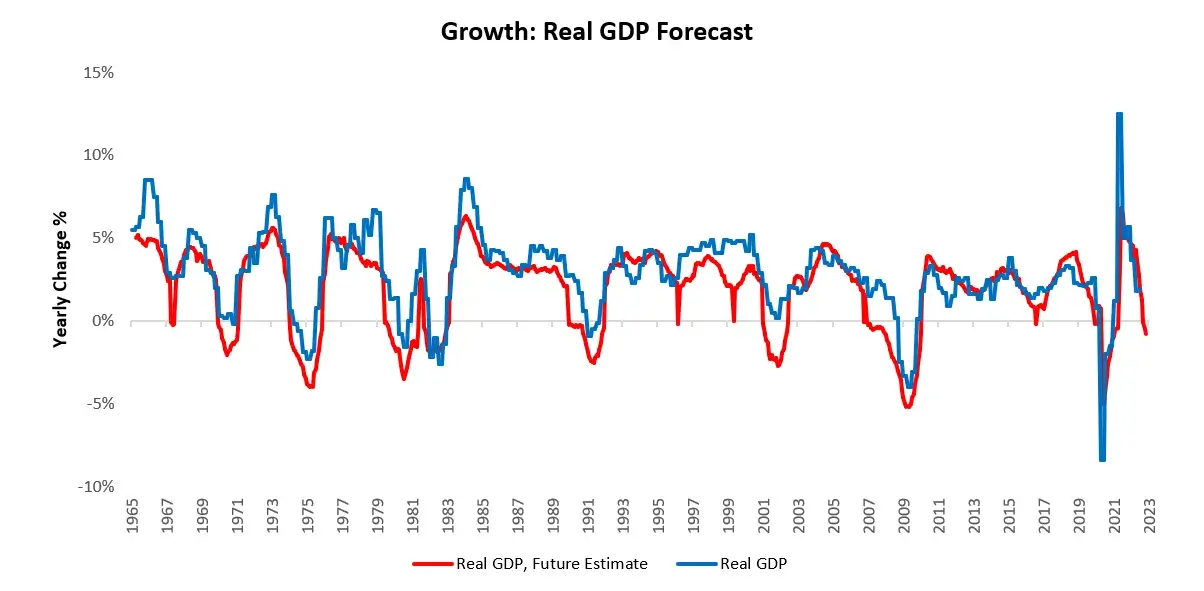

Following CPI, we had the Federal Reserve come out with a 50 basis point hike to interest rates, alongside a strong message from Jerome Powell that the Fed would like to see a sustained tightening of financial conditions. This messaging is consistent with our expectations, i.e., the Federal Reserve will likely lean on maintaining interest rates at a high level to achieve this tightening rather than accelerating the pace or size of further hikes. Our assessment of economic conditions suggests that the initial conditions required to facilitate contraction in economic growth and stabilization of inflation (though far from the 2% target) are already in place. Our systems are now moving to estimate a GDP contraction in the coming quarters; we show this below:

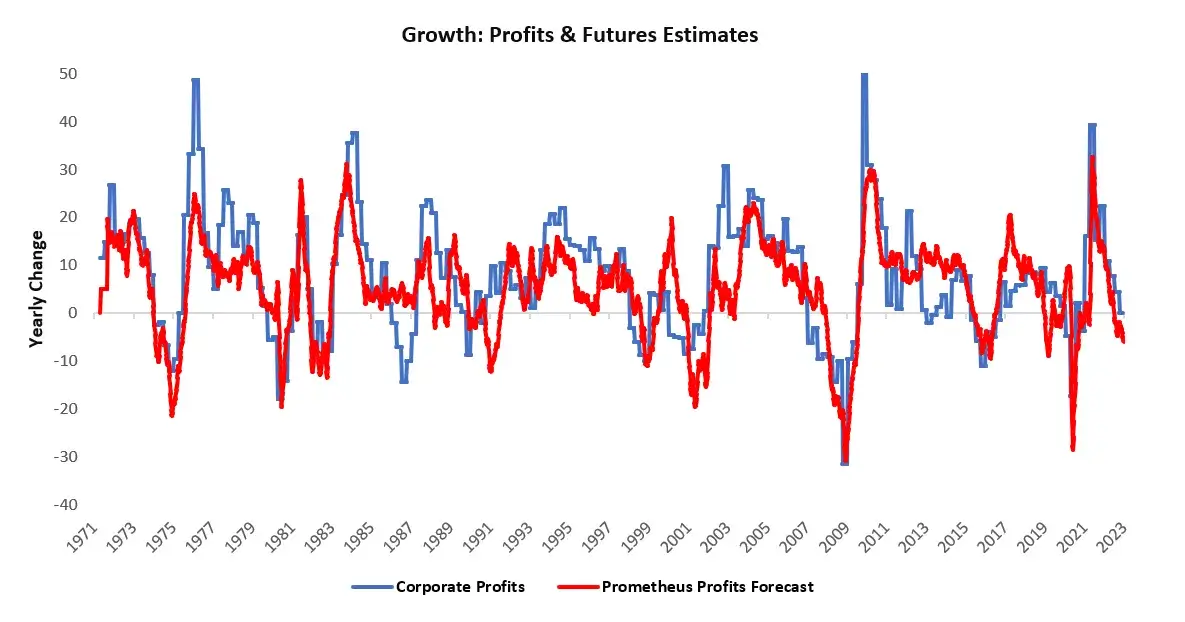

These expectations of a potential real GDP contraction come alongside expectations of a nominal profit contraction:

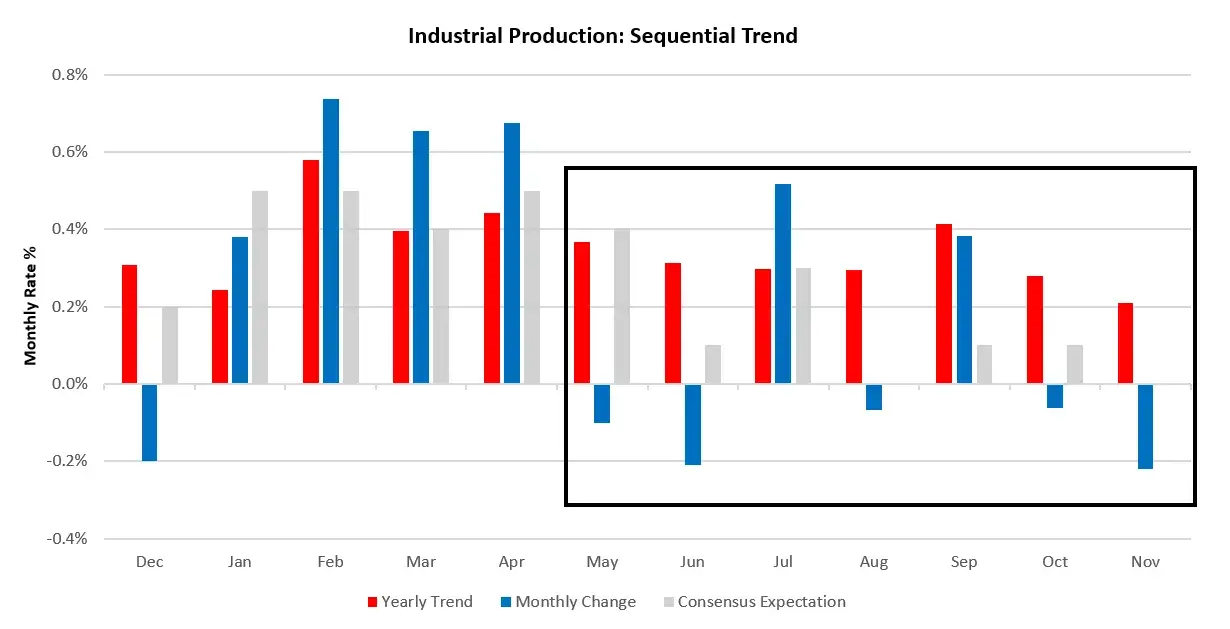

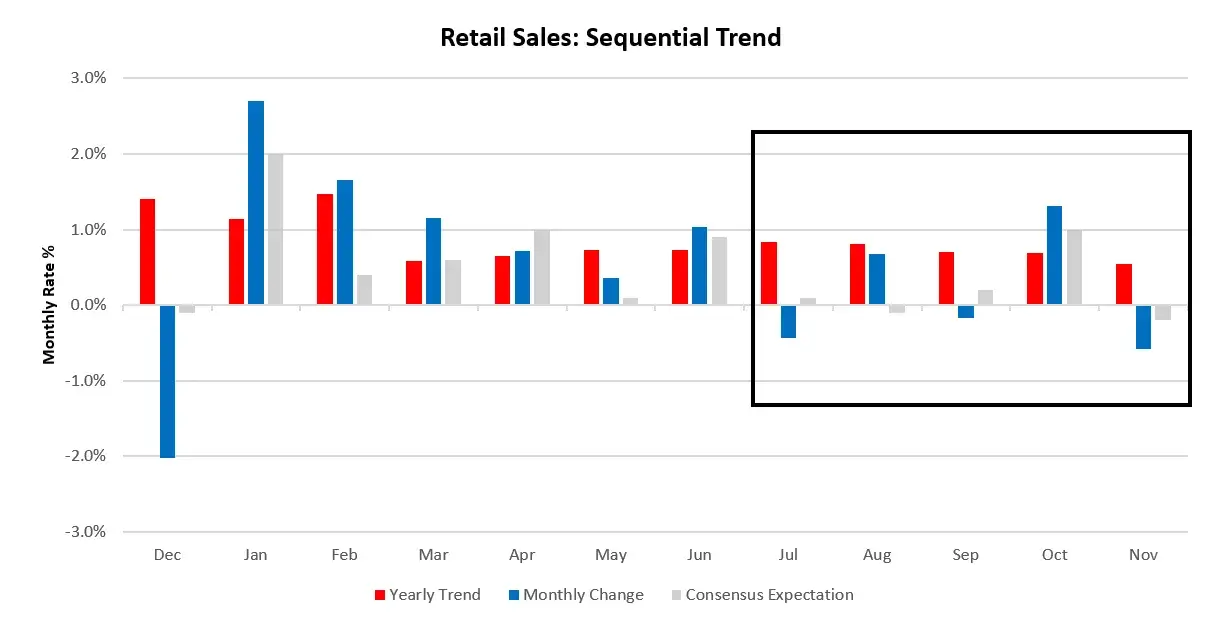

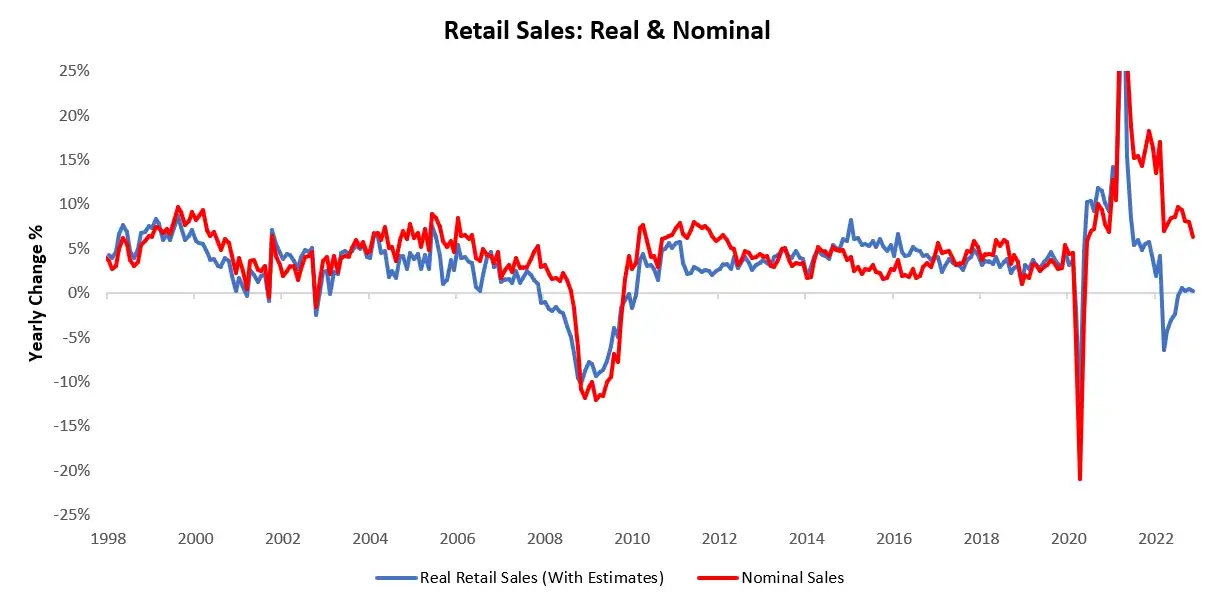

Incremental data this week have brought our tracking of economic conditions further in line with these future estimates. Both retail sales and industrial production showed contractionary prints this week. Below, we offer the sequential evolution of both, starting with industrial production:

As we can see above, the trend in production continues to weaken, and as base effects from earlier in the year fade, conditions are lining up for production to contract in 2023. Next, we show nominal retail sales:

Keep in mind, the sequential shown above are nominal, with real data significantly worse:

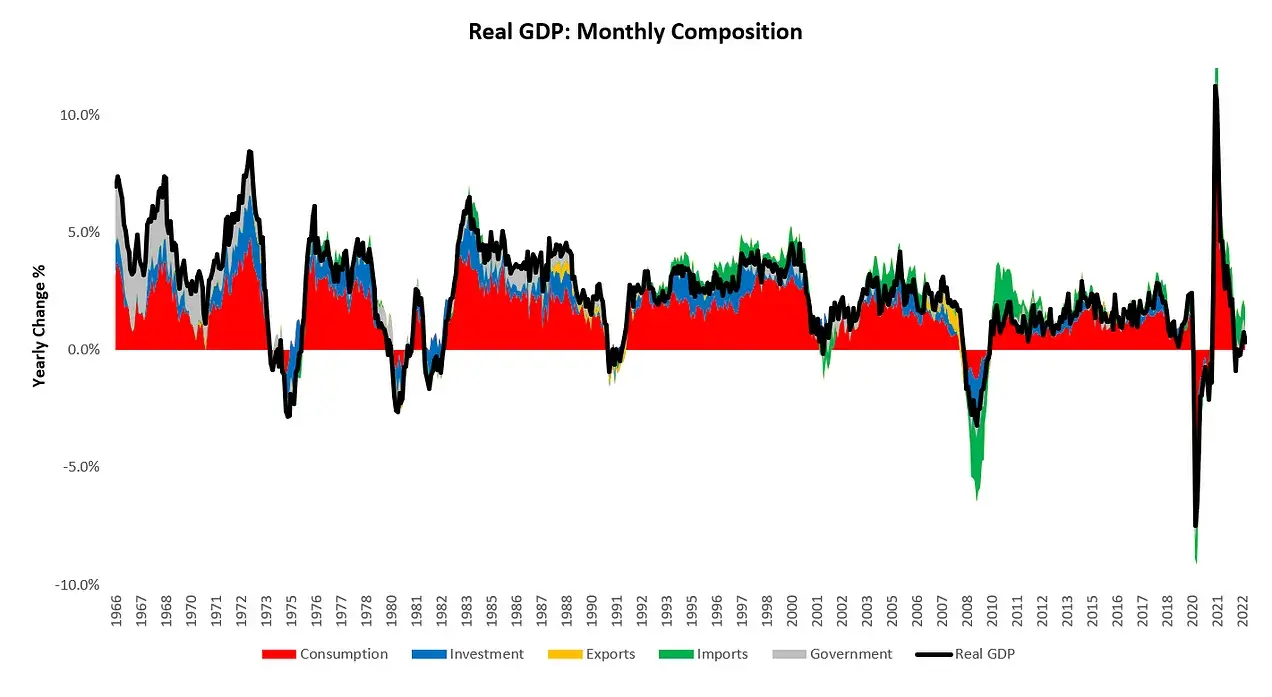

The combination of these factors leads our tracking of real GDP lower, now consistent with real GDP of 1% versus one year prior:

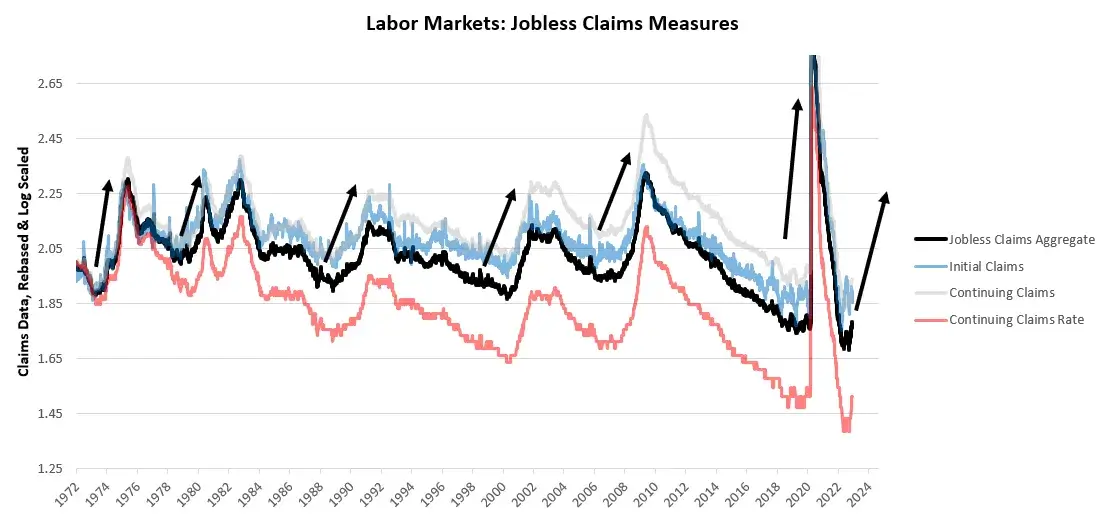

We remain on the path towards contractionary activity, with industrial production now conforming with our expectations alongside weaker consumption. Export activity will likely follow. Our attention now shifts toward the labor market, which remains the stronghold of economic output. The potential for volatility in the labor market has built over the year, and the potential for weaker employment is considerable.

We reiterate that the moves in the labor market tend to be nonlinear, with weakening labor markets moving at multiple times the speed and size of strengthening ones. We will continue to monitor these dynamics carefully as we progress through the cycle. We now turn to our positioning.

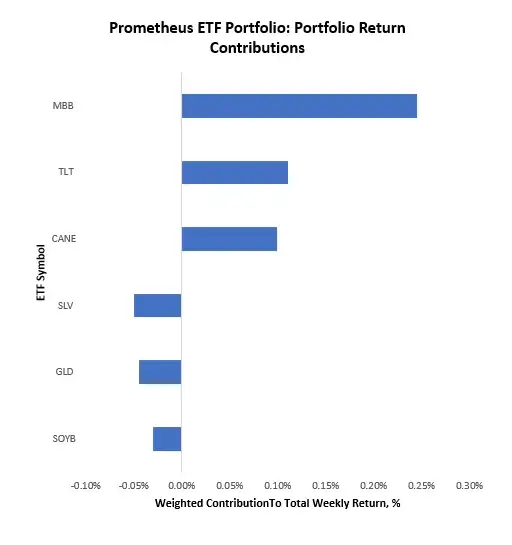

The Prometheus ETF Portfolio ended the week up 0.30%; we show the contributions to this return below:

The key takeaway from this week’s performance is the positive contribution of fixed income amidst a tough week for equity markets. As we mentioned in last week’s note, change is afoot in markets, and our systems have been ahead of the initial phases of this change thus far.

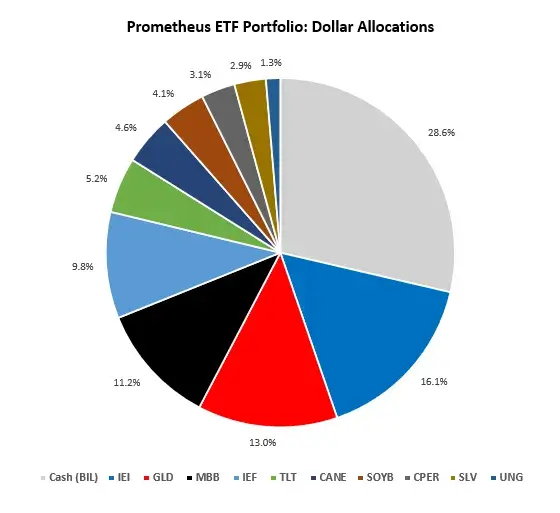

Turning to next week’s allocations, the Prometheus ETF Portfolio will be looking to position as follows:

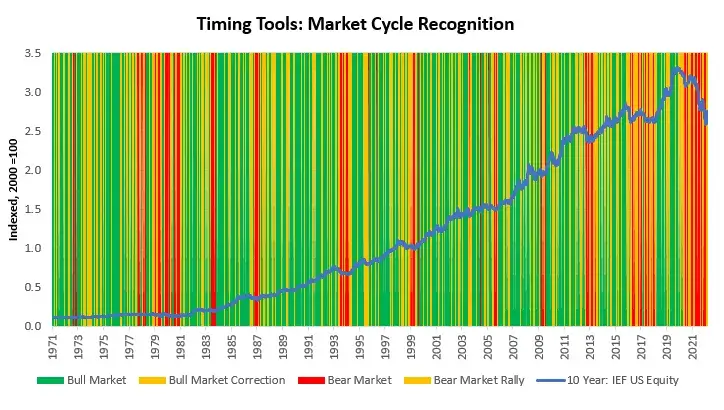

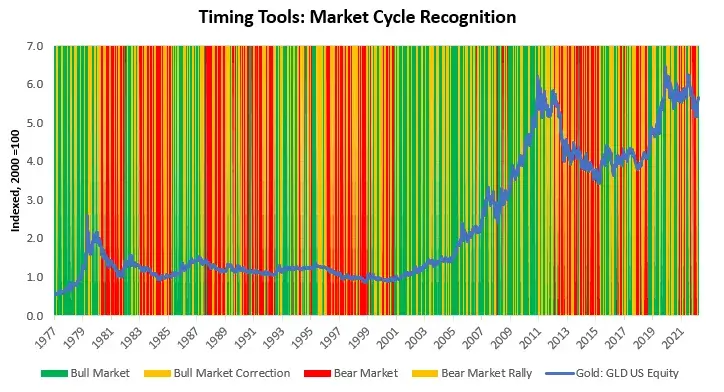

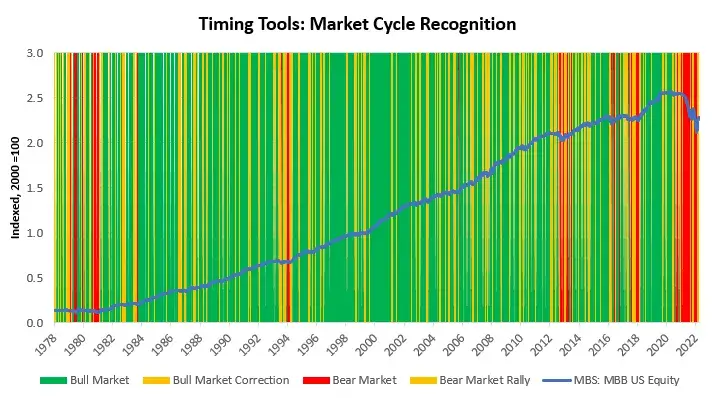

This allocation has an expected annualized volatility of 5.9% and a maximum volatility of 10%. The added diversity of bets creates conditions wherein maximum volatility is less likely to be achieved, allowing those who wish to add exposure the potential to do so. For additional color, we share some of our market timing tools to help contextualize the positions within the broader economic context.

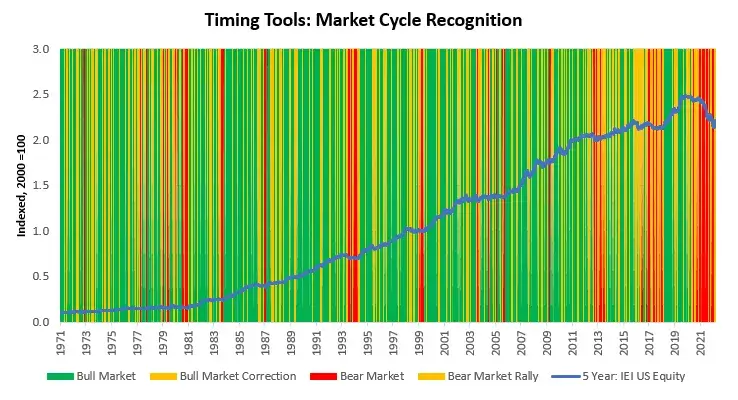

- IEI: 7-10 Year remains in a Bear Market Rally. Bear market rallies can initiate regime change, and current market pricing suggests beta capture opportunities.

- GLD: Gold has transitioned into a Bear Market Rally from a Bull Market. Bear market rallies can initiate regime change, and current market pricing suggests beta capture opportunities.

- MBB: MBS remains in a Bear Market Rally. Bear market rallies can initiate regime change, and current market pricing suggests beta capture opportunities.

- IEF: 5 Year remains in a Bear Market Rally. Bear market rallies can initiate regime change, and current market pricing suggests beta capture opportunities.

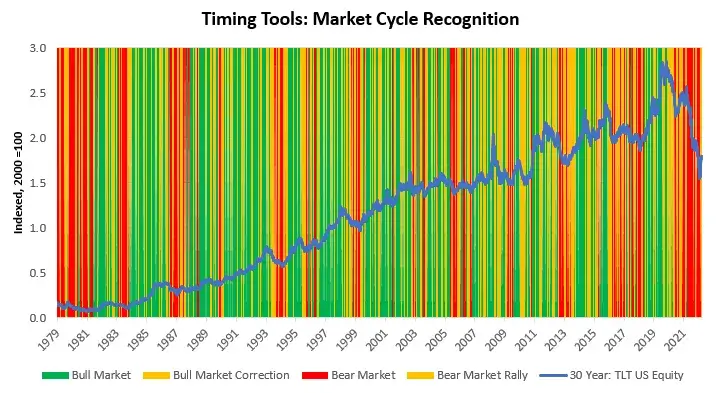

- TLT: 30 Year remains in a Bear Market Rally. Bear market rallies can initiate regime change, and current market pricing suggests beta capture opportunities.

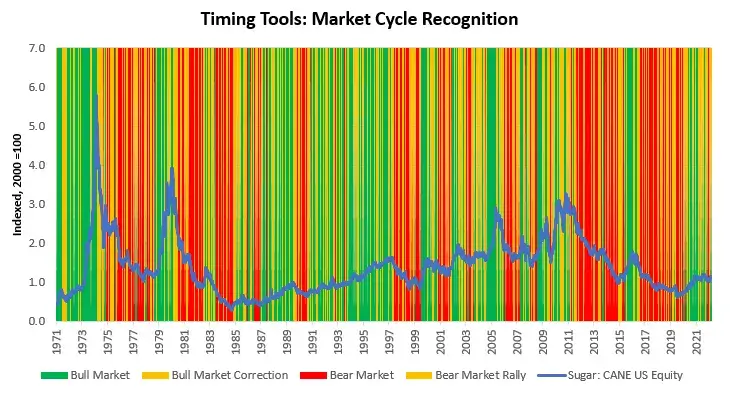

- CANE: Sugar remains in a Bull Market. Consistent with this, current market pricing suggests beta capture opportunities.

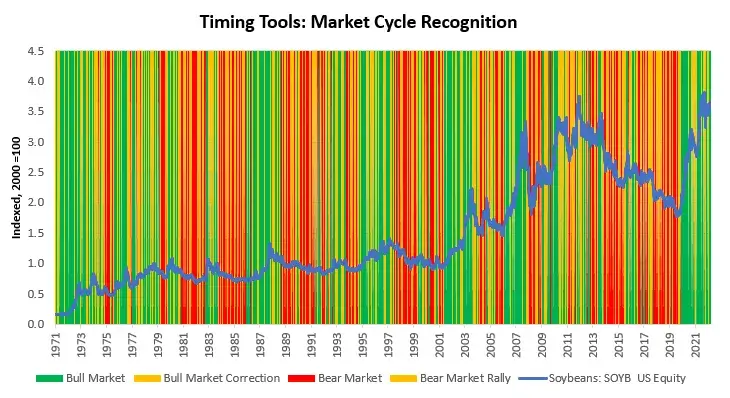

- SOYB: Soybeans remain in a Bull Market. Consistent with this, current market pricing suggests beta capture opportunities.

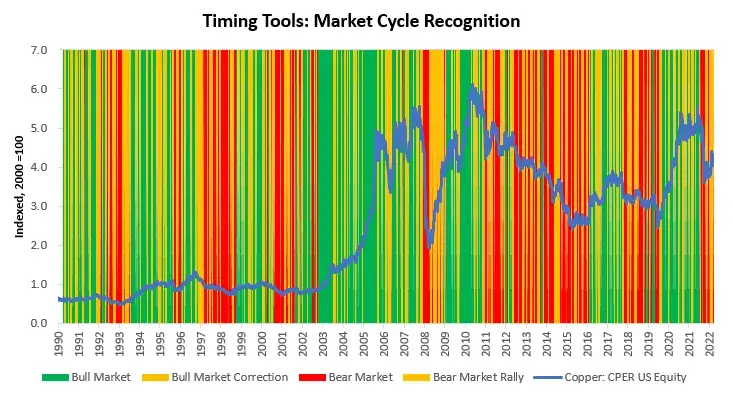

- CPER: Copper remains in a Bear Market Rally. Bear market rallies can initiate regime change, and current market pricing suggests beta capture opportunities.

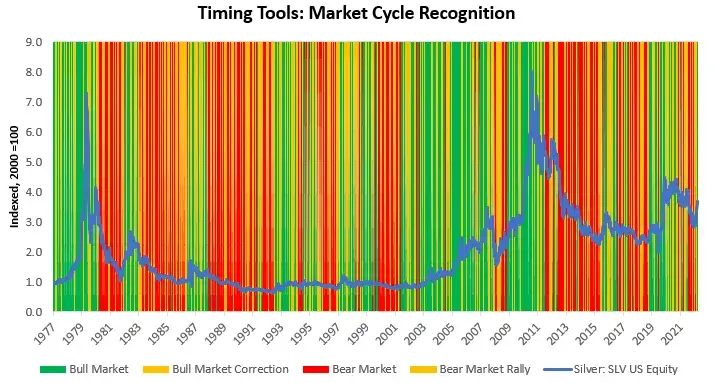

- SLV: Silver remains in a Bull Market. Consistent with this, current market pricing suggests beta capture opportunities.

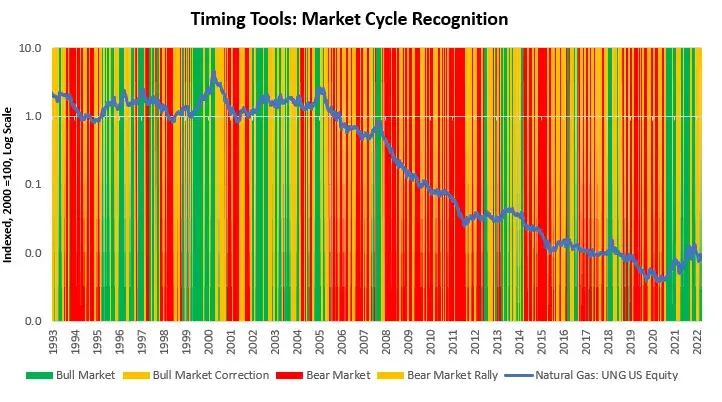

- UNG: Natural Gas has transitioned into a Bull Market Correction from a Bull Market.

Overall, market and macro conditions continue to tell us that we are at a point where future economic conditions could potentially evolve in a very different manner than they have in 2022. We must manage risk consistent with these conditions. Until next week.

They provide global solutions to local health challenges.

where can i buy lisinopril without a prescription

They simplify global healthcare.

The staff ensures a seamless experience every time.

where can i buy clomid tablets

The free blood pressure check is a nice touch.

The team always ensures that I understand my medication fully.

is gabapentin good for tooth pain

From greeting to checkout, always a pleasant experience.

Read here.

get clomid without dr prescription

Their commitment to international standards is evident.

They provide valuable advice on international drug interactions.

pregabalin and gabapentin combination therapy

Global reach with a touch of personal care.

Tamoxifen and clomiphene can be taken throughout cycles to prevent extreme estrogen ranges that can trigger gynecomastia.

Clomiphene, also referred to as Clomid, also doesn’t negatively

affect cholesterol levels (31). Elite feminine bodybuilders can take high

doses of 10–20 mg; nevertheless, such customers can expect to experience masculinization effects.

SERMs are able to restoring testosterone levels post-steroids,

with tamoxifen and clomiphene being the most effective options in our experience.

These unwanted side effects are instantly associated to the

water retention capabilities of Dianabol. There are additionally

very real well being dangers, together with elevated blood strain, elevated risk of cardiovascular problems, liver injury, gynecomastia, and hormonal imbalances.

This steroid is particularly in style for its ability to assist customers achieve speedy weight achieve, with some customers reporting positive aspects of as a lot as 25 lbs of muscle mass in as little as 4-6 weeks.

Taking much less Dbol dosage at night time might not trigger

any negative side effects, and you’ll be succesful of sleep while taking it.

For instance, in case your physician prescribed you 60 mg daily, break up the dosage into 24 hours, leaving 10 to twenty mg

earlier than bedtime. If you’re a first-time consumer,

you want to know that Dbol could be administered orally and intravenously.

Dianabol could be taken both; earlier than and

after a workout; nevertheless, it really works finest as

a pre-workout supplement. The men’s arteries got worse the

longer they used steroids, in accordance with the American Faculty of Cardiology analysis.

Nevertheless, Dianabol just must be used for 4 weeks

to begin exhibiting effects. It’s additionally

potential that taking less Dbol at night won’t have any antagonistic effects, and

you’ll have the flexibility to sleep while

doing so.

Throughout this ’60s/70s period, bodybuilders might

merely go to their medical doctors and ask for Dianabol (and different steroids) to

get greater and stronger, and their request can be granted.

Steroids’ antagonistic effects were not well-known, and so they had been 100% legal.

If you would possibly be nonetheless on the lookout for something to use that will help you enhance lean muscle mass,

you can hop over to CrazyBulk and order a bottle of D-Bal.

Nonetheless, it’s essential to focus on the potential downside of steroid use before making the

choice to make use of them. Dianabol significantly boosts

protein synthesis, which is the process that helps muscular tissues

restore and develop after intense exercise. This improve in protein synthesis leads

to faster muscle development and allows users to coach with shorter restoration occasions between periods, attaining faster outcomes than training

alone. Bodybuilders like Lou Ferrigno and Arnold Schwarzenegger showed what

Dianabol can do within the ’60s and ’70s.

Such cycles are typically performed by bodybuilders seeking to add

massive quantities of hypertrophy. Such dosages can be thought

of deleterious and high-risk based on our expertise.

It’s as a end result of anabolic steroids are

an artificial version of testosterone, and their use raises testosterone levels, leading to enhanced

muscle mass and power. Dianabol can convert to estrogen in the

body, which can cause gynecomastia (enlargement of breast tissue in men) and water retention. These estrogenic

effects can result in a bloated appearance and probably enhance blood pressure.

He achieved this with Dianabol’s androgenic rating of 60,

compared to testosterone’s one hundred. Dr. Ziegler famous that the Russian athletes

were experiencing androgenic unwanted effects in the course of the 1956 Olympics (in Australia) when he

discovered they have been experiencing issue urinating.

This was due to enlarged prostates attributable to the

excessive conversion from testosterone to DHT. All oral steroids must be taken away from meals as food can decrease the bioavailability of oral Steroids.

Due to a few of these effects, I’d suggest making an attempt Dbal, which is a pure

and effective various that comes with none unwanted

side effects.

In some instances, cystic acne can appear to resemble the scale of a

golf ball underneath the pores and skin (although this is uncommon).

Dianabol users can even experience low libido, decreased well-being,

despair, decrease ranges of vitality, and erectile dysfunction when testosterone levels

plummet. Being an oral steroid, Dianabol will trigger C17-alpha

alkylation, which is a modification to the 17th carbon position.

Sustaining correct hydration and a heart-healthy food regimen might help mitigate these cardiovascular unwanted effects.

As the popularity of Dianabol continues to develop, so does the curiosity in understanding the earlier than and after outcomes of its use.

Many individuals want to see real-world examples and testimonials from those who have skilled the advantages and

downsides of incorporating this powerful steroid

into their fitness routine.

Thus, gynecomastia and water retention (bloating) are much

less more doubtless to happen with the addition of Proviron. Deca Durabolin can be

significantly less androgenic in comparability with Dianabol, that means ladies are less more doubtless to experience virilization unwanted effects on Deca in low doses compared to Dianabol.

IFBB bodybuilders, when competing, are sometimes seen to possess low ranges of

subcutaneous fat however high ranges of visceral fat (due to extreme

steroid use). Nevertheless, 6 months later, when the

mice have been subjected to power coaching (this time without steroids),

they grew by 30% in comparability with a control group that didn’t

develop significantly.

He, like many others, skilled significant muscle-building and bulking results from this

powerful oral anabolic steroid. The steroid works by enhancing how the physique processes protein and retains nitrogen. Dianabol in high doses might significantly compromise a user’s

health, notably in regard to ldl cholesterol and liver values.

natural steroid supplements

Artificial steroids, however, include each medical and performance-enhancing

makes use of. Corticosteroids, such as prednisone, are prescribed to manage irritation and immune issues.

Anabolic steroids, artificial versions of testosterone, have been misused by athletes and bodybuilders for muscle development.

Pure steroids, typically misunderstood and generally

confused with their synthetic counterparts, play essential

roles in sustaining our health and well-being.

In contrast to artificial steroids, which can result in adverse

unwanted effects, pure steroids are natural substances that our

our bodies naturally produce. These compounds are primarily synthesized throughout the adrenal glands, gonads, and liver.

Oral anabolic steroids are synthetic derivatives of testosterone designed

to be taken by mouth.

To optimize benefits, corticosteroids are prescribed at the

absolute best dose within the shortest period of time for you and your vitality to accomplish the perfect potential results.

For athletes, rising muscle mass may promote power, which may enhance strength-based sports activities performance.

Anabolic steroids (artificial androgens) work by activating androgen receptors in your body and mimicking the

results of natural androgens. Healthcare providers present corticosteroids rather

more often than anabolic steroids. Anabolic steroids are manufactured medicine that closely

resemble the hormone testosterone or different androgens.

Steroids are man-made chemicals to simulate the impression of sure hormones that exist within the human physique.

Steroids are a number of sorts and serve totally different purposes in medical and

non-medical settings.

HGH continues to impression our our bodies throughout maturity, influencing muscle mass, body fats

distribution, and even energy levels. You can study extra about tips on how to enhance HGH naturally through life-style changes

and other strategies. For specific information about HGH, WebMD provides a comprehensive useful resource.

It could seem that they can not have any use in sports,

as they weaken muscular tissues and bones, cut back immunity (most results are almost opposite of anabolic steroids).

They are used in shorter cycles to beat irritation and ache associated to coaching, and thus may assist prepare better.

Nonetheless, on the planet of performance-enhancing drugs, the word “Steroid”

is used to explain anabolic and androgenic steroids (AASs).

In this case, our patient’s physique temperature increases by

approximately 1 diploma. We find that fat loss ceases

roughly 4-6 weeks right into a cycle when the body inevitably reaches homeostasis and cools

down. This is why bodybuilders sometimes cycle clenbuterol for short durations, with transient protocols of two

weeks on and a couple of weeks off for maximum efficacy.

Deca Durabolin is never administered by itself, because it reduces androgenicity, potentially inflicting sexual unwanted facet effects,

together with impotence (erectile dysfunction). Due To This Fact,

it is usually stacked with Anadrol, testosterone, or trenbolone.

Edema (swelling) is a common facet impact as a result of testosterone increasing aromatization (the conversion of testosterone to estrogen).

Throughout this course of, estrogen ranges

rise, causing water retention in users.

Steroids are a category of compounds that all have a similar construction and bind to hormone

receptors within the body. Anabolic steroids bind to the androgen receptors, whereas corticosteroids bind to

the glucocorticoid receptors – leading to totally different effects on the physique.

When it comes to steroids, nonetheless, that description is simply one piece of the equation. There are actually multiple classes

of steroids, together with anabolic steroids and corticosteroids,

which have totally different uses, unwanted effects, and performance-enhancing qualities.

If used correctly and based on the indicated scientific guidelines they can be used for

the treatment of various conditions e.g., hypogonadism (anabolic

steroids) and asthma (corticosteroids).

Nonetheless, such reductions are sometimes delicate in contrast

to other anabolic steroids. Winstrol’s results are similar to Anavar’s, permitting customers to scale back fat

mass while including moderate quantities of muscle tissue.

The following is a complete listing of extra anabolic

steroid cycles that simultaneously promote muscle hypertrophy and enhance

fats burning. Deca Durabolin’s weak androgenic nature,

when combined with high prolactin levels,

can contribute to cases of erectile dysfunction. When androgen ranges are insufficient, nitric

oxide (NO) concentrations decrease. Enough NO manufacturing is important for the provision of blood to the penile

tissue. This stack was believed to be one of the most outstanding steroid cycles from the Golden Era, thought to have been utilized by Arnold Schwarzenegger and different basic bodybuilders from the 1970s.

Moreover, their use in sports can lead to disqualification and authorized penalties.

The legality and ethics surrounding artificial steroids can differ widely from one nation to

a different and from one sport to another. When most athletes

run oral steroids, their focus is almost entirely on liver protection — and for good purpose.

Injectable steroids sometimes use long esters (e.g., Testosterone

Enanthate, Nandrolone Decanoate, Boldenone Undecylenate) which can stay lively within the system for 2–4 weeks post-injection.

Estrogen will increase sodium retention, and the anabolic results mess with protein synthesis in a method that encourages fluid buildup.

Both NPP and Deca deliver nandrolone, so their anabolic effects

match up. You’ll see related muscle protein synthesis and nitrogen retention from both

one. In terms of pure muscle tissue being constructed, trenbolone

can rival any bulking steroid. However, as a result of

it doesn’t cause extreme weight gain due to water loss and fats loss, it takes the 4th spot.

Oral steroids stimulate hepatic lipase within the liver, further

reducing high-density lipoprotein (HDL) cholesterol and thus exacerbating blood strain. The aromatizing nature of Dianabol also causes

water retention, which increases blood viscosity, lowering circulation to the guts.