At Prometheus, we are committed to equipping our clients with the most granular, high-frequency, and actionable understanding of macro conditions in the industry. We offer our clients a range of research solutions, from big-picture macro themes to actionable trading signals. In the spirit of giving back to the community, we are excited to offer an All-Access week in our Institutional Services. Each day this week, we will unveil one product offering from our extensive Institutional Offering. If you’re interested in institutional access, please contact us at info@prometheus-research.com.

Today, we share a note from The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real-time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

The Observatory – Commodities & Industrial Production

Our primary takeaways are as follows:

• The latest industrial production data confirms the sequential improvement in manufacturing revenue conditions.

• These improvements have been broad-based; however, profit pressures persist for manufacturers. The combination of these dynamics creates a near-term positive backdrop for commodities.

• Relative to these expectations, commodity markets are pricing in expectations of modestly lower prices over the next few months but higher prices over time.

• Our Alpha Strategies for commodities see this as an opportunity to be long commodities; however, signal strength is modest given fundamental pressures. Given these fundamental pressures, we don’t see commodities as value additive to long-only asset allocation but as suitable for faster-moving alpha strategies.

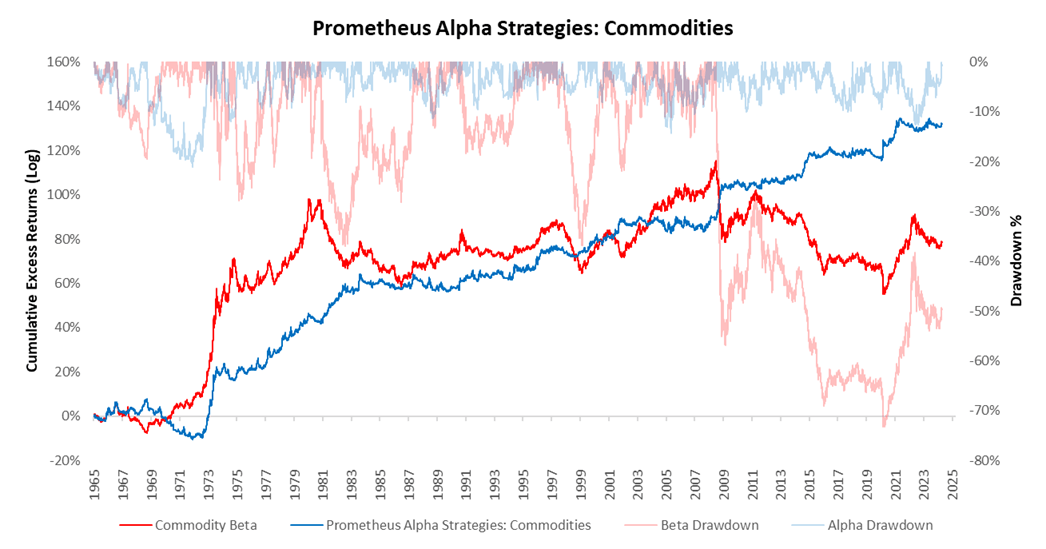

We begin by showing the recent context for our Alpha Strategies for Commodities:

While our systems estimate that fundamental pressures persist in the manufacturing economy, our broad-based tracking of the ongoing macro impulse continues to show the improvement of top line conditions. The net effect of these conditions drives our modest long positions. We discuss the data driving this assessment on the pages that follow.

While our systems estimate that fundamental pressures persist in the manufacturing economy, our broad-based tracking of the ongoing macro impulse continues to show the improvement of top line conditions. The net effect of these conditions drives our modest long positions. We discuss the data driving this assessment on the pages that follow.

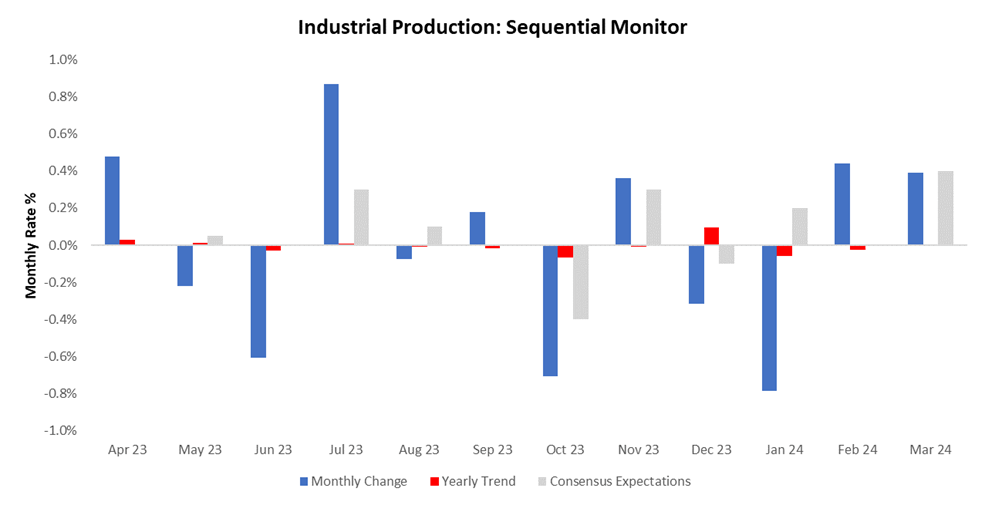

We begin with the latest industrial production data. The latest data for March shows Industrial Production increased, coming in at 0.39%. This print disappointed consensus expectations of 0.4% and contributed to an acceleration in the three-month trend relative to the twelve-month trend. We show the sequential evolution of the data below:

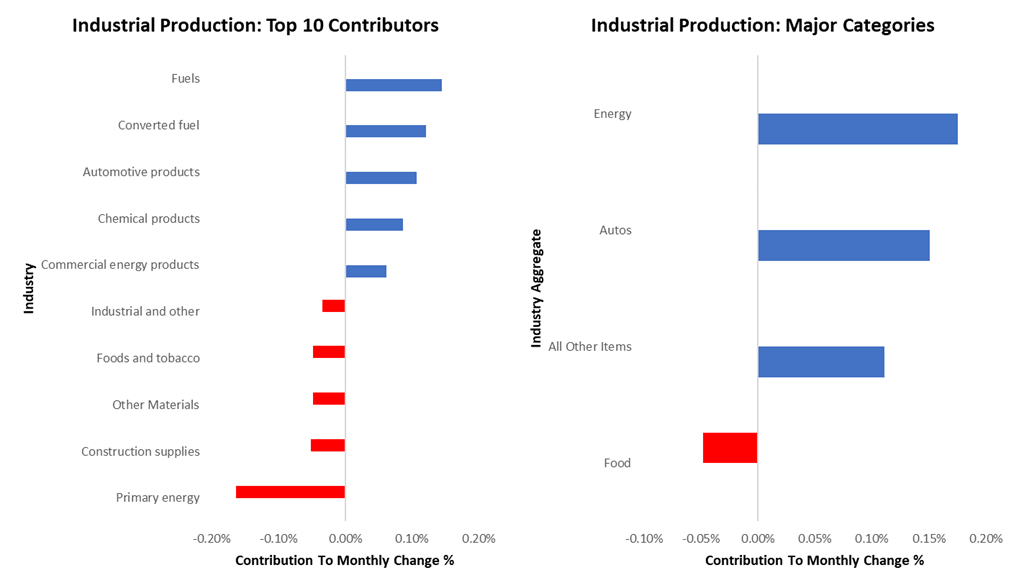

We break this print into its contributions from production coming from Food (-0.05%), Energy (0.18%), Autos (0.15%), and All Other Items (0.11%). Additionally, we also showcase the top 10 contributions by industry. The largest contributor this month was Fuels, and the largest detractor was Primary energy:

We break this print into its contributions from production coming from Food (-0.05%), Energy (0.18%), Autos (0.15%), and All Other Items (0.11%). Additionally, we also showcase the top 10 contributions by industry. The largest contributor this month was Fuels, and the largest detractor was Primary energy:

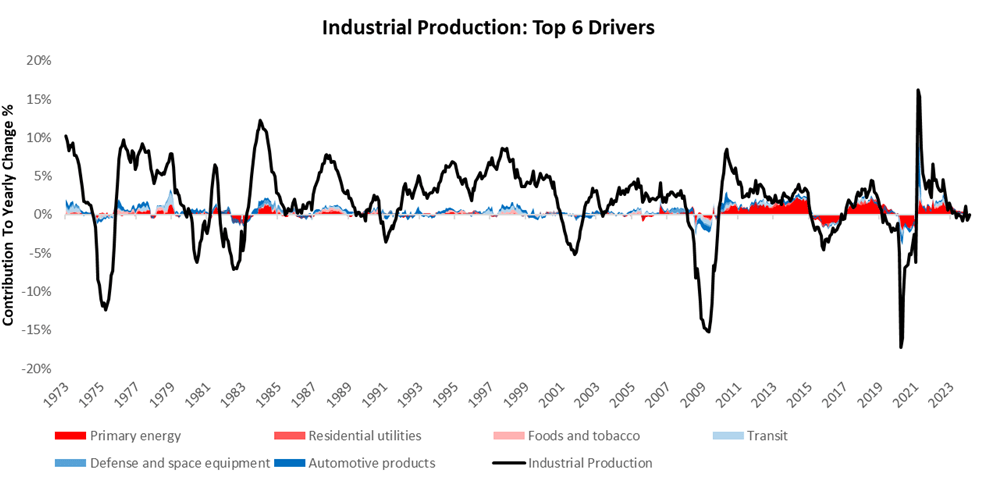

We zoom out to offer further context on the dynamics of industrial production. Over the last year, industrial production has contracted by 0%. Below, we present the top six drivers of industrial production, with the three strongest industries highlighted in blue (Automotive products, Défense and space equipment, and Transit) and the three weakest industries highlighted in red (Primary energy, Residential utilities, and Foods and tobacco):

We zoom out to offer further context on the dynamics of industrial production. Over the last year, industrial production has contracted by 0%. Below, we present the top six drivers of industrial production, with the three strongest industries highlighted in blue (Automotive products, Défense and space equipment, and Transit) and the three weakest industries highlighted in red (Primary energy, Residential utilities, and Foods and tobacco):

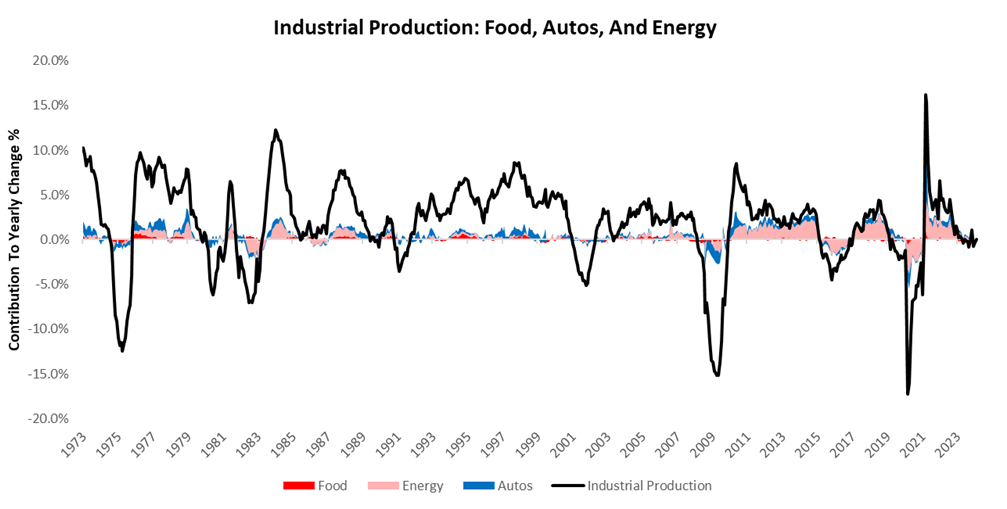

Over the last few decades, the importance of food, energy, and automobiles has risen, accounting for a significant amount of the variation in industrial production.

Over the last few decades, the importance of food, energy, and automobiles has risen, accounting for a significant amount of the variation in industrial production.

Over the last year, food, energy, and automobiles have contributed 0.04% to the 0% change in industrial production.

Over the last year, food, energy, and automobiles have contributed 0.04% to the 0% change in industrial production.

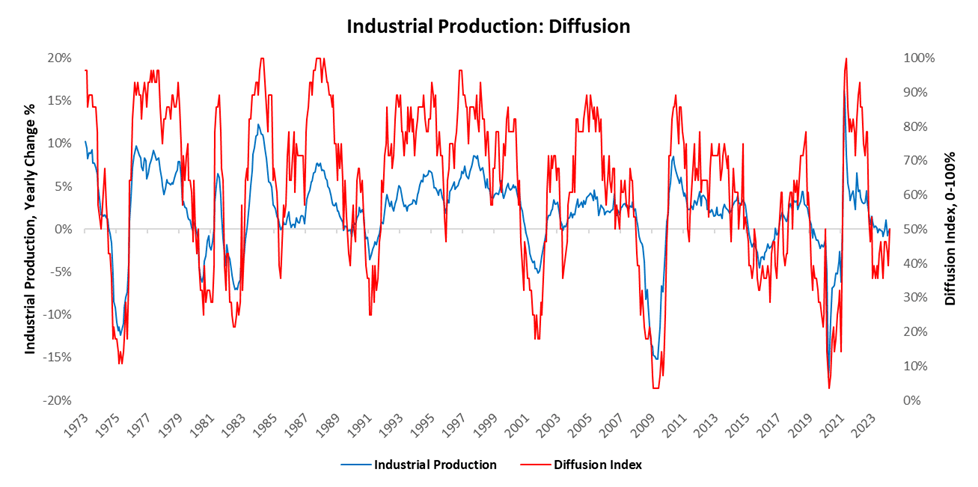

To further assess the health of the current contraction of industrial production, we examine the diffusion of the 28 subsectors we track. This perspective involves examining the number of industries that are expanding versus the number of industries that are contracting. We find that 50% of industries are contracting. Below, we visualize how a diffusion index has generally been a good barometer of the durability of upturns and downturns in industrial production:

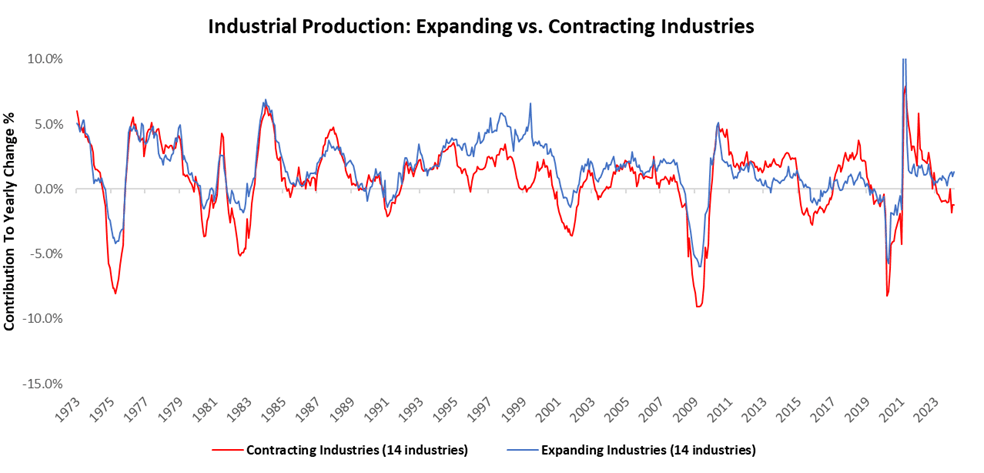

To elaborate further, currently, 14 industries are expanding and contributing 1.35% to industrial production, compared to 14 industries showing contraction and detracting -1.2% from industrial production growth compared to one year prior. We visualize their respective weighted contributions below:

To elaborate further, currently, 14 industries are expanding and contributing 1.35% to industrial production, compared to 14 industries showing contraction and detracting -1.2% from industrial production growth compared to one year prior. We visualize their respective weighted contributions below:

As we can see above, the pervasiveness of pressure on industrial production has eased recently.

As we can see above, the pervasiveness of pressure on industrial production has eased recently.

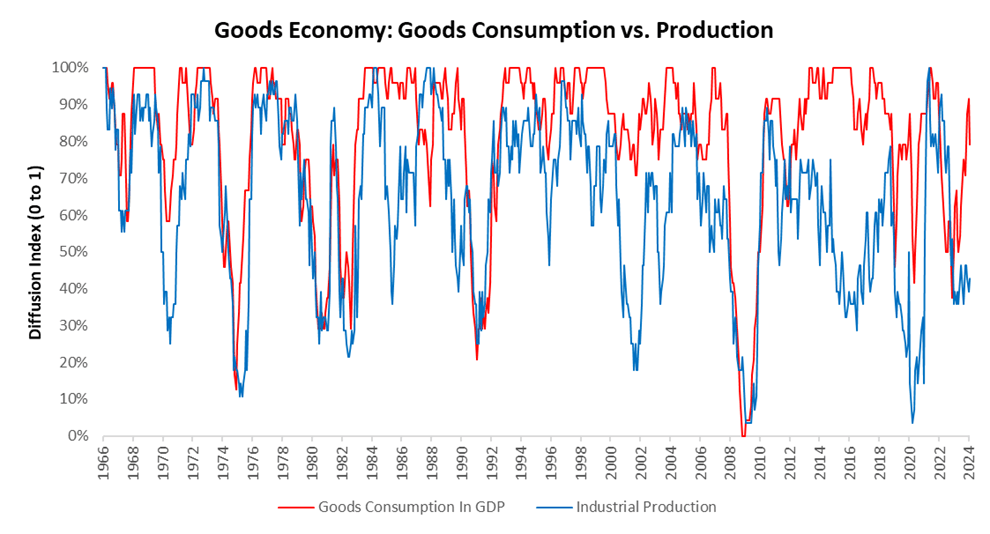

We see the easing of pressures on industrial output as largely a function of elevated goods demand from the consumer. Below, we show how goods demand in GDP has broadly improved in recent months, using diffusion measures:

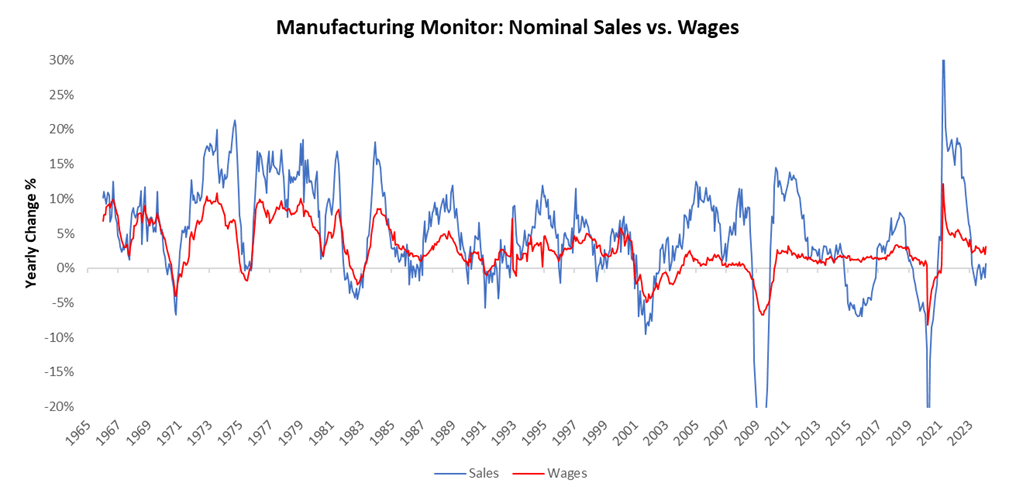

As we can see above, demand for goods has increased significantly. However, we continue to see significant pressure on manufacturers’ profit margins. Below, we show how nominal wages paid to manufacturing employees is current outstripping sales growth:

As we can see above, demand for goods has increased significantly. However, we continue to see significant pressure on manufacturers’ profit margins. Below, we show how nominal wages paid to manufacturing employees is current outstripping sales growth:

Thus, while consumer conditions remain strong, we don’t see business conditions as comparably robust.

Thus, while consumer conditions remain strong, we don’t see business conditions as comparably robust.

Thus, while nominal spending in the broader economy supports production and business toplines, we continue to see pressures on business bottom lines that will likely result in decreased employment. However, a well-balanced systematic process does not over-anchor any one view and uses incoming data’s breath and ongoing impulse to understand the probable path. In line with the principle, our process accounts for the fact that while business conditions may eventually lead to a self-reinforcing downturn for manufacturing, it currently isn’t in that state. Our investment approach is to wait for the early inklings of macro moves to begin playing out to ride the wave rather than swim against the macro tides.

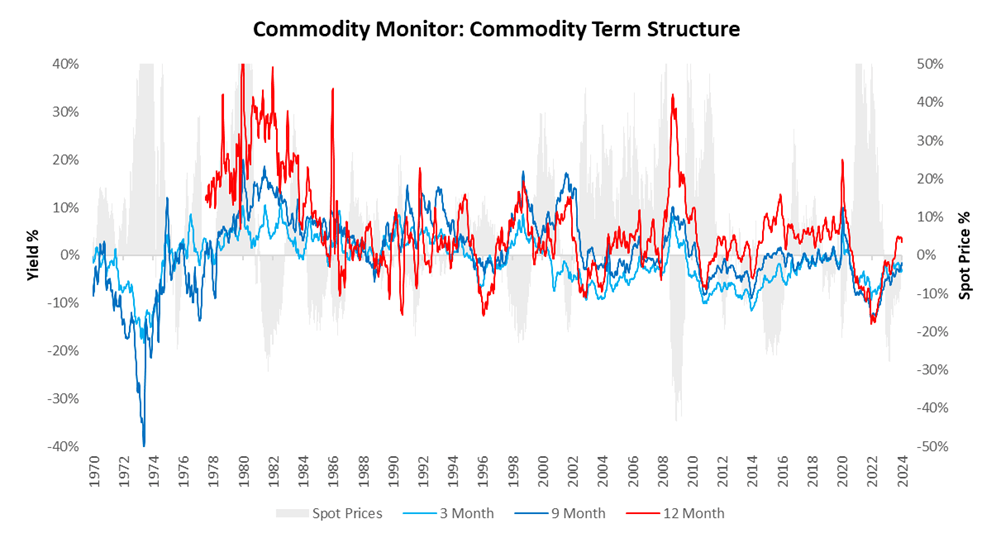

Relative to this nuanced outlook, commodity markets also have priced in a somewhat mixed outlook. Below, we visualize our aggregated commodity futures term structure across 26 commodity markets:

As we can see above, commodity markets continue to price in conditions over the near term that are consistent with lower commodity prices. This dynamic creates a modestly attractive opportunity for long positions if top line manufacturing business conditions continue to support commodity price action.

As we can see above, commodity markets continue to price in conditions over the near term that are consistent with lower commodity prices. This dynamic creates a modestly attractive opportunity for long positions if top line manufacturing business conditions continue to support commodity price action.

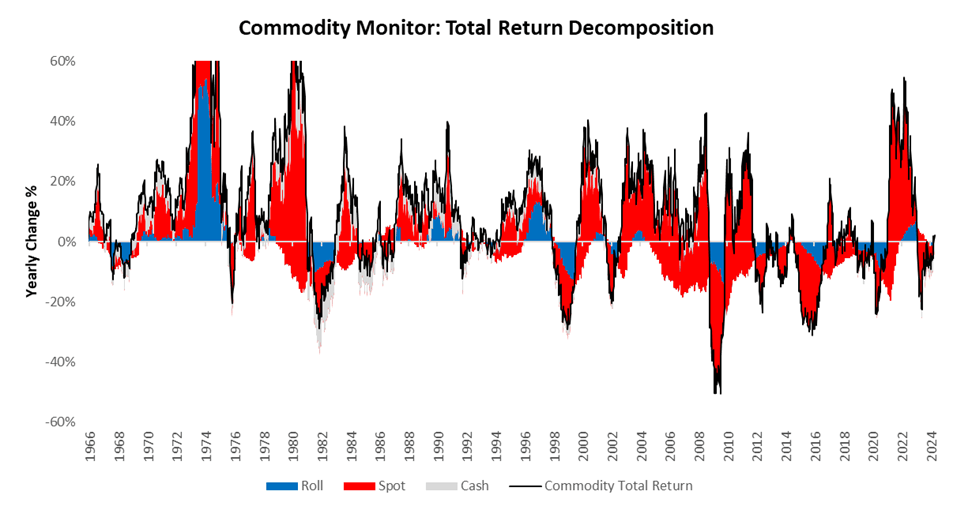

This expectation of commodities also creates an environment where commodity carry is positive. This will allow roll yield to be a stronger contributor to total returns:

Nonetheless, it is crucial to recognize that commodity returns are almost always dominated by spot conditions, which are driven by fundamental macro conditions. We visualize this relationship below:

Nonetheless, it is crucial to recognize that commodity returns are almost always dominated by spot conditions, which are driven by fundamental macro conditions. We visualize this relationship below:

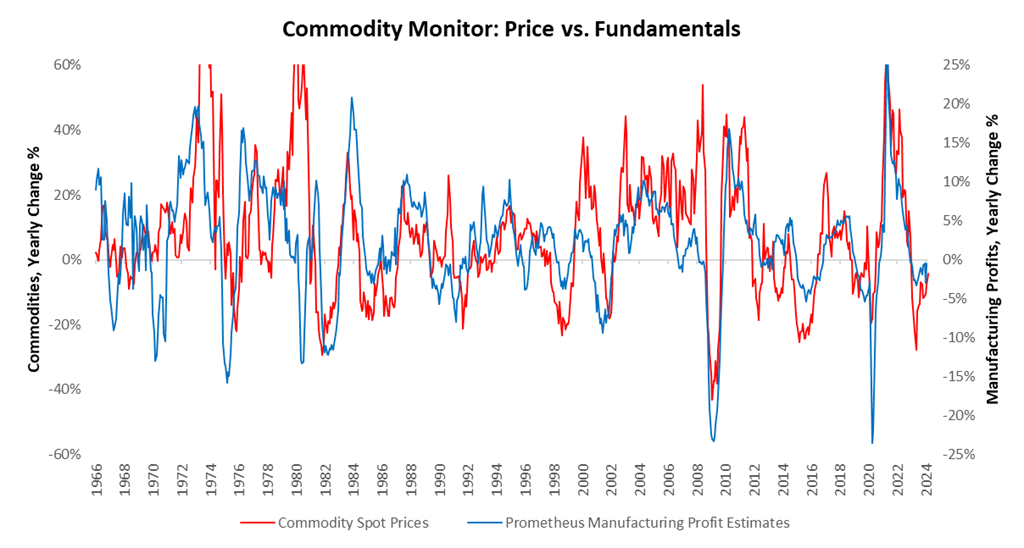

Fundamental conditions have improved during a downturn, supporting commodity price action. Recognizing this dynamic, our strategies maintain tactical long exposure, though we continue to view commodity beta as unsuitable for long-only asset allocators. Until tomorrow.

Fundamental conditions have improved during a downturn, supporting commodity price action. Recognizing this dynamic, our strategies maintain tactical long exposure, though we continue to view commodity beta as unsuitable for long-only asset allocators. Until tomorrow.

7 thoughts on “All-Access Week”

where buy generic clomid how to get cheap clomiphene no prescription where can i get clomid price can you buy cheap clomiphene prices clomid costo clomiphene only cycle where can i buy cheap clomiphene price

This is the stripe of topic I have reading.

order azithromycin 250mg online – generic tinidazole buy metronidazole generic

rybelsus pills – buy semaglutide generic cyproheptadine 4 mg us

motilium over the counter – buy domperidone 10mg online buy cyclobenzaprine without a prescription

oral inderal 20mg – buy clopidogrel sale buy methotrexate 10mg

amoxil cost – generic diovan 160mg cost ipratropium 100mcg