This is our best Month In Macro yet, with 45 pages of macro, markets, & signals. Our offering is now without peer in terms of depth, breadth, and granularity. We will soon be migrating from this platform, and to make sure we have you on our mailing list in the future, please subscribe below so we can continue to bring you our work.

This report is part of our ongoing effort to provide economic and market guidance to our subscribers during a period of historic levels of uncertainty. This note aims to share our research team’s internal checkpoint process in evaluating the current state of the economy as it pertains to markets. The pages that follow will have familiar content for those who follow our work, but with the added benefit of our connecting the dots across all the economic and financial data that our systems use to make portfolio decisions. Our primary takeaways are as follows:

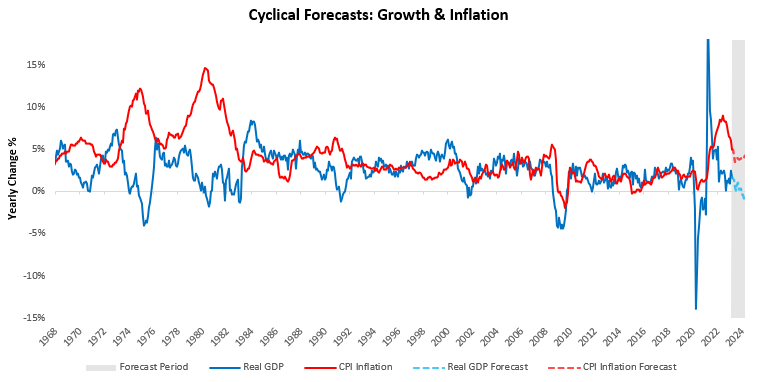

- Nominal GDP slowed through April, with real GDP contracting by -0.47% and inflation rising by 0.23%. Nominal GDP has grown approximately 4.7% from one year prior, continuing the downtrend beginning in February 2022.

- During this time, equity markets have posed significant strength (though lopsided), while treasury markets have weakened in unison.

- Looking forward, these sequential improvements have adjusted our real growth outlook, with a contraction in yearly real GDP growth more likely in H1 2024 than in Q4 2023. Our inflation outlook remains one of resilient inflation.

- Neither stocks nor bonds offer attractive return-on-risk here. Stocks remain highly exposed to weakness in the economic growth cycle, while bonds likely face headwinds from higher rates to combat resilient inflation. Cash remains an attractive hiding place for most investors.

While recent tailwinds to 60/40 portfolios in the form of disinflation (which we were ahead of) and AI innovations (which we were offside) have helped traditional investors, our outlook suggests that those tailwinds will likely prove transitory. Below, we show the visualization of our expectations for growth and inflation over the next twelve months.

To dive in, click the link below:

Month In Macro – May Edition

I am really impressed with your writing abilities

and also with the structure for your blog.

Is that this a paid theme or did you customize it

your self? Anyway stay up the excellent quality writing,

it’s rare to look a nice blog like this one nowadays. TikTok ManyChat!