Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real-time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

Our primary takeaways are as follows:

● The latest industrial production data softened on a sequential basis, disappointing consensus expectations.

● Of the 28 subsectors that we track, 61% remain in contraction. This softening of industrial production remains indicative of the slowdown of the good economy.

● However, its impact on the top-line nominal growth conditions remains negligible. In the context of markets, our Commodities Alpha Strategy remains modestly exposed to long-commodities.

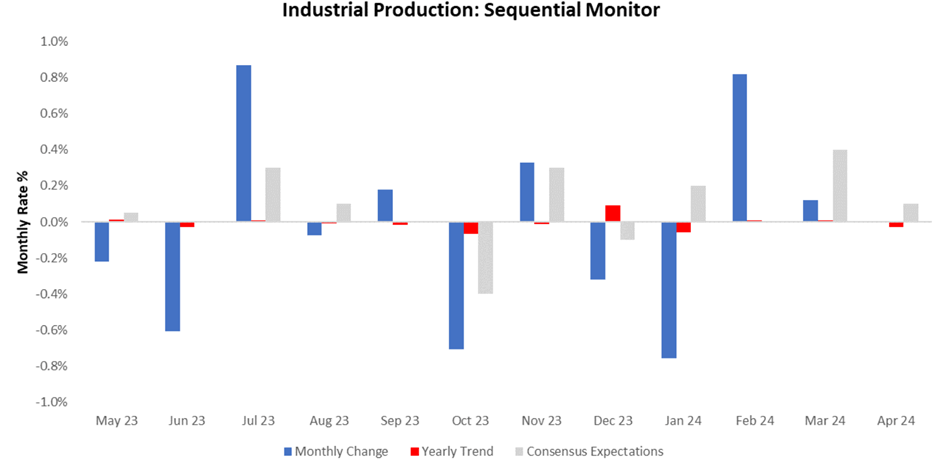

The latest data for April shows Industrial Production increased, coming in at 0.01%. This print disappointed consensus expectations of 0.1% and contributed to an acceleration in the three-month trend relative to the twelve-month trend. We show the sequential evolution of the data below:

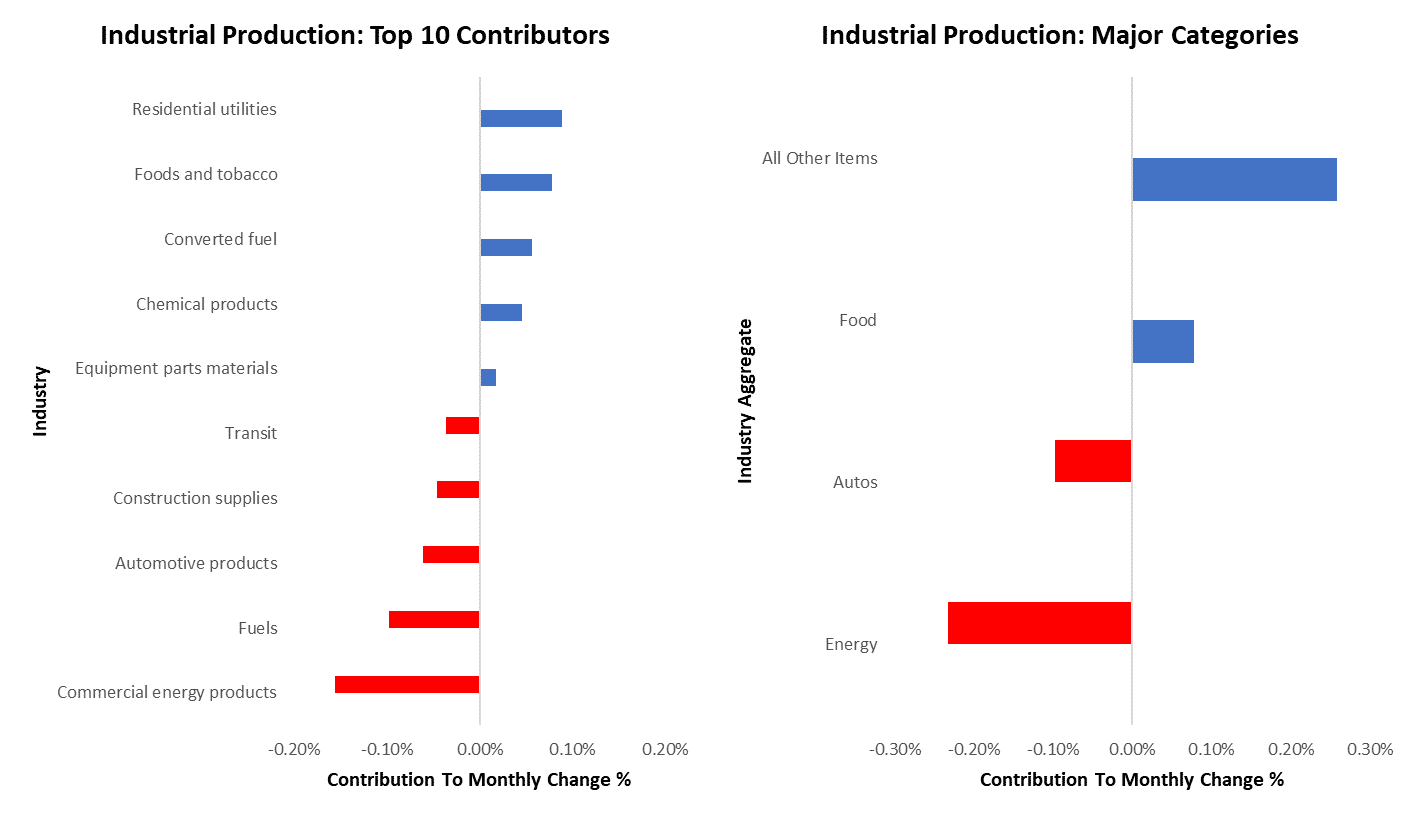

We break this print into its contributions from production coming from Food (0.08%), Energy (-0.23%), Autos (-0.1%), and All Other Items (0.26%). Additionally, we also showcase the top 10 contributions by industry. The largest contributor this month was Residential utilities, and the largest detractor was Commercial energy products:

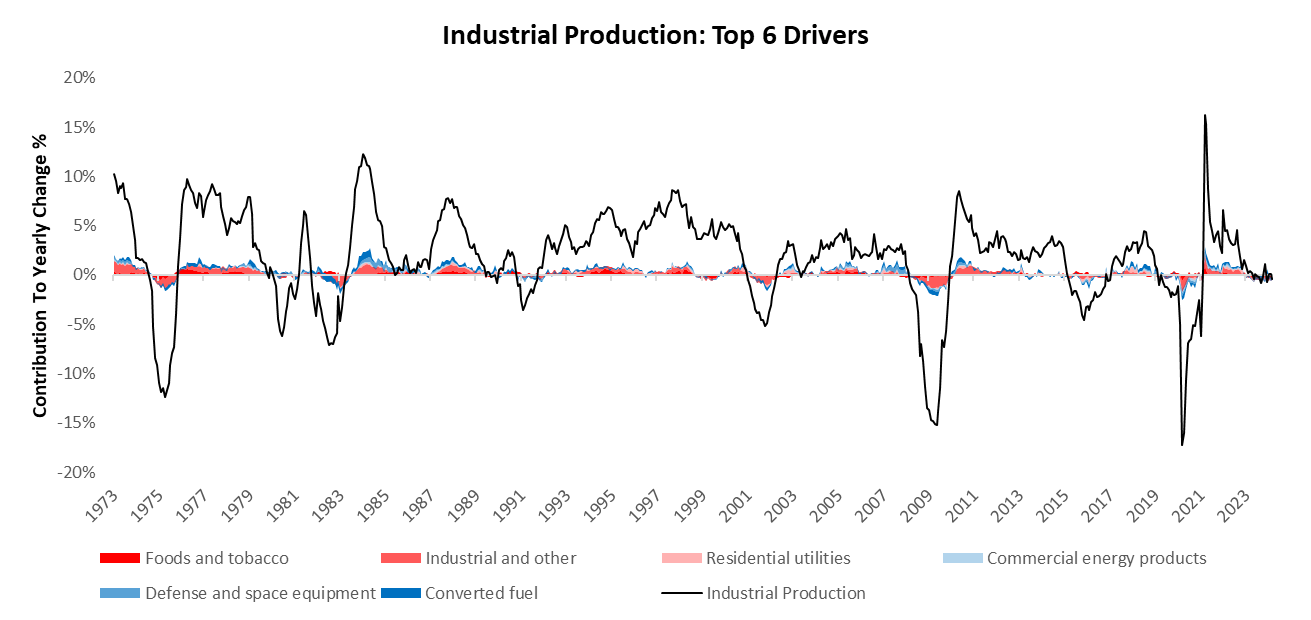

We zoom out to offer further context on the dynamics of industrial production. Over the last year, industrial production has contracted by -0.38%. Below, we present the top six drivers of industrial production, with the three strongest industries highlighted in blue (Converted fuel, Défense and space equipment, and Commercial energy products) and the three weakest industries highlighted in red (Foods and tobacco, Industrial and other, and Residential utilities):

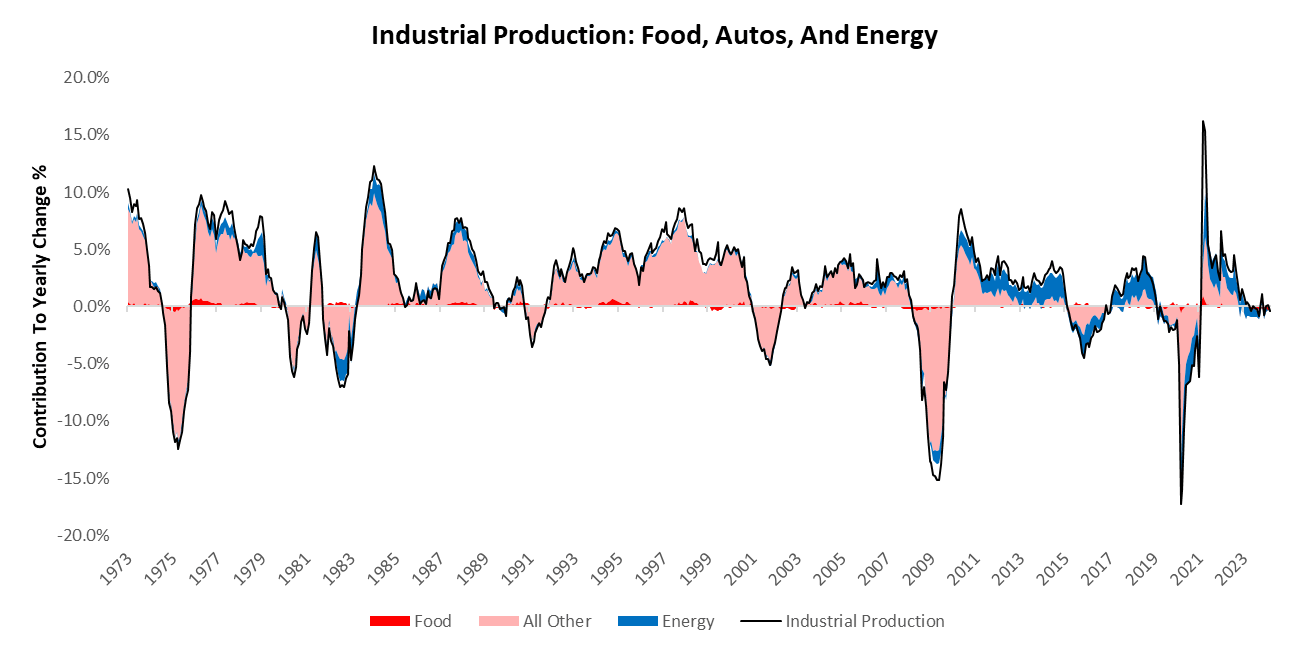

Over the last few decades, the importance of food, energy, and automobiles has risen, accounting for a significant amount of the variation in industrial production. Over the last year, food, energy, and automobiles have contributed -0.15% to the -0.38% change in industrial production. We show this impact below:

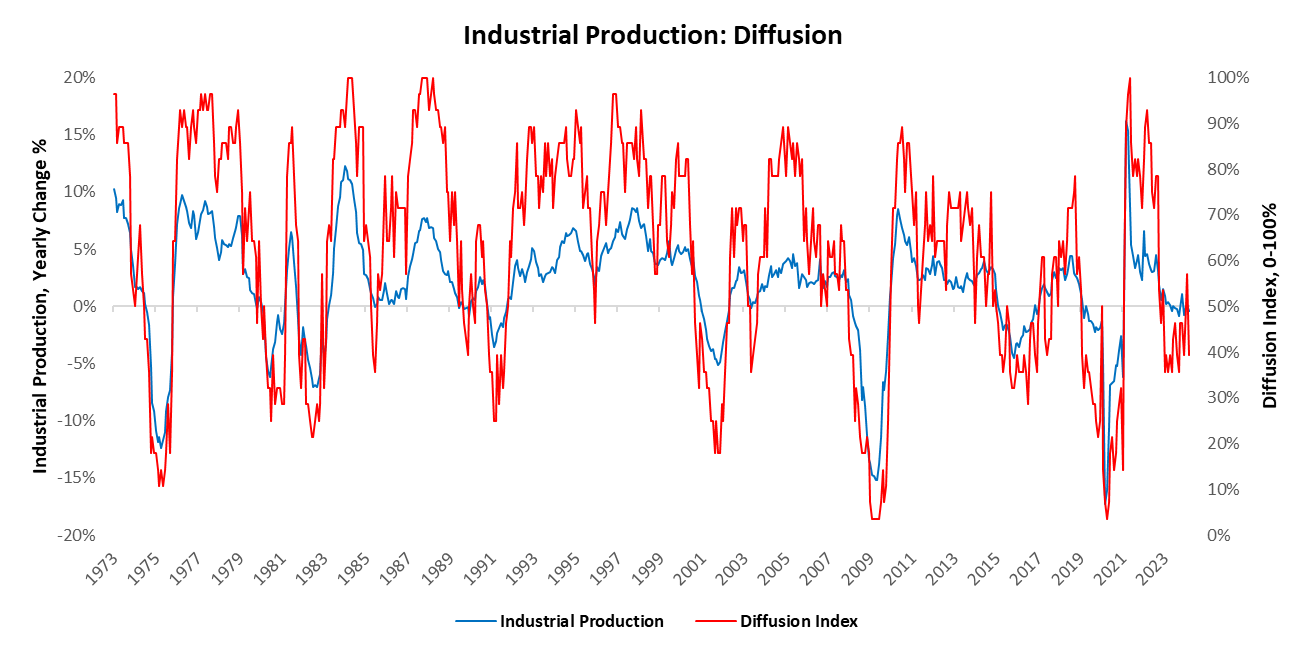

To further assess the health of the current contraction of industrial production, we examine the diffusion of the 28 subsectors we track. This involves examining the number of industries that are expanding versus the number of industries that are contracting. We find that 61% of industries are contracting. Below, we visualize how a diffusion index has generally been a good barometer of the durability of upturns and downturns in industrial production:

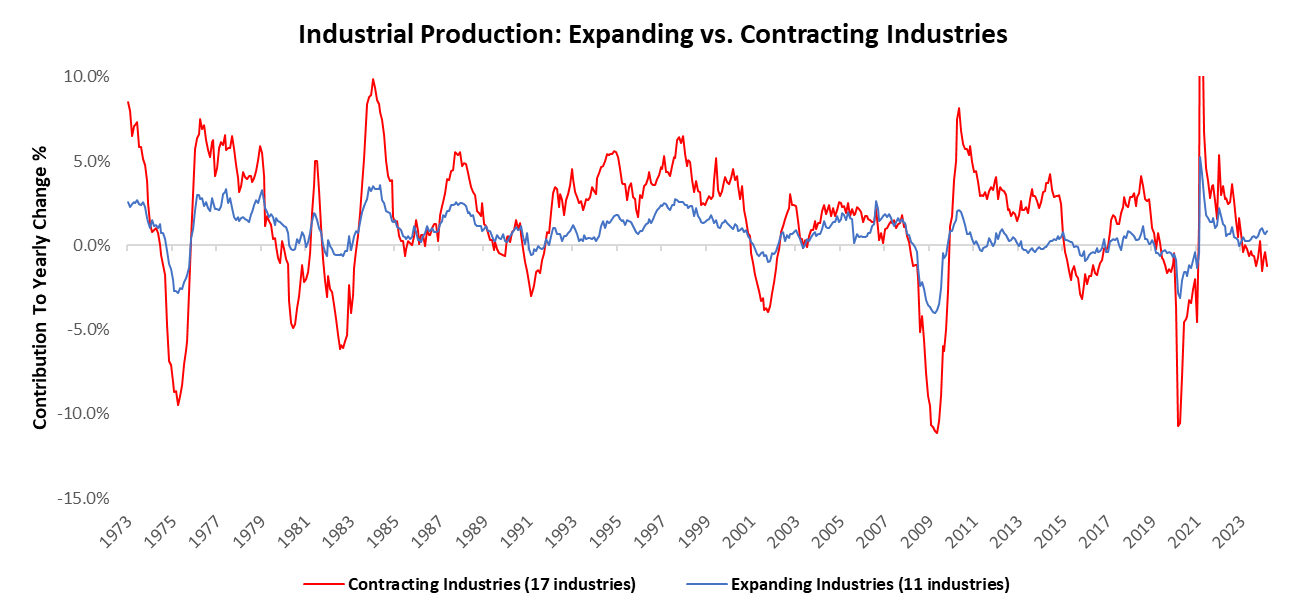

To elaborate further, currently 11 industries are expanding and contributing 0.86% to industrial production, compared to 17 industries showing contraction and detracting -1.2% from industrial production growth compared to one year prior. We visualize their respective weighted contributions below:

Overall, a softening of industrial production remains indicative of the deacceleration of the good economy. Nonetheless, our process accounts for the fact that while business conditions may eventually lead to a self-reinforcing downturn for manufacturing, it currently isn’t in that state. Consequently, our Commodities Alpha Strategy remains modestly exposed to long commodities. Until next time.

8 thoughts on “Assessing Industrial Production”

clomiphene one fallopian tube where buy clomid tablets can i purchase cheap clomid without a prescription how to buy cheap clomid withou can i buy generic clomiphene price can i order cheap clomiphene without insurance can i get clomid without rx

Greetings! Jolly useful advice within this article! It’s the crumb changes which choice make the largest changes. Thanks a portion towards sharing!

The reconditeness in this tune is exceptional.

zithromax 500mg uk – tinidazole 500mg for sale buy flagyl 400mg pill

brand domperidone 10mg – buy sumycin online cheap flexeril sale

inderal usa – purchase plavix generic buy methotrexate generic

amoxil uk – buy combivent 100mcg pill combivent 100 mcg pill

azithromycin ca – tinidazole 500mg generic nebivolol uk