Today, we will provide updates on our ETF Strategy. Our ETF Strategy algorithmically employs our systematic analysis of the US economy and financial markets to create a rules-based, quantitative portfolio. At Prometheus,, we focus on understanding the underlying mechanics that drive market environments. We use fundamental economic and high-frequency financial data to understand these macroeconomic environments and codify how to best trade markets. This process creates a robust portfolio solution that attempts to provide high return/risk characteristics and high percentage positive ratios at the portfolio level, regardless of the economic environment. Subscribe below so that you never miss out on our systematic insights into markets and portfolio strategy:

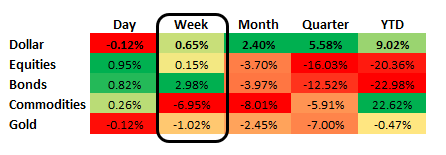

Over the last week, markets have moved to price tightening liquidity across asset classes, outweighing concerns over stagflation. Equities found modest support, though they traded in a choppy fashion. The dollar and treasuries remained bid, with strong price rises in treasuries. Gold continues to struggle, despite a fundamental backdrop that remains fairly supportive.

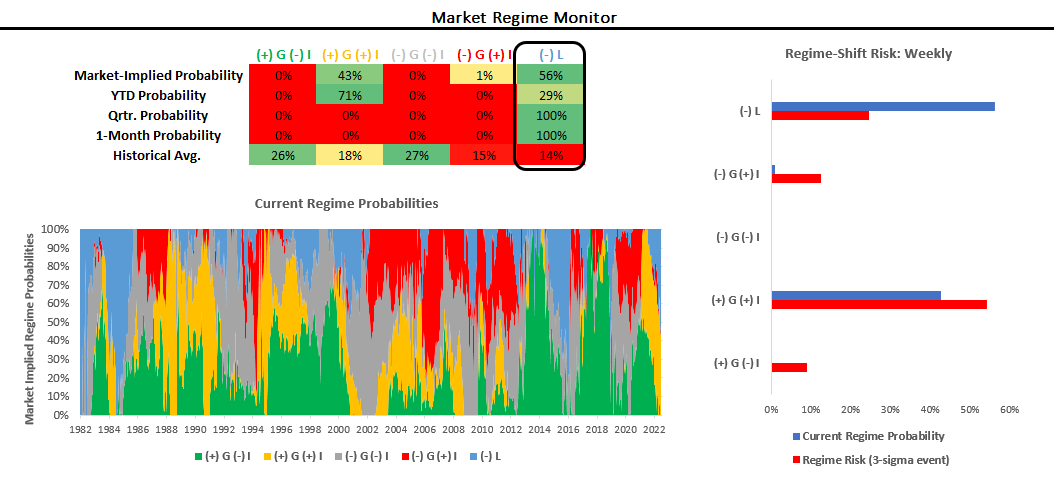

In line with these market moves, our market-implied regime monitors continue to show a dominance of tightening liquidity in market pricing. We highlight below how this pricing is consistent across durations:

Periods of tightening liquidity, i.e., environments where monetary & fiscal authorities contract the supply of high-quality collateral assets, are typically short but extremely painful for pro-cyclical assets like stocks and commodities. During these periods, yield curves flatten, the dollar rises, risk premia rise, & the outlook for economic growth remains bleak. These dynamics can last as long as the US Sovereign (Fed & Treasury) can remain resolute in tightening liquidity conditions. We expect policymakers will not be able to stay resolute in the face of contractionary forces that are building up in the economy; however, we will rely on our systems to guide the way on this front.

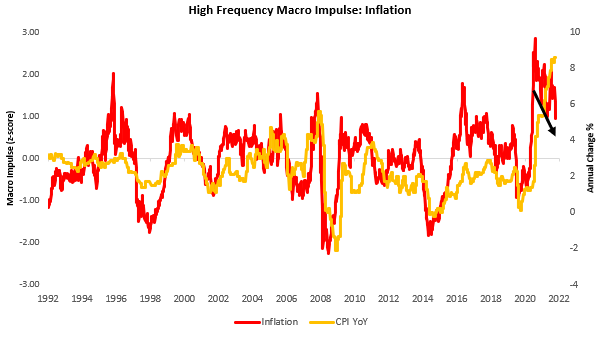

We think what is particularly important to note is that these tightening liquidity dynamics are coming alongside a decelerating inflation impulse. We show our proprietary High-Frequency Inflation measures below:

Our tracking of inflation pressures shows that inflation momentum has waned, i.e., inflation is running at a slower clip than earlier this year. While these rate of change metrics matter, the level of inflation plays an important role. If we settle at these inflation levels, we could see sustained support for commodities, significantly less than earlier this year. We expect inflation to be curbed through slowing demand, and we look like we are in a transitioning environment. Still, our systems are yet to confirm any significant asset allocation pivots.

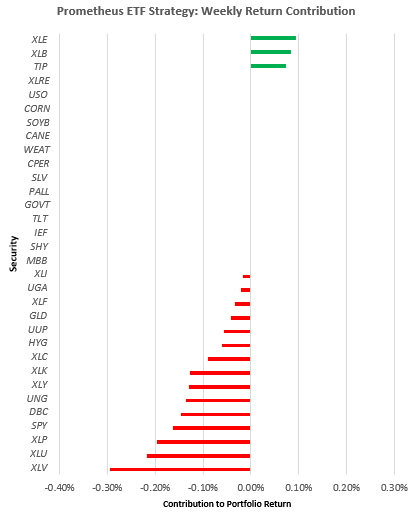

Turning to the ETF Strategy, these fast-moving dynamics caught our systems off-guard this week, particularly with the significant moves in the commodity complex. With our systems conviction on the stagflationary impulse prevalent in markets, we remained allocated long commodities, and short equities resulting in portfolio losses. We show the week-to-date portfolio returns for the ETF Strategy below:

These market moves led to an unlevered loss of 2.5%. However, these moves were well within the range of probabilities. By our estimation, these reflect a cross-asset shock of 1.2 standard deviations, i.e., these moves aren’t out of the ordinary, but rather the combination of these moves the impacted performance. We show the impact of these moves on cumulative returns below:

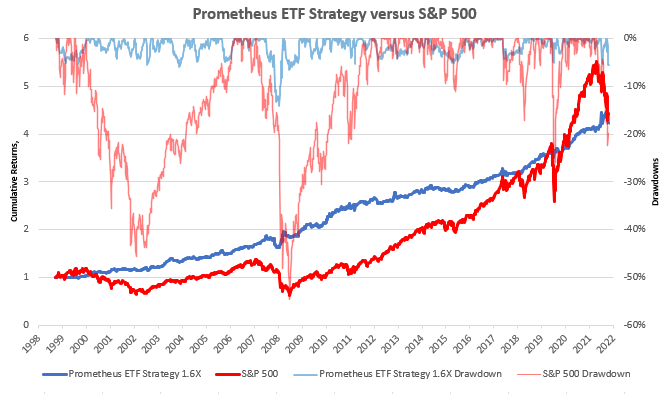

Nonetheless, we remain confident our ETF Strategy can continue to generate strong risk-adjusted performance over the market cycle. Below, we show how historically, this approach has resulted in lower drawdowns, increasing the opportunity to compound at higher capital levels. We offer the full-sample performance of the ETF Strategy below (matched to S&P 500 returns):

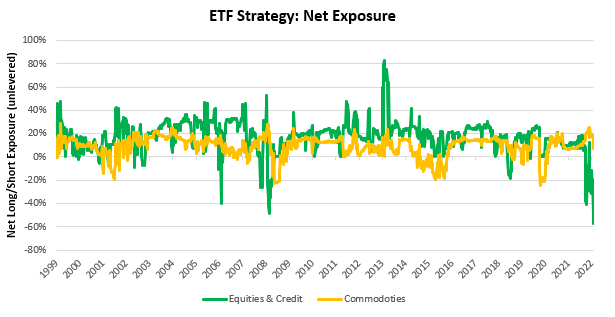

Turning to how our systems are positioning the ETF Strategy, we think it is imperative to note that the most recent commodity moves have resulted in significantly lower commodity exposures. Furthermore, despite this weeks price action, the conviction remains strong on equity and credit shorts. We show the net positioning in equities & credit versus commodities below:

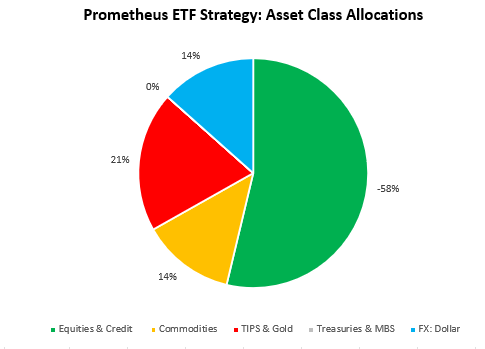

Given the economic and market environment, the strategy remains tilted towards the dollar as the number one long exposure. We show the ETF Strategy exposure at the asset class level below:

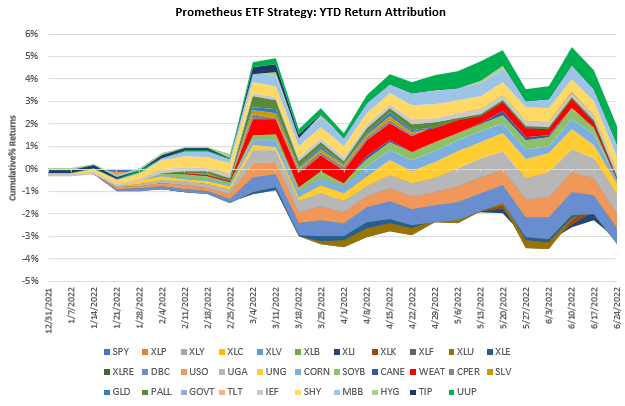

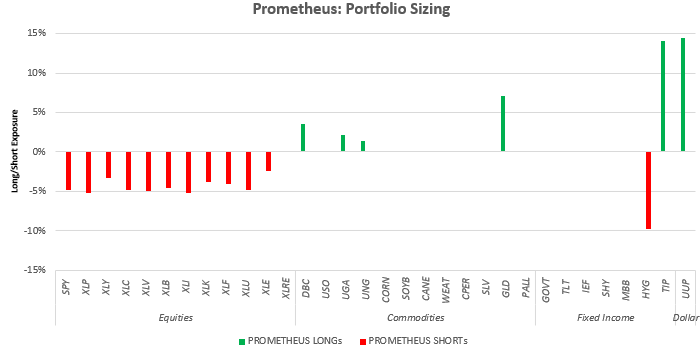

Finally, we offer how these allocations are at the security level for next week. We think it is important to note that commodity exposure has been significantly whittled down in terms of breadth of exposure:

-

Stocks: SPY (-5%), XLP (-6%), XLY (-4%), XLC (-5%), XLV (-5%), XLB (-5%), XLI (-6%), XLK (-4%), XLF (-5%), XLU (-5%), XLE (-3%)

-

Commodities: DBC (4%), UGA (3%), UNG (2%), GLD (8%)

-

Fixed Income: HYG (-10%), TIP (15%)

-

Dollar: UUP (15%)

We show this visually below:

Markets have been discounting waning inflation momentum; however, this doesn’t mean inflation is no longer a concern for both the real economy and financial markets. This change is an incremental signal, and we continue to adjust accordingly. We continue to be in a period of stagflationary nominal growth, with tightening liquidity driving markets lower. Stay nimble.