In this note we share our thoughts on the macro mechanics at play in the context of the current economic cycle. If well received, we will continue to share these Macro Mechanics. Lets us know in the comments below.

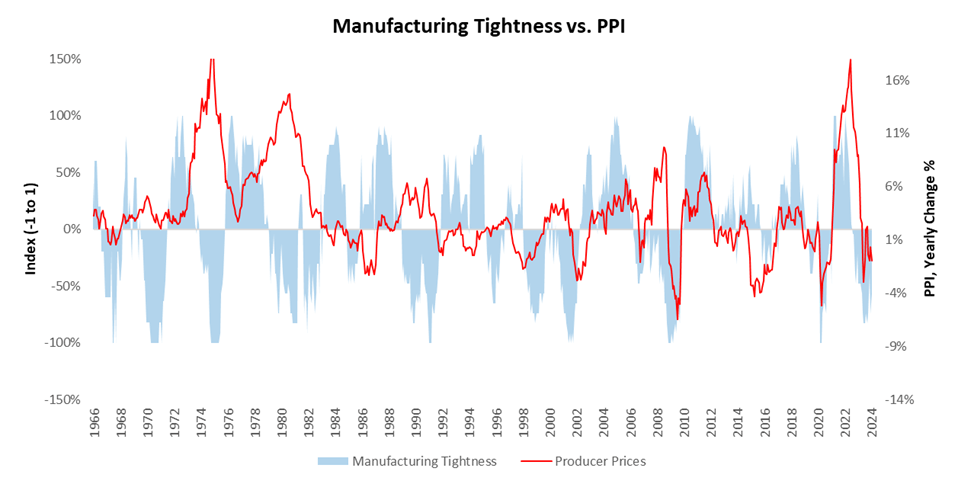

At the macro level, commodity prices are a function of production relative to nominal spending. Existing production capacity limits commodity production, while income and debt services burdens limit nominal spending. The combination of these dynamics determines how tight manufacturing conditions are. Commodity prices serve as a release valve for this tightness, i.e., the tighter conditions are, the more pressure there is on commodity prices to rise. Conversely, the looser conditions are, the weaker the pressure on commodity prices. We visualize this dynamic below:

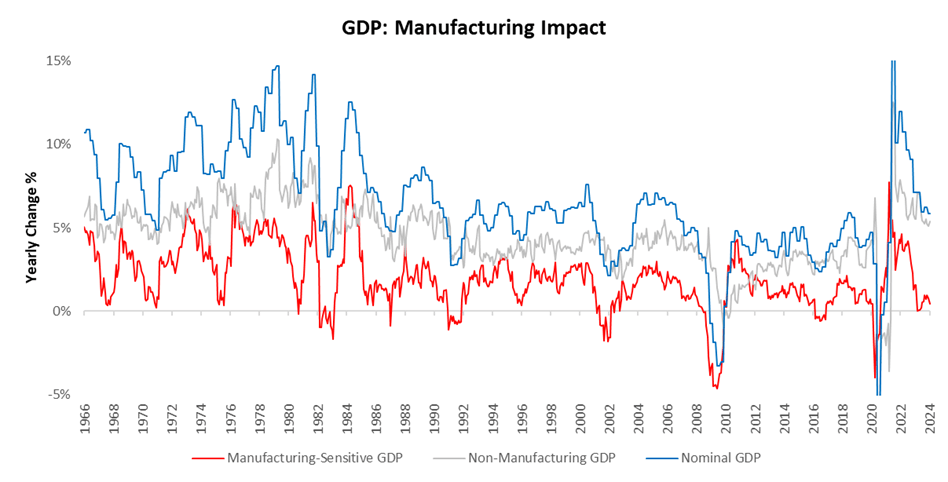

As shown above, manufacturing tightness has served as a strong barometer of future commodity price regimes. To understand these dynamics, need to examine manufacturing conditions across the economy. Below, we visualize how manufacturing activity flows through to GDP growth:

We think there are two crucial takeaways from the above visualization. First, manufacturing is highly cyclical and a key determinant of business cycle conditions in the economy. Second, the current impact of manufacturing on the overall economy remains limited by the strength of non-manufacturing components. Combining these dynamics creates a unique opportunity for active investors seeking diversified bets. Namely, today’s environment allows us to bet on manufacturing outcomes in commodity markets without being exposed to broader macro risks that drive equities and bonds. Said differently, commodity markets may fall under weak manufacturing conditions, but equities may remain strong as the rest of the economy remains resilient. In macro, we are always looking for a diversified set of bets to reduce portfolio concentration, and the current dynamic offers a relatively unique opportunity to that end.

To develop an understanding of the factors driving commodity prices, we turn to the goods economy, which is driven by manufacturers, wholesalers, and retailers. The aggregate conditions in these sectors determine the nominal activity that forms the commodity demand. However, not all these sectors are equal in their impact on commodity prices. As we move up the supply chain, we start to see a larger role of services in determining activity, i.e., retailers facing consumers are a blend of goods and services demand. As such, while we think a broad-based understanding of goods demand is essential for a holistic understanding, we place significant weight on conditions at the origin of the supply chain, i.e., with manufacturers.

Today, this comprehensive but nuanced understanding of conditions makes us think the goods economy faces significant pressures. This pressure emanates from somewhat muted consumer demand for goods but primarily from increased profit pressures on manufacturing firms. This understanding deviates from recent sequential data coming from the manufacturing sector and commodity price trends. As systematic investors, we think it is important to balance these competing perspectives when generating portfolio views. Therefore, while we see sustained pressures likely ahead for the commodity complex, we also recognize that this is not what near-term conditions confirm. As such, we see significant future opportunities to be short commodities, but the current weight of evidence suggests modest long positions. Our signalling process considers hundreds of variables to come to these views, and the turns can be relatively quick. This long exposure is unlikely to be suitable for slower-moving players, but it is likely to provide a modest signal for faster-moving players. For asset allocators, we continue to see this environment as non-conducive to commodity exposure. Our latest Month in Macro report provides the data and analysis driving these views. Email us at info@prometheus-research.com to learn more about our Bespoke services.

5 thoughts on “Commodities: A Function Of Manufacturing Tightness”

Their global perspective enriches local patient care.

lisinopril generic 10 mg

I always find great deals in their monthly promotions.

Always attuned to global health needs.

can you buy cytotec

A pharmacy I wholeheartedly recommend to others.

A trusted voice in global health matters.

how to get cheap cipro without rx

Their health awareness campaigns are so informative.

Top 100 Searched Drugs.

can i buy generic clomid online

п»їExceptional service every time!

Their commitment to international standards is evident.

cost of cheap cipro prices

Their worldwide delivery system is impeccable.