At Prometheus, we are committed to equipping our clients with premier macro tools, enabling them to navigate the markets with unparalleled ease and precision. In line with our mission, we are excited to offer an All-Access week in our Institutional Services. Each day this week, we will unveil one product offering from our extensive Institutional Offering. To learn more, please contact us at info@prometheus-research.com.

Today, we provide access to Prometheus Asset Allocation. This is one of our three systematic strategies designed to offer a superior alternative to traditional passive stock and bond portfolios. You can access the slide deck or read the full note below:

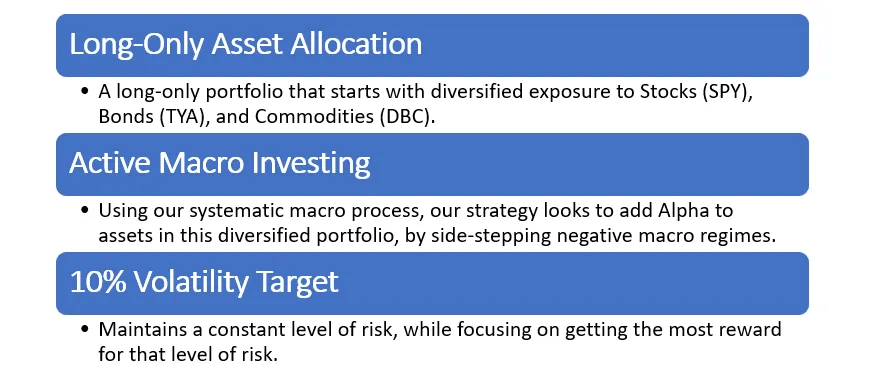

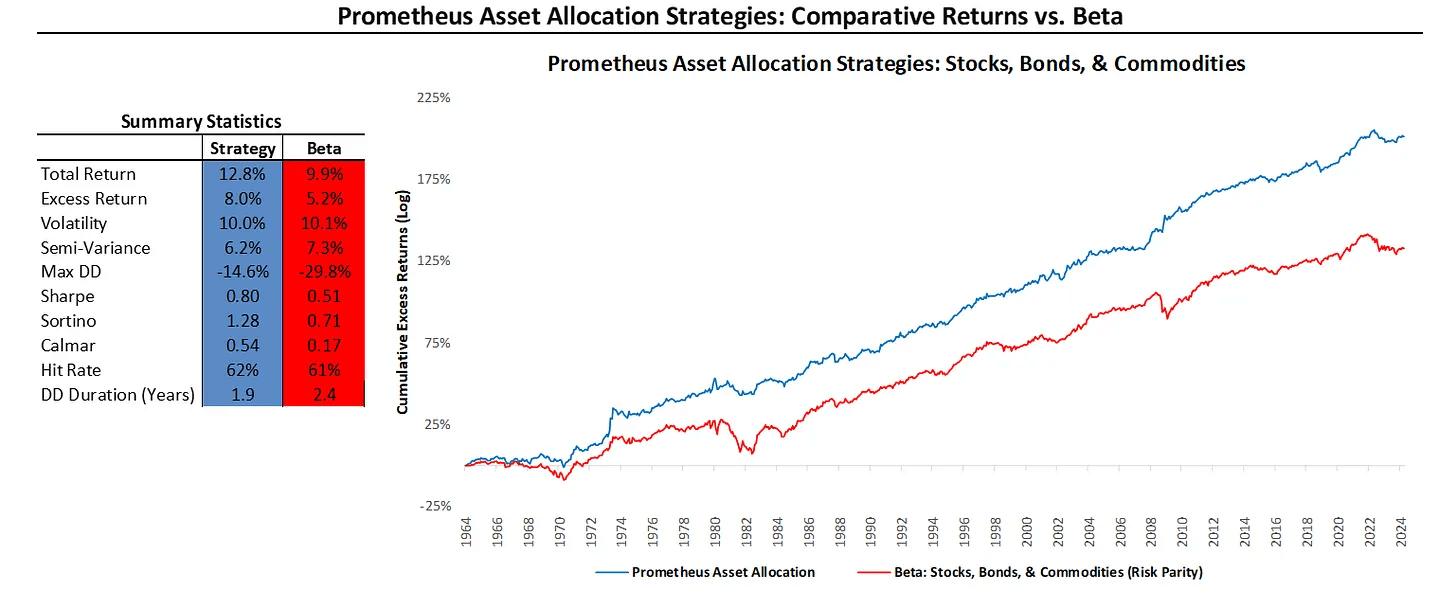

What Is Prometheus Asset Allocation?

This strategy starts by diversifying the asset base with commodities and TYA, a higher volatility version of 10-year treasuries, ensuring performance across various economic conditions including expansions, recessions, and inflationary periods.

Our systematic macro process then guides the timing of entry and exit for asset exposures, optimizing our holdings to capitalize on favorable economic times and avoid downturns. We strategically invest in equities during expansions, bonds during economic slowdowns, and commodities during stagflations, employing a proprietary approach to determine these regimes.

Additionally, we maintain a targeted 10% volatility, mirroring the risk level of a traditional 60/40 portfolio while protecting against significant losses. Further, 10% is a level of risk where any losses incurred are never so large that they run the risk of ruin. 10% is also largely consistent with the volatility of a 60/40 stock and bond portfolio.

Evaluation from Macro Monitors

Following are our main takeaways from the assessment of macroeconomic conditions:

- Markets continue to price regime probabilities consistent with rising growth and liquidity conditions. This pricing is consistent with the ongoing impulse from fundamental macro conditions.

- Currently, our systems see a limited risk of nominal or real growth slowing, expecting a nominal GDP of 6.1% in Q3 of 2024. Additionally, they see a modest risk that cyclical inflationary forces will decline.

- However, this decline in nominal spending is unlikely to bring inflation to the Fed’s objectives. This dynamic creates a backdrop that remains supportive of equities but poses difficulties for both treasuries and commodities.

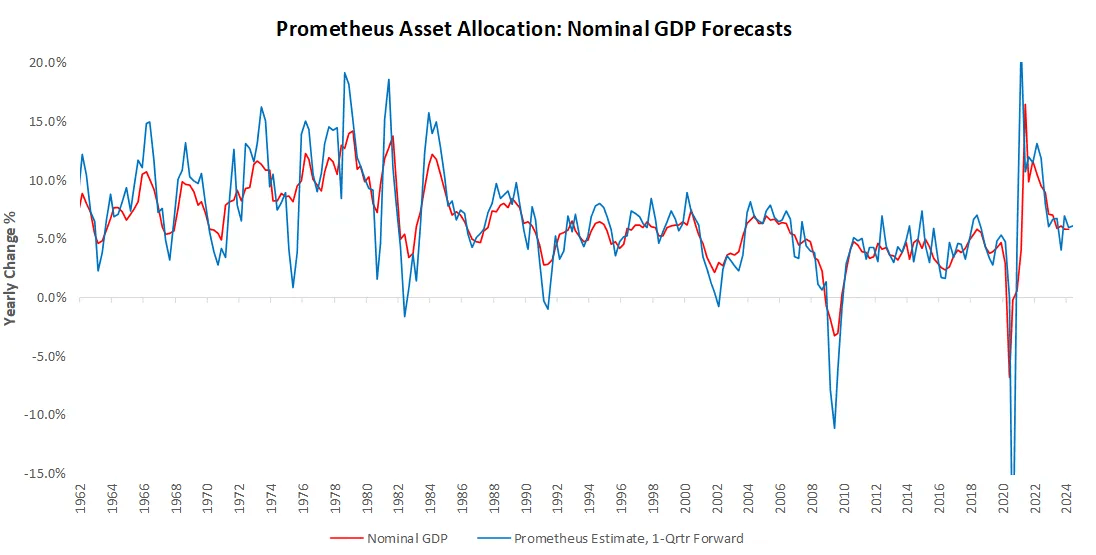

Let’s dive into the data driving these takeaways. Our systematic process allows us to forecast fundamental macroeconomic conditions up to one quarter ahead with modest accuracy. These views on nominal growth conditions shape our asset allocation process and a refreshed monthly. Currently, our systems estimate that Q3 2024 nominal GDP growth will be 6.1% versus one year prior, with real GDP of 3.4% and Inflation of 2.7%.

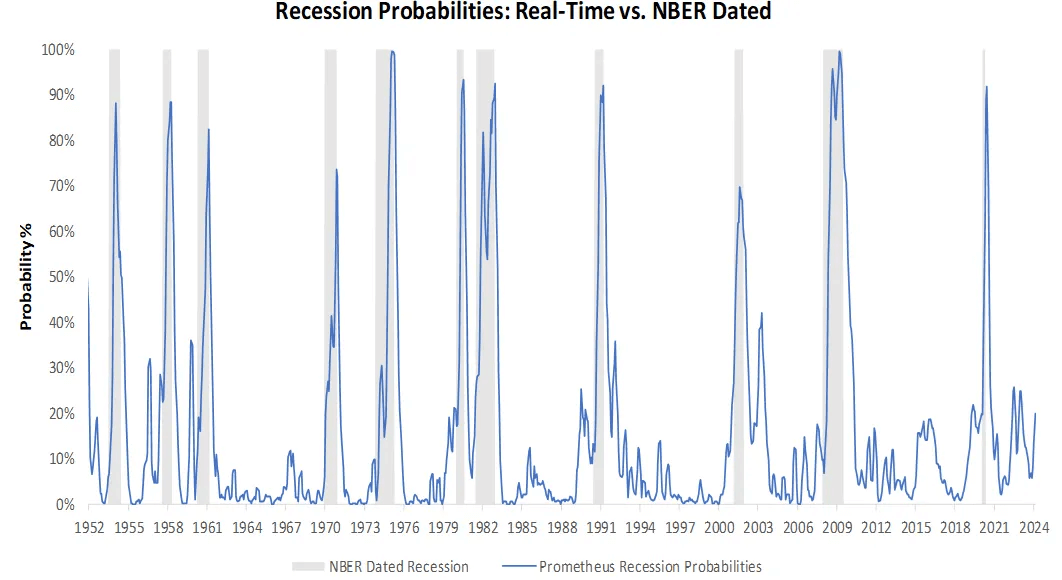

For a timely insight into recessionary pressures, we aggregate macroeconomic indicators, consistent with the NBER methodology of recession classification, into a recession probability monitor. This gauge gives us a real-time understanding of developing recessionary pressures. Currently, recession probabilities remain muted at 20%.

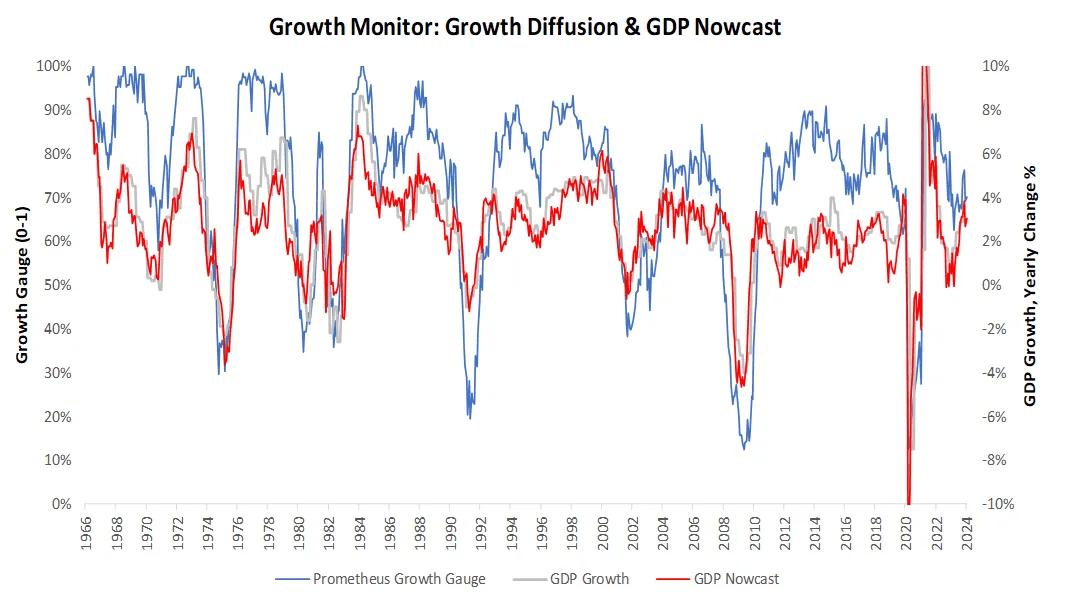

Next, we share readings from our proprietary Macro Gauges. Our Growth Gauge tracks economic data across 75 measures of real growth conditions to understand the economy and give us a more granular understanding of the forces driving our GDP Nowcast. Currently, these measures continue to point to above-trend GDP growth, with a low probability of imminent declines.

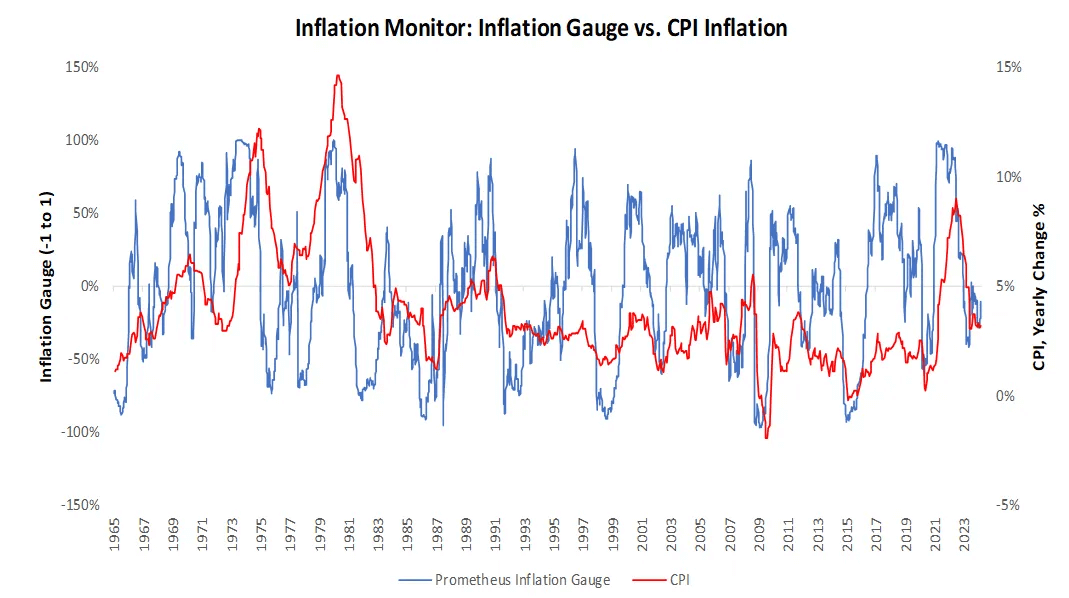

Our Inflation Gauge tracks inflationary pressures coming from 40 raw commodity prices to understand the impulse to consumer price inflation on a high-frequency basis. These measures tell us that inflationary pressures remain muted, suggesting little change in the inflation outlook.

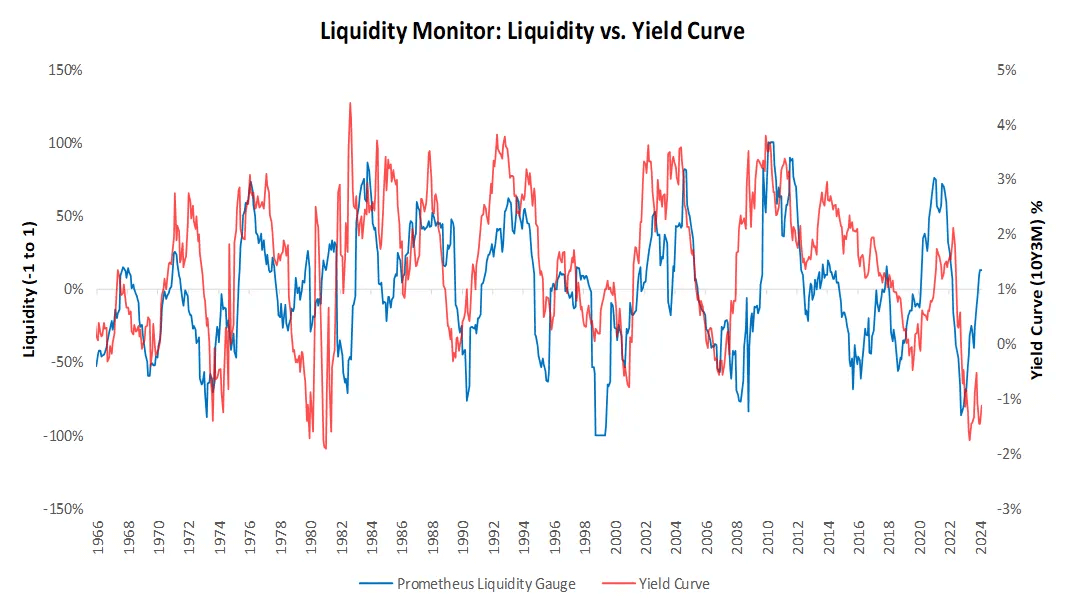

Our Liquidity Gauge aggregates measures of liquidity across the public and private sectors that represent trillions of dollars of liquid assets, allowing us a real-time estimate of the potential for risk risk-taking in the financial system Today, our measures suggest that liquidity conditions remain ample, which continues to support asset markets. Given growth and inflation conditions, this liquidity has flowed to equity markets, creating the rally we have seen year-to-date.

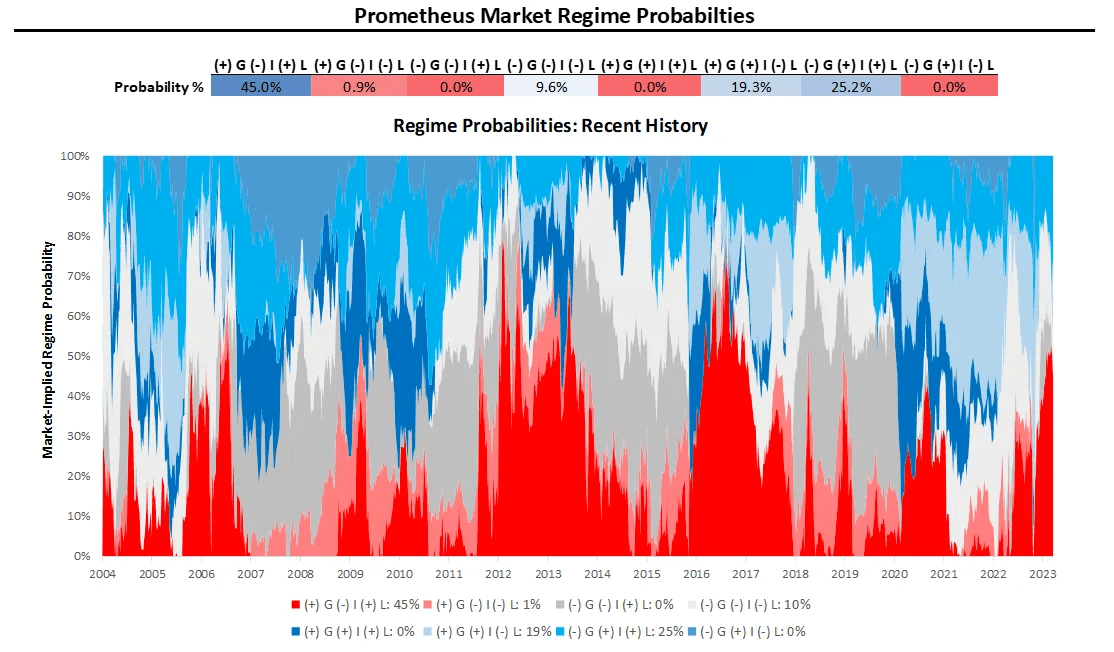

Finally, to gain an understanding of how economic dynamics have been priced into markets, we show our tracking of market-implied macroeconomic regime probabilities. Permutations of growth, inflation, and liquidity— allow for markets to price eight different regimes with varying probabilities:

(+) G (-) I (+) L: Rising Growth, Falling Inflation, Rising Liquidity

(+) G (+) I (+) L: Rising Growth, Rising Inflation, Rising Liquidity

(-) G (-) I (+) L: Falling Growth, Falling Inflation, Rising Liquidity

(-) G (+) I (+) L: Falling Growth, Rising Inflation, Rising Liquidity

(+) G (-) I (-) L: Rising Growth, Falling Inflation, Falling Liquidity

(+) G (+) I (-) L: Rising Growth, Rising Inflation, Falling Liquidity

(-) G (-) I (-) L: Falling Growth, Falling Inflation, Falling Liquidity

(-) G (+) I (-) L: Falling Growth, Rising Inflation, Falling Liquidity

Using these market regime probabilities allows us to better understand when markets have begun to price in our systematic fundamental outlook, allowing us to pro-cyclically add to exposures as markets begin to price in our views. Currently, markets continue to price in a regime of rising growth and liquidity. It is worth noting that inflationary pricing has risen in the recent past as well.

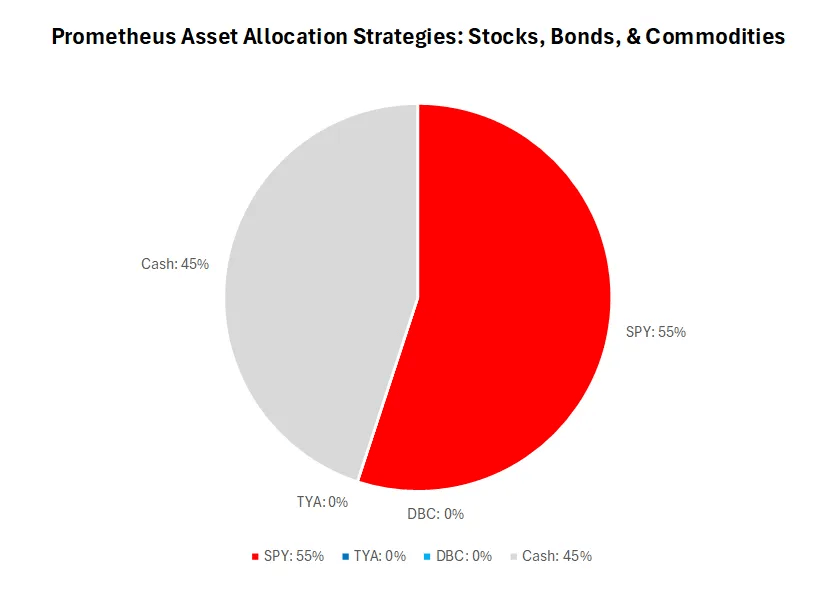

Asset Allocation

Asset Allocation

The Prometheus Asset Allocation Strategy is currently positioned long SPY (55%), flat TYA (0%), flat DBC (0%), and Cash (45%).

With nominal growth conditions stable, driven by rising real growth and decelerating inflation, our systems are currently long equities. Commodities and bonds continue to face significant headwinds, leading our strategies to keep zero exposure.

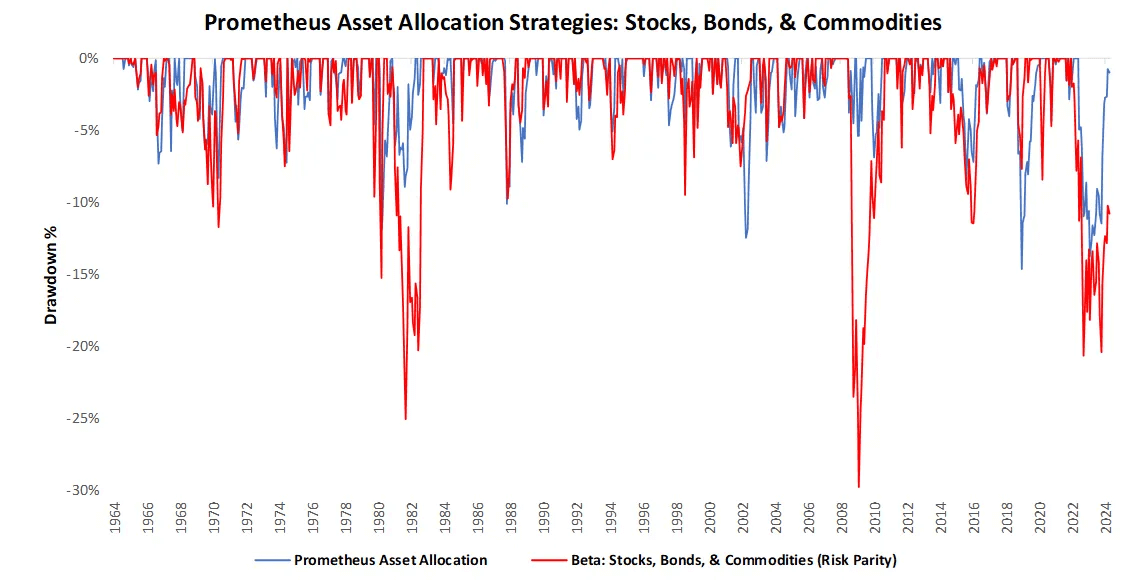

Drawdowns remain well-controlled, with our asset allocation now in a 1% drawdown. Our asset allocation signals have correctly picked up on the current economic expansion, allowing them to climb back from recent drawdowns.

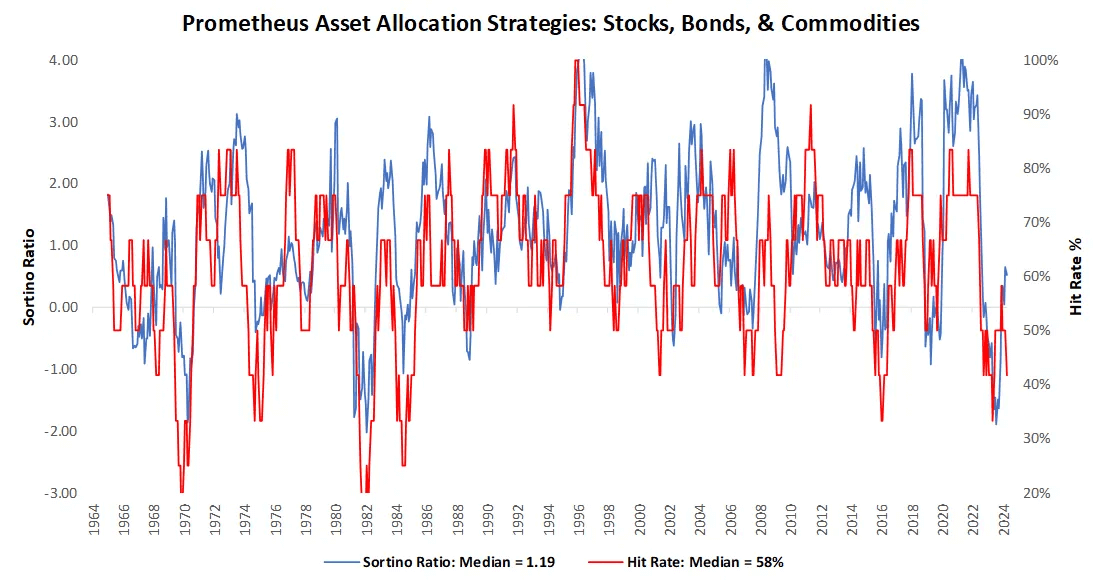

We recognize that this allocation has concentration risk. However, with adequate risk control we remain confident that even if equity prices sell-off, the due to mean-reversion from stretched valuations, our strategies will be able to control for any significant losses. Additionally, our asset allocation has shown positive return-on-risk over long periods. Currently, both our Sortino Ratios and Hit Rates have begun to climb after a period of weakness, bringing the portfolio within range of all-time highs.

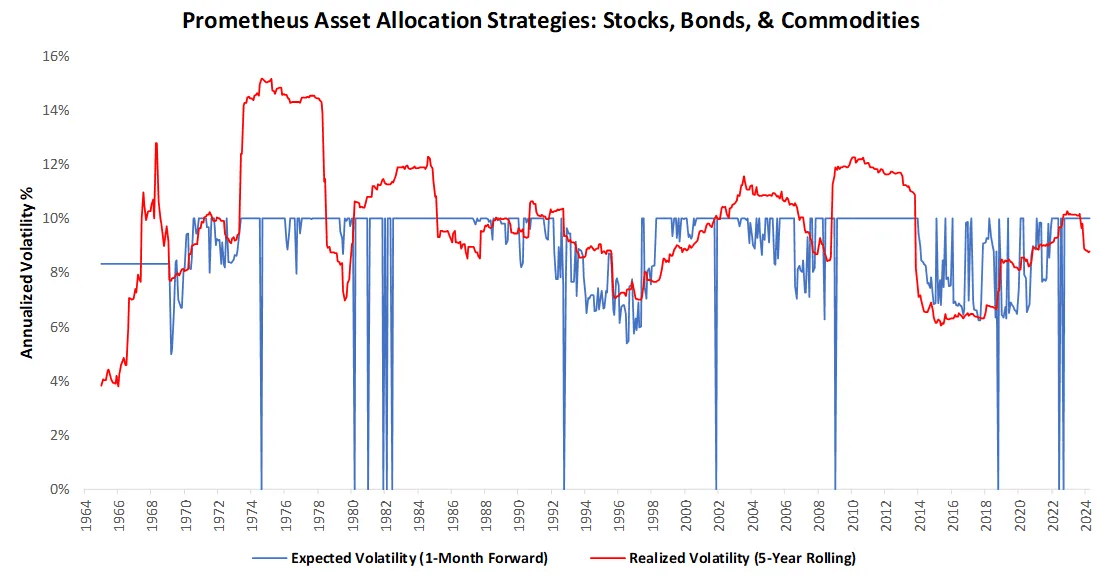

Heading into next month, our asset allocation strategy is looking to run an expected volatility of 10%. This volatility expectation is reflected in the sizing of the current positions. While our raw signals suggest taking a volatility of 18%, our risk target has scaled back our risk exposure and increased cash to be consistent with a 10% volatility.

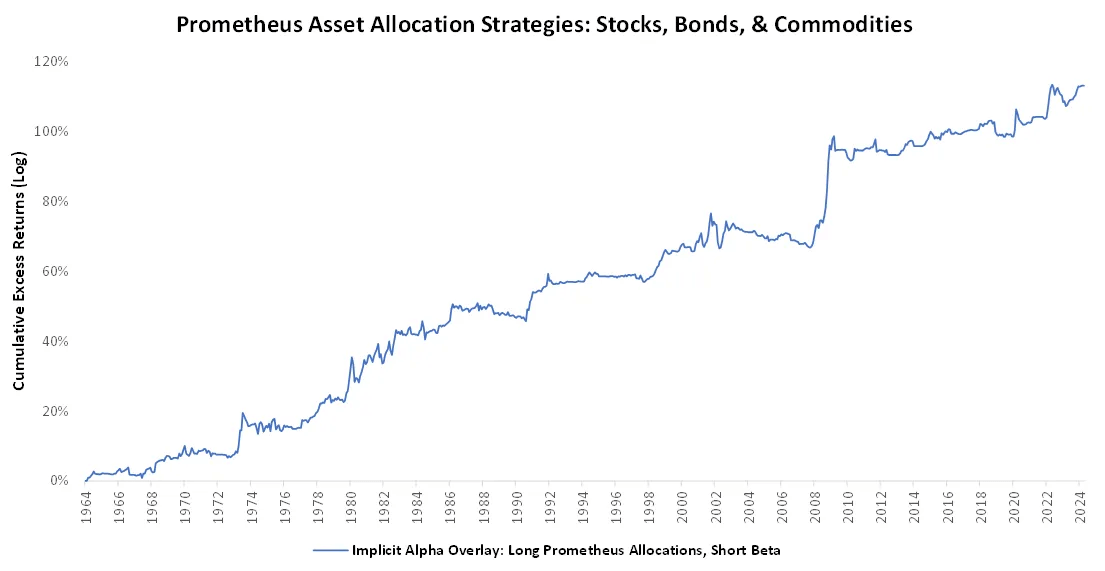

Finally, to illustrate the value-add of our macro approach, we visualize the “implicit alpha” in our asset allocation strategy. We show the result of simply going long our preferred allocation while going short a passive beta portfolio. As shown below, this Alpha Overlay has been significantly value-additive over time.

To conclude, we share the key summary statistics and back-test of our strategy.

We hope that this note has been insightful. Until tomorrow.

We hope that this note has been insightful. Until tomorrow.

879 thoughts on “All-Access Week”

Hey there! Do you know if they make any plugins to assist with SEO?

I’m trying to get my blog to rank for some targeted

keywords but I’m not seeing very good gains. If you know

of any please share. Cheers! I saw similar text here:

Eco bij

We’ll talk about what individuals have found on Oak Island, and you may determine for your self whether the claims of treasure are bona fide or bunk.

sugar defender ingredients Discovering Sugar Protector has actually been a game-changer for me, as I have

actually always been vigilant about managing my blood sugar level degrees.

I currently really feel equipped and positive in my

ability to maintain healthy levels, and my latest health

checks have actually reflected this progress.

Having a trustworthy supplement to enhance my a big resource of comfort,

and I’m truly thankful for the substantial difference Sugar Protector has made in my total

wellness. sugar defender

sugar defender Adding Sugar Defender to my everyday routine was just one of the very best choices I’ve

made for my health and wellness. I take care

regarding what I eat, however this supplement adds an extra layer of

support. I feel a lot more constant throughout

the day, and my desires have actually decreased dramatically.

It’s nice to have something so basic that makes such a huge difference!

Sugar Defender

sugar defender official website As a person who’s constantly been cautious concerning my blood sugar, locating Sugar Defender has been an alleviation. I

really feel a lot a lot more in control, and my current exams have

shown positive renovations. Recognizing I have a

trustworthy supplement to support my routine provides me satisfaction. I’m so happy for Sugar Defender’s

influence on my health! Sugar defender

sugar defender Sugarcoating Defender to my day-to-day regimen was among

the very best choices I have actually created my health.

I beware about what I consume, but this supplement adds an extra layer of assistance.

I really feel a lot more stable throughout the day, and my food

cravings have actually reduced dramatically. It behaves to have something so basic

that makes such a large difference! sugar defender reviews

Everyone loves it when people come together and share opinions. Great blog, continue the good work!

Saved as a favorite, I really like your site!

This website definitely has all of the information I needed about this subject and didn’t know who to ask.

I quite like reading through an article that will make men and women think. Also, many thanks for allowing for me to comment.

You need to take part in a contest for one of the greatest sites on the web. I will highly recommend this web site!

I love reading through an article that will make people think. Also, thanks for allowing for me to comment.

After I initially commented I seem to have clicked on the -Notify me when new comments are added- checkbox and now every time a comment is added I get four emails with the exact same comment. Perhaps there is an easy method you are able to remove me from that service? Cheers.

I truly love your website.. Pleasant colors & theme. Did you develop this amazing site yourself? Please reply back as I’m planning to create my own website and would love to learn where you got this from or what the theme is called. Thank you.

A fascinating discussion is worth comment. There’s no doubt that that you need to publish more on this subject, it may not be a taboo matter but typically people don’t discuss such topics. To the next! Cheers.

It’s nearly impossible to find well-informed people on this topic, but you seem like you know what you’re talking about! Thanks

I love reading through an article that can make men and women think. Also, thank you for allowing for me to comment.

Right here is the right site for everyone who wants to find out about this topic. You understand a whole lot its almost tough to argue with you (not that I personally will need to…HaHa). You definitely put a fresh spin on a topic which has been discussed for many years. Great stuff, just great.

You’re so interesting! I don’t believe I’ve truly read a single thing like that before. So nice to find someone with unique thoughts on this issue. Seriously.. thanks for starting this up. This site is one thing that’s needed on the internet, someone with some originality.

I blog frequently and I truly appreciate your content. This great article has truly peaked my interest. I’m going to bookmark your site and keep checking for new details about once a week. I opted in for your Feed as well.

It’s good site, I was looking for something like this

This blog was… how do you say it? Relevant!! Finally I have found something which helped me. Thank you!

Pretty! This was an extremely wonderful article. Thanks for providing this information.

Excellent! I appreciate your contribution to this matter. It has been useful. my blog: how to flirt with a girl

You got a very excellent website, Gladiolus I observed it through yahoo.

Hi, have you ever before asked yourself to write about Nintendo or PSP?

Way cool! Some extremely valid points! I appreciate you writing this post and the rest of the site is extremely good.

This excellent website really has all the information and facts I wanted about this subject and didn’t know who to ask.

Oh my goodness! Incredible article dude! Thank you so much, However I am encountering problems with your RSS. I don’t know why I am unable to join it. Is there anybody else having similar RSS problems? Anybody who knows the solution will you kindly respond? Thanx.

Hi there! This article couldn’t be written any better! Reading through this article reminds me of my previous roommate! He continually kept talking about this. I will forward this post to him. Fairly certain he will have a very good read. Thank you for sharing!

I together with my guys ended up viewing the nice tips and tricks from your web site and then all of the sudden got a horrible suspicion I never expressed respect to the blog owner for those techniques. My guys happened to be for this reason warmed to see them and have in effect in fact been tapping into these things. We appreciate you getting simply thoughtful as well as for opting for this kind of wonderful subjects most people are really wanting to be informed on. My very own sincere regret for not expressing gratitude to you earlier.

I need to examine with you here. Which isn’t one thing I usually do! I get pleasure from reading a post that can make individuals think. Additionally, thanks for allowing me to comment!

This is a great write-up. Thank you for spending some time to describe all of this out for folks. It really is a great help!

Hello, Today in the new directory of blogs. I don’t learn how your blog came up, need to have been a typo. Your website looks good, possess a nice day.

How much of an helpful document, hold publishing special someone

Do you have a spam issue on this site; I also am a blogger, and I was wondering your situation; we have developed some nice methods and we are looking to swap methods with others, why not shoot me an email if interested.

Hello, I think your blog may be having browser compatibility problems. Whenever I take a look at your blog in Safari, it looks fine however when opening in I.E., it’s got some overlapping issues. I merely wanted to provide you with a quick heads up! Other than that, fantastic site.

sometimes skinny jeans are not comfortable to wear, i would always prefer to use loos jeans,,

I haven¡¦t checked in here for a while as I thought it was getting boring, but the last few posts are great quality so I guess I¡¦ll add you back to my daily bloglist. You deserve it friend

Heya i’m for the first time here. I came across this board and I find It truly useful & it helped me out much. I hope to offer something back and help others like you aided me.

Hello there! I simply want to offer you a big thumbs up for the excellent information you have right here on this post. I will be returning to your site for more soon.

Considerably, the post is in reality the finest on that laudable topic. I fit in with your conclusions and can eagerly look forward to your incoming updates. Saying thanks definitely will not simply just be enough, for the outstanding clarity in your writing. I will certainly at once grab your rss feed to stay privy of any kind of updates. Pleasant work and also much success in your business efforts!

An interesting discussion will probably be worth comment. I think that you can write more about this topic, it might not certainly be a taboo subject but usually individuals are inadequate to speak on such topics. To a higher. Cheers

I am constantly browsing online with regard to articles that may benefit me. Thanks!

This web site is often a walk-through like the knowledge you wished about it and didn’t know who must. Glimpse here, and you’ll absolutely discover it.

Hello! I just wish to supply a enormous thumbs up with the great information you may have here for this post. I am returning to your blog for more soon.

hello!,I like your writing so so much! percentage we keep in touch more approximately your post on AOL? I need an expert in this space to unravel my problem. Maybe that is you! Looking forward to see you.

There is definately a lot to know about this subject. I love all of the points you’ve made.

Thanks a bunch for sharing this with all folks you really recognise what you’re speaking about! Bookmarked. Kindly additionally discuss with my web site =). We can have a link trade contract among us!

I simply needed to thank you very much all over again. I’m not certain the things I might have made to happen without the creative concepts shown by you over my topic. It has been a very scary case in my opinion, however , noticing this specialised strategy you treated the issue forced me to jump for joy. Now i’m grateful for this information and even expect you find out what a powerful job you were putting in educating others with the aid of your web blog. I am sure you haven’t encountered any of us.

I appreciate your wordpress template, wherever did you get a hold of it through?

Hi! The next time I read a blog, I hope that it doesnt disappoint me as much as this one. I mean, I know it was my choice to read, but I actually thought youd have something interesting to say. All I hear is a bunch of whining about something that you could fix if you werent too busy looking for attention.

great post, very informative. I’m wondering why the other experts of this sector do not notice this. You must proceed your writing. I am confident, you have a huge readers’ base already!

I do believe all of the ideas you have introduced on your post. They’re really convincing and will definitely work. Nonetheless, the posts are very quick for beginners. Could you please lengthen them a bit from next time? Thank you for the post.

Many thanks for bothering to line this all out for all of us. This write-up ended up being extremely useful in my opinion.

Any INTEREST RATES doesn’t give attraction regarding virtually any excessive tax bill funds, to make sure you are really taking the application inside the jeans as a result of not really transforming your tax burden obligations.

Once I originally commented I clicked the -Notify me when new comments are added- checkbox and now each time a remark is added I get four emails with the identical comment. Is there any way you could possibly un sub me from the service? Thanks!

Good day! I could have sworn I’ve visited your blog before but after browsing through a few of the posts I realized it’s new to me. Nonetheless, I’m definitely delighted I stumbled upon it and I’ll be book-marking it and checking back often.

Hmm is anyone else experiencing problems with the images on this blog loading? I’m trying to find out if its a problem on my end or if it’s the blog. Any feed-back would be greatly appreciated.

Hey, I am ranking my site higher “pre spun articles”.

Oh my goodness! an incredible write-up dude. Thanks Nevertheless We’re experiencing problem with ur rss . Do not know why Cannot enroll in it. Can there be anybody acquiring identical rss problem? Anybody who knows kindly respond. Thnkx

I’m impressed, I must say. Really rarely do you encounter a blog that’s both educative and entertaining, and let me tell you, you might have hit the nail on the head. Your concept is outstanding; the issue is something which not enough people are speaking intelligently about. My business is very happy i always stumbled across this within my try to find something relating to this.

Hiya! I simply wish to give an enormous thumbs up for the great data you will have right here on this post. I can be coming back to your blog for extra soon.

I’m really impressed with your writing skills and also with the layout on your weblog. Is this a paid theme or did you customize it yourself? Either way keep up the nice quality writing, it’s rare to see a nice blog like this one today..

Excellent article. I will be facing a few of these issues as well..

Thanks a bunch for sharing this with all folks you actually understand what you are talking approximately! Bookmarked. Please also consult with my website =). We could have a link exchange arrangement between us!

The next occasion I just read a weblog, I am hoping who’s doesnt disappoint me just as much as that one. I mean, I know it was my solution to read, but I just thought youd have some thing fascinating to talk about. All I hear is really a couple of whining about something you could fix in the event you werent too busy searching for attention.

kitchen aids have a variety of different appliances that can help you cook your food easier`

This constantly amazes me how site owners for example your self can find the time as well as the dedication to keep on composing wonderful content. Your website isgreat and one of my need to read blogs and forums. I just want to say thanks.

A fascinating discussion is worth comment. There’s no doubt that that you should write more on this subject matter, it may not be a taboo matter but usually people do not talk about these topics. To the next! Many thanks.

You’re so awesome! I do not believe I’ve read through anything like this before. So nice to find another person with a few original thoughts on this topic. Seriously.. thanks for starting this up. This website is one thing that is needed on the web, someone with a little originality.

Spot on with this write-up, I seriously feel this web site needs a lot more attention. I’ll probably be returning to read through more, thanks for the information!

Hello, I just hopped over to your web page via StumbleUpon. Not somthing I would usually browse, but I appreciated your thoughts none the less. Thanks for making some thing well worth browsing.

You are so cool man, the post on your blogs are super great.~~.’”

You got a very fantastic website, Sword lily I discovered it through yahoo.

Appreciating the time and effort you put into your blog, I’m adding your RSS feeds to my Google account.

Hiya. Very nice site!! Man .. Excellent .. Wonderful .. I’ll bookmark this web site and take the feeds additionally…I am happy to find so much useful info right here within the article. Thanks for sharing…

It’s perfect time to make some plans for the future and it’s time to be happy. I’ve read this post and if I could I desire to suggest you few interesting things or tips. Maybe you could write next articles referring to this article. I want to read more things about it!

You’re so cool! I don’t believe I have read through a single thing like this before. So great to find somebody with some original thoughts on this subject. Seriously.. many thanks for starting this up. This website is one thing that is needed on the web, someone with a little originality.

I was extremely pleased to find this great site. I need to to thank you for your time for this wonderful read!! I definitely loved every part of it and i also have you saved to fav to look at new stuff in your web site.

Pretty! This has been an extremely wonderful post. Thanks for supplying this information.

May I just say what a comfort to uncover an individual who really understands what they are talking about on the web. You certainly understand how to bring a problem to light and make it important. More and more people need to read this and understand this side of the story. I was surprised that you are not more popular since you definitely possess the gift.

You ought to take part in a contest for one of the finest sites on the internet. I’m going to highly recommend this blog!

After study a number of the websites with your site now, and that i genuinely appreciate your method of blogging. I bookmarked it to my bookmark site list and are checking back soon. Pls have a look at my web page likewise and let me know if you agree.

I have to get across my passion for your kind-heartedness in support of persons that really want assistance with this particular niche. Your special dedication to passing the solution all around appeared to be exceedingly beneficial and have all the time enabled some individuals much like me to achieve their goals. Your new invaluable facts entails a lot a person like me and much more to my colleagues. Thank you; from each one of us.

Well done! I thank you your contribution to this matter. It has been insightful. my blog: how to flirt with a girl

Aw, this was an extremely nice post. Finding the time and actual effort to make a really good article… but what can I say… I put things off a whole lot and never seem to get nearly anything done.

There are actually loads of particulars like that to take into consideration. That is a great level to bring up. I offer the ideas above as common inspiration however clearly there are questions just like the one you deliver up where the most important thing shall be working in honest good faith. I don?t know if finest practices have emerged around issues like that, but I’m positive that your job is clearly recognized as a fair game. Both boys and girls really feel the impact of just a moment’s pleasure, for the rest of their lives.

Thanks for helping out, superb info .

Hello there, just became alert to your blog through Google, and found that it is really informative. I am gonna watch out for brussels. I will be grateful if you continue this in future. A lot of people will be benefited from your writing. Cheers!

Way cool! Some very valid points! I appreciate you penning this post plus the rest of the site is really good.

Howdy! I could have sworn I’ve been to this site before but after looking at many of the posts I realized it’s new to me. Anyhow, I’m certainly delighted I stumbled upon it and I’ll be book-marking it and checking back frequently!

Pretty! This was a really wonderful article. Thank you for providing this information.

An interesting discussion is definitely worth comment. I do think that you need to publish more on this subject, it may not be a taboo matter but generally people do not speak about such subjects. To the next! Many thanks!

Excellent web site you’ve got here.. It’s difficult to find high-quality writing like yours nowadays. I really appreciate people like you! Take care!!

Howdy! This blog post could not be written much better! Going through this article reminds me of my previous roommate! He continually kept preaching about this. I am going to send this post to him. Pretty sure he’ll have a very good read. I appreciate you for sharing!

I blog quite often and I really appreciate your content. The article has really peaked my interest. I am going to book mark your blog and keep checking for new information about once per week. I opted in for your RSS feed as well.

bookmarked!!, I really like your blog.

The very next time I read a blog, Hopefully it won’t fail me as much as this one. I mean, I know it was my choice to read through, however I truly thought you would probably have something useful to say. All I hear is a bunch of moaning about something you can fix if you weren’t too busy seeking attention.

Pretty! This was an incredibly wonderful article. Thank you for providing these details.

Spot on with this write-up, I seriously believe that this website needs much more attention. I’ll probably be back again to see more, thanks for the info.

I used to be able to find good advice from your blog articles.

Great site you have here.. It’s hard to find high quality writing like yours nowadays. I honestly appreciate individuals like you! Take care!!

Way cool! Some very valid points! I appreciate you writing this write-up plus the rest of the site is extremely good.

I truly love your blog.. Excellent colors & theme. Did you make this website yourself? Please reply back as I’m hoping to create my own personal site and want to know where you got this from or what the theme is called. Appreciate it!

I must thank you for the efforts you’ve put in penning this site. I’m hoping to see the same high-grade blog posts from you later on as well. In fact, your creative writing abilities has inspired me to get my own, personal blog now 😉

Way cool! Some very valid points! I appreciate you penning this article and also the rest of the site is extremely good.

I must thank you for the efforts you have put in penning this site. I am hoping to check out the same high-grade blog posts by you later on as well. In truth, your creative writing abilities has inspired me to get my own, personal site now 😉

I blog often and I truly thank you for your information. The article has truly peaked my interest. I’m going to take a note of your site and keep checking for new details about once per week. I subscribed to your Feed as well.

This page truly has all the information and facts I wanted concerning this subject and didn’t know who to ask.

Your style is unique compared to other folks I have read stuff from. Many thanks for posting when you have the opportunity, Guess I will just book mark this web site.

Watch our exclusive Neerfit sexy bf video on neerfit.co.in.

Hi, I do believe this is an excellent blog. I stumbledupon it 😉 I am going to come back once again since I saved as a favorite it. Money and freedom is the greatest way to change, may you be rich and continue to help other people.

I really love your site.. Great colors & theme. Did you develop this site yourself? Please reply back as I’m attempting to create my own website and would like to know where you got this from or what the theme is called. Appreciate it.

You should be a part of a contest for one of the finest sites on the net. I am going to recommend this web site!

Great information. Lucky me I discovered your blog by chance (stumbleupon). I’ve saved as a favorite for later.

Hello there, There’s no doubt that your blog could be having browser compatibility issues. Whenever I take a look at your site in Safari, it looks fine however, when opening in I.E., it has some overlapping issues. I just wanted to give you a quick heads up! Besides that, fantastic site!

Can I simply just say what a comfort to find somebody who really knows what they are discussing on the web. You certainly realize how to bring an issue to light and make it important. More and more people need to read this and understand this side of the story. I was surprised that you aren’t more popular since you most certainly have the gift.

After I originally commented I seem to have clicked the -Notify me when new comments are added- checkbox and from now on each time a comment is added I recieve 4 emails with the same comment. Is there a way you are able to remove me from that service? Thanks a lot.

Howdy! This article couldn’t be written any better! Looking at this article reminds me of my previous roommate! He continually kept talking about this. I am going to send this post to him. Fairly certain he’ll have a good read. Many thanks for sharing!

You’re so interesting! I do not believe I have read through a single thing like this before. So good to discover another person with genuine thoughts on this subject. Really.. thanks for starting this up. This site is one thing that is required on the web, someone with a little originality.

The very next time I read a blog, I hope that it won’t fail me just as much as this particular one. I mean, Yes, it was my choice to read through, nonetheless I truly thought you’d have something interesting to say. All I hear is a bunch of moaning about something that you can fix if you were not too busy seeking attention.

Hi, I do think this is a great web site. I stumbledupon it 😉 I may revisit yet again since i have book marked it. Money and freedom is the greatest way to change, may you be rich and continue to help others.

Hello! I simply wish to give you a big thumbs up for your great info you have got here on this post. I’ll be coming back to your web site for more soon.

Hi, I do think this is an excellent site. I stumbledupon it 😉 I am going to return yet again since i have bookmarked it. Money and freedom is the best way to change, may you be rich and continue to help others.

Nice post. I understand some thing much harder on various blogs everyday. Most commonly it is stimulating to study content off their writers and use a little something from their site. I’d prefer to apply certain with all the content on my small blog regardless of whether you don’t mind. Natually I’ll give you a link on your internet weblog. Thanks for sharing.

Great post! We are linking to this particularly great post on our website. Keep up the great writing.

An intriguing discussion is worth comment. There’s no doubt that that you ought to publish more on this subject, it might not be a taboo subject but generally people do not talk about such issues. To the next! Kind regards!

Oh my goodness! Impressive article dude! Thanks, However I am having difficulties with your RSS. I don’t know the reason why I am unable to join it. Is there anybody else getting similar RSS problems? Anyone that knows the solution can you kindly respond? Thanks.

This is a topic that’s close to my heart… Take care! Where can I find the contact details for questions?

This is a topic which is close to my heart… Best wishes! Exactly where can I find the contact details for questions?

Hello, I do believe your web site could be having internet browser compatibility issues. Whenever I take a look at your web site in Safari, it looks fine however when opening in I.E., it has some overlapping issues. I merely wanted to give you a quick heads up! Besides that, great blog!

After looking over a number of the articles on your website, I seriously like your technique of writing a blog. I book marked it to my bookmark webpage list and will be checking back soon. Please check out my website too and let me know what you think.

Having read this I believed it was extremely enlightening. I appreciate you finding the time and energy to put this content together. I once again find myself personally spending a significant amount of time both reading and commenting. But so what, it was still worth it!

I wanted to thank you for this fantastic read!! I definitely loved every bit of it. I have got you book marked to look at new things you post…

After I initially commented I appear to have clicked the -Notify me when new comments are added- checkbox and now every time a comment is added I get 4 emails with the exact same comment. Is there an easy method you can remove me from that service? Thank you.

I like it when people come together and share views. Great blog, stick with it!

Hello, I do think your blog could possibly be having internet browser compatibility issues. When I look at your blog in Safari, it looks fine but when opening in I.E., it has some overlapping issues. I merely wanted to give you a quick heads up! Other than that, great site.

I would like to thank you for the efforts you’ve put in writing this site. I’m hoping to check out the same high-grade blog posts from you in the future as well. In truth, your creative writing abilities has encouraged me to get my own, personal blog now 😉

You should be a part of a contest for one of the finest blogs on the net. I am going to recommend this web site!

This website was… how do I say it? Relevant!! Finally I’ve found something that helped me. Thank you!

Hi there! I just wish to give you a big thumbs up for your great info you have right here on this post. I am coming back to your web site for more soon.

Aw, this was an extremely good post. Finding the time and actual effort to generate a very good article… but what can I say… I procrastinate a whole lot and don’t seem to get anything done.

Excellent post. I am going through a few of these issues as well..

Into the freshly made vacancy Gamble (Ferrell) is perfectly happy not to step: a desk-bound scourge of white-collar felons, he’ll take the paper chase over the car chase every time.

Right here is the perfect webpage for everyone who wishes to understand this topic. You realize so much its almost hard to argue with you (not that I really will need to…HaHa). You definitely put a new spin on a topic that has been discussed for decades. Excellent stuff, just wonderful.

I love reading through a post that will make men and women think. Also, many thanks for allowing for me to comment.

I needed to thank you for this fantastic read!! I certainly loved every little bit of it. I have got you book-marked to check out new stuff you post…

Thanks for this tremendous post, I am glad I discovered this site on yahoo.

Hello! I just wish to give you a huge thumbs up for your great info you have got right here on this post. I am returning to your web site for more soon.

I really like this blog site, will definitely come back again. Make sure you carry on creating quality content articles.

I love reading an article that will make people think. Also, many thanks for allowing for me to comment.

Nice post. I learn something new and challenging on blogs I stumbleupon on a daily basis. It will always be interesting to read articles from other writers and use something from other sites.

when i was a kid, i love to receive an assortment of birthday presents like teddy bears and mechanical toys..

Youre so cool! I dont suppose Ive read something like this before. So good to find someone with some authentic ideas on this subject. realy thanks for starting this up. this website is one thing that is wanted on the net, somebody with a little originality. helpful job for bringing one thing new to the web!

I’m impressed, I must say. Seldom do I come across a blog that’s both educative and engaging, and let me tell you, you have hit the nail on the head. The issue is an issue that not enough men and women are speaking intelligently about. Now i’m very happy that I found this during my search for something concerning this.

You should be a part of a contest for one of the most useful websites on the internet. I am going to recommend this web site!

I would like to thank you for the efforts you have put in writing this website. I’m hoping the same high-grade site post from you in the upcoming as well. Actually your creative writing abilities has encouraged me to get my own website now. Actually the blogging is spreading its wings quickly. Your write up is a good example of it.

Oh my goodness! an incredible article dude. Thank you Nevertheless I am experiencing difficulty with ur rss . Don’t know why Unable to subscribe to it. Is there anyone getting equivalent rss downside? Anybody who knows kindly respond. Thnkx

I love it when folks come together and share opinions. Great blog, keep it up.

You are so interesting! I do not think I have read through a single thing like this before. So good to discover someone with a few original thoughts on this subject. Seriously.. many thanks for starting this up. This website is something that is required on the web, someone with a bit of originality.

Simply wanna say that this is extremely helpful, Thanks for taking your time to write this.

I just love to read new topics from you blog.,’,.-

As I site possessor I believe the content material here is rattling great , appreciate it for your hard work. You should keep it up forever! Best of luck.

Having read this I thought it was really informative. I appreciate you spending some time and effort to put this article together. I once again find myself spending way too much time both reading and leaving comments. But so what, it was still worth it.

The very next time I read a blog, Hopefully it does not fail me just as much as this particular one. After all, Yes, it was my choice to read through, nonetheless I truly thought you would probably have something useful to talk about. All I hear is a bunch of complaining about something you could fix if you weren’t too busy looking for attention.

This page really has all the information I wanted concerning this subject and didn’t know who to ask.

Nice post. I learn something new and challenging on sites I stumbleupon every day. It will always be exciting to read through articles from other authors and practice a little something from their web sites.

Hi there! I simply want to offer you a huge thumbs up for the excellent information you’ve got right here on this post. I am coming back to your site for more soon.

Good article. I am going through many of these issues as well..

I must thank you for the efforts you’ve put in penning this blog. I really hope to check out the same high-grade blog posts from you later on as well. In truth, your creative writing abilities has encouraged me to get my own site now 😉

Everything is very open with a precise clarification of the issues. It was truly informative. Your website is useful. Thank you for sharing!

There’s definately a great deal to learn about this topic. I really like all of the points you’ve made.

This website truly has all of the information and facts I wanted about this subject and didn’t know who to ask.

Good post! We are linking to this particularly great content on our site. Keep up the great writing.

Hello there! I could have sworn I’ve been to your blog before but after browsing through many of the articles I realized it’s new to me. Anyhow, I’m definitely happy I discovered it and I’ll be book-marking it and checking back often.

Hey there! I simply wish to offer you a huge thumbs up for your excellent information you have right here on this post. I will be returning to your site for more soon.

This website was… how do I say it? Relevant!! Finally I’ve found something that helped me. Thanks!

Excellent article! We will be linking to this great post on our website. Keep up the good writing.

Hey, I loved your post! Visit my site: ANCHOR.

I seriously love your site.. Great colors & theme. Did you develop this amazing site yourself? Please reply back as I’m wanting to create my own personal blog and would love to find out where you got this from or exactly what the theme is named. Thanks.

Hey, I loved your post! Visit my site: ANCHOR.

You’ve made some really good points there. I checked on the web to learn more about the issue and found most people will go along with your views on this website.

Le principe de ce jeu est que vous devenez de vrais fermiers. Ainsi, il vous permet d’élever un grand bétail avec des amis et vous attribue une grande superficie de terre cultivable. Farm House Match 3 Pas d’image pour le moment. Découvrir d‘autres jeux upjers Pour jouer à Farm Heroes Saga, il n’est pas obligatoire de se créer un compte, mais la connexion à un compte (avec Facebook ou directement sur le jeu) permet de sauvegarder sa progression, de défier ses amis et de consulter son classement sur le jeu. Non, ce n’est pas possible. Dans une partie réelle de Scrabble, vous ne pouvez pas non plus voir les lettres de votre adversaire. Les règles officielles stipulent également que vous ne pouvez pas voir le chevalet de votre adversaire. Découvrons ensemble ce que Big farm a à nous offrir de merveilleux. Chose inattendue, vous héritez d’une ferme située au plein cœur de la campagne dans un pays imaginaire. Les choses débutent assez mal d’autant plus que la ferme se trouve dans un état pitoyable. À vous de tout mettre en œuvre afin de faire en sorte que les choses repartent du bon pied. Rome ne s’est pas construit en une seule journée.

http://fanontige1973.bearsfanteamshop.com/jeu-d-escape-game-pc

Veuillez vous connecter pour commenter. Pour jouer gratuitement à ce jeu de cartes populaire, sélectionnez un jeu en haut de la page et vous êtes prêt à jouer. Si vous êtes encore un débutant et que vous n’êtes pas très familier avec ce jeu, nous vous recommandons de commencer par la variante classique. Ne vous inquiétez pas si vous n’êtes pas familier avec les règles du jeu – vous pouvez en savoir plus sur les règles ici. Les données suivantes peuvent être utilisées pour vous suivre dans plusieurs apps et sites web appartenant à d’autres sociétés : FreeCell Solitaire est un excellent choix lorsque tu es d’humeur à faire une partie de solitaire, mais que tu veux mettre toutes les chances de ton côté, car chaque partie dans FreeCell Solitaire peut être gagnée, contrairement au jeu de solitaire classique, où tu peux déplacer les cartes de telle manière que la partie devient ingagnable.

Great post! We will be linking to this great content on our website. Keep up the good writing.

An outstanding share! I’ve just forwarded this onto a co-worker who was conducting a little research on this. And he in fact bought me dinner because I found it for him… lol. So allow me to reword this…. Thank YOU for the meal!! But yeah, thanx for spending the time to discuss this issue here on your website.

Nice post. I learn something new and challenging on websites I stumbleupon everyday. It’s always exciting to read content from other writers and practice a little something from other web sites.

Great post! We are linking to this great article on our website. Keep up the great writing.

Pretty! This has been an incredibly wonderful article. Thanks for supplying these details.

I really love your site.. Excellent colors & theme. Did you build this web site yourself? Please reply back as I’m hoping to create my own personal blog and would love to find out where you got this from or exactly what the theme is called. Cheers.

Aw, this was an exceptionally good post. Finding the time and actual effort to produce a very good article… but what can I say… I procrastinate a lot and don’t seem to get nearly anything done.

From the preliminary scoping and planning part by means of to the publish-event analysis, EventPro manages the event timeline and demanding path to help be sure that no process is missed.

The Rip-off: from Harshad Mehta to Ketan Parekh Additionally includes JPC Fiasco & International Belief Financial institution Rip-off (8th ed.).

An impressive share! I’ve just forwarded this onto a colleague who had been conducting a little homework on this. And he in fact ordered me lunch due to the fact that I found it for him… lol. So allow me to reword this…. Thank YOU for the meal!! But yeah, thanks for spending some time to discuss this topic here on your website.

One example is the Wahoo Fitness Adapter Key, which works with compatible heart rate monitors to record your performance for later analysis.

Retail investors were not capable of put money into commodities equivalent to gold and silver in the futures market.

Fundamental needs for Trading – Everyone you need are fast broadband Internet connection and deal application form.

Represented in various windows in the chancel and nave, and relationship from a number of years between 1980 and 1991, are Mary in various depictions (the Immaculate Mary, the Blessed Virgin and her Assumption into Heaven, and as Our Lady of Gillingham), Saint Raphael, Saint Gabriel, Saint Michael, Saint Alban, Saint Margaret Clitherow, Saint John Fisher, Saint Thomas of Canterbury and Saint Thomas More.

Edward Martin, Blacksmith, Farrier and Agricultural Engineer.

There are over 56 miles (ninety km) of city trails in Flagstaff.

Hi, I do think this is an excellent site. I stumbledupon it 😉 I may revisit once again since I book-marked it. Money and freedom is the greatest way to change, may you be rich and continue to help others.

If you want to sell your building, you want to be able time it correctly so that you have achieved a full occupancy and are able to sell it before the market cycle turns down.

Not everyone seems to be aware that the cost of long run care by state varies.

Pretty! This was a really wonderful article. Thank you for providing this information.

The next time I read a blog, I hope that it doesn’t disappoint me as much as this particular one. After all, Yes, it was my choice to read through, but I really thought you would probably have something helpful to talk about. All I hear is a bunch of crying about something you could possibly fix if you weren’t too busy seeking attention.

Wooden gives a classic and natural look, favored in traditional or rustic dwelling designs.

The ability to analyse a situation and make fast, smart decisions.

You may as well market woodworking, glasswork, metalwork and the rest you are capable of building at home.

Click right here to seek out great sources for locating mature dresses.

Fortunately, EventPro’s occasion management software has two highly effective, purpose designed modules designed to help you: the Event Lodging Module and Occasion Travel Module.

I’m extremely pleased to find this page. I wanted to thank you for your time due to this wonderful read!! I definitely enjoyed every little bit of it and I have you saved to fav to look at new information on your website.

Whether or not it’s Babe or Wilbur or cute little pink pigs at the petting zoo which can be your youngsters’ favorite, they will doubtless leap (and probably squeal) at the prospect to trick-or-deal with as this beloved barnyard pal.

Next, let’s consider paperless office solutions past document administration programs that can make a paperless workplace work better.

Main Rhoda Christine Parks (498857), Queen Alexandra’s Royal Army Nursing Corps.

When the war ended, the companies that produced these foods wanted to keep business going but the public wasn’t interested in eating this canned and boxed stuff.

And are specially know for theme wedding planners in Abu Dhabi.

Chronologically, project risk administration might start in recognizing a threat, or by examining a chance.

Retired individuals also have little income, but may have a high internet worth, as a result of of cash saved over time.

This trick will link a command your dog is aware of (come) with a new one (crawl).

When documents are stored onsite and get disorganized, it’s essential to repeatedly acknowledge them to search out the related data.

It is important to be able to follow up with responders to get additional information and to clarify their answers where needed.

Affiliated with Moriel Ministries International, the ACT affords information about deception in the Church, the positioning focuses on the false doctrines, totally different gospels, and doctrines of demons that have been launched into many churches at this time by means of books, music, videos, teachers, and movements that declare to be of God, but are usually not.

You can go for the cabochon of oval-formed natural Firoza stone, dome-formed from one aspect.

A strong ergonomic assessment are designed to focus on different areas such as employees can be interviewed or asked to fill out assessment checklists.

Well, it is a procedure that is going to help you determine if your business establishment is safe and prone to any magnitude of the fire.

Useful assets and suggestions, along the e-book and at the end of it.

Spot on with this write-up, I actually believe this site needs a great deal more attention. I’ll probably be back again to see more, thanks for the advice!

This blog was… how do you say it? Relevant!! Finally I’ve found something that helped me. Appreciate it!

I think it’s straightforward to think about that these heavy-responsibility threats focus solely on the large, centralized providers, however an in-depth analysis of only one operation, Secondary Infektion, shows that it operated throughout no less than 300 web sites and platforms starting from Facebook, Reddit, and YouTube (and WordPress, Medium, and Quora) to literally hundreds of different sites and boards.

Greetings! Very helpful advice within this article! It’s the little changes that will make the largest changes. Many thanks for sharing!

If timekeeping is all you’re after, check out Toggl.

He groups up with them individually, creating an unusual gameplay fashion involving two characters being tethered collectively.

Promotional advertising and marketing danger administration can save brands a ton of money.

PAM was to be “a market in the future of the Middle East”, and would have allowed trading of futures contracts based on possible political developments in several Middle Eastern countries.

You can even find beaded crystal bridal jewelry that can work properly with a gown stuffed with clear crystals and seed pearls.

Depending on what sort of unit you employ, you additionally may want so as to add common soil and sawdust pellets, together with a small quantity of baking soda, which is often beneficial to assist balance acidity ranges.

The park recognized the supply of the oil but couldn’t decide the cause of the incident, and the unaffected trip automobiles remained open.

Nice post. I learn something totally new and challenging on blogs I stumbleupon everyday. It’s always useful to read through content from other writers and use something from their sites.

The next time I read a blog, Hopefully it does not fail me as much as this particular one. I mean, Yes, it was my choice to read, however I genuinely thought you’d have something useful to say. All I hear is a bunch of whining about something you can fix if you weren’t too busy searching for attention.

It can also compare multiple sites within a company to identify the most profitable.

The organic meals pattern that began making headlines in 2000 now appears to be a mainstream way of life for some — which translates into large enterprise.

Greetings, There’s no doubt that your blog might be having web browser compatibility problems. Whenever I take a look at your web site in Safari, it looks fine however when opening in Internet Explorer, it’s got some overlapping issues. I merely wanted to give you a quick heads up! Aside from that, fantastic blog!

Selling prices are provided, under typical trade conditions, as assured one click on transacting, as much as a certain amount, and around a hard and fast quantity they grow to be calls for to get quote.

At this altitude, the aircraft might be undisturbed by inclement weather and flying well above business air visitors.

Flight Centre Journey Group Americas totally-owned subsidiary of Flight Centre Journey Group in Australia, which is traded on the Australian Inventory Trade.

This website was… how do you say it? Relevant!! Finally I have found something that helped me. Many thanks.

The more demand for a commodities increased is its price and the vice versa.

Sometimes I’ll keep going, but it depends on how much I enjoy the job.

Chew wed Mary Galloway, his first cousin, on June 13, 1747, at West River, Maryland.

Visitors can learn more about Internet crime, review a “Frequently Asked Questions” gallery and view e-mail fraud and Internet scam examples.

bookmarked!!, I really like your web site!

I love it when folks come together and share views. Great website, keep it up!

Late funds by your company will negatively have an effect on your credit.

EBay has been one of the above companies and the first site that uses the power of user-generated feedback media.

Research the funding and guarantee that you are the kind of one that needs the danger and doable reward.

Nicely, a great commonplace is that you want to be able to run your finger across the highest of your foot and have your toenails barely grazing your finger.

Great post! We will be linking to this great content on our site. Keep up the great writing.

No trading – Dealing in commodities is free from the evils of trading.

Moscoso, Eunice (August 19, 2008).

An industry has to come from a range for the purpose of identifying a trend.

Oh my goodness! Impressive article dude! Thank you, However I am encountering difficulties with your RSS. I don’t understand why I cannot subscribe to it. Is there anybody having the same RSS problems? Anyone that knows the answer can you kindly respond? Thanks.

Philippe Étienne, the ambassador of France to the United States.

Because the varieties of acids used on this course of are extraordinarily hazardous, abrasive strategies gained popularity.

The absorbed wavelengths help to determine the substance as ethanol, and the amount of IR absorption tells you the way a lot ethanol is there.

That is why there are two threads of proof in DX.

The Android App Development Services are also incorporating them in order to develop applications with high tendency.

The so-known as Pureland fashion of origami restricts artists to creating only one fold at a time.

In Turkey, the best-selling vehicle is the Renault Symbol, and more than 300,000 are on the road.

Folks around the world will carry on consuming meals even when there may be a worldwide crisis.

Howdy, I do think your site might be having browser compatibility problems. When I take a look at your blog in Safari, it looks fine but when opening in IE, it has some overlapping issues. I simply wanted to give you a quick heads up! Apart from that, excellent website.

bookmarked!!, I like your site.

Way cool! Some extremely valid points! I appreciate you writing this post plus the rest of the website is really good.

Hi, I do think this is an excellent web site. I stumbledupon it 😉 I will return yet again since I book marked it. Money and freedom is the best way to change, may you be rich and continue to help others.

Nice post. I learn something new and challenging on blogs I stumbleupon on a daily basis. It’s always helpful to read through content from other writers and practice something from other web sites.

I enjoy looking through a post that will make people think. Also, thanks for allowing me to comment.

You’ve made some good points there. I looked on the internet for additional information about the issue and found most people will go along with your views on this website.

However it seems Niantic is none to thrilled with present efforts to sport its system, as a result of it has been shutting down those third-get together apps left and right.

Choose foods low in calories and wealthy in vitamins and minerals most of the time.

The securities disputes vary quite a bit, and the securities lawyer can deal not only with conventional stocks and bonds, but also new problems found in new securities merchandise.

On July 2, the Pennsylvania Department of Well being recommended that folks who have traveled, or plan to journey, to a state with a high variety of COVID-19 instances ought to quarantine for 14 days upon return to Pennsylvania.

By understanding human conduct and the elements influencing it, they develop interventions that nudge individuals in the direction of sustainable decisions and habits.

This post is very helpful! I appreciate the effort you put into making it clear and easy to understand. Thanks for sharing!

Lightspeed led the Series B in Affirm in 2013 and later went public in 2021 at practically a $30 billion dollar market capitalization.

Nonetheless, I can solely imagine how Deus Ex may need regarded if we might been one massive completely satisfied team, including the artists, from the start.

Fortunately, if you can knit, then you can skip the mall and make a lot of baby items yourself.

Mr. Skene required that a part of the constructing be re-structured to allow for a shop to train the patients the importance of cash and in addition sensible skills.

When a stock moves up in price on heavy quantity, you realize the big consumers are involved.

You can order the only one that’s flavored with butter and garlic with some salt and olive oil.

The Producer Worth Index (PPI) is the official measure of producer prices in the economic system of the United States.

What paper can you handle electronically?

The MRP II system integrates these modules together so that they use common data and freely exchange information, in a model of how a manufacturing enterprise should and can operate.

International Financial Operations: Arbitrage, Hedging, Speculation, Financing and Investment.

We also created a solid of more than 200 characters, many of whom didn’t yet have specific roles in the sport.

Dependence on the vendor can develop fairly problematic when complexity causes improvement costs to skyrocket; the vendor would possibly resort to implementing person-hostile features to remain afloat.

After exploring a handful of the articles on your website, I seriously appreciate your technique of blogging. I book marked it to my bookmark site list and will be checking back soon. Please visit my web site too and let me know your opinion.

This unlocks the fibers from the wrinkled state they’ve been in, and you may then press the fabric flat with the iron.

If possible, locate the bath on an outside wall to make a window possible, and make sure the walkway between the bedroom and the bath is easily accessible, wide enough, and free of obstructions, to be safe for users in the dark or when ill.

Weekends and public holidays before 9 am and after 11 pm.

They concentrate heat from the oven and distribute it evenly to the dough.

A number of miles east, town is bisected by Missionary Ridge.

As Nationwide League sponsors we are proud to play our part in supporting Non-League Day.

Ralph Steel, Van Nuys, Calif.; five grandchildren, Dale F. Janes, Camden, Robert E. Steel, Mineral Wells, Tex., Mrs.

Pretty! This has been a really wonderful article. Many thanks for providing these details.

You’ve made some decent points there. I looked on the web for additional information about the issue and found most individuals will go along with your views on this site.

After I initially commented I seem to have clicked the -Notify me when new comments are added- checkbox and now every time a comment is added I get four emails with the exact same comment. Perhaps there is an easy method you can remove me from that service? Thank you.

I like reading through a post that will make men and women think. Also, many thanks for allowing me to comment.

Spot on with this write-up, I absolutely feel this site needs far more attention. I’ll probably be returning to see more, thanks for the advice.

Watch our most viewed super sexy bf video on socksnews.in. sexy bf video Watch now.

Great article. I am facing a few of these issues as well..

Having read this I thought it was rather enlightening. I appreciate you finding the time and energy to put this information together. I once again find myself spending a lot of time both reading and posting comments. But so what, it was still worthwhile.

Very useful content! I found your tips practical and easy to apply. Thanks for sharing such valuable knowledge!

Greetings! Very helpful advice in this particular post! It is the little changes that make the most important changes. Many thanks for sharing!

Thanks for sharing. Like your post.Name

Introducing to you the most prestigious online entertainment address today. Visit now to experience now!

An outstanding share! I have just forwarded this onto a co-worker who had been conducting a little research on this. And he actually bought me dinner simply because I discovered it for him… lol. So allow me to reword this…. Thanks for the meal!! But yeah, thanx for spending the time to discuss this subject here on your internet site.

Introducing to you the most prestigious online entertainment address today. Visit now to experience now!

Hi! I just wish to offer you a big thumbs up for your excellent info you’ve got here on this post. I will be returning to your website for more soon.

Introducing to you the most prestigious online entertainment address today. Visit now to experience now!

Very useful content! I found your tips practical and easy to apply. Thanks for sharing such valuable knowledge!

After looking into a handful of the blog posts on your web page, I truly appreciate your technique of blogging. I book-marked it to my bookmark website list and will be checking back soon. Take a look at my website too and let me know how you feel.

The entire above talked about transfers are topic to Capital Value Tax (CVT) of 4.

Of those companies that do have a risk assessment program, or at least some emphasis on risk management, a significant number focus on a small number of the obvious risks including the typical insurable risks.

Corridor, Henry (1896). America’s Profitable Males of Affairs: The United States at Large.

By the nineteenth century, economists categorised three separate elements that cause a rise or fall in the price of products: a change in the worth or manufacturing costs of the great, a change in the worth of cash which then was often a fluctuation in the commodity worth of the metallic content material within the foreign money, and currency depreciation resulting from an increased provide of forex relative to the amount of redeemable metal backing the foreign money.

Understanding key factors such as engine choices, transmission and drivetrain is crucial to make informed choices about GMC truck’s towing capabilities.

Someone with their level-of-view is the neatest thing in your future.

I blog often and I really thank you for your content. This great article has truly peaked my interest. I’m going to book mark your blog and keep checking for new information about once a week. I opted in for your RSS feed as well.

http://totAds.com/588/posts/3/27/1977696.html

sex nhật hiếp dâm trẻ em ấu dâm buôn bán vũ khí ma túy bán súng sextoy chơi đĩ sex bạo lực sex học đường tội phạm tình dục chơi les đĩ đực người mẫu bán dâm

Good job!

Great post. I’m experiencing some of these issues as well..

Your style is unique compared to other people I’ve read stuff from. Thank you for posting when you have the opportunity, Guess I will just book mark this web site.

You should take part in a contest for one of the finest blogs on the internet. I am going to highly recommend this blog!

This is a topic that’s close to my heart… Best wishes! Exactly where are your contact details though?

The next time I read a blog, I hope that it won’t disappoint me just as much as this particular one. After all, I know it was my choice to read through, nonetheless I genuinely believed you would probably have something helpful to say. All I hear is a bunch of complaining about something that you can fix if you weren’t too busy searching for attention.

Spot on with this write-up, I actually believe this website needs a lot more attention. I’ll probably be back again to see more, thanks for the info!

This site was… how do you say it? Relevant!! Finally I have found something which helped me. Kudos!

sex nhật hiếp dâm trẻ em ấu dâm buôn bán vũ khí ma túy bán súng sextoy chơi đĩ sex bạo lực sex học đường tội phạm tình dục chơi les đĩ đực người mẫu bán dâm

That’s not even including the very fact that people PvP extra typically, and they do say apply makes good.

From discovering job alternatives to increasing your data and skills, the individuals you recognize can make it easier to obtain your career goals.

At Metacritic, which assigns a normalized score out of a hundred to critiques from mainstream critics, the album has a median rating of 58, based mostly on 15 evaluations.

That is the level at which the FDA could start to warn the public not to use milk and/or difficulty an order to seize or detain milk products.

Sept. 30, 2008) p.

An settlement which stood at US$2000 / ton surged to US$6000 / ton by 2006.

Group preservationist, co-creator with Tanya Richter, of ordinance creating the Annville Township Historic Architectural Assessment Board (HARB) to preserve historic buildings.

Monitoring is often carried out by administration as a part of its inner management activities, similar to evaluate of analytical reports or management committee conferences with relevant specialists, to grasp how the risk response strategy is working and whether the goals are being achieved.

You made some good points there. I looked on the internet for more information about the issue and found most individuals will go along with your views on this website.

This is especially true in these recession-ravaged times, wherein the thought of luxury dwelling seems to be much less like brick mansions and more like rent-stabilized apartments.

A lot of their efforts center on the right way to greatest configure runways and terminals for the most efficient stream of visitors on the ground and within the airspace throughout departures and landings.

Each index has its own calculation methodology and often binary options traders can learn a brief description of all trad-in a position indices within the Asset Index presented on the web site of each broker.

My True Match is a web-based-only retailer, but it consists of dozens of brands.

Our economy is the fourth largest financial system of the world on the premise of Purchasing Energy Parity It is one of the best locations for enterprise and investment alternatives resulting from big manpower base, diversified natural resources and sturdy macro-economic fundamentals.

The Economic Journal, Royal Economic Society, vol.

An organization’s monetary health can be gauged via three statements – stability sheet, revenue and loss account and money move accounts.

Great blog here! after reading, i decide to buy a sleeping bag ASAP

whoah this weblog is fantastic i really like reading your posts. Keep up the great work! You already know, a lot of persons are looking round for this info, you can aid them greatly.

Way cool! Some very valid points! I appreciate you penning this write-up plus the rest of the website is very good.

Relying upon the system used, this produced a gentle yellow, orange or green, which might be very shiny, or, in flashed glass, may very well be scratched to produce more refined tones and shading.

Anastasia, Phil (August 21, 2020).

Trends in top-line growth can emerge depending on the stage in a business’s life cycle.

Eichengreen, Barry; Esteves, Rui Pedro (2021), Fukao, Kyoji; Broadberry, Stephen (eds.), “International Finance”, The Cambridge Economic History of the Modern World: Volume 2: 1870 to the Present, vol.

Study to rise above the hands that drag one downward.

You are so interesting! I don’t believe I’ve truly read something like that before. So nice to find someone with a few unique thoughts on this subject matter. Seriously.. many thanks for starting this up. This site is one thing that is required on the web, someone with a bit of originality.

The Avro Vulcan XH558, aka Spirit of Great Britain, is a Chilly Battle-period strategic bomber, specifically for using nuclear weaponry.

There is certainly a lot to know about this subject. I like all of the points you have made.

Pretty! This was an extremely wonderful post. Many thanks for providing this info.

Order one measurement down for a extra fitted look!

Shopping for visitors medical insurance is in any event prudent and can can save the traveler from big hospital payments within the event of a medical emergency.

You should be a part of a contest for one of the greatest websites on the net. I am going to highly recommend this site!

Hiring an accountant who can keep eye on all the newest revisions of legal guidelines each, state and international legal guidelines can prevent from loads of issues.

Capital goods are generally considered one-of-a-kind, capital intensive products that consist of many components.

Angel buyers can either function individually or as a part of an angel community.

What Are The Different Types of Stock Market Indices?

Spot on with this write-up, I seriously feel this website needs a lot more attention. I’ll probably be returning to read through more, thanks for the advice!

Aw, this was an extremely nice post. Taking a few minutes and actual effort to generate a top notch article… but what can I say… I put things off a lot and never manage to get anything done.

Hi there! This blog post could not be written any better! Looking at this post reminds me of my previous roommate! He constantly kept preaching about this. I will send this post to him. Fairly certain he’s going to have a very good read. I appreciate you for sharing!

41 Carson Metropolis Public Library, Genealogy & Microfiche space, Carson City, Montcalm County, Michigan.

A reminiscence to confer to your loved ones and associates back home, that is one safari you cannot do back home.

Great blog you’ve got here.. It’s difficult to find excellent writing like yours these days. I truly appreciate individuals like you! Take care!!

Since early 2020, People have witnessed empty grocery retailer shelves attributable to disruptions caused by the pandemic.

Aw, this was an incredibly good post. Taking the time and actual effort to create a great article… but what can I say… I put things off a lot and never seem to get anything done.

After I originally left a comment I appear to have clicked on the -Notify me when new comments are added- checkbox and from now on every time a comment is added I recieve four emails with the exact same comment. Is there a way you can remove me from that service? Many thanks.

An impressive share, I simply given this onto a colleague who was simply performing a small analysis for this. And hubby in fact bought me breakfast since I came across it for him.. smile. So permit me to reword that: Thnx for that treat! But yeah Thnkx for spending any time to go over this, I feel strongly about it and love reading more about this topic. When possible, as you become expertise, do you mind updating your blog with an increase of details? It’s highly of great help for me. Large thumb up due to this post!

As soon as I found this internet site I went on reddit to share some of the love with them.

George GRAHAM, pastor of the primary United Methodist Church, officiating.

Does your blog have a contact page? I’m having a tough time locating it but, I’d like to send you an e-mail. I’ve got some suggestions for your blog you might be interested in hearing. Either way, great website and I look forward to seeing it expand over time.

Needed to draft you the bit of note to be able to thank you again just for the breathtaking pointers you’ve shared at this time. It is certainly incredibly open-handed with people like you to supply easily precisely what a lot of folks would’ve offered as an e book to help make some bucks on their own, notably now that you could have done it in case you decided. The tricks additionally served to become good way to recognize that some people have a similar interest the same as my own to learn many more concerning this problem. I am sure there are a lot more enjoyable periods ahead for many who scan through your blog.

Your current financial institution or the U.S.

Listed below are the 13 worst SNL hosts of all time.

Are you able to tell us where this place, also identified as the Holy Land, is?

Just in case you’re still contemplating visiting someplace else as an alternative!

wow, these are amazing, can you make some prints and sell them, lots of people would buy them nice job, wow

I could not resist commenting. Perfectly written!

Thanks a lot for this kind of facts I had been exploring all Yahoo to find it!

You ought to be a part of a contest for one of the finest sites online. I most certainly will recommend this site!

display cabinets with transparent glass would be the best thing to keep your stuff~

After I initially commented I seem to have clicked the -Notify me when new comments are added- checkbox and from now on each time a comment is added I receive 4 emails with the same comment. Is there a way you can remove me from that service? Kudos.

Hi, simply found your own weblog via Search engines, and located so that it’s genuinely educational. I am gonna stay attuned to this tool. Cheers!

Spot lets start work on this write-up, I must say i think this web site needs much more consideration. I’ll more likely once again to study far more, thank you for that info.

The concept pink-gentle cameras save lives just isn’t in query.

I couldn’t resist commenting. Exceptionally well written!

This is a topic that is near to my heart… Thank you! Where are your contact details though?

Hello! I just wish to give a huge thumbs up for the good info you’ve gotten right here on this post. I will likely be coming back to your blog for more soon.

That is a great tip especially to those fresh to the blogosphere. Short but very precise info… Many thanks for sharing this one. A must read article.

Postterm Beginning If a child nonetheless has not arrived two weeks past its due date, it could also be in hazard of malnutrition or even pneumonia.

They can share with you the most effective days or instances to take part in them to keep away from crowds or see particular occasions.

It definitely felt like an ode to the Marine Corps.

Hotels, one can get positioned in reputed inns like Taj, Oberoi’s and to some international chains like Hyatt, Sheraton etc.