At Prometheus, we are committed to equipping our clients with the most granular, high-frequency, and actionable understanding of macro conditions in the industry. We offer our clients a range of research solutions, from big-picture macro themes to actionable trading signals. In the spirit of giving back to the community, we are excited to offer an All-Access week in our Institutional Services. Each day this week, we will unveil one product offering from our extensive Institutional Offering. If you’re interested in institutional access, please contact us at info@prometheus-research.com.

Welcome to Prometheus Asset Allocation. The Prometheus Asset Allocation program offers a stable, macro-focused approach to asset management. Prometheus Asset Allocation aims to outperform a traditional stock and bond portfolio by leveraging our proprietary systematic macro process to rotate between 3 ETFs monthly (plus cash). As part of the program, we will be sharing our views on Growth, Inflation, and Liquidity in addition to our monthly video updates.

Our primary takeaways are as follows:

- Liquidity is driven by both private and public sources. Currently, private sources continue to be the dominant players in the liquidity ecosystem.

- Reserve balances and commercial paper issuance remain neutral; bill issuance has slowed down but remains elevated; and repo activity remains extremely strong.

- Overall, liquidity dynamics in the US remain stable, supporting all assets.

Recent market conditions have shown significant volatility, with markets experiencing the fallout of global de-risking of fast-money portfolios. Scanning through the liquidity system, we see little deterioration in liquidity conditions that could propagate a self-reinforcing downturn in asset markets.

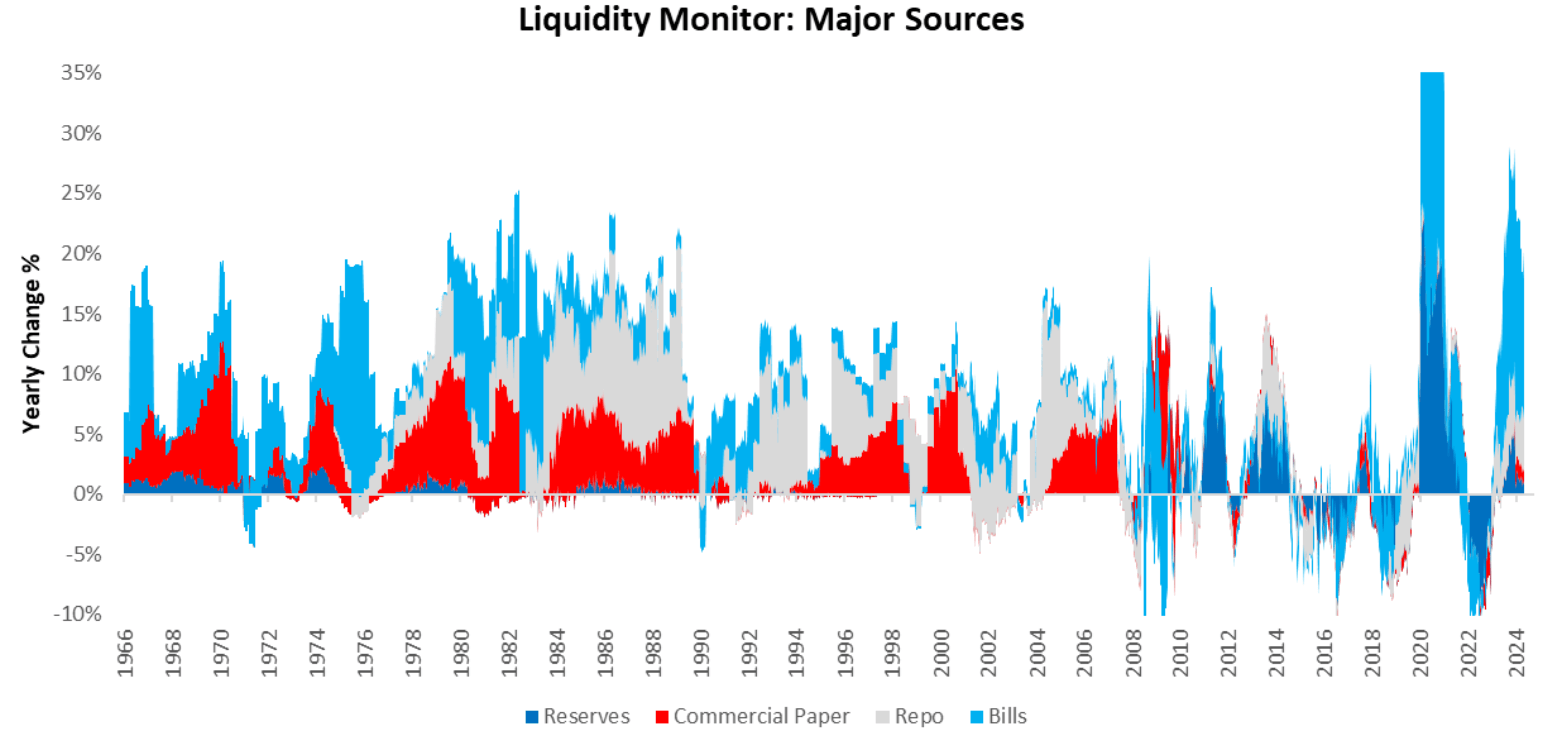

Liquidity is the flow of cash and cash-like assets that potentiate spending in the economy. Liquidity is determined by nominal dollar values and the relative risk profile of the various sources of liquidity. We begin our tracking of liquidity conditions by sharing the weighted growth rate of the major sources of liquidity: reserves, treasury bills, commercial paper, & repurchase agreements. As we can see below, the current liquidity dynamics are primarily driven by repo conditions after being dominated by treasury bill issuance.

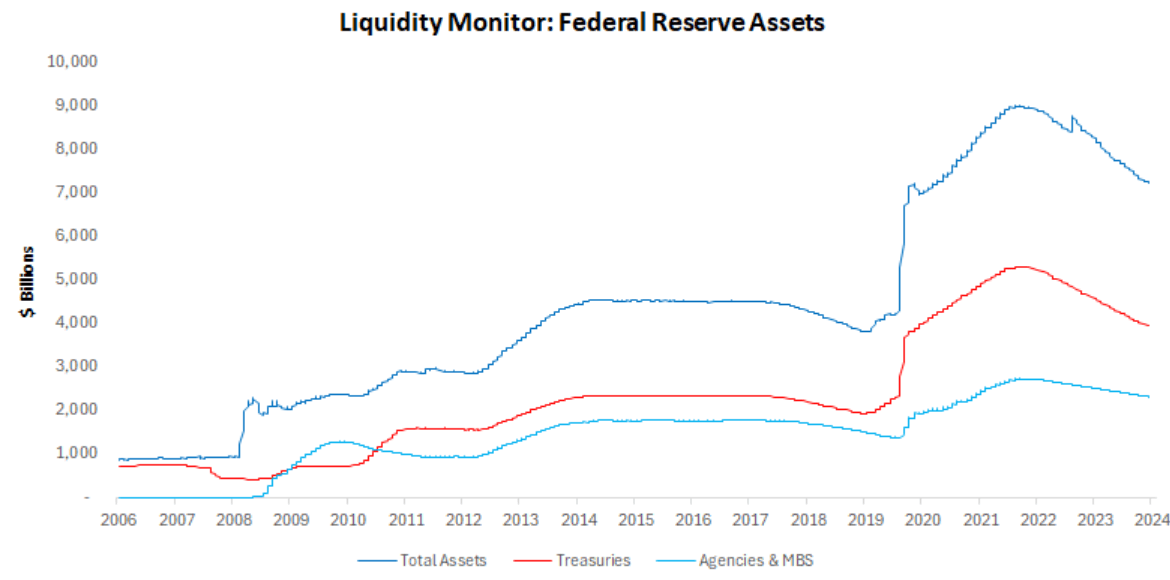

We zoom on each of these components, starting with reserve balances. Reserve balances held by financial institutions at the Fed are a function of the gross liquidity supplied by the Fed through the asset side of their balance sheet, relative to the gross liquidity absorbed by inflows into the liability side of their balance sheet. As we can see below, the current trend in reserve assets has been declining as the Fed engages in its QT program. However, while the asset side is declining, the Fed liabilities, particularly the reverse repo have been declining faster.

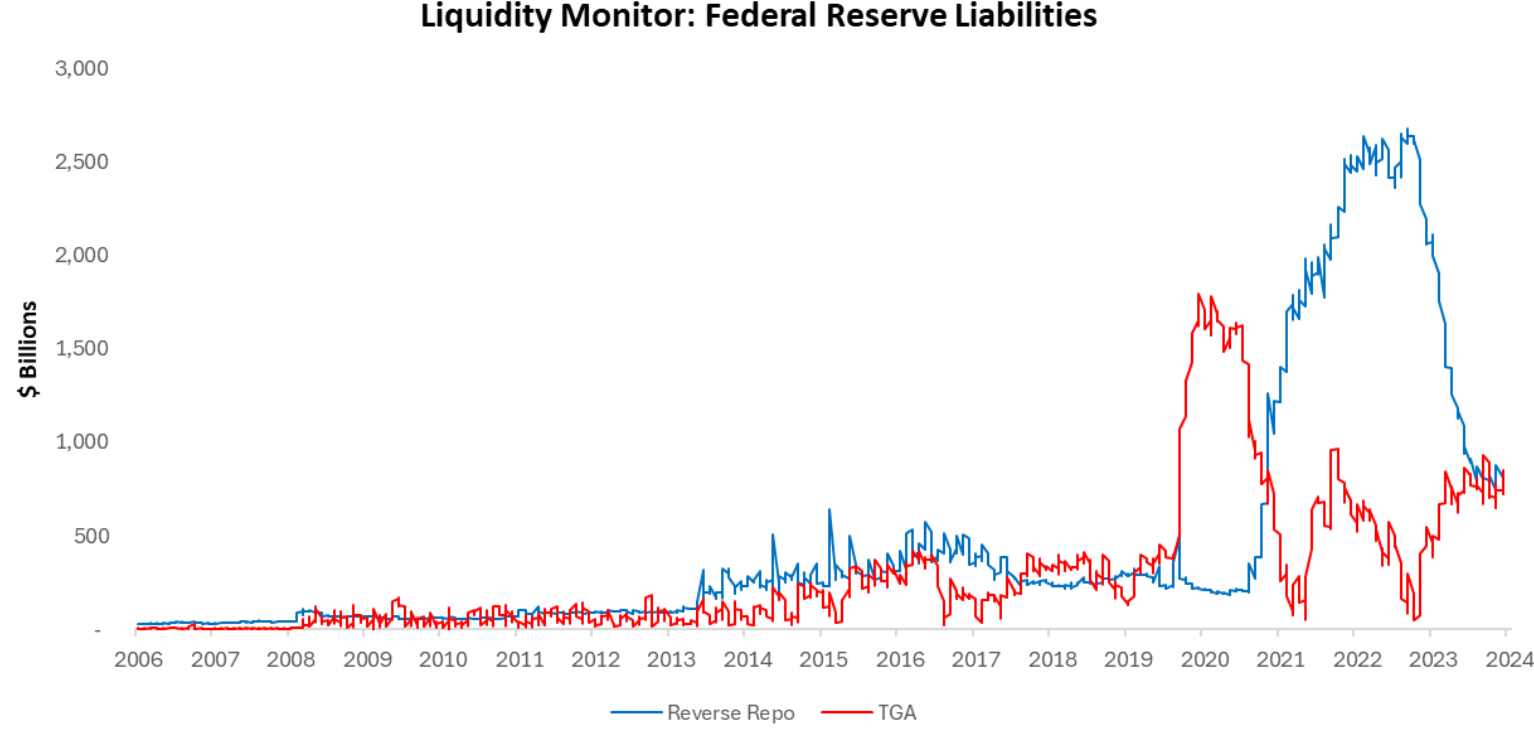

Additionally, we examine the changes in major liabilities of the Fed, i.e. the liquidity drains on the financial sector:

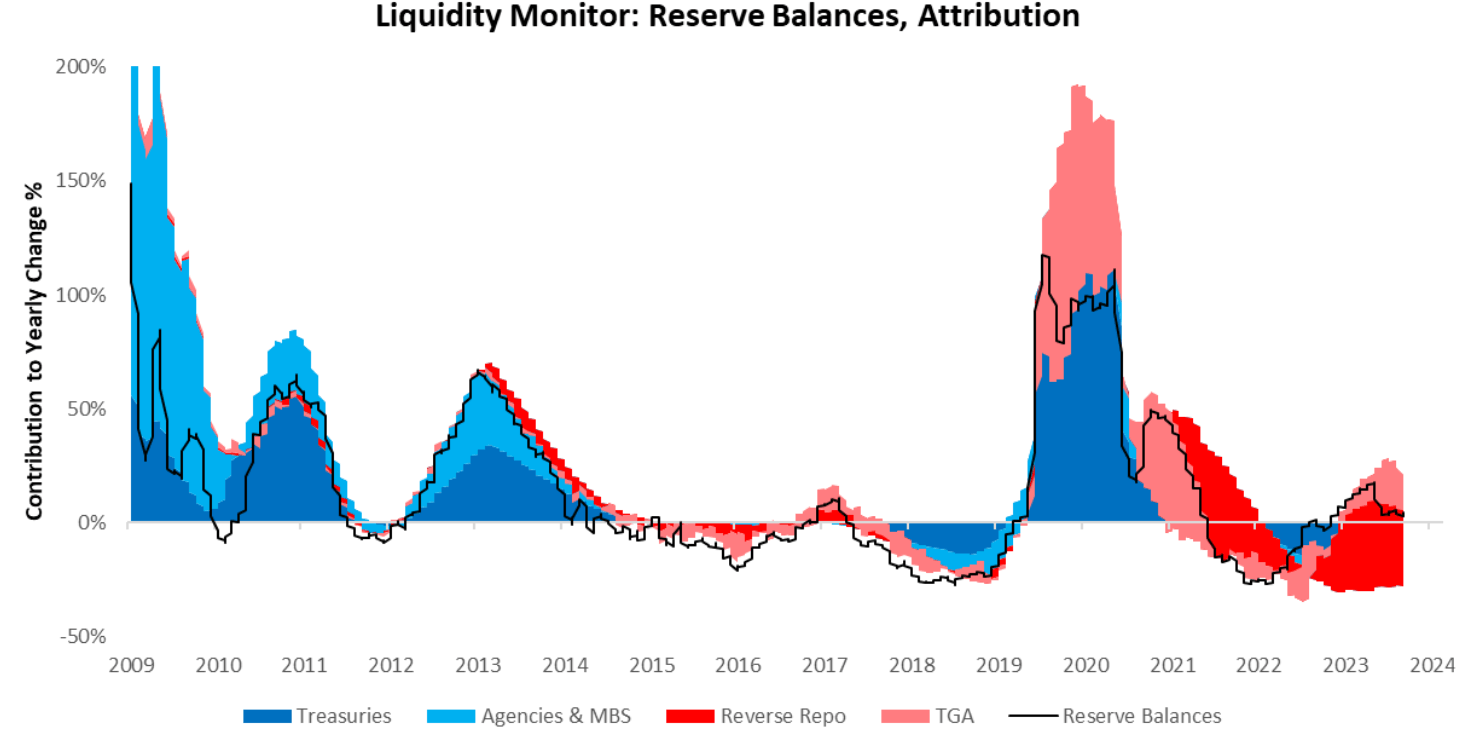

We combine these perspectives to show the drivers of changes in reserve balances over time. While the Fed has decreased its assets, the outflows of its liabilities through reverse repo have made reserve balances resilient to the Fed’s QT program. This has led to the neutral growth of reserves.

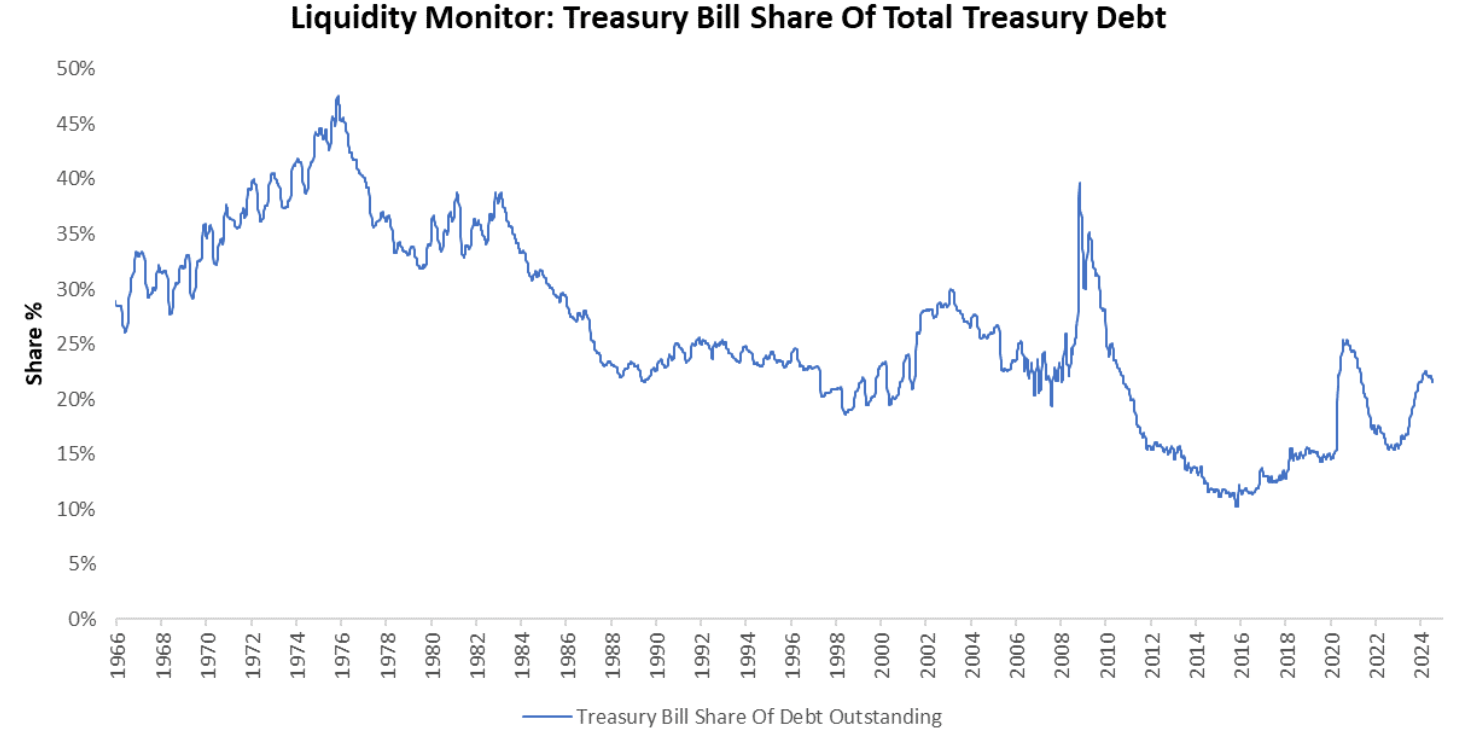

Next, we turn to the other side of government liquidity, i.e., Treasury bill supply. Much like the Fed, the treasury can impact liquidity conditions by increasing the supply of liquid assets, primarily through treasury bill issuance. We begin by showing the secular context for this liquidity supply by showing the treasury bills outstanding as a share of total treasury debt. Post-COVID-19, we have entered a regime of higher bill supply compared to the pre-existing conditions.

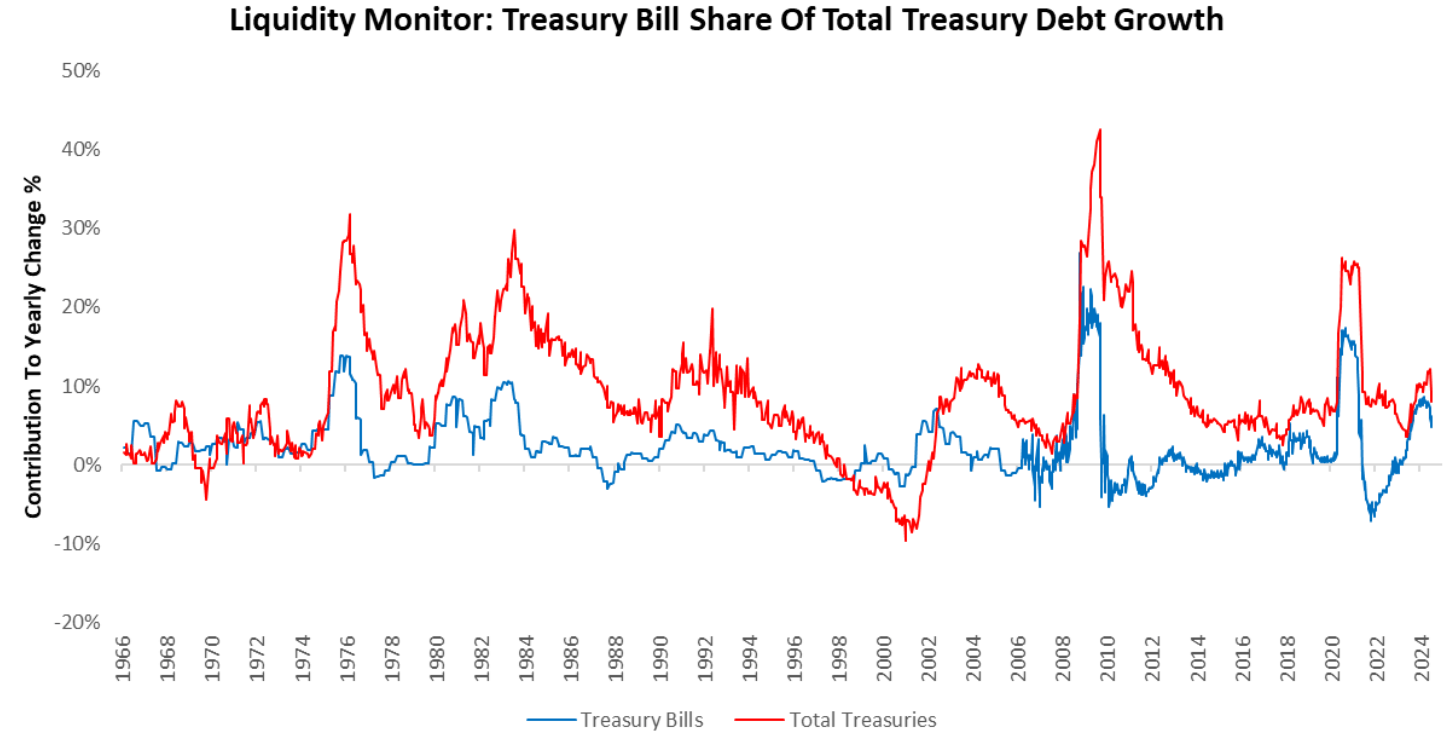

For a timelier perspective, we examine the contribution of treasury bill growth to total treasury debt growth over time. Again, we observe that even at a delta level, bill supply continues to be the primary driver of total treasury debt growth.

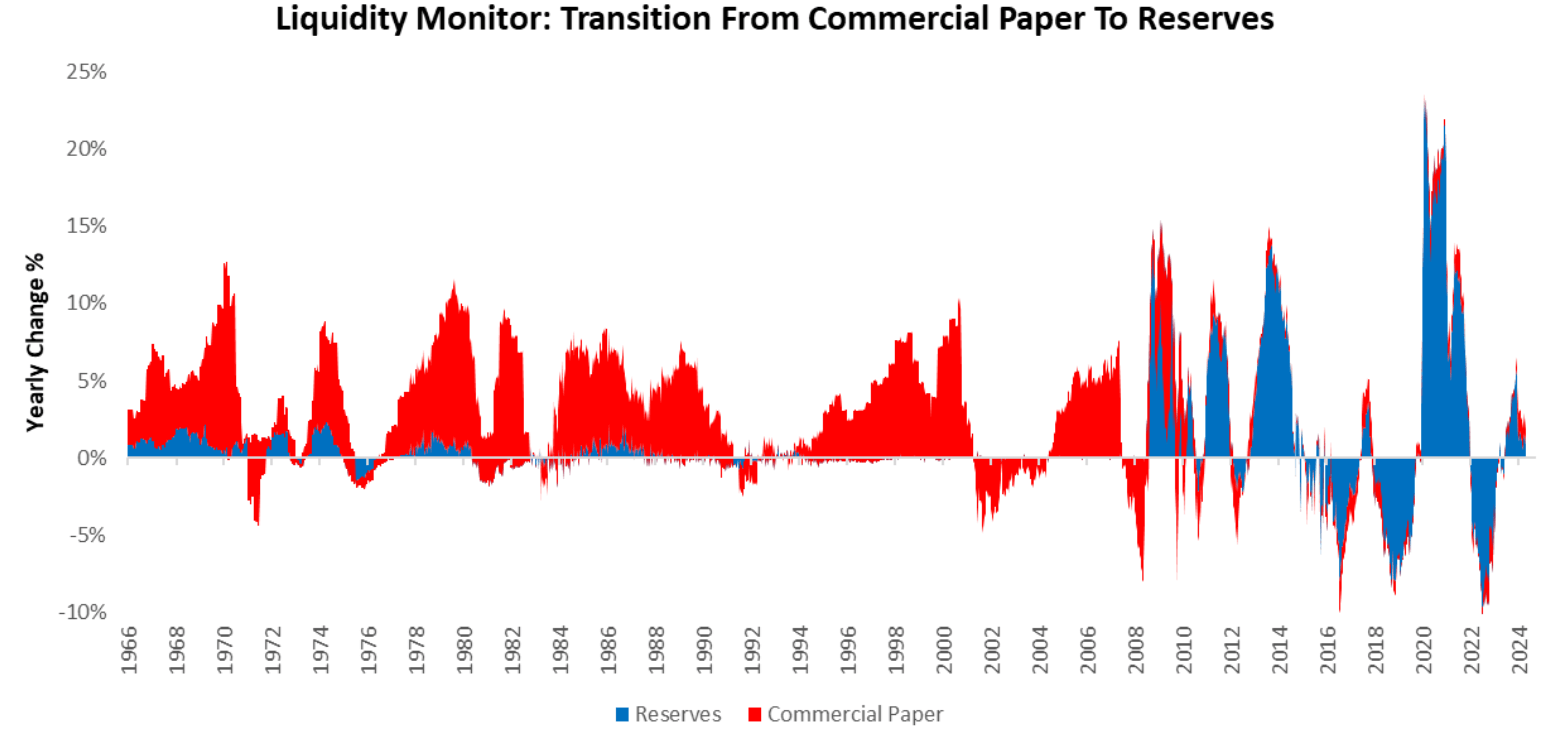

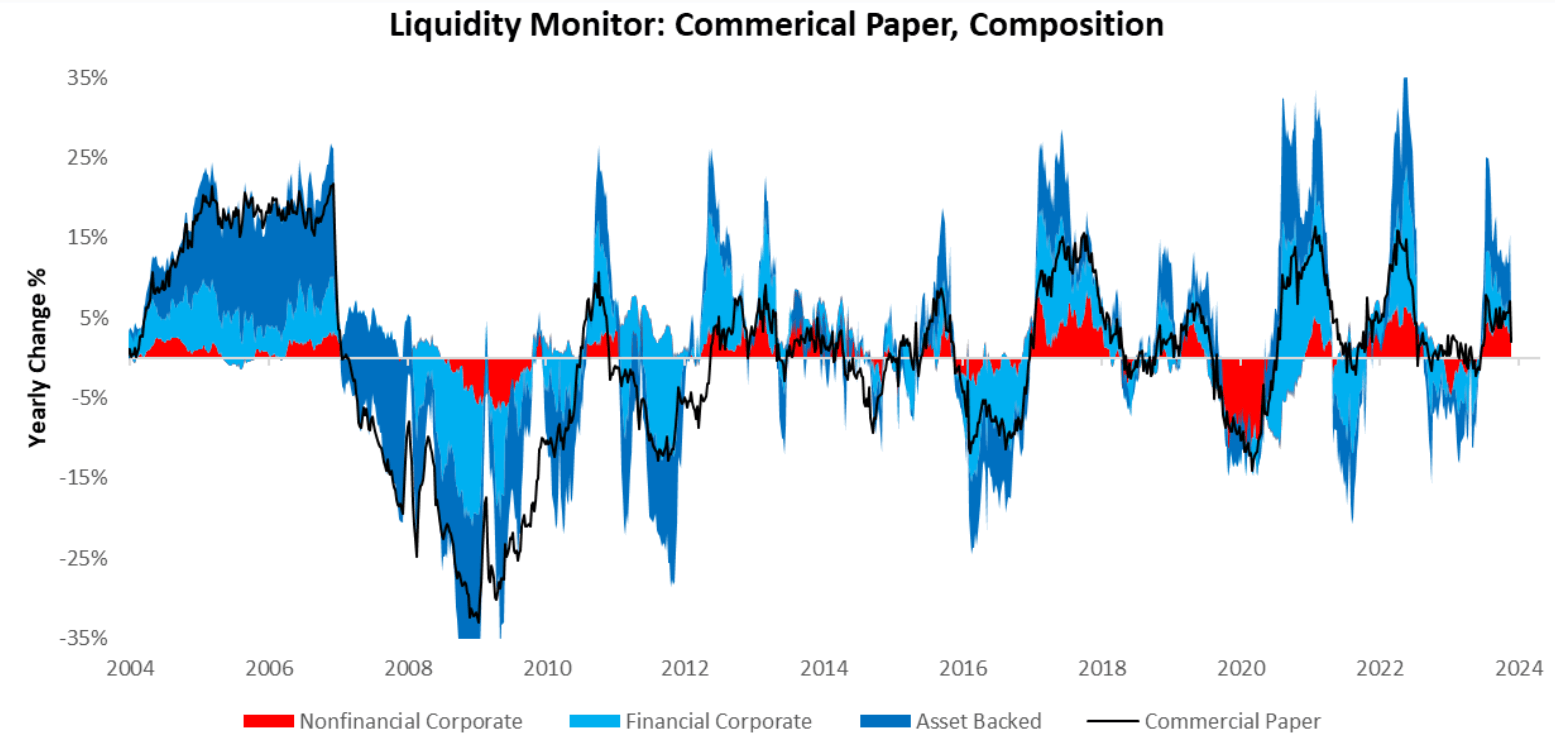

Now that we have looked through the primary government sources of liquidity, we now turn to the private sector. We begin with commercial paper markets. During the financial crisis, commercial paper markets were replaced by reserves as the primary receptacle to store short-term liquid assets. Nonetheless, commercial paper remains a mechanical driver of the liquidity ecosystem. We visualize the transition from commercial paper to reserves:

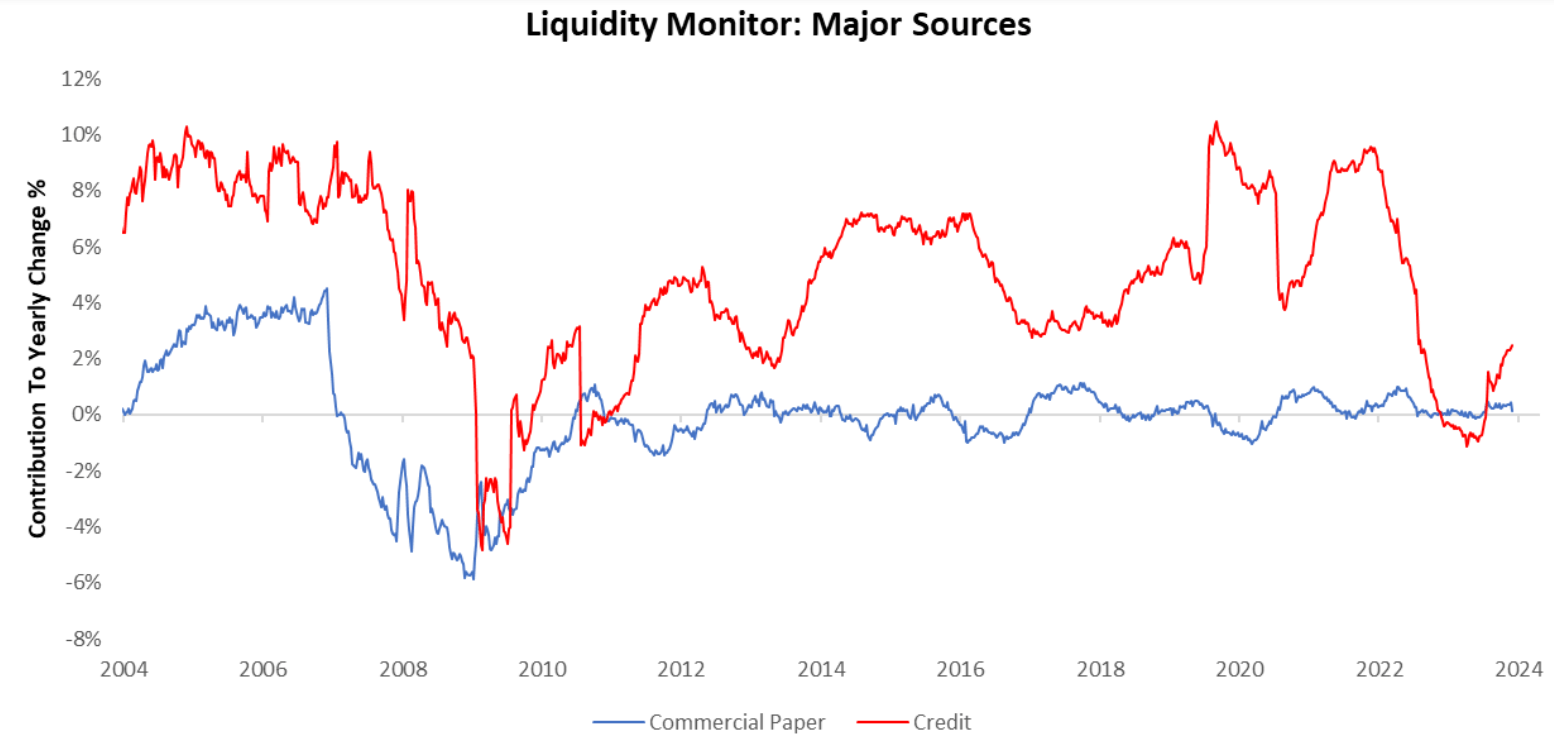

To further contextualize commercial paper activity, we compare the growth of commercial paper to total bank credit. The recent growth in commercial paper relative to overall credit growth remains subdued.

Additionally, we examine the composition of the commercial paper market, grouped into financial, nonfinancial, and asset-backed issuers. Historically, financial & asset-backed issuers have dominated commercial paper growth:

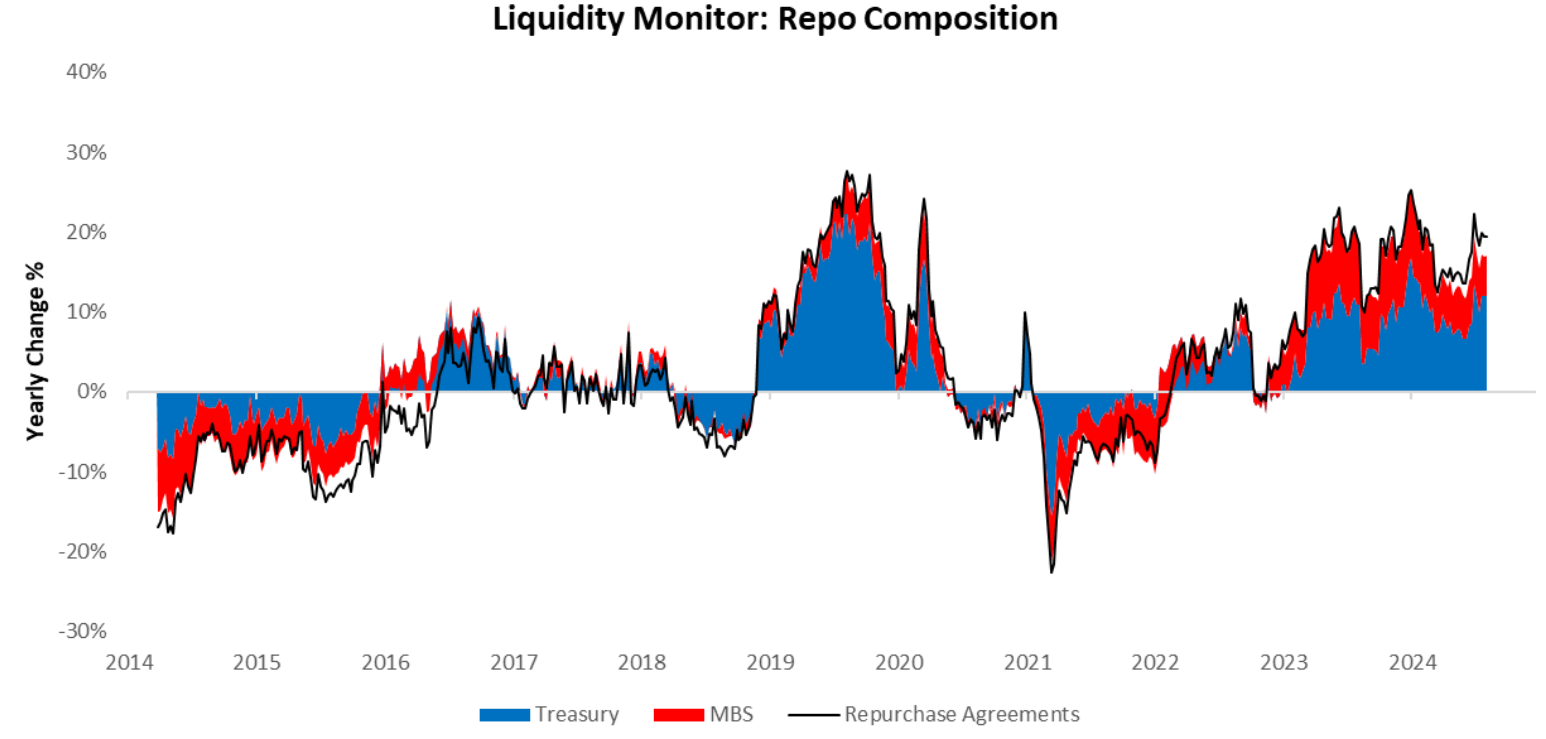

While private sector activity in the form of commercial paper has dwindled, other forms of private sector activity have flourished. Particularly, repo markets have expanded to become a dominant driver of financial markets. Repo market activity is largely contingent upon the collateral supply, particularly in the form of Treasury & MBS securities. We show the composition of repo growth below:

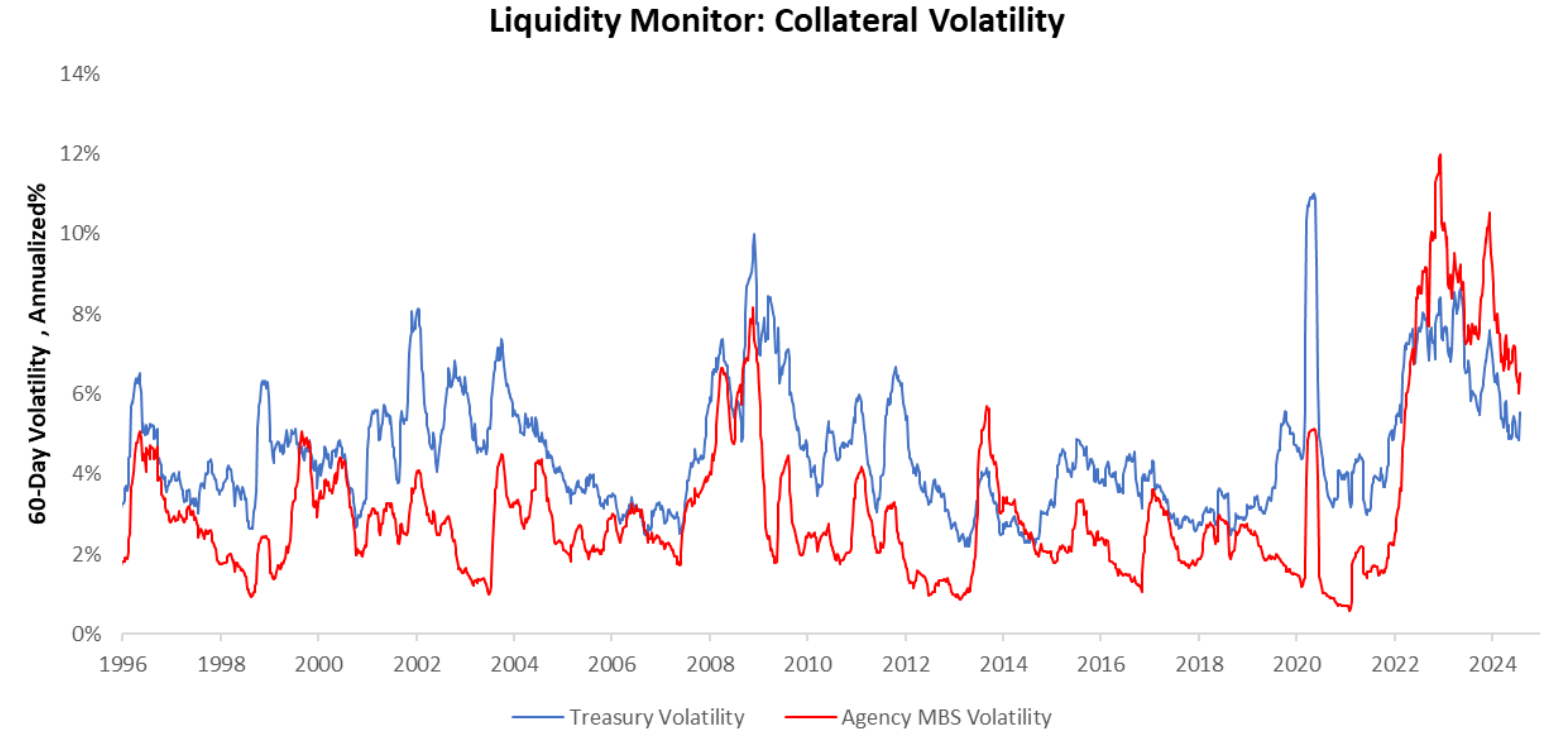

For a further understanding of the drivers of repo activity, we examine the volatility of the underlying collateral, i.e., the volatility of Treasury & Agency MBS. As we can see below, trends in both of these variables are mean-reverting to their historical averages as we head towards to potential easing cycle.

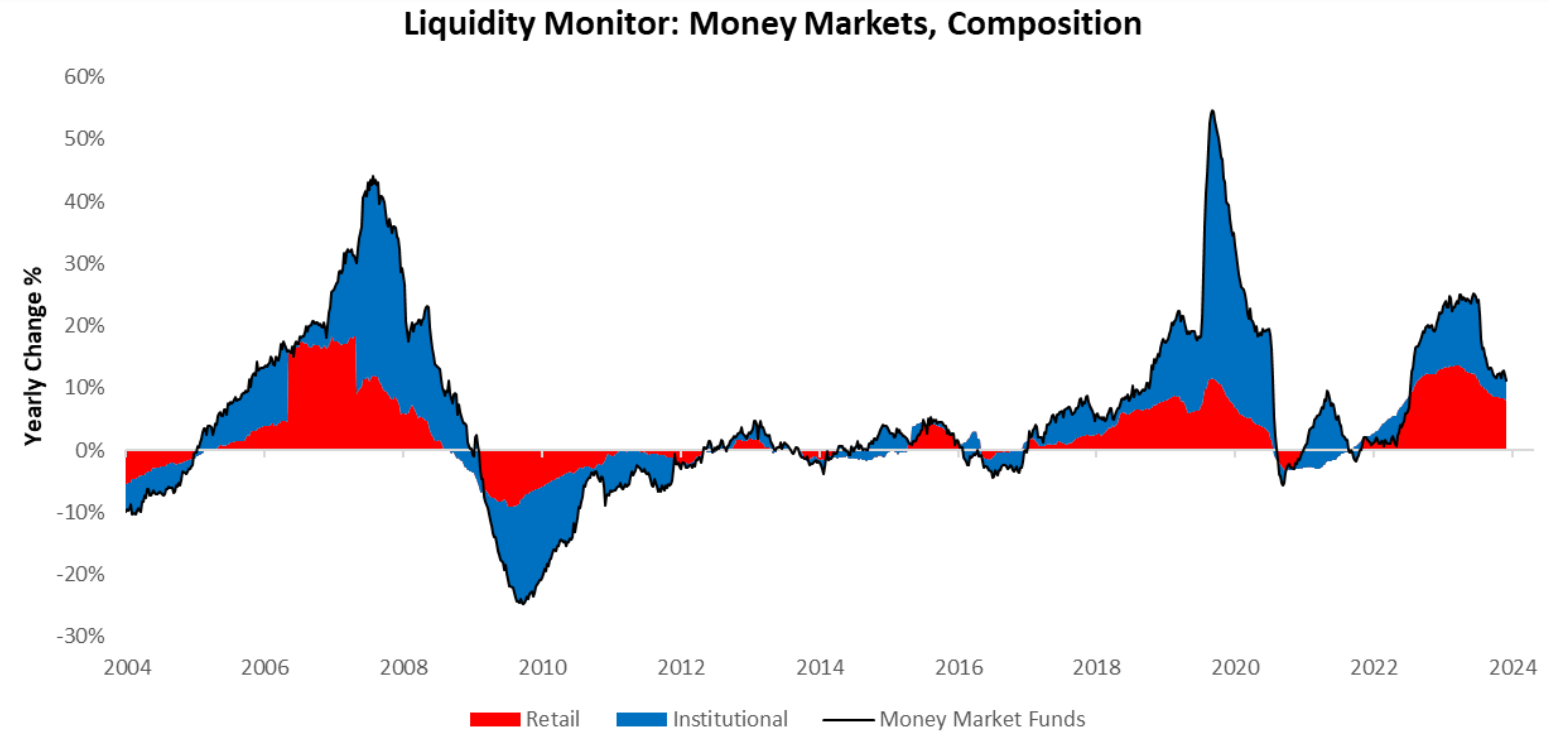

While collateral quality is essential to create a supportive backdrop for repo activity, we can gain a further understanding of the drivers of repo by examining the primary source of funds for repo activity – money market funds. Retail MMFs have been the primary source of funds for the recent change in repo activity. Below, we visualize the growth of money market funds, along with its composition:

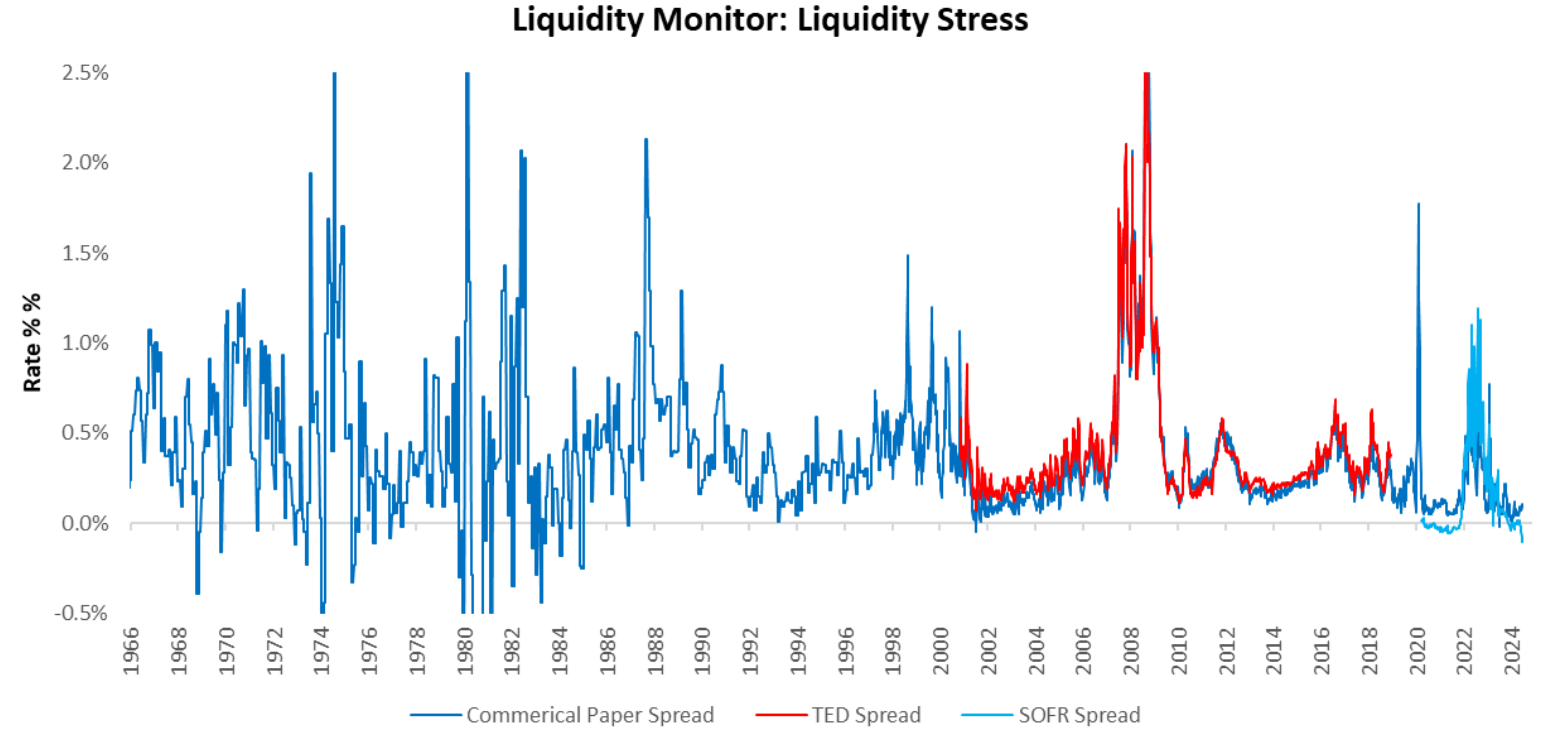

Now that we have examined all big-picture drivers of liquidity dynamics, we conclude by examining timely measures of liquidity stress in the form of short-term spreads. A widening of spreads will impact private sector credit creation and liquidity conditions. Stability in these spreads continues to support ongoing liquidity creation. Currently, these spreads remain stable.

Overall, reserve balances and commercial paper issuance remain neutral; bill issuance has slowed down but remains elevated; and repo activity remains extremely strong. Overall, liquidity dynamics in the US remain stable, supporting all assets. Until next time.

8 thoughts on “Liquidity Views”

Muchas gracias. ?Como puedo iniciar sesion?

cost generic clomid for sale clomid only cycle buying clomiphene price where to get generic clomid pill can i get cheap clomid no prescription clomiphene price uk can i purchase clomiphene without insurance

This is the type of advise I unearth helpful.

More delight pieces like this would insinuate the интернет better.

zithromax tablet – order ciprofloxacin 500mg without prescription metronidazole 200mg pills

buy domperidone pills – domperidone pill buy cyclobenzaprine online cheap

buy cheap generic propranolol – methotrexate drug methotrexate ca

where can i buy amoxicillin – order ipratropium 100mcg for sale buy combivent 100mcg pill