At Prometheus, innovation has been the cornerstone of our evolution, and we’re constantly pushing forward our understanding of macroeconomic dynamics to further our edge in markets. A key driver of this evolution is our iterative research process, where we try to systematize our ongoing understanding of macro conditions into investment strategies. Keeping with this process over the last year has allowed us to improve our process substantially and create our next generation of programs: Alpha Strategies. Alpha Strategies reflects the best parts of our understanding of macro, markets, and portfolio construction. The purpose of Alpha Strategies is simple: to provide durable and consistent return streams independent of beta. These strategies will span equities, fixed income, and commodities, which will be released individually over the next few months. Eventually, we will combine these into a single strategy, which will be accessible to subscribers in a similar format to our ETF Portfolio. For now, this will only be available to our Prometheus Bespoke clients. In the future, we may make this available as a standalone product.

If you’re interested in access to Bespoke & Alpha Strategies, please get in touch by emailing info@prometheus-research.com.

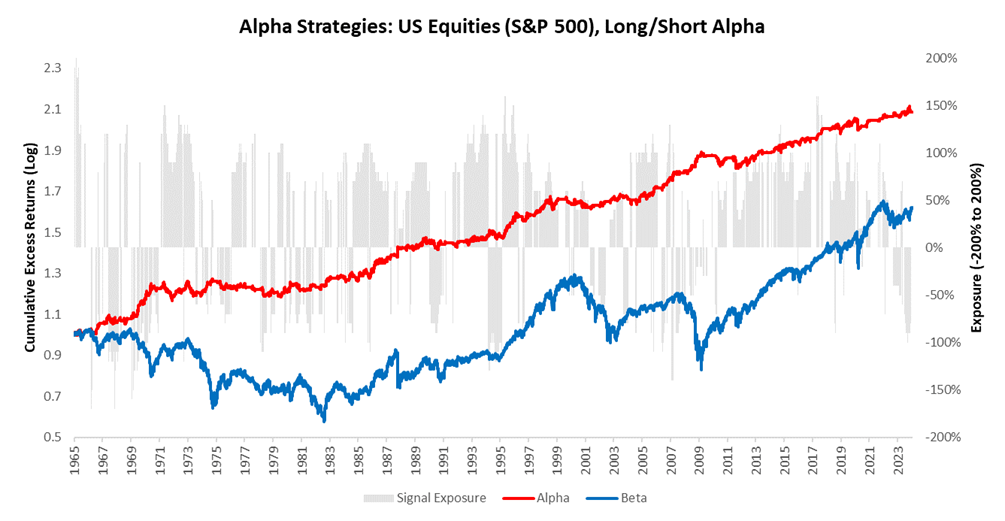

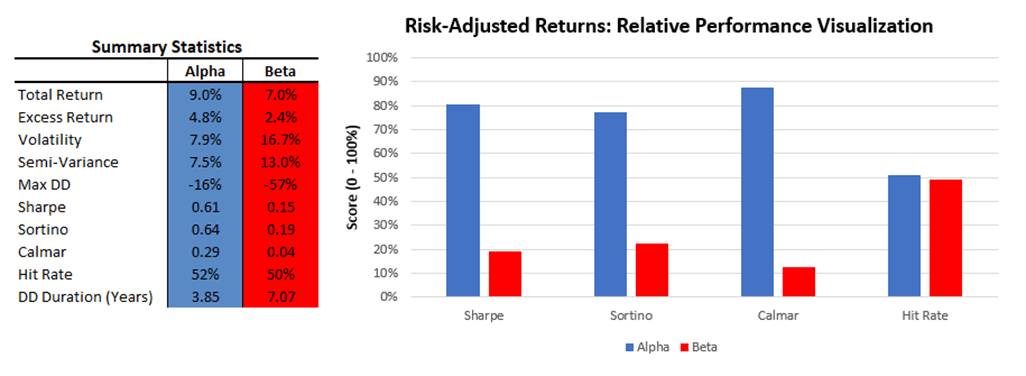

Today, we kick things off with our Alpha Strategy for US Equities (S&P 500). We begin with the high-level performance statistics:

As we can see, our Alpha Strategy has largely outperformed beta exposure in terms of providing a smooth return path over time, as evidenced by the cumulative excess return path. Furthermore, the Alpha Strategy outperforms beta exposure across measures of risk-adjusted returns, with higher returns and lower risk across measures. While the outperformance of this strategy is evident from these statistics, we think it is important to recognize that the objective of alpha is not to outperform beta but rather to add value to beta in an uncorrelated fashion. Thus, while we display our Alpha Strategy relative to its underlying beta, outperforming this beta is not an explicit objective but a welcome outcome. Alpha is always scarce in markets, and adding alpha to any return stream is additive to the portfolio. Our approach seeks to generate macro alpha, i.e., alpha that stems from correctly identifying future economic conditions relative to what markets have currently priced.

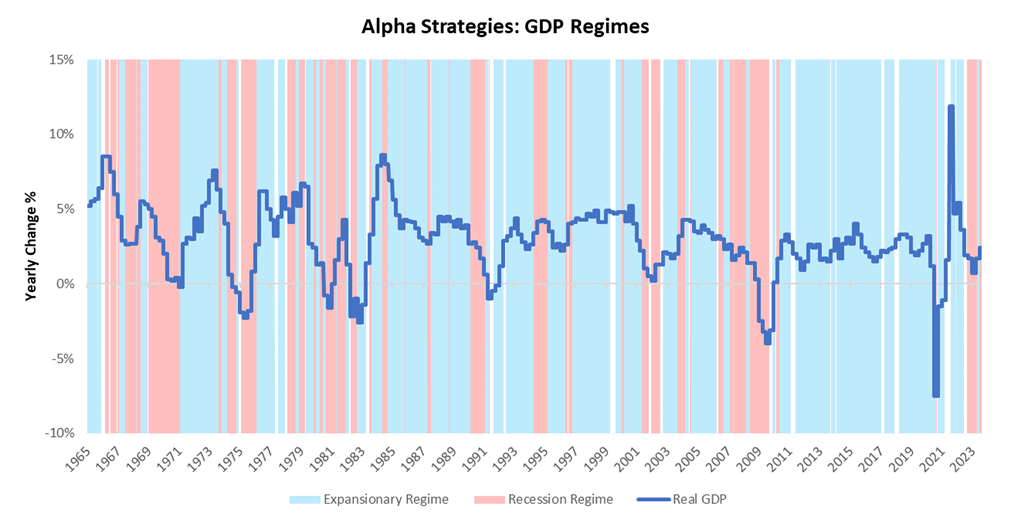

In the case of US Equities, this requires having a view of the business cycle. The single most significant driver of equity market returns over long periods is the level and change of real GDP growth. Using a vast array of economic data, we can estimate expected regimes for the economy. We visualize this high-level regime recognition below:

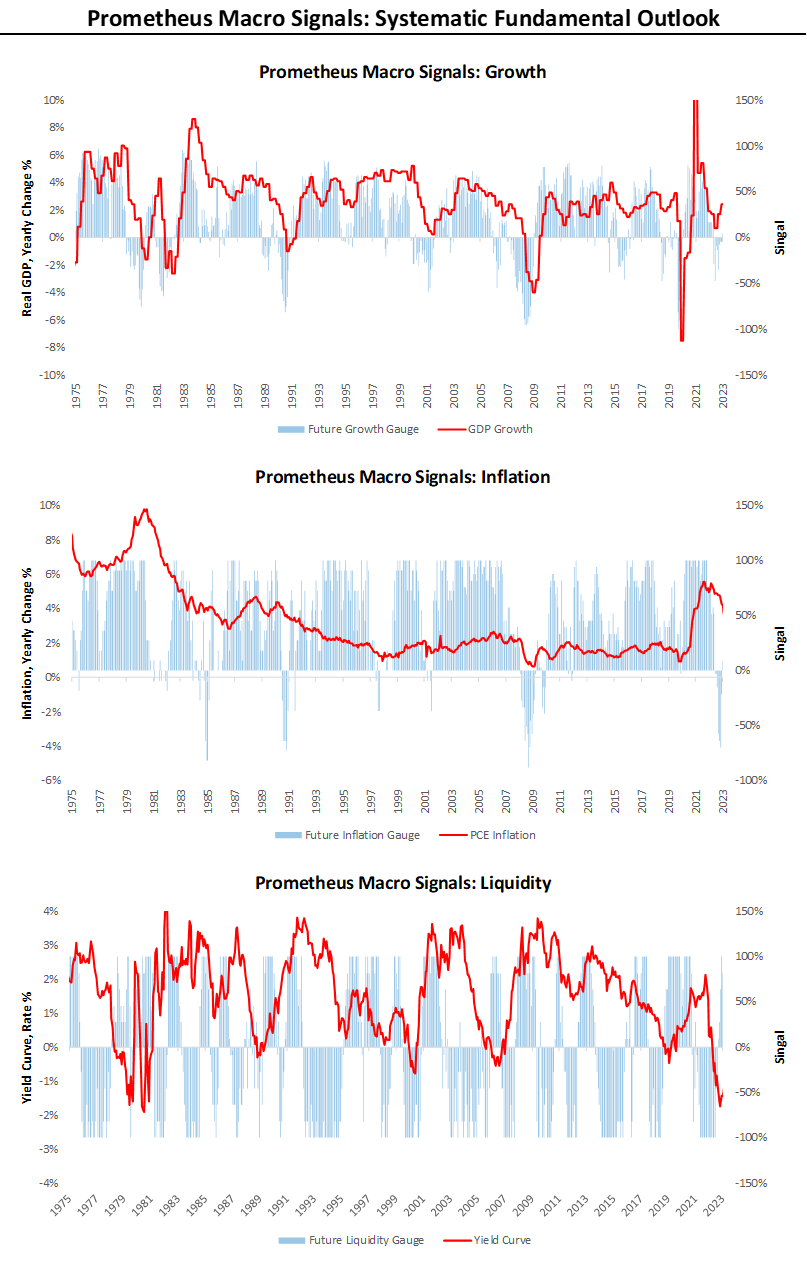

As shown above, our systematic regime recognition process has generally proven adept in spotting turning points and cascades in GDP regimes. This regime recognition stems from our comprehensive tracking of macroeconomic conditions, detailed in the thousands of pages of research we have shared in our Month In Macro and The Observatory. While we do not share the specifics of our signal construction to protect our edge in markets, we will continue to share the intuitions and frameworks driving our systematic assessment of future economic conditions. Below, we show some of the high-level factors that drive our systems’ assessment of where we are in the economic cycle:

This broad-based assessment of macro conditions allows our strategies to be wary of macroeconomic risks to equities, creating the potential for us to profit from declines in equity prices that markets may not have priced in. Conversely, when asset prices are weak, but fundamentals point to a strong environment ahead, our strategies can find significant value in being long equities. The strategy will likely run limited exposure during periods where mispricings are limited.

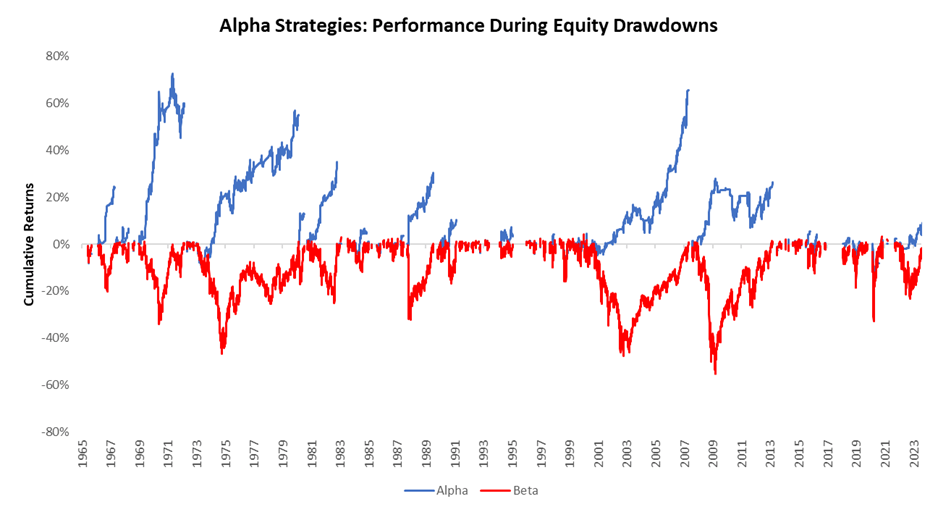

As shown above, our systems avoid large drawdowns in equities while participating in rebounds. We visualize the outperformance during beta drawdowns below, where we visualize cumulative strategy performance during beta drawdowns of greater than 5%:

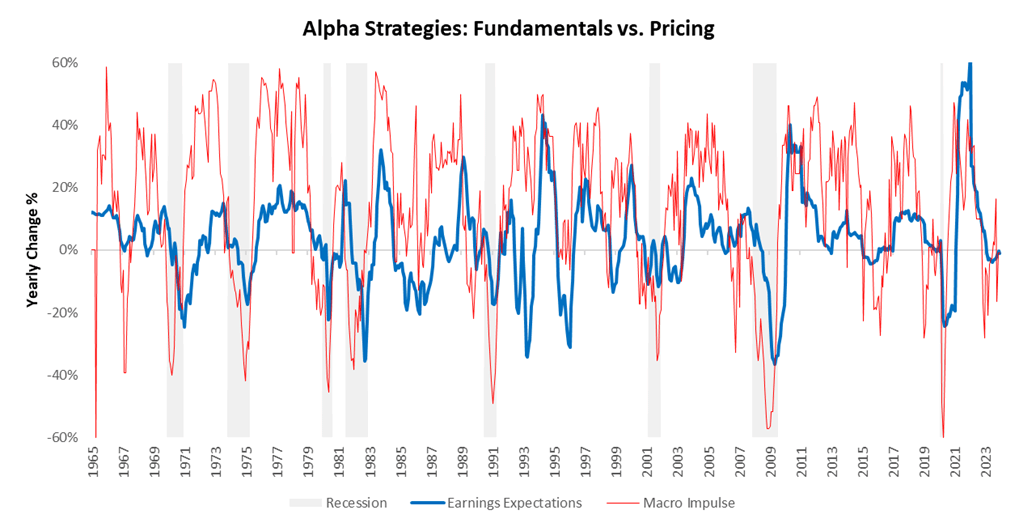

As we can see above, our Alpha Strategy recognizes potential downside risk in equity markets and seeks to preserve and potentially even compound capital during these downturns. An essential part of this process is understanding not just the potential path of the economy but how probable that is relative to what is priced in by asset markets. We do this by assessing both fundamental dynamics:

And market-implied pricing of conditions:

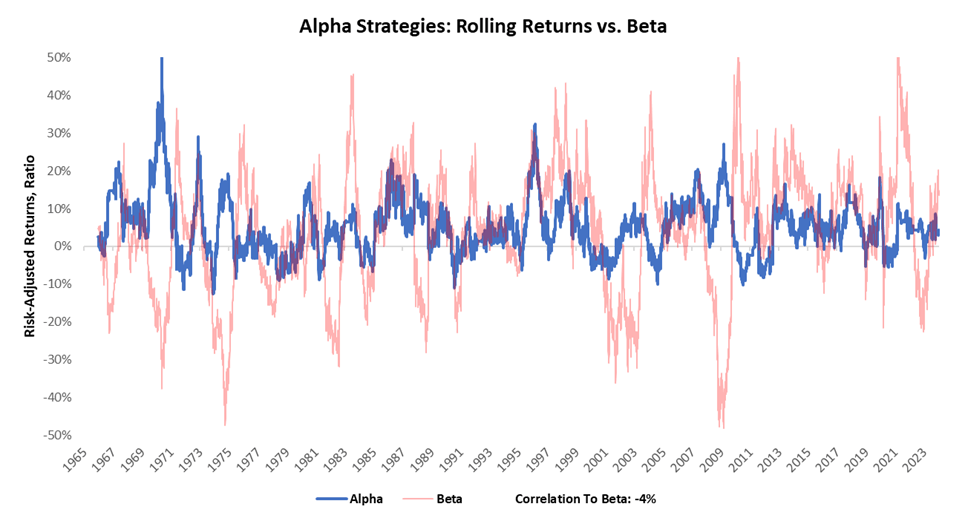

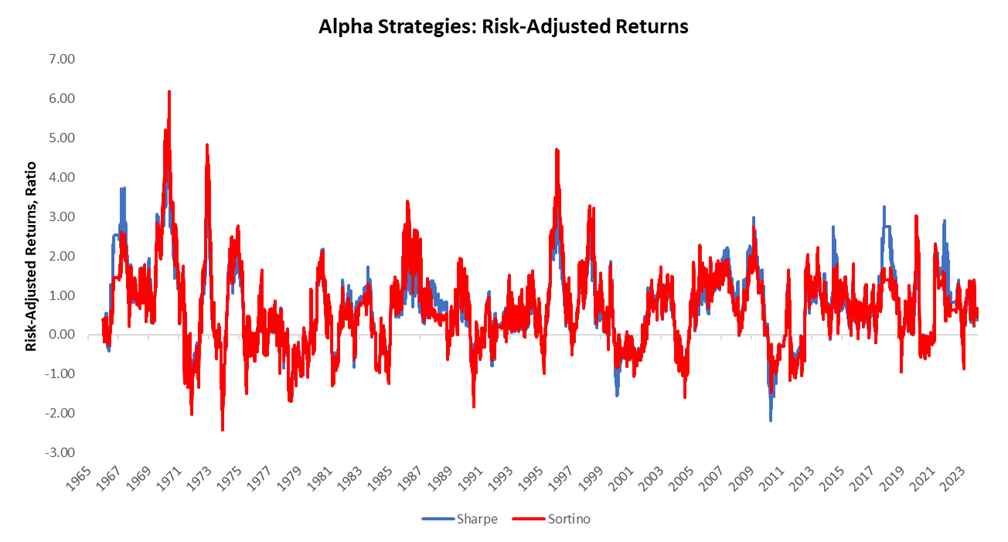

Combining a very modest edge in assessing forward-looking macro conditions and an assessment of market pricing of those allows us to take on bets that offer a better risk-reward profile. We see this in our assessment of rolling risk-adjusted returns, with rolling Sharpe (0.61) and Sortino (0.64) ratios in positive territory on average, with positive skew:

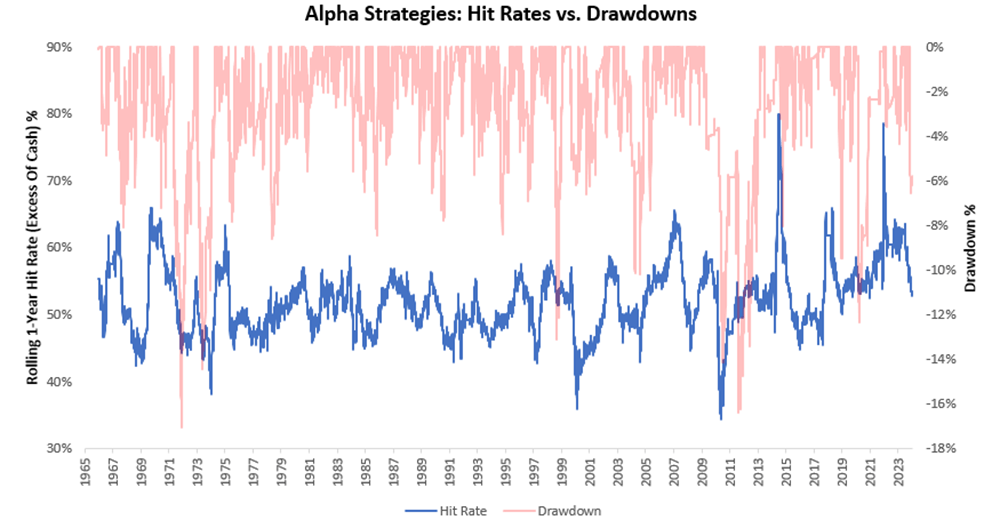

These positive risk-adjusted returns come as a function of a modest edge in hit rates, with an average daily hit rate of 52%:

Now, while a daily hit rate of 52% represents a modest edge, the cumulative effect of this edge over long periods with a modest skew can contribute to significant cumulative return impacts. Creating the conditions for this compounding to occur requires a considerable focus on drawdown control.

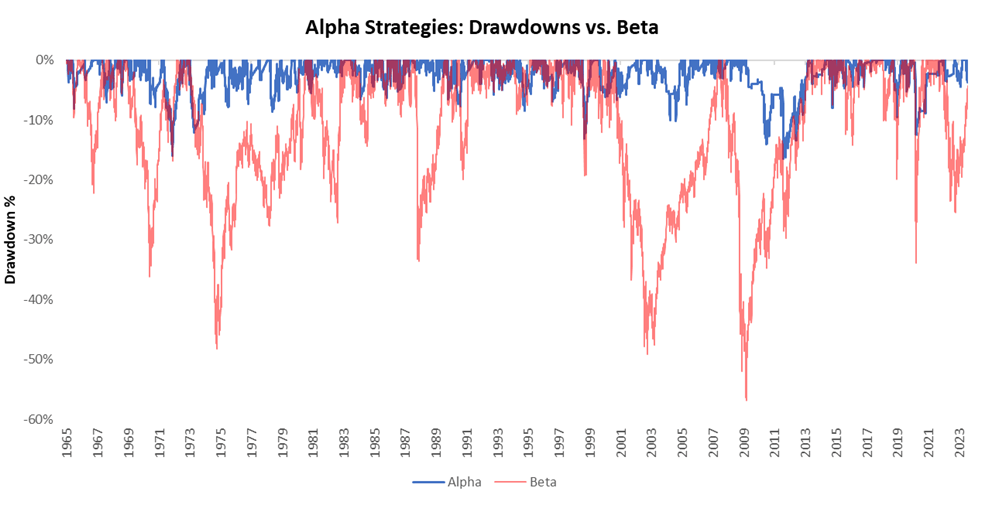

Below, we show the drawdowns for our Alpha Strategy versus Beta:

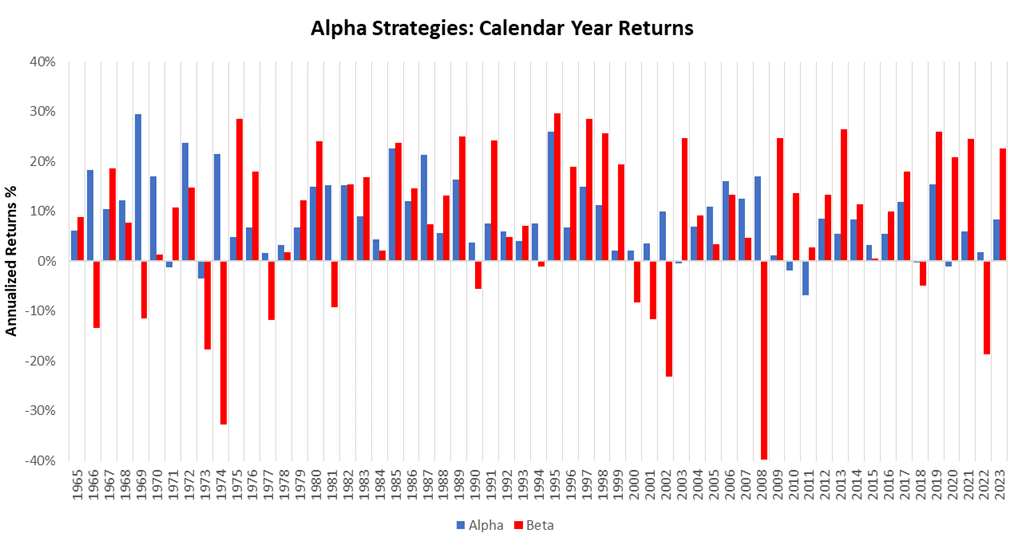

As shown above, our Alpha Strategies has shown limited drawdowns over our simulation history, with a maximum drawdown of 16%. Importantly, our strategy has maintained this limited drawdown profile despite facing hit rates as low as 30% (i.e., 70% offside trades in a year). This drawdown profile has allowed our simulated strategy to show strong calendar year performance, with only six down years since 1965:

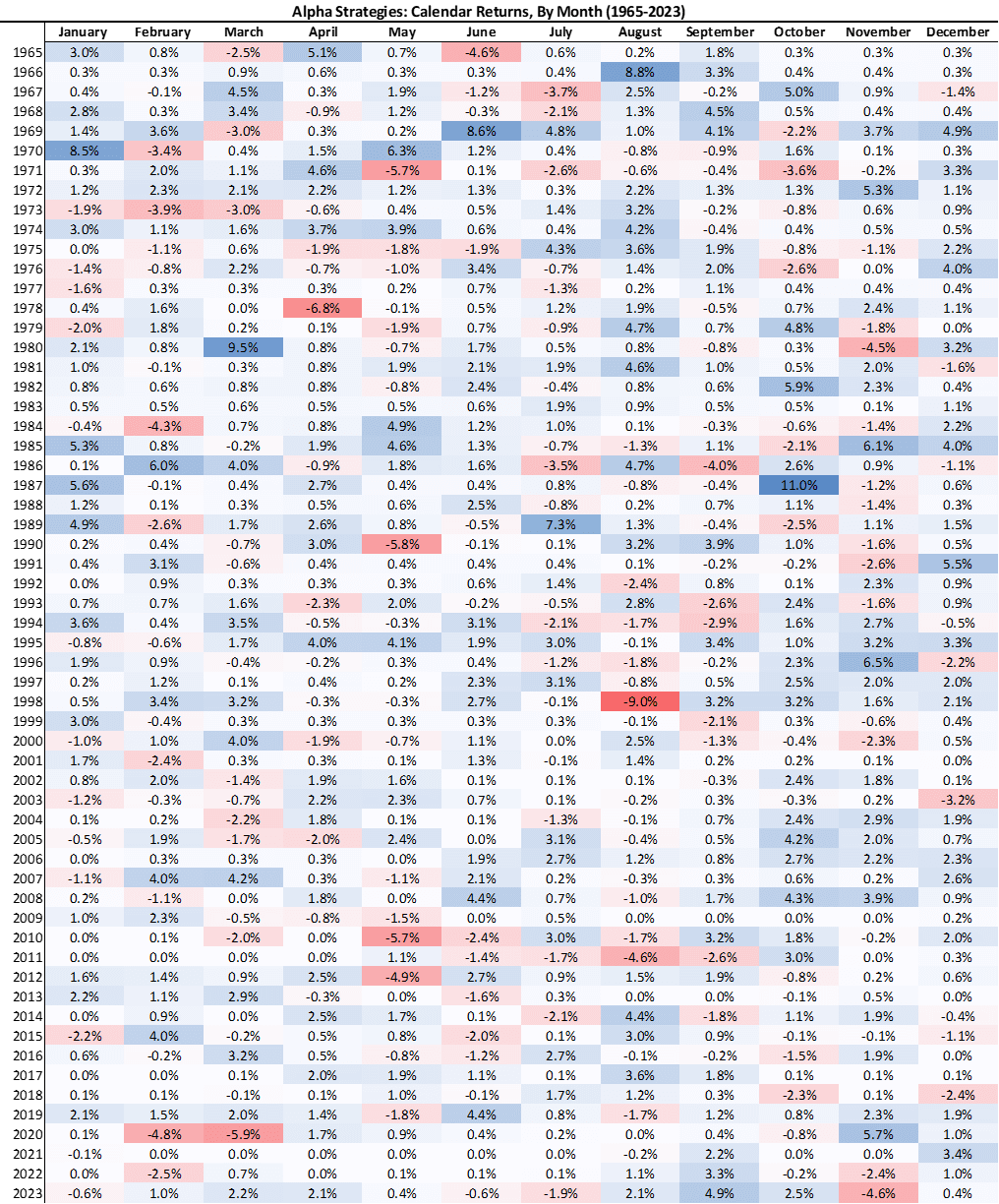

Below, we offer the calendar mean returns by month for those wishing for some more texture:

As we can see, the strategy has experienced various conditions and shown durable performance.

As we mentioned at the onset of this note, these strategies aim not to outperform passive beta but to provide uncorrelated alpha. Consistent with this objective, we have thus far shown S&P 500 beta excluding dividends. The purpose of excluding dividends is that our Alpha Strategy aims to predict asset price returns over cash, with dividends simply reflecting a near-constant drift factor within the total returns of an asset. Therefore, we exclude dividends from our alpha and beta simulations for the purest evaluation of alpha. This exclusion does not mean we ignore dividends but recognize that they are not part of the evaluation of an alpha seeking to predict prices. This nuance does not take away from the value-addition from our signal, and we show how we can create outperformance relative to a passive benchmark with dividend reinvestment using our approach.

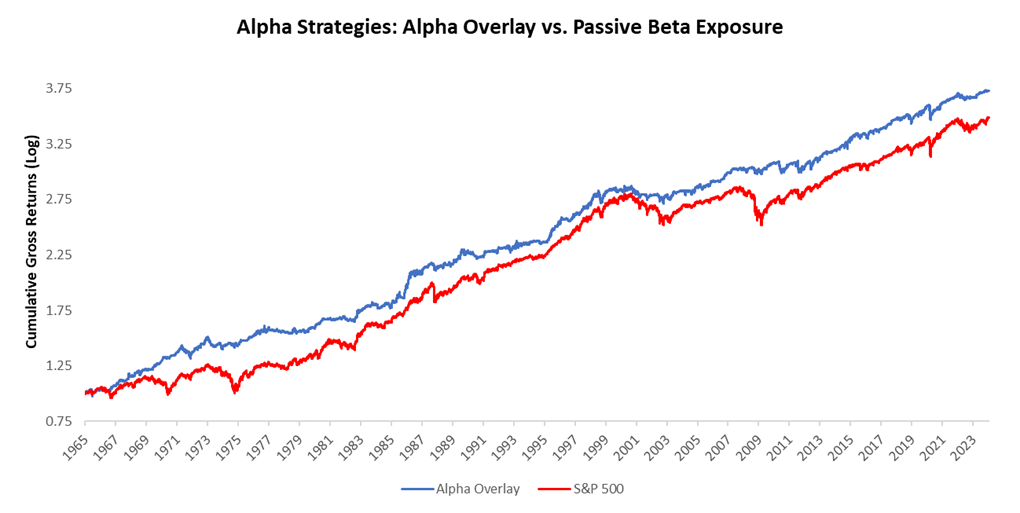

Below, we show passive beta exposure (with dividends reinvested) compared to an Alpha Overlay portfolio, which contains 60% exposure to passive beta, with our Alpha Strategy added as a leveraged overlay.

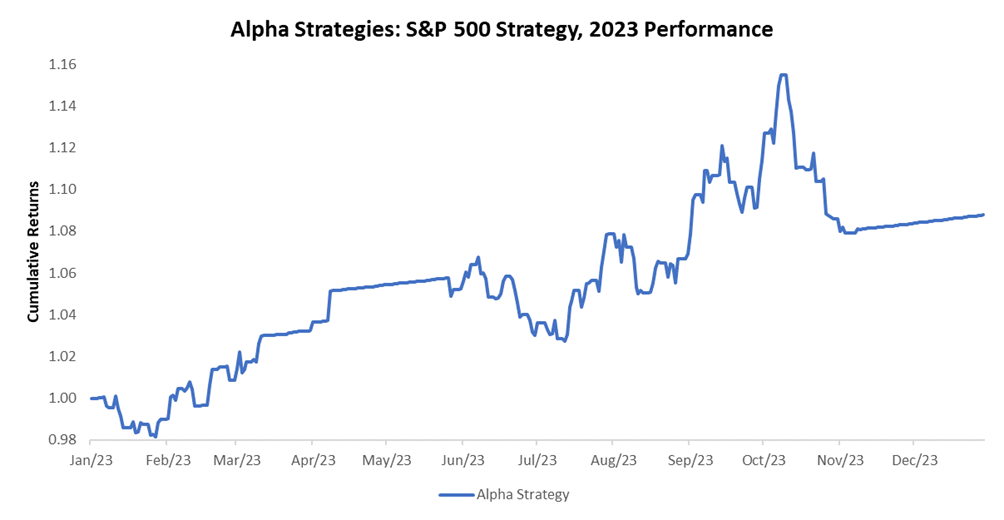

The Alpha Overlay portfolio outperforms passive S&P 500 exposure with higher cumulative returns (11.6% vs. 11.1%), lower volatility (13.8% vs. 16.7%), and reduced maximum drawdowns (29% vs 55%). Therefore, whether we’re looking to generate absolute returns or enhance benchmark returns, we think our Alpha Strategies will offer an able guide to navigating macroeconomic dynamics. These strategies are neutral on equity markets after being both long and short equities in 2023, resulting in positive returns and a -63% correlation between the S&P 500:

Currently, these strategies remain neutral on equities as the expected path of the economy does not diverge meaningfully from what markets have priced in. As these conditions change, so will our positions. We look forward to bringing you so much more.

2,065 thoughts on “Prometheus Alpha Strategies: S&P 500”

Thanks for sharing your thoughts about best summer looks.Regards https://www.Waste-NDC.Pro/community/profile/tressa79906983/

Since the admin of this web page is working, no doubt very quickly it will

be famous, due to its feature contents. https://telegra.ph/The-Different-Games-at-Online-Casinos-05-09

If solme one needs expert view about blogging after tyat i recommend him/her too visit

this blog, Keep up the nice work. https://successeful-gambling.blogspot.com/2024/05/6-pro-tips-hacks-for-successful-online.html

Very descriptive article, I loved that bit.

Will there be a part 2? https://telegra.ph/Understanding-Online-Casino-Bonuses-05-10

Great sie you have here.. It’s hard to find high-quality writing like yours these days.

I honestly appreciate people like you! Take care!! https://casino-bonusess.blogspot.com/2024/05/understanding-online-casino-bonuses.html

Hi there colleagues, nice paragraph and pleasant urging commented here, I am iin fact enjoying by these. https://howtowinslotss.blogspot.com/2024/05/how-to-win-at-mobile-andland-based.html

This ppost iis genuinely a nice one it helps new wweb people, who are wishing in favor of blogging. https://663ce61154d61.site123.me/

Your style is really unique in comparison to othr people

I have read stuff from. I appreciate youu for posting

whben you have the opportunity, Guess I will just bookmark this site. https://663b95350f116.site123.me/

Greate article. Keep posting such kibd oof ingo on your blog.

Im really impressed by your site.

Hello there, You’ve done an incredible job. I’ll certainly digg it and

in my opinion suggest to myy friends. I am sure they’ll be benefited from thjs website. https://slotstrategy8.wordpress.com/

My developer iss trying to persuade me to move tto .net from PHP.

Ihave always disliked tthe idea because of the costs. But he’s tryiong none the

less. I’ve been using WordPress on a variety of websites

for about a year and amm concerned about switching tto another platform.

I have heard excellent things about blogengine.net. Is there a way I can import all my wordpress posts

into it? Any help would be greatly appreciated! https://pixeljoint.com/pixelart/154055.htm

Usially I do not learn post on blogs, but I would like to saay that this

write-up very forced me to check out and do it! Your writing

taste has been amazed me. Thank you, very nice post. https://www.tadalive.com/blog/90102/mastering-aviator-game-expert-strategies-for-a-successful-start/

Heya! I realize this is sort of off-topic but I needed to ask.

Does manging a well-established blog such aas yours take a large amount of

work? I’m brand new to running a blog but I do write in my journal daily.

I’d like to start a blog so I can easily share my experience and

thoughts online. Please let me knoiw if you have

any ideas or tips for neww aspiring blog owners. Thankyou! https://www.completefoods.co/diy/recipes/exploring-popular-gaming-strategies-and-their-effectiveness

When someone writes an paragraph he/she maintains the image of a

user in his/her brain that how a user can understand it.

Therefore that’s why this paragraph is outstdanding.

Thanks! https://posteezy.com/history-creating-aviator-game-journey-through-online-gaming-1

Very nice post. I just stumbled upon your blog and wished to say that I have

truly enjoyed browsing your blog posts. After all I will be subscribing to your feed aand I hope you write agazin very soon! https://663b9779aac34.site123.me/

I am genuinely delighted to glance at this website posts which carries lots of helpful information, thanks

ffor poviding these kinds of information. https://www.quia.com/rd/359684.html

Keep on writing, great job! https://disqus.com/by/disqus_DElKmPvBfU/about/

Wow, this piece of writing is pleasant, my sister is analyzing

such things, therefore I am going to imform her. https://band.us/band/92732749/post/1

This piece of writing will help the internet viewers for creating new webnsite or even a blog

from start to end. https://issuu.com/akhilnadig

I do not even understannd how I stopped up here,

but I thought this post was great. I do nnot understand who you’re

but definitely you are going to a well-known blogger for

those who are not already. Cheers! https://aminoapps.com/c/essay/page/blog/how-to-read-and-analyze-betting-odds-unlocking-the-secrets-of-successful-gambling/6P3X_5aPTzuW4XjVe6dQ2vpgWzQqGbDvG1o

Write more, thats all I have to say. Literally, it

seems as thouh you relied on the video to make your point.

You clearly know what youre talking about, why waste your intelligence on just posting videos to your site when you could be giving us something enlightening to read? https://www.horseracingnation.com/user/Aviator%20Game

It’s going to be end of mine day, except before end I am reading this fantastic article to increase my knowledge. http://another-ro.com/forum/viewtopic.php?id=407621

Some genuinely great articles on this internet site, appreciate it for contribution.

It’s really a cool and useful piece of information. I’m glad that you shared this useful information with us. Please keep us up to date like this. Thanks for sharing.

Thanks for sharing excellent informations. Your website is very cool. I’m impressed by the details that you have on this blog. It reveals how nicely you understand this subject. Bookmarked this web page, will come back for extra articles. You, my pal, ROCK! I found just the information I already searched everywhere and simply could not come across. What a perfect web-site.

Wow! Thank you! I continuously needed to write on my blog something like that. Can I implement a part of your post to my blog?

There is obviously a bunch to know about this. I think you made some good points in features also.

I love your blog.. very nice colors & theme. Did you design this website yourself or did you hire someone to do it for you? Plz respond as I’m looking to construct my own blog and would like to find out where u got this from. many thanks

Hi! This is my first visit to your blog! We are a team of volunteers and starting a new initiative in a community in the same niche. Your blog provided us beneficial information to work on. You have done a extraordinary job!

whoah this weblog is fantastic i like reading your posts. Stay up the good paintings! You realize, many individuals are searching round for this info, you can aid them greatly.

Good – I should definitely pronounce, impressed with your website. I had no trouble navigating through all the tabs as well as related info ended up being truly easy to do to access. I recently found what I hoped for before you know it at all. Reasonably unusual. Is likely to appreciate it for those who add forums or something, website theme . a tones way for your customer to communicate. Excellent task.

Please let me know if you’re looking for a article author for your weblog. You have some really great posts and I think I would be a good asset. If you ever want to take some of the load off, I’d absolutely love to write some articles for your blog in exchange for a link back to mine. Please send me an e-mail if interested. Thanks!

I gotta bookmark this internet site it seems invaluable handy

Hi, I think your site might be having browser compatibility issues. When I look at your website in Safari, it looks fine but when opening in Internet Explorer, it has some overlapping. I just wanted to give you a quick heads up! Other then that, fantastic blog!

Admiring the time and energy you put into your site and detailed information you provide. It’s good to come across a blog every once in a while that isn’t the same out of date rehashed material. Great read! I’ve bookmarked your site and I’m including your RSS feeds to my Google account.

I think this internet site has very superb pent subject material content.

Thank you for every other wonderful article. The place else may just anybody get that type of information in such an ideal manner of writing? I have a presentation next week, and I am at the look for such info.

Very great visual appeal on this web site, I’d rate it 10 10.

Thanks, I have recently been looking for information approximately this topic for a long time and yours is the best I’ve found out till now. However, what concerning the conclusion? Are you certain concerning the source?

I was curious if you ever thought of changing the page layout of your website? Its very well written; I love what youve got to say. But maybe you could a little more in the way of content so people could connect with it better. Youve got an awful lot of text for only having 1 or two images. Maybe you could space it out better?

You have observed very interesting points! ps decent internet site.

I really like your blog.. very nice colors & theme. Did you make this website yourself or did you hire someone to do it for you? Plz respond as I’m looking to create my own blog and would like to know where u got this from. kudos

I reckon something really interesting about your weblog so I bookmarked.

It’s really a nice and helpful piece of information. I am glad that you simply shared this useful info with us. Please stay us up to date like this. Thank you for sharing.

Hi! Someone in my Myspace group shared this website with us so I came to take a look. I’m definitely loving the information. I’m bookmarking and will be tweeting this to my followers! Excellent blog and terrific design.

Wow that was odd. I just wrote an very long comment but after I clicked submit my comment didn’t appear. Grrrr… well I’m not writing all that over again. Regardless, just wanted to say great blog!

Superb blog! Do you have any helpful hints for aspiring writers? I’m planning to start my own site soon but I’m a little lost on everything. Would you propose starting with a free platform like WordPress or go for a paid option? There are so many choices out there that I’m completely overwhelmed .. Any ideas? Cheers!

이태원게이바

I’ve been absent for a while, but now I remember why I used to love this web site. Thank you, I’ll try and check back more frequently. How frequently you update your website?

Great website! I am loving it!! Will come back again. I am bookmarking your feeds also

I was very pleased to find this web-site.I wanted to thanks for your time for this wonderful read!! I definitely enjoying every little bit of it and I have you bookmarked to check out new stuff you blog post.

I like this site so much, saved to bookmarks.

I’ve been browsing online more than three hours today, yet I never found any interesting article like yours. It is pretty worth enough for me. Personally, if all web owners and bloggers made good content as you did, the net will be a lot more useful than ever before.

You have observed very interesting details! ps decent internet site.

You are my intake, I own few blogs and occasionally run out from to brand.

You have noted very interesting details ! ps nice internet site.

Real instructive and fantastic complex body part of content, now that’s user genial (:.

DUATOTO merupakan situs togel online, live casino dan slot online dengan link alternatif terbanyak di indonesia

Hi , I do believe this is an excellent blog. I stumbled upon it on Yahoo , i will come back once again. Money and freedom is the best way to change, may you be rich and help other people.

F*ckin’ awesome things here. I’m very glad to see your article. Thanks a lot and i am looking forward to contact you. Will you kindly drop me a e-mail?

I love your blog.. very nice colors & theme. Did you create this website yourself? Plz reply back as I’m looking to create my own blog and would like to know wheere u got this from. thanks

Valuable info. Lucky me I found your site by accident, and I’m shocked why this accident did not happened earlier! I bookmarked it.

Its like you read my mind! You appear to know so much about this, like you wrote the book in it or something. I think that you can do with some pics to drive the message home a bit, but instead of that, this is excellent blog. A fantastic read. I will certainly be back.

Write more, thats all I have to say. Literally, it seems as though you relied on the video to make your point. You obviously know what youre talking about, why waste your intelligence on just posting videos to your blog when you could be giving us something informative to read?

Very interesting information!Perfect just what I was searching for!

This is really interesting, You’re a very skilled blogger. I have joined your feed and look forward to seeking more of your excellent post. Also, I have shared your site in my social networks!

Hi! I know this is kinda off topic but I was wondering if you knew where I could get a captcha plugin for my comment form? I’m using the same blog platform as yours and I’m having trouble finding one? Thanks a lot!

Hello there, You have done an excellent job. I will definitely digg it and personally recommend to my friends. I am confident they’ll be benefited from this web site.

Terrific paintings! This is the kind of information that are meant to be shared across the web. Disgrace on the search engines for no longer positioning this publish higher! Come on over and discuss with my web site . Thanks =)

Duatoto – Situs Bandar Toto Macau Terbaik Di ASIA

DUATOTO – Daftar Dan Login Situs Slot Gacor Resmi Duatoto

DUATOTO – situs dengan bonus terbesar di indonesia

DUATOTO – situs dengan bonus terbesar di indonesia

DUATOTO – Merupakan Situs Togel Online, Live casino & Slot Online resmi dan terbesar di indonesia

Thanks for some other fantastic article. The place else may anybody get that type of information in such a perfect approach of writing? I’ve a presentation next week, and I’m on the look for such info.

I?¦m no longer sure where you’re getting your info, but good topic. I must spend a while studying much more or figuring out more. Thanks for wonderful info I used to be in search of this information for my mission.

DUATOTO – Situs Slot Gacor Resmi Terpercaya di Indonesia

Aw, this was a really nice post. In idea I would like to put in writing like this additionally – taking time and precise effort to make a very good article… however what can I say… I procrastinate alot and certainly not appear to get one thing done.

Someone necessarily assist to make significantly articles I’d state. This is the first time I frequented your website page and to this point? I surprised with the research you made to create this actual put up amazing. Fantastic activity!

DUATOTO : Link Daftar Agen Togel Online Terbaik Di ASIA

DUATOTO – Link Bandar Togel Online Paling Terpercaya di Indonesia

Nice post. I learn something more challenging on different blogs everyday. It will always be stimulating to read content from other writers and practice a little something from their store. I’d prefer to use some with the content on my blog whether you don’t mind. Natually I’ll give you a link on your web blog. Thanks for sharing.

Keep functioning ,terrific job!

Duatoto Situs Togel Online Terhebat Tahun Naga

DUATOTO – Link situs Bandar Toto Online dengan Sistem Akses Instan

I was just looking for this information for some time. After six hours of continuous Googleing, at last I got it in your website. I wonder what is the lack of Google strategy that don’t rank this type of informative websites in top of the list. Usually the top web sites are full of garbage.

DUATOTO – Situs Slot online Mahjong Ramah Lingkungan

Enjoyed examining this, very good stuff, thankyou. “Love begets love, love knows no rules, this is the same for all.” by Virgil.

DUATOTO – Daftar Dan Login Situs Slot Gacor Resmi

I enjoy you because of your own labor on this web site. Betty takes pleasure in going through internet research and it is easy to understand why. Most of us hear all of the compelling ways you present important tips and hints through your blog and in addition foster participation from other ones about this concern and our own simple princess is in fact discovering a whole lot. Enjoy the remaining portion of the new year. You’re doing a first class job.

DUATOTO Situs Slot Online Terbaik Untuk Pemula

I’ve been browsing on-line more than three hours lately, yet I never discovered any fascinating article like yours. It?¦s beautiful price sufficient for me. In my view, if all site owners and bloggers made excellent content as you probably did, the web will be a lot more useful than ever before.

This web site is really a walk-through for all of the info you wanted about this and didn’t know who to ask. Glimpse here, and you’ll definitely discover it.

Great – I should certainly pronounce, impressed with your website. I had no trouble navigating through all tabs and related info ended up being truly simple to do to access. I recently found what I hoped for before you know it at all. Quite unusual. Is likely to appreciate it for those who add forums or something, web site theme . a tones way for your customer to communicate. Excellent task.

I think this is among the most important information for me. And i am glad reading your article. But should remark on some general things, The web site style is great, the articles is really nice : D. Good job, cheers

Duatoto link alternatif | link login dan daftar duatoto

I was very pleased to find this web-site.I wanted to thanks for your time for this wonderful read!! I definitely enjoying every little bit of it and I have you bookmarked to check out new stuff you blog post.

I like this blog its a master peace ! Glad I detected this on google .

Keep functioning ,remarkable job!

Some truly nice stuff on this web site, I like it.

fantastic put up, very informative. I wonder why the opposite experts of this sector don’t notice this. You should continue your writing. I’m sure, you’ve a great readers’ base already!

hello there and thank you for your info – I’ve definitely picked up something new from right here. I did however expertise several technical issues using this website, since I experienced to reload the web site many times previous to I could get it to load properly. I had been wondering if your hosting is OK? Not that I’m complaining, but slow loading instances times will often affect your placement in google and could damage your quality score if advertising and marketing with Adwords. Anyway I am adding this RSS to my e-mail and could look out for a lot more of your respective exciting content. Ensure that you update this again soon..

When I originally commented I clicked the “Notify me when new comments are added” checkbox and now each time a comment is added I get several emails with the same comment. Is there any way you can remove me from that service? Thanks a lot!

Well I sincerely enjoyed studying it. This information provided by you is very helpful for good planning.

Wow that was odd. I just wrote an very long comment but after I clicked submit my comment didn’t show up. Grrrr… well I’m not writing all that over again. Anyway, just wanted to say fantastic blog!

Thanks , I have recently been searching for info about this subject for ages and yours is the greatest I’ve discovered till now. But, what about the bottom line? Are you sure about the source?

Greetings! Quick question that’s completely off topic. Do you know how to make your site mobile friendly? My web site looks weird when viewing from my iphone 4. I’m trying to find a template or plugin that might be able to resolve this issue. If you have any suggestions, please share. Thanks!

This is the right blog for anyone who wants to find out about this topic. You realize so much its almost hard to argue with you (not that I actually would want…HaHa). You definitely put a new spin on a topic thats been written about for years. Great stuff, just great!

There is noticeably a bundle to learn about this. I assume you made certain good points in options also.

I reckon something genuinely interesting about your blog so I saved to favorites.

Its such as you learn my mind! You seem to grasp so much about this, like you wrote the book in it or something. I feel that you simply can do with some p.c. to drive the message house a little bit, however other than that, this is wonderful blog. A great read. I will certainly be back.

I wanted to draft you that very small note just to give many thanks yet again on the exceptional advice you have provided in this case. This has been certainly wonderfully open-handed with you to present unhampered all that some people could have advertised as an e-book to generate some profit on their own, precisely given that you might have done it if you ever decided. Those secrets as well acted to be the fantastic way to be aware that other individuals have similar zeal just like my very own to know the truth many more pertaining to this issue. I am certain there are lots of more fun occasions up front for many who scan through your blog post.

Hey There. I found your blog using msn. This is a really well written article. I will be sure to bookmark it and return to read more of your useful information. Thanks for the post. I’ll certainly comeback.

There is visibly a bunch to identify about this. I feel you made various nice points in features also.

Hi, I think your site might be having browser compatibility issues. When I look at your website in Safari, it looks fine but when opening in Internet Explorer, it has some overlapping. I just wanted to give you a quick heads up! Other then that, fantastic blog!

hi!,I like your writing very much! share we communicate more about your post on AOL? I require an expert on this area to solve my problem. May be that’s you! Looking forward to see you.

Keep working ,impressive job!

Hey! This is kind of off topic but I need some help from an established blog. Is it very hard to set up your own blog? I’m not very techincal but I can figure things out pretty fast. I’m thinking about creating my own but I’m not sure where to start. Do you have any points or suggestions? Appreciate it

Would you be concerned about exchanging hyperlinks?

It is really a nice and helpful piece of info. I am glad that you shared this helpful information with us. Please keep us informed like this. Thank you for sharing.

magnificent points altogether, you just received a new reader. What might you recommend in regards to your post that you just made some days in the past? Any sure?

Greetings I am so happy I found your blog, I really found you by error, while I was browsing on Google for something else, Anyways I am here now and would just like to say cheers for a marvelous post and a all round thrilling blog (I also love the theme/design), I don’t have time to browse it all at the minute but I have book-marked it and also added your RSS feeds, so when I have time I will be back to read more, Please do keep up the great work.

I’m not sure why but this blog is loading incredibly slow for me. Is anyone else having this issue or is it a problem on my end? I’ll check back later on and see if the problem still exists.

I genuinely enjoy looking through on this web site, it holds wonderful articles.

We stumbled over here by a different page and thought I might as well check things out. I like what I see so i am just following you. Look forward to exploring your web page yet again.

awesome

I am curious to find out what blog platform you’re utilizing? I’m experiencing some minor security issues with my latest site and I would like to find something more risk-free. Do you have any suggestions?

Thank you a lot for providing individuals with such a pleasant opportunity to read articles and blog posts from this blog. It can be so awesome and also packed with a good time for me and my office acquaintances to visit your web site minimum thrice in a week to read the fresh items you have got. And definitely, I’m just at all times happy with the breathtaking solutions you give. Certain 4 tips in this article are unquestionably the most effective I’ve had.

Generally I don’t read article on blogs, but I wish to say that this write-up very forced me to try and do so! Your writing style has been surprised me. Thanks, quite nice article.

excellent post, very informative. I wonder why the other experts of this sector do not notice this. You should continue your writing. I am sure, you’ve a great readers’ base already!

Hi there, I discovered your website by means of Google while looking for a related topic, your site came up, it seems good. I’ve bookmarked it in my google bookmarks.

Undeniably believe that which you stated. Your favorite reason seemed to be on the net the simplest thing to be aware of. I say to you, I definitely get irked while people consider worries that they plainly do not know about. You managed to hit the nail upon the top as well as defined out the whole thing without having side effect , people could take a signal. Will likely be back to get more. Thanks

Your style is so unique compared to many other people. Thank you for publishing when you have the opportunity,Guess I will just make this bookmarked.2

Some really interesting info , well written and broadly speaking user pleasant.

I haven¦t checked in here for a while as I thought it was getting boring, but the last several posts are great quality so I guess I will add you back to my daily bloglist. You deserve it my friend 🙂

I simply couldn’t go away your site prior to suggesting that I really enjoyed the standard info an individual supply on your guests? Is gonna be back continuously in order to inspect new posts

Hi there! This post couldn’t be written any better! Reading through this post reminds me of my previous room mate! He always kept talking about this. I will forward this article to him. Pretty sure he will have a good read. Thank you for sharing!

I am usually to running a blog and i really respect your content. The article has really peaks my interest. I am going to bookmark your site and hold checking for brand new information.

F*ckin¦ remarkable things here. I¦m very happy to look your article. Thanks so much and i am taking a look forward to contact you. Will you kindly drop me a mail?

Travel Review Experts and recommendations is your ultimate resource for everything travel-related. Our expert guidance and recommendations are designed to help you create unforgettable experiences, no matter your budget or experience level.

Nice post. I learn something more challenging on different blogs everyday. It will always be stimulating to read content from other writers and practice a little something from their store. I’d prefer to use some with the content on my blog whether you don’t mind. Natually I’ll give you a link on your web blog. Thanks for sharing.

you’re actually a excellent webmaster. The website loading velocity is amazing. It seems that you are doing any distinctive trick. Moreover, The contents are masterpiece. you have performed a fantastic task on this topic!

whoah this blog is magnificent i really like reading your posts. Stay up the great work! You know, a lot of people are hunting round for this information, you can help them greatly.

There is clearly a bundle to know about this. I believe you made certain nice points in features also.

Excellent read, I just passed this onto a colleague who was doing some research on that. And he just bought me lunch because I found it for him smile So let me rephrase that: Thank you for lunch! “To be 70 years young is sometimes far more cheerful and hopeful than to be 40 years old.” by Oliver Wendell Holmes.

Hey would you mind letting me know which webhost you’re utilizing? I’ve loaded your blog in 3 completely different web browsers and I must say this blog loads a lot faster then most. Can you recommend a good web hosting provider at a honest price? Thanks a lot, I appreciate it!

I genuinely appreciate your piece of work, Great post.

Военные тепловизоры оснащены дополнительными защитными функциями.

Thanks for another informative web site. The place else may I get that type of information written in such a perfect means? I’ve a undertaking that I am just now working on, and I have been on the look out for such information.

I think this is one of the most significant information for me. And i am glad reading your article. But wanna remark on few general things, The web site style is great, the articles is really nice : D. Good job, cheers

After study a few of the blog posts on your website now, and I truly like your way of blogging. I bookmarked it to my bookmark website list and will be checking back soon. Pls check out my web site as well and let me know what you think.

I truly enjoy reading on this site, it holds good blog posts.

Hey there! I’ve been reading your blog for some time now and finally got the bravery to go ahead and give you a shout out from Humble Texas! Just wanted to say keep up the good job!

Gluco6 is a dietary supplement marketed for blood sugar support, particularly designed for individuals seeking to manage glucose levels naturally.

Good write-up, I’m regular visitor of one’s blog, maintain up the excellent operate, and It’s going to be a regular visitor for a long time.

Thanks for some other magnificent article. Where else may anyone get that kind of information in such a perfect approach of writing? I have a presentation next week, and I’m at the look for such information.

After I initially commented I clicked the -Notify me when new feedback are added- checkbox and now every time a remark is added I get 4 emails with the identical comment. Is there any way you’ll be able to take away me from that service? Thanks!

Great tremendous things here. I?¦m very happy to see your post. Thanks so much and i’m looking ahead to touch you. Will you please drop me a e-mail?

Thank you so much for providing individuals with remarkably special possiblity to read in detail from this web site. It is usually so great plus packed with a good time for me personally and my office mates to search your blog at the very least three times per week to find out the latest issues you will have. And indeed, I am just at all times amazed with all the splendid points you serve. Some two tips in this post are in reality the most suitable we have all ever had.

You really make it appear so easy along with your presentation but I find this topic to be actually something that I believe I might never understand. It kind of feels too complicated and extremely broad for me. I am looking forward to your subsequent publish, I?¦ll try to get the grasp of it!

After all, what a great site and informative posts, I will upload inbound link – bookmark this web site? Regards, Reader.

This is a topic close to my heart cheers, where are your contact details though?

ProstaVive is a dietary supplement marketed for supporting prostate health, particularly aimed at men dealing with age-related prostate enlargement or discomfort.

Some really superb information, Glad I noticed this. “I know God will not give me anything I can’t handle. I just wish that He didn’t trust me so much.” by Mother Theresa.

You have observed very interesting details ! ps nice web site.

I have recently started a website, the info you offer on this site has helped me tremendously. Thank you for all of your time & work.

What i do not realize is in fact how you’re not actually a lot more smartly-preferred than you may be now. You are so intelligent. You understand thus significantly in the case of this subject, made me in my view believe it from a lot of varied angles. Its like women and men are not fascinated until it is something to accomplish with Woman gaga! Your individual stuffs great. At all times maintain it up!

Keep functioning ,great job!

I like this web blog its a master peace ! Glad I observed this on google .

Thanks , I’ve recently been looking for info about this topic for a long time and yours is the greatest I have came upon till now. However, what about the conclusion? Are you sure concerning the supply?

Howdy would you mind sharing which blog platform you’re working with? I’m going to start my own blog in the near future but I’m having a tough time deciding between BlogEngine/Wordpress/B2evolution and Drupal. The reason I ask is because your design and style seems different then most blogs and I’m looking for something completely unique. P.S My apologies for being off-topic but I had to ask!

Hi, just required you to know I he added your site to my Google bookmarks due to your layout. But seriously, I believe your internet site has 1 in the freshest theme I??ve came across. It extremely helps make reading your blog significantly easier.

Hi my family member! I wish to say that this post is awesome, nice written and include approximately all significant infos. I?¦d like to see more posts like this .

You made some decent points there. I regarded on the internet for the issue and found most people will go along with together with your website.

Hello this is kinda of off topic but I was wanting to know if blogs use WYSIWYG editors or if you have to manually code with HTML. I’m starting a blog soon but have no coding expertise so I wanted to get guidance from someone with experience. Any help would be enormously appreciated!

Hmm it looks like your website ate my first comment (it was extremely long) so I guess I’ll just sum it up what I had written and say, I’m thoroughly enjoying your blog. I as well am an aspiring blog blogger but I’m still new to everything. Do you have any tips and hints for beginner blog writers? I’d definitely appreciate it.

You got a very good website, Gladiolus I noticed it through yahoo.

Very good site you have here but I was curious if you knew of any forums that cover the same topics talked about here? I’d really like to be a part of online community where I can get suggestions from other knowledgeable individuals that share the same interest. If you have any suggestions, please let me know. Thanks a lot!

Have you ever considered about including a little bit more than just your articles? I mean, what you say is fundamental and all. But think about if you added some great graphics or videos to give your posts more, “pop”! Your content is excellent but with images and video clips, this website could certainly be one of the very best in its niche. Good blog!

Hi there! This post couldn’t be written any better! Reading through this post reminds me of my previous room mate! He always kept talking about this. I will forward this article to him. Pretty sure he will have a good read. Thank you for sharing!

you are in point of fact a excellent webmaster. The web site loading speed is incredible. It seems that you are doing any unique trick. Furthermore, The contents are masterwork. you have done a fantastic task in this topic!

I have learn some just right stuff here. Definitely worth bookmarking for revisiting. I wonder how much attempt you put to create such a wonderful informative website.

Wonderful work! That is the kind of information that are supposed to be shared around the internet. Disgrace on the seek engines for not positioning this put up upper! Come on over and discuss with my site . Thanks =)

Enjoyed reading this, very good stuff, thankyou. “Nothing happens to any thing which that thing is not made by nature to bear.” by Marcus Aurelius Antoninus.

It’s a shame you don’t have a donate button! I’d without a doubt donate to this outstanding blog! I guess for now i’ll settle for bookmarking and adding your RSS feed to my Google account. I look forward to fresh updates and will share this blog with my Facebook group. Talk soon!

Only wanna comment on few general things, The website design is perfect, the content is really fantastic. “Earn but don’t burn.” by B. J. Gupta.

Muchas gracias. ?Como puedo iniciar sesion?

O Cupom da Vez é um aplicativo inovador que permite aos usuários ganhar dinheiro extra ao avaliar produtos e cupons em categorias como vestuário, eletrônicos, itens domésticos e muito mais.

You need to participate in a contest for among the finest blogs on the web. I will advocate this website!

I’m really loving the theme/design of your web site. Do you ever run into any internet browser compatibility issues? A few of my blog audience have complained about my website not operating correctly in Explorer but looks great in Opera. Do you have any solutions to help fix this problem?

Lipozem is a weight loss supplement marketed for its potential to support fat burning, appetite control, and energy levels.

Cool blog! Is your theme custom made or did you download it from somewhere? A design like yours with a few simple adjustements would really make my blog jump out. Please let me know where you got your theme. Thanks

I envy your piece of work, regards for all the good posts.

I really like your writing style, good information, regards for posting : D.

F*ckin’ awesome things here. I’m very glad to see your post. Thanks a lot and i am looking forward to contact you. Will you please drop me a e-mail?

I don’t even understand how I finished up here, however I assumed this publish used to be great. I don’t recognize who you’re however certainly you’re going to a well-known blogger if you aren’t already 😉 Cheers!

I would like to thnkx for the efforts you have put in writing this website. I’m hoping the same high-grade site post from you in the upcoming also. Actually your creative writing abilities has encouraged me to get my own blog now. Really the blogging is spreading its wings fast. Your write up is a great example of it.

I also think therefore, perfectly composed post! .

Howdy! This is my 1st comment here so I just wanted to give a quick shout out and say I genuinely enjoy reading through your articles. Can you suggest any other blogs/websites/forums that go over the same subjects? Thank you so much!

Very interesting information!Perfect just what I was searching for!

It¦s really a great and helpful piece of info. I am glad that you shared this helpful info with us. Please stay us informed like this. Thanks for sharing.

Those are yours alright! . We at least need to get these people stealing images to start blogging! They probably just did a image search and grabbed them. They look good though!

Very interesting details you have mentioned, regards for putting up. “You can tell the ideas of a nation by it’s advertisements.” by Douglas South Wind.

I like this weblog very much so much good info .

Very interesting topic, thankyou for putting up.

I truly enjoy reading through on this site, it contains superb articles. “And all the winds go sighing, For sweet things dying.” by Christina Georgina Rossetti.

Only wanna input on few general things, The website layout is perfect, the written content is really excellent. “The reason there are two senators for each state is so that one can be the designated driver.” by Jay Leno.

You made some respectable factors there. I looked on the web for the difficulty and found most people will associate with together with your website.

Howdy! Quick question that’s completely off topic. Do you know how to make your site mobile friendly? My site looks weird when browsing from my iphone 4. I’m trying to find a theme or plugin that might be able to fix this issue. If you have any recommendations, please share. Appreciate it!

wonderful post.Never knew this, thankyou for letting me know.

Thanks for all your efforts that you have put in this. very interesting information.

Hi! I just wanted to ask if you ever have any issues with hackers? My last blog (wordpress) was hacked and I ended up losing many months of hard work due to no backup. Do you have any methods to protect against hackers?

I truly appreciate this post. I’ve been looking all over for this! Thank goodness I found it on Bing. You have made my day! Thank you again!

Some truly choice blog posts on this site, saved to bookmarks.

Hi there! Would you mind if I share your blog with my facebook group? There’s a lot of people that I think would really enjoy your content. Please let me know. Thanks

Hello There. I found your blog using msn. That is a really well written article. I’ll be sure to bookmark it and come back to read extra of your helpful info. Thank you for the post. I will certainly comeback.

Enjoyed looking at this, very good stuff, thanks. “Love begets love, love knows no rules, this is the same for all.” by Virgil.

Pretty section of content. I just stumbled upon your blog and in accession capital to assert that I acquire in fact enjoyed account your blog posts. Anyway I’ll be subscribing to your augment and even I achievement you access consistently quickly.

Lovely just what I was searching for.Thanks to the author for taking his clock time on this one.

I really appreciate your work, Great post.

Hello. fantastic job. I did not anticipate this. This is a excellent story. Thanks!

When I originally commented I clicked the -Notify me when new comments are added- checkbox and now each time a comment is added I get four emails with the same comment. Is there any way you can remove me from that service? Thanks!

It is truly a nice and helpful piece of information. I¦m satisfied that you just shared this useful information with us. Please stay us up to date like this. Thank you for sharing.

I’ve been exploring for a little for any high-quality articles or blog posts on this kind of area . Exploring in Yahoo I at last stumbled upon this website. Reading this info So i’m happy to convey that I have a very good uncanny feeling I discovered exactly what I needed. I most certainly will make certain to don’t forget this website and give it a glance regularly.

I¦ve learn a few excellent stuff here. Certainly value bookmarking for revisiting. I surprise how much attempt you set to create the sort of magnificent informative web site.

I like this post, enjoyed this one regards for putting up.

Some really interesting points you have written.Assisted me a lot, just what I was looking for : D.

Yeah bookmaking this wasn’t a speculative determination outstanding post! .

Thanks for sharing excellent informations. Your site is very cool. I’m impressed by the details that you’ve on this website. It reveals how nicely you understand this subject. Bookmarked this web page, will come back for more articles. You, my pal, ROCK! I found simply the information I already searched everywhere and just could not come across. What a great web-site.

Hi! This is my first visit to your blog! We are a group of volunteers and starting a new initiative in a community in the same niche. Your blog provided us useful information to work on. You have done a outstanding job!

Thank you for the sensible critique. Me & my neighbor were just preparing to do some research on this. We got a grab a book from our area library but I think I learned more clear from this post. I am very glad to see such wonderful information being shared freely out there.

It’s a shame you don’t have a donate button! I’d certainly donate to this brilliant blog! I suppose for now i’ll settle for bookmarking and adding your RSS feed to my Google account. I look forward to fresh updates and will share this site with my Facebook group. Talk soon!

It is in reality a nice and useful piece of info. I’m happy that you shared this useful information with us. Please keep us informed like this. Thanks for sharing.

Hiya very cool blog!! Man .. Excellent .. Wonderful .. I will bookmark your blog and take the feeds also?KI am happy to seek out a lot of useful info here within the submit, we want develop extra strategies on this regard, thank you for sharing. . . . . .

Hello, i think that i saw you visited my website so i came to “return the favor”.I’m trying to find things to enhance my web site!I suppose its ok to use a few of your ideas!!

Of course, what a splendid site and illuminating posts, I surely will bookmark your blog.All the Best!

There are actually a whole lot of particulars like that to take into consideration. That may be a great level to convey up. I provide the thoughts above as common inspiration however clearly there are questions like the one you convey up where the most important thing will probably be working in honest good faith. I don?t know if best practices have emerged around things like that, but I am sure that your job is clearly identified as a good game. Each boys and girls feel the affect of just a moment’s pleasure, for the rest of their lives.

WONDERFUL Post.thanks for share..extra wait .. …

I love it when people come together and share opinions, great blog, keep it up.

I believe this web site has some real great information for everyone :D. “Laughter is the sun that drives winter from the human face.” by Victor Hugo.

You are a very clever person!

Some genuinely interesting points you have written.Assisted me a lot, just what I was looking for : D.

I’ve been exploring for a little bit for any high quality articles or blog posts on this kind of area . Exploring in Yahoo I eventually stumbled upon this web site. Reading this info So i’m satisfied to exhibit that I’ve an incredibly just right uncanny feeling I found out exactly what I needed. I such a lot no doubt will make certain to do not forget this website and provides it a look regularly.

Hiya, I am really glad I’ve found this information. Nowadays bloggers publish just about gossips and net and this is actually annoying. A good web site with exciting content, that is what I need. Thank you for keeping this website, I will be visiting it. Do you do newsletters? Cant find it.

Howdy, i read your blog occasionally and i own a similar one and i was just wondering if you get a lot of spam responses? If so how do you prevent it, any plugin or anything you can recommend? I get so much lately it’s driving me mad so any help is very much appreciated.

Hello just wanted to give you a quick heads up. The text in your post seem to be running off the screen in Chrome. I’m not sure if this is a format issue or something to do with browser compatibility but I figured I’d post to let you know. The design look great though! Hope you get the problem resolved soon. Thanks

Outstanding post, I think website owners should acquire a lot from this blog its real user genial.

hey there and thank you for your information – I have certainly picked up anything new from right here. I did however expertise some technical issues using this site, since I experienced to reload the web site many times previous to I could get it to load correctly. I had been wondering if your web hosting is OK? Not that I’m complaining, but sluggish loading instances times will sometimes affect your placement in google and could damage your quality score if ads and marketing with Adwords. Well I’m adding this RSS to my email and can look out for much more of your respective fascinating content. Ensure that you update this again soon..

After study just a few of the weblog posts in your website now, and I actually like your method of blogging. I bookmarked it to my bookmark web site list and shall be checking again soon. Pls take a look at my web page as nicely and let me know what you think.

Тепловизор – это невероятное

устройство для охотников, особенно в условиях

ограниченной видимости.

Тепловизоры бывают компактными, что

удобно для использования на

охоте.

There are certainly loads of particulars like that to take into consideration. That is a great level to carry up. I supply the ideas above as general inspiration however clearly there are questions like the one you carry up the place a very powerful factor shall be working in honest good faith. I don?t know if greatest practices have emerged round issues like that, but I am sure that your job is clearly recognized as a good game. Each girls and boys really feel the impression of just a moment’s pleasure, for the remainder of their lives.

Thanks for the sensible critique. Me and my neighbor were just preparing to do a little research about this. We got a grab a book from our area library but I think I learned more clear from this post. I’m very glad to see such fantastic info being shared freely out there.

Its like you learn my thoughts! You seem to understand a lot approximately this, like you wrote the book in it or something. I feel that you just can do with some p.c. to drive the message home a little bit, but other than that, this is great blog. A fantastic read. I will certainly be back.

I truly appreciate this post. I’ve been looking everywhere for this! Thank goodness I found it on Bing. You have made my day! Thanks again

Some truly nice and useful information on this internet site, likewise I conceive the style has got fantastic features.

I wanted to thank you for this great read!! I definitely enjoying every little bit of it I have you bookmarked to check out new stuff you post…

Hey there! I’ve been following your web site for a while now and finally got the bravery to go ahead and give you a shout out from New Caney Texas! Just wanted to say keep up the excellent job!

I have been absent for some time, but now I remember why I used to love this site. Thanks, I?¦ll try and check back more often. How frequently you update your website?

Greetings from Ohio! I’m bored at work so I decided to browse your blog on my iphone during lunch break. I really like the knowledge you present here and can’t wait to take a look when I get home. I’m amazed at how quick your blog loaded on my mobile .. I’m not even using WIFI, just 3G .. Anyhow, great site!

Hello! This is kind of off topic but I need some guidance from an established blog. Is it very hard to set up your own blog? I’m not very techincal but I can figure things out pretty quick. I’m thinking about making my own but I’m not sure where to begin. Do you have any ideas or suggestions? Appreciate it

Very good written post. It will be beneficial to anyone who utilizes it, as well as me. Keep doing what you are doing – i will definitely read more posts.

It’s a pity you don’t have a donate button! I’d most certainly donate to this outstanding blog! I guess for now i’ll settle for bookmarking and adding your RSS feed to my Google account. I look forward to brand new updates and will talk about this blog with my Facebook group. Talk soon!

Yeah bookmaking this wasn’t a bad decision great post! .

Great web site. Lots of useful info here. I am sending it to several pals ans also sharing in delicious. And naturally, thank you in your effort!

whoah this blog is fantastic i love reading your posts. Keep up the great work! You know, a lot of people are hunting around for this information, you can aid them greatly.

My developer is trying to persuade me to move to .net from PHP. I have always disliked the idea because of the costs. But he’s tryiong none the less. I’ve been using Movable-type on numerous websites for about a year and am concerned about switching to another platform. I have heard good things about blogengine.net. Is there a way I can import all my wordpress content into it? Any kind of help would be really appreciated!

Aw, this was a really nice post. In thought I would like to put in writing like this moreover – taking time and actual effort to make a very good article… however what can I say… I procrastinate alot and by no means seem to get something done.

Hi, I think your site might be having browser compatibility issues. When I look at your website in Safari, it looks fine but when opening in Internet Explorer, it has some overlapping. I just wanted to give you a quick heads up! Other then that, fantastic blog!

Hello. impressive job. I did not imagine this. This is a impressive story. Thanks!

After study just a few of the weblog posts in your website now, and I actually like your way of blogging. I bookmarked it to my bookmark website checklist and can be checking again soon. Pls check out my web site as well and let me know what you think.

Военные тепловизоры часто защищены от ударов и выдерживают экстремальные условия.

Hiya! Quick question that’s entirely off topic. Do you know how to make your site mobile friendly? My web site looks weird when browsing from my iphone4. I’m trying to find a theme or plugin that might be able to resolve this problem. If you have any suggestions, please share. With thanks!

My brother suggested I may like this blog. He was once entirely right. This post actually made my day. You cann’t imagine just how a lot time I had spent for this information! Thank you!

Lovely just what I was looking for.Thanks to the author for taking his time on this one.

Hello! I know this is kinda off topic but I was wondering which blog platform are you using for this website? I’m getting tired of WordPress because I’ve had problems with hackers and I’m looking at options for another platform. I would be awesome if you could point me in the direction of a good platform.

Для охотников тепловизоры – это шанс увидеть то, что недоступно обычному зрению.

Feel free to surf to my site :: https://utahsyardsale.com/author/winniemancu/

I’ve been surfing on-line more than three hours nowadays, but I never discovered any interesting article like yours. It?¦s beautiful price sufficient for me. In my view, if all website owners and bloggers made good content material as you did, the web might be a lot more useful than ever before.

Today, I went to the beach with my children. I found a sea shell and gave it to my 4 year old daughter and said “You can hear the ocean if you put this to your ear.” She placed the shell to her ear and screamed. There was a hermit crab inside and it pinched her ear. She never wants to go back! LoL I know this is completely off topic but I had to tell someone!

Hey there! Someone in my Myspace group shared this website with us so I came to give it a look. I’m definitely loving the information. I’m book-marking and will be tweeting this to my followers! Outstanding blog and excellent style and design.

850849 33302I adore gathering valuable information, this post has got me even a lot more information! . 618977

Keep functioning ,remarkable job!

Outstanding post but I was wondering if you could write a litte more on this subject? I’d be very thankful if you could elaborate a little bit further. Thank you!

Well I definitely liked reading it. This information procured by you is very constructive for good planning.

I have recently started a web site, the information you provide on this site has helped me greatly. Thanks for all of your time & work.

С помощью тепловизоров можно вести наблюдение даже в самых густых зарослях.

my website :: https://bbarlock.com/index.php/User:KateFortier

Yay google is my world beater helped me to find this outstanding site! .

Whats up this is kinda of off topic but I was wondering if blogs use WYSIWYG editors or if you have to manually code with HTML. I’m starting a blog soon but have no coding expertise so I wanted to get advice from someone with experience. Any help would be greatly appreciated!

Keep working ,great job!

Hmm it looks like your website ate my first comment (it was extremely long) so I guess I’ll just sum it up what I had written and say, I’m thoroughly enjoying your blog. I too am an aspiring blog blogger but I’m still new to everything. Do you have any points for rookie blog writers? I’d certainly appreciate it.

Thank you for another informative blog. Where else could I get that kind of information written in such a perfect way? I’ve a project that I’m just now working on, and I have been on the look out for such information.

There is noticeably a bundle to know about this. I assume you made certain nice points in features also.

Hello there, You’ve done a fantastic job. I’ll certainly digg it and personally suggest to my friends. I’m confident they’ll be benefited from this web site.

This internet site is my aspiration, real good style and perfect written content.

Thanks for some other informative web site. The place else could I get that kind of info written in such a perfect method? I’ve a project that I am simply now operating on, and I have been on the look out for such information.

hi!,I like your writing very much! share we communicate more about your post on AOL? I require a specialist on this area to solve my problem. May be that’s you! Looking forward to see you.

I conceive you have remarked some very interesting details, thanks for the post.

Regards for this wondrous post, I am glad I found this site on yahoo.

I’m extremely inspired with your writing talents and also with the structure in your weblog. Is this a paid topic or did you modify it your self? Either way keep up the nice quality writing, it is uncommon to look a nice weblog like this one today..

I truly appreciate this post. I have been looking everywhere for this! Thank goodness I found it on Bing. You have made my day! Thank you again

hey there and thank you for your information – I have definitely picked up something new from right here. I did however expertise some technical issues using this web site, as I experienced to reload the web site many times previous to I could get it to load correctly. I had been wondering if your web host is OK? Not that I’m complaining, but sluggish loading instances times will very frequently affect your placement in google and could damage your high quality score if advertising and marketing with Adwords. Anyway I am adding this RSS to my e-mail and can look out for a lot more of your respective exciting content. Make sure you update this again very soon..

I like this site very much so much fantastic information.

Hi there! This is my first visit to your blog! We are a collection of volunteers and starting a new initiative in a community in the same niche. Your blog provided us useful information to work on. You have done a outstanding job!

Its excellent as your other posts : D, thankyou for posting. “Even Albert Einstein reportedly needed help on his 1040 form.” by Ronald Reagan.

Простота использования тепловизоров делает их доступными даже для новичков.

Also visit my web-site https://turkbellek.org/index.php/Teplovizor_30g

I used to be very happy to search out this net-site.I wished to thanks on your time for this excellent learn!! I positively having fun with every little little bit of it and I have you bookmarked to check out new stuff you weblog post.

I as well believe thus, perfectly composed post! .

I gotta favorite this website it seems invaluable very helpful

Hello! This is kind of off topic but I need some help from an established blog. Is it tough to set up your own blog? I’m not very techincal but I can figure things out pretty quick. I’m thinking about creating my own but I’m not sure where to begin. Do you have any tips or suggestions? Thank you

Dead written subject matter, regards for entropy. “The earth was made round so we would not see too far down the road.” by Karen Blixen.

you may have a terrific weblog right here! would you prefer to make some invite posts on my weblog?

Hi, just required you to know I he added your site to my Google bookmarks due to your layout. But seriously, I believe your internet site has 1 in the freshest theme I??ve came across. It extremely helps make reading your blog significantly easier.

I would like to thnkx for the efforts you have put in writing this blog. I am hoping the same high-grade blog post from you in the upcoming as well. In fact your creative writing abilities has inspired me to get my own blog now. Really the blogging is spreading its wings quickly. Your write up is a good example of it.

Awsome site! I am loving it!! Will come back again. I am bookmarking your feeds also

After research a couple of of the blog posts in your website now, and I really like your way of blogging. I bookmarked it to my bookmark website checklist and will probably be checking again soon. Pls take a look at my site as well and let me know what you think.

You have brought up a very excellent details , regards for the post.

You really make it appear so easy together with your presentation however I in finding this topic to be really something that I think I’d never understand. It seems too complicated and extremely large for me. I am looking ahead for your next post, I?¦ll attempt to get the cling of it!

Sweet blog! I found it while searching on Yahoo News. Do you have any suggestions on how to get listed in Yahoo News? I’ve been trying for a while but I never seem to get there! Appreciate it

Wow! This could be one particular of the most helpful blogs We’ve ever arrive across on this subject. Actually Great. I’m also an expert in this topic therefore I can understand your effort.

Would you be interested in exchanging hyperlinks?

Heya i’m for the first time here. I came across this board and I find It really useful & it helped me out a lot. I’m hoping to give something back and aid others such as you aided me.

I do not even know how I stopped up here, however I believed this publish was great. I do not understand who you are however certainly you are going to a well-known blogger when you are not already 😉 Cheers!

I’ve been absent for some time, but now I remember why I used to love this site. Thank you, I will try and check back more frequently. How frequently you update your web site?

Wonderful paintings! That is the type of information that should be shared around the net. Disgrace on Google for now not positioning this submit higher! Come on over and consult with my web site . Thank you =)

Great – I should certainly pronounce, impressed with your web site. I had no trouble navigating through all the tabs and related info ended up being truly easy to do to access. I recently found what I hoped for before you know it at all. Quite unusual. Is likely to appreciate it for those who add forums or anything, site theme . a tones way for your client to communicate. Nice task..

Great site. A lot of useful info here. I’m sending it to a few friends ans also sharing in delicious. And of course, thanks for your sweat!

Hi there, I discovered your web site by way of Google at the same time as searching for a comparable topic, your site got here up, it appears to be like good. I have bookmarked it in my google bookmarks.

I like this web blog its a master peace ! Glad I noticed this on google .

I am very happy to read this. This is the type of manual that needs to be given and not the accidental misinformation that’s at the other blogs. Appreciate your sharing this greatest doc.

I?¦ll right away grab your rss as I can not find your e-mail subscription link or newsletter service. Do you have any? Please permit me recognise so that I could subscribe. Thanks.

Some truly tremendous work on behalf of the owner of this web site, absolutely great articles.

hey there and thank you for your info – I have definitely picked up anything new from right here. I did however expertise some technical points using this website, since I experienced to reload the web site many times previous to I could get it to load correctly. I had been wondering if your hosting is OK? Not that I’m complaining, but slow loading instances times will sometimes affect your placement in google and can damage your high quality score if advertising and marketing with Adwords. Anyway I’m adding this RSS to my email and can look out for much more of your respective intriguing content. Ensure that you update this again soon..

I got good info from your blog

I am really loving the theme/design of your website. Do you ever run into any internet browser compatibility problems? A handful of my blog audience have complained about my website not operating correctly in Explorer but looks great in Opera. Do you have any advice to help fix this issue?

This website is really a stroll-by for all the data you wished about this and didn’t know who to ask. Glimpse right here, and you’ll positively uncover it.

I am usually to running a blog and i actually appreciate your content. The article has really peaks my interest. I’m going to bookmark your site and maintain checking for new information.

I¦ve been exploring for a bit for any high quality articles or blog posts in this kind of house . Exploring in Yahoo I at last stumbled upon this site. Studying this info So i am happy to convey that I’ve an incredibly just right uncanny feeling I found out just what I needed. I so much surely will make sure to do not put out of your mind this website and provides it a look on a constant basis.

I got what you intend,saved to bookmarks, very decent web site.

Great line up. We will be linking to this great article on our site. Keep up the good writing.

We are a bunch of volunteers and opening a new scheme in our community. Your website offered us with useful info to paintings on. You have done a formidable process and our whole neighborhood will likely be thankful to you.

Definitely imagine that which you said. Your favorite reason appeared to be on the net the simplest factor to take note of. I say to you, I definitely get annoyed at the same time as folks consider worries that they just don’t realize about. You managed to hit the nail upon the highest as smartly as outlined out the entire thing without having side-effects , other folks could take a signal. Will probably be back to get more. Thanks

В тумане или в темноте тепловизор незаменим как для охотников, так и для военных.

Also visit my homepage: https://pastoralcaremission.org/bbs/board.php?bo_table=free&wr_id=2382944

After I initially commented I clicked the -Notify me when new comments are added- checkbox and now each time a comment is added I get four emails with the identical comment. Is there any method you possibly can take away me from that service? Thanks!

Hi! I know this is kinda off topic but I was wondering if you knew where I could locate a captcha plugin for my comment form? I’m using the same blog platform as yours and I’m having problems finding one? Thanks a lot!

I have been absent for some time, but now I remember why I used to love this blog. Thanks , I’ll try and check back more often. How frequently you update your web site?

I keep listening to the newscast speak about getting boundless online grant applications so I have been looking around for the best site to get one. Could you tell me please, where could i get some?

Great website you have here but I was wanting to know if you knew of any discussion boards that cover the same topics discussed here? I’d really love to be a part of group where I can get comments from other knowledgeable individuals that share the same interest. If you have any suggestions, please let me know. Appreciate it!

Very interesting info!Perfect just what I was looking for!

Would you be interested in exchanging links?

I have not checked in here for a while as I thought it was getting boring, but the last several posts are good quality so I guess I?¦ll add you back to my daily bloglist. You deserve it my friend 🙂

After study a few of the blog posts on your website now, and I truly like your way of blogging. I bookmarked it to my bookmark website list and will be checking back soon. Pls check out my web site as well and let me know what you think.

Some really interesting information, well written and loosely user genial.

I really like your writing style, good information, thanks for putting up : D.

Enjoyed reading through this, very good stuff, appreciate it.

I wanted to thank you for this great read!! I definitely enjoying every little bit of it I have you bookmarked to check out new stuff you post…

I am not certain where you’re getting your info, however great topic. I needs to spend a while finding out much more or working out more. Thank you for great info I used to be looking for this info for my mission.

What i do not understood is actually how you’re not actually much more well-liked than you might be right now. You’re so intelligent. You realize thus considerably relating to this subject, produced me personally consider it from numerous varied angles. Its like men and women aren’t fascinated unless it is one thing to accomplish with Lady gaga! Your own stuffs great. Always maintain it up!

A person essentially help to make seriously articles I’d state. That is the first time I frequented your web page and thus far? I surprised with the research you made to make this actual publish extraordinary. Wonderful task!

We are a group of volunteers and opening a new scheme in our community. Your web site provided us with valuable information to work on. You’ve done a formidable job and our whole community will be thankful to you.

Thanks for any other informative blog. Where else could I get that type of information written in such a perfect way? I’ve a venture that I’m just now operating on, and I’ve been on the look out for such information.

I don’t even know how I ended up here, but I thought this post was good. I don’t know who you are but definitely you are going to a famous blogger if you aren’t already 😉 Cheers!

Some really fantastic posts on this website , appreciate it for contribution.

As a Newbie, I am continuously searching online for articles that can be of assistance to me. Thank you

Just what I was searching for, thanks for putting up.

I truly appreciate this post. I?¦ve been looking everywhere for this! Thank goodness I found it on Bing. You have made my day! Thank you again

When I originally commented I clicked the -Notify me when new comments are added- checkbox and now each time a comment is added I get four emails with the same comment. Is there any way you can remove me from that service? Thanks!

Great post. I am facing a couple of these problems.