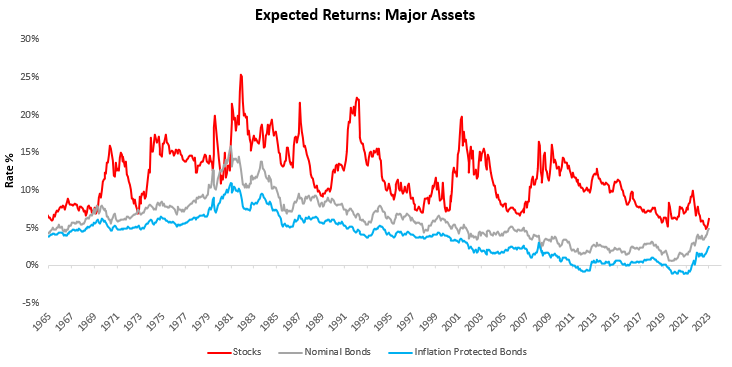

Equity markets have posted some of the strongest relative price performance gains this year, as fixed-income assets have suffered the impacts of the Fed’s tightening cycle. As we approach what looks like an interim top in the hiking cycle, we think it is important to take stock of the drivers of equity market return to inform our outlook.

Before diving into our outlook, we think it is important to frame how we think through the drivers. Equities are an asset that represents the present value of a discounted flow of cash flows generated by corporations. The value of these assets is driven by a combination of policy rates, nominal GDP, profitability, and liquidity conditions. Maintaining a durable edge in equities requires a view of all of the above.

We begin with the policy rate, which has two components: the realized policy rate and the expected path for the policy rate. The realized policy rate has little immediate effect on equity prices, as what is priced into asset markets are changes in expectations. However, where the realized policy rate is important is in its impact on debt service costs, which rise in response to policy rates, compressing profitability. This dynamic has more to do with the economic cycle than the immediate pricing of market conditions, which is an important distinction. The expected path of the policy rate, on the other hand, has significant impacts on the price of equities, as changes in the implied discount rate on cash flows over the discount period. As such, the expected path of the short rate can have significant, meaningful effects on the repricing of securities nearly immediately, while the level of the policy rate works through the economy over time.

Both the realized policy rate and expected policy rate path are typically responsive to nominal GDP conditions. The faster the clip of nominal GDP, the higher the policy rate typically rises to keep inflationary conditions under control. Nominal GDP flows directly to company toplines, and to the extent that they are not already expected, accelerations in nominal GDP benefit equities and vice versa. An important nuance of how this nominal GDP flows into equities is the ability of corporations to take an existing pie of nominal GDP and carve out a section of it into profits. Before they can carve out this profitability, they must give away shares of nominal GDP to capital and labor costs. The greater the ability of the corporation to extract profits from a pool of nominal GDP relative to what is expected, the greater the beneficial impact on equity prices. In large part, expectations for business costs scale in line with inflation. This mechanism creates a duality in terms of equity market pricing with regard to inflation. On the one hand, equity markets benefit from higher-than-expected inflation via nominal GDP, but on the other, they also suffer from higher-than-expected costs. This combination of features is often what leads equities to look like a real growth asset, i.e., one that benefits from real growth conditions rather than nominal ones. While this serves as a good approximation, it is important to recognize it is not a precise one. Precision requires an understanding of how nominal GDP flows to profitability, which is largely a function of the composition of spending in the economy, with more spending and investment relative to incomes stimulative of profits and vice versa. In addition to these immediate-term drivers, equities also receive a premium for the optionality of management decisions to return capital to shareholders, either directly through dividends and buybacks or indirectly through the reinvestment of the business. None of these avenues are guaranteed and hence require additional compensation relative to a fixed-income credit instrument.

Finally, while the economic drivers of police rates, nominal growth, and profitability determine the direction of the moves relative to other asset classes, the total size of the move in prices is driven by liquidity conditions, i.e., how much cash or cash-like assets are available to purchases equities at a given time. Part of this flow is mechanical in that savings from nominal GDP enter into market prices, and part of this is contingent upon the relative attractiveness of equities versus other assets. Said differently, there can be more cash chasing all assets, or there can be more cash chasing one asset in favorable environments. Reality is always a combination of these factors. To summarize, market pricing of equities is driven by a combination of the policy rate, nominal GDP, profitability, and how much liquidity is able to underwrite this combination of fundamental dynamics.

Now that we’ve outlined the drivers, we dive into our big-picture views. This year, equities have benefitted from inflationary pricing in markets remaining subdued, nominal growth remaining resilient, and profitability outperforming relative to what was expected. At the same time, equities have been hurt by the repricing of the expected rate path, as markets have repeatedly moved to price out the likelihood of interest rate cuts. These fundamental dynamics net out to positive economic conditions for equities. These positive conditions were underwritten by a significant amount of liquidity present in financial markets, driven by the net impact of the Fed and Treasury, along with a positive private sector. This liquidity impulse during an inflationary period created a rise in equity prices, consistent with investors’ needs to maintain a higher equity exposure as nominal bonds underperformed. These conditions have created a strong backdrop for equity markets, which have risen significantly relative to other assets.

Looking ahead, we think the continuation of this equity outperformance looks unlikely. Policy rates look unlikely to begin easing, and with a more modest amount of interest rate cuts priced into short-term interest rate markets, an easy of policy conditions seems unlikely. Turning to nominal GDP, it is likely that nominal GDP will continue to deteriorate, which is likely to extend the ongoing pressures on business profitability. Furthermore, these pressures remain inconsistent with earnings expectations priced into equity markets, which show consensus expectations of expanding earnings. As such, we expect earnings expectations to decline from here alongside a deceleration in economic data momentum. Now, what remains significantly in favor of equity markets are liquidity conditions and the dynamics of liquidity conditions. In an environment of above-target inflation and persistent deficit spending, the aggregate investor allocation to equities is likely to remain well supported until activity turns. Putting these factors together, we think that the sustained outperformance of equities has likely reached its zenith, and a correction in these dynamics can come in one of two ways: equity markets can fall, or credit and bond markets can rise. Given the current state of liquidity dynamics, we have seen more of the latter over the last few weeks, with assets catching up to equities by our measures. For equities to turn lower from here, we require a re-evaluation of profit expectations alongside a pullback in policy liquidity conditions. We see the profit re-evaluation as more likely in the immediate term than the liquidity reversal. The combination of these drivers will likely initiate a bear market in equities, and we will continue to monitor them as they evolve.

While we may be wrong on any of the drivers at a given time, we think it is important to provide this framework to help create a roadmap for synthesizing views. We hope this helps offer clarity on the drivers of equity market returns and our outlook. Until next time.

Hi there! Do you know if they make any plugins to help with

Search Engine Optimization? I’m trying to get my website to rank for

some targeted keywords but I’m not seeing very good gains.

If you know of any please share. Cheers! You can read similar blog here:

Warm blankets

Hi! Do you know if they make any plugins to assist with Search Engine Optimization? I’m trying to get my blog to

rank for some targeted keywords but I’m not seeing very good

results. If you know of any please share. Appreciate it!

You can read similar art here: Change your life

I’m really impressed together with your writing abilities and also with

the format on your weblog. Is this a paid subject

or did you modify it your self? Either way keep up the

excellent quality writing, it is rare to peer a nice blog like this one nowadays.

Blaze AI!

I am extremely inspired together with your writing talents as neatly as with the layout for

your weblog. Is that this a paid subject matter or did you modify it your self?

Either way stay up the nice high quality writing,

it is rare to see a nice blog like this one today. Blaze AI!

I am extremely impressed together with your writing talents as neatly as with the format in your weblog. Is this a paid subject matter or did you customize it your self? Anyway stay up the excellent quality writing, it is uncommon to see a great weblog like this one today. I like prometheus-research.com ! It’s my: Snipfeed

buying clomid without prescription where to get clomiphene without prescription where to buy cheap clomid no prescription says: order clomid without insurance can i get cheap clomid tablets can you get cheap clomid without insurance cost generic clomid pills

I’ll certainly return to skim more.

This website absolutely has all of the tidings and facts I needed there this thesis and didn’t positive who to ask.

oral azithromycin 250mg – purchase tetracycline pills flagyl 400mg ca

order semaglutide pill – periactin 4 mg generic buy periactin 4mg generic

motilium brand – order tetracycline 500mg for sale order cyclobenzaprine

oral propranolol – clopidogrel 75mg brand buy methotrexate 5mg without prescription

amoxil for sale – buy valsartan 80mg pills order ipratropium 100mcg

buy zithromax 250mg generic – buy tinidazole paypal cost nebivolol 20mg