Slowing Nominal Activity: Long Stocks & Bonds

Welcome to our official publication of the Prometheus ETF Portfolio. The Prometheus ETF portfolio systematically combines our knowledge of macro & markets to create an active portfolio that aims to offer high risk-adjusted returns, durable performance, & low drawdowns. Given its systematic nature, we have tested the Prometheus ETF Portfolio through decades of history and have shown its durability. For those of you who are unacquainted with our systematic process, we offer a detailed explanation here:

In this publication, we will discuss the performance, positioning, & risks of the Prometheus ETF Portfolio and it will be published every week on Fridays to help investors understand how our systematic process is navigating through markets. Before diving into our ETF Portfolio positions, we think it is important for subscribers to understand the context within which our systems choose their exposures. Below, we offer our latest Month In Macro note, which contains the conceptual underpinnings of our systematic process within the context of the latest economic data:

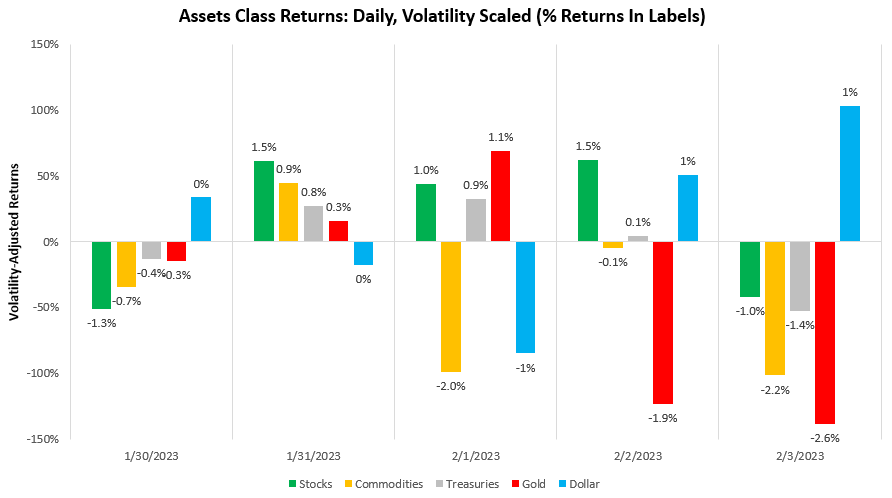

We highly recommend you get acquainted with our outlook to understand best our systematic positioning outlined in this note. We will keep today’s note brief as we wish to allow you to focus on the outlook provided in Month In Macro. This week saw markets move roughly in line with our expected disinflation theme. Stock and bonds showed decent performance:

This performance is consistent with the most recent market pricing of falling inflation. We show this below:

The biggest shock to this market pricing occurred on Friday in the form of the nonfarm-payrolls report, which showed significant strength. Markets moved to price this as a need for incremental tightening from the Fed, causing a sell-off across assets. However, looking under the hood of this report, we don’t see signs that will meaningfully counteract our expectations of a slowdown. We briefly explain our thoughts.

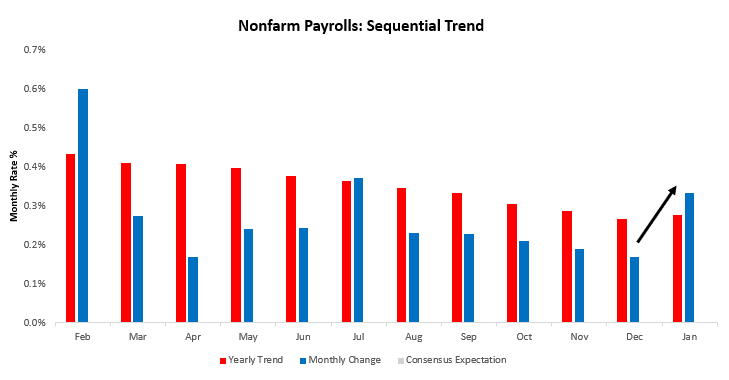

Nonfarm Payrolls increased 0.45% in January, surprising consensus expectations of 0.12%. This print contributed to a sequential deceleration in the quarterly trend relative to the yearly trend. Below, we show the monthly evolution of the data relative to its 12-monthly trend and consensus expectations:

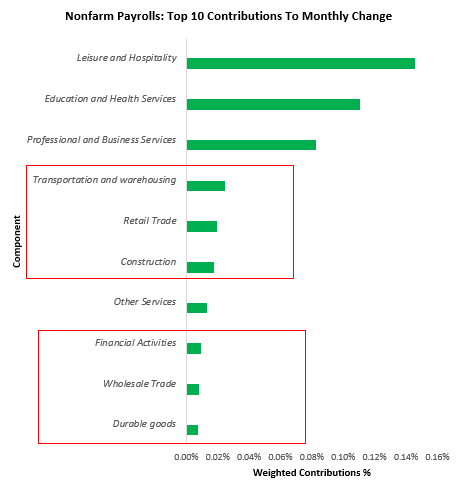

This strength was driven by non-cyclical components of employment, i.e., components that do not contract even during recessions. When we look at the cyclical components of employment, they we all weak contributors to this report:

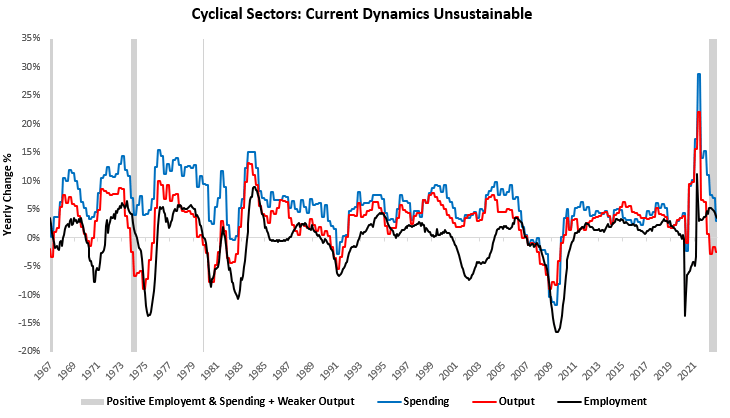

Employment in cyclical areas remains at odds with the output of these areas. In fact, this recent print was a further sequential slowing in both quarterly and yearly trends for employment in these sectors. We continue to expect this imbalance to correct itself through lower employment, which begins with a deceleration before a contraction.

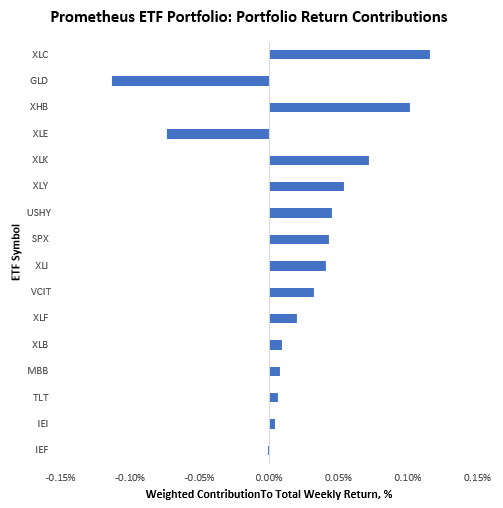

For more detail on these dynamics, please refer to our Month In Macro report above. Overall, we remain on a path toward a disinflationary nominal growth slowdown. Within this context, the Prometheus ETF Portfolio performed admirably, netting a 0.40% gain this week. We show the composition of these gains below:

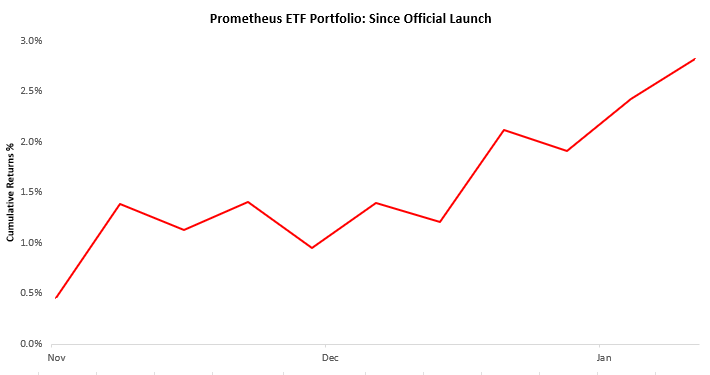

Recent performance has been strong, with solid risk-adjusted returns, and we showcase the cumulative returns since our official launch last year:

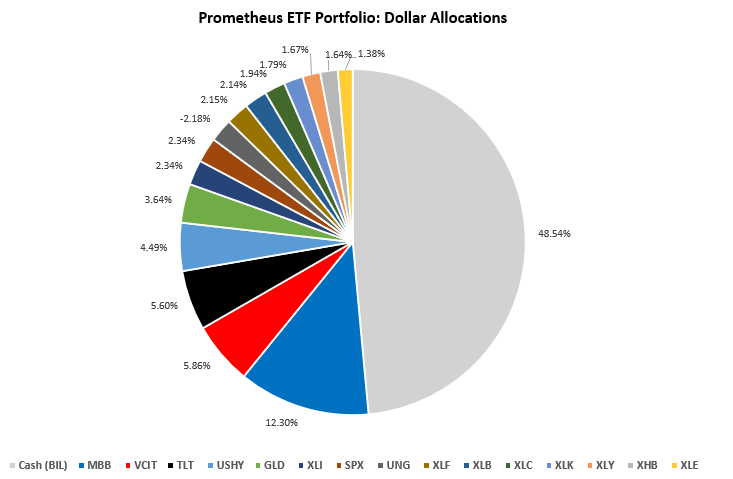

Turning to next week, our systems are looking to position as follows:

Positions: Cash (BIL): 48.54% MBB : 12.3% VCIT: 5.86% TLT : 5.6% USHY: 4.49% GLD : 3.64% XLI : 2.34% SPX : 2.34% UNG : -2.18% XLF : 2.15% XLB : 2.14% XLC : 1.94% XLK : 1.79% XLY : 1.67% XHB : 1.64% XLE : 1.38%

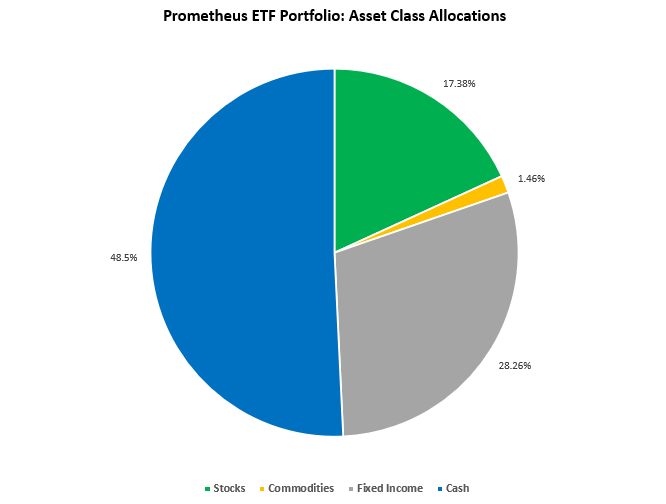

At the asset class level:

This portfolio allocation has an expected volatility of 6.8% and a maximum expected volatility of 10%. We see next week as a relatively low risk in terms of achieving maximum volatility, largely due to the lack of growth, inflation, or liquidity catalysts. The primary risk to these positions will emerge the week after next as we head into CPI. We will be watching carefully to assess risks heading into the event. Overall, we remain on a path where nominal activity slows, with real activity likely to contract and inflation likely to compress. Markets are pricing these forces and will continue to do so until the volatility of real growth outshines that of inflation. Until next time.

I’m really impressed with your writing talents as well as with the layout in your blog.

Is that this a paid subject matter or did you customize it your self?

Anyway keep up the nice quality writing, it is rare to see

a great blog like this one nowadays. Fiverr Affiliate!