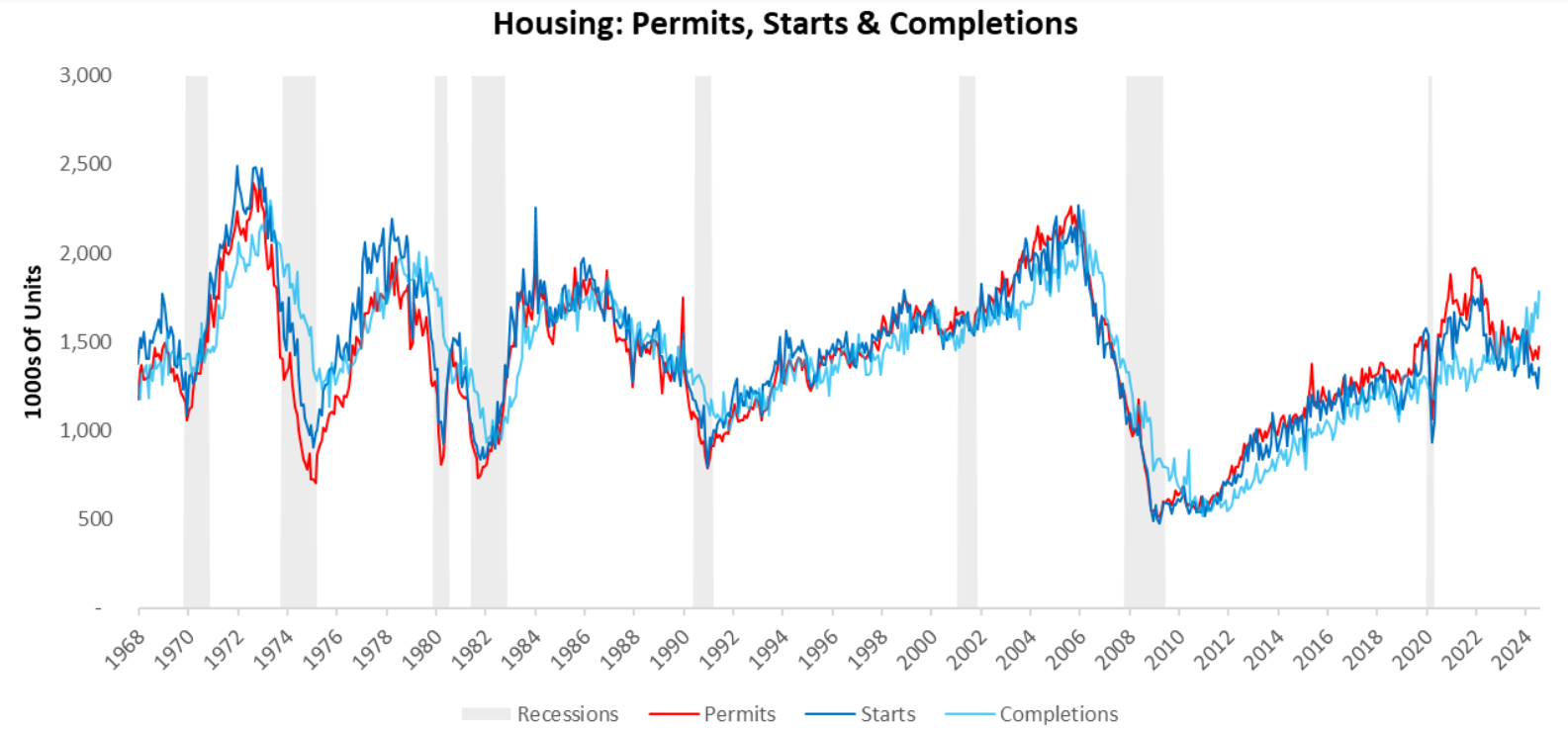

Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real-time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

Our primary takeaways are as follows:

- The recent trend in housing data showed signs of a sequential improvement, with building permits, starts, and completions increasing.

- However, upon zooming out, we continue to observe pressures persist in our estimates for residential investment which remain in contraction.

- Additionally, our cyclical measures of residential investment such as permit slowdown and pending construction projects are also within the ballpark of a recession.

- In the context of markets, homebuilders’ equity prices have increased sequentially, in line with the current relief in the residential investment trend. However, pressures persist and we continue to remain in a Slowing but Growing economy.

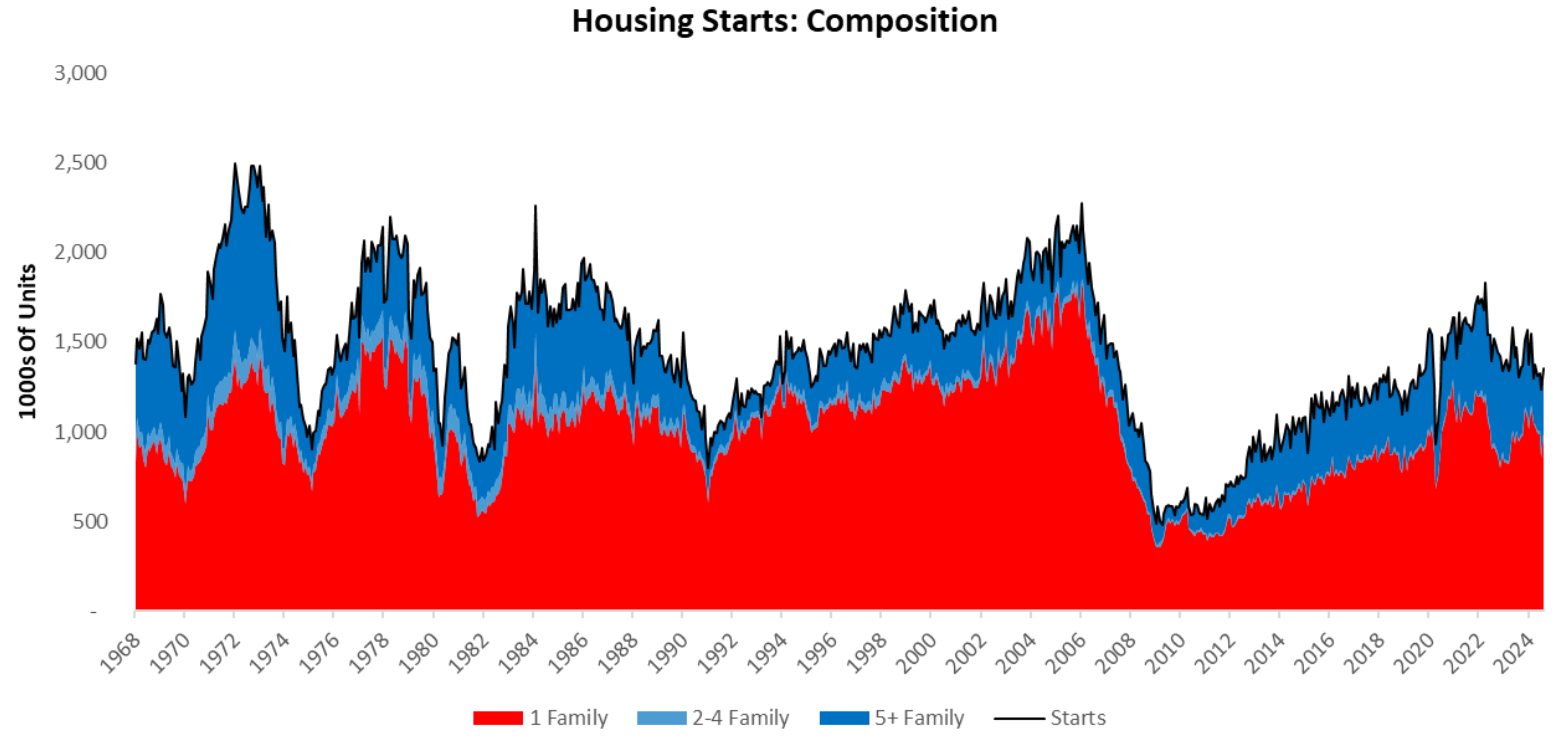

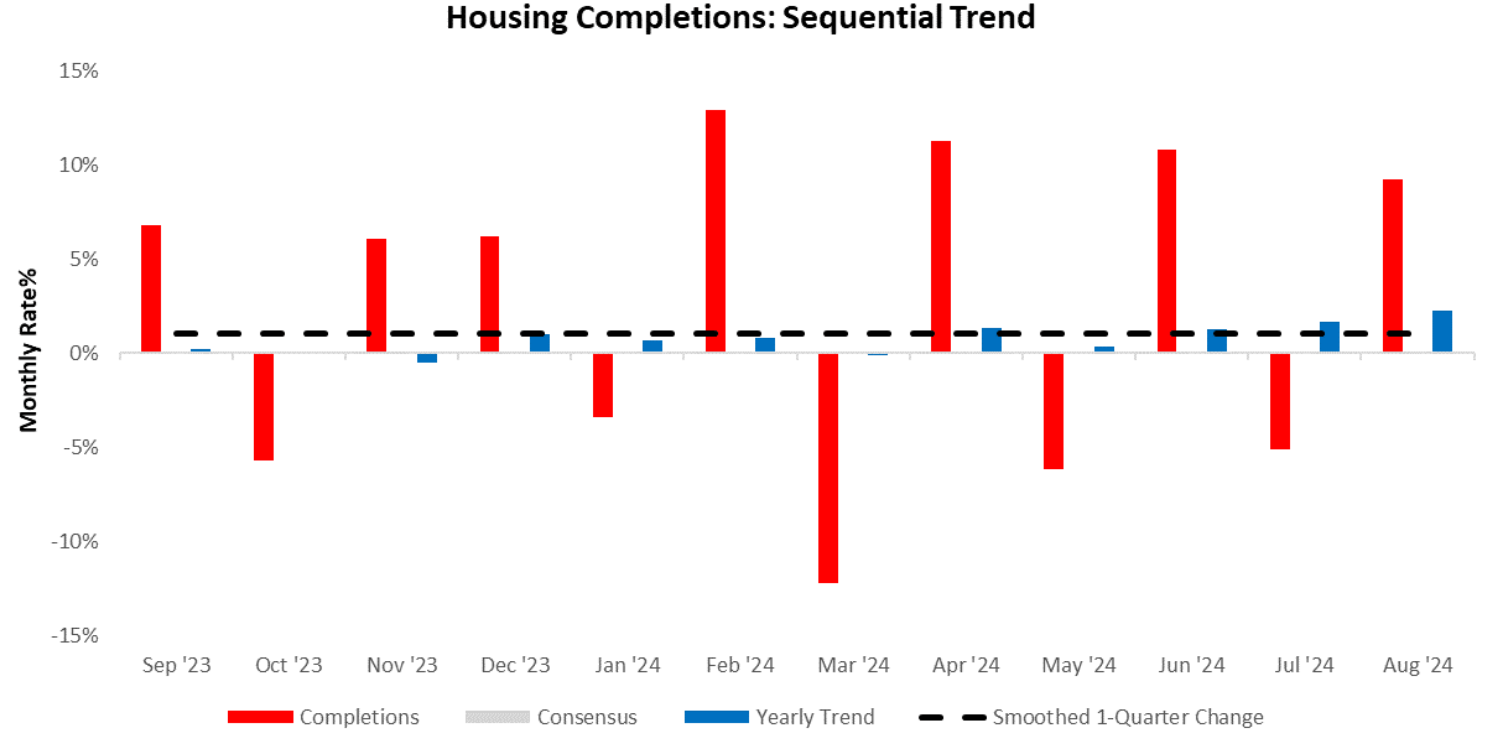

The latest data for August showed housing permits increased by 4.91%, housing starts increased by 9.62%, and housing completions increased by 9.22%. Below, we show the current levels for the same:

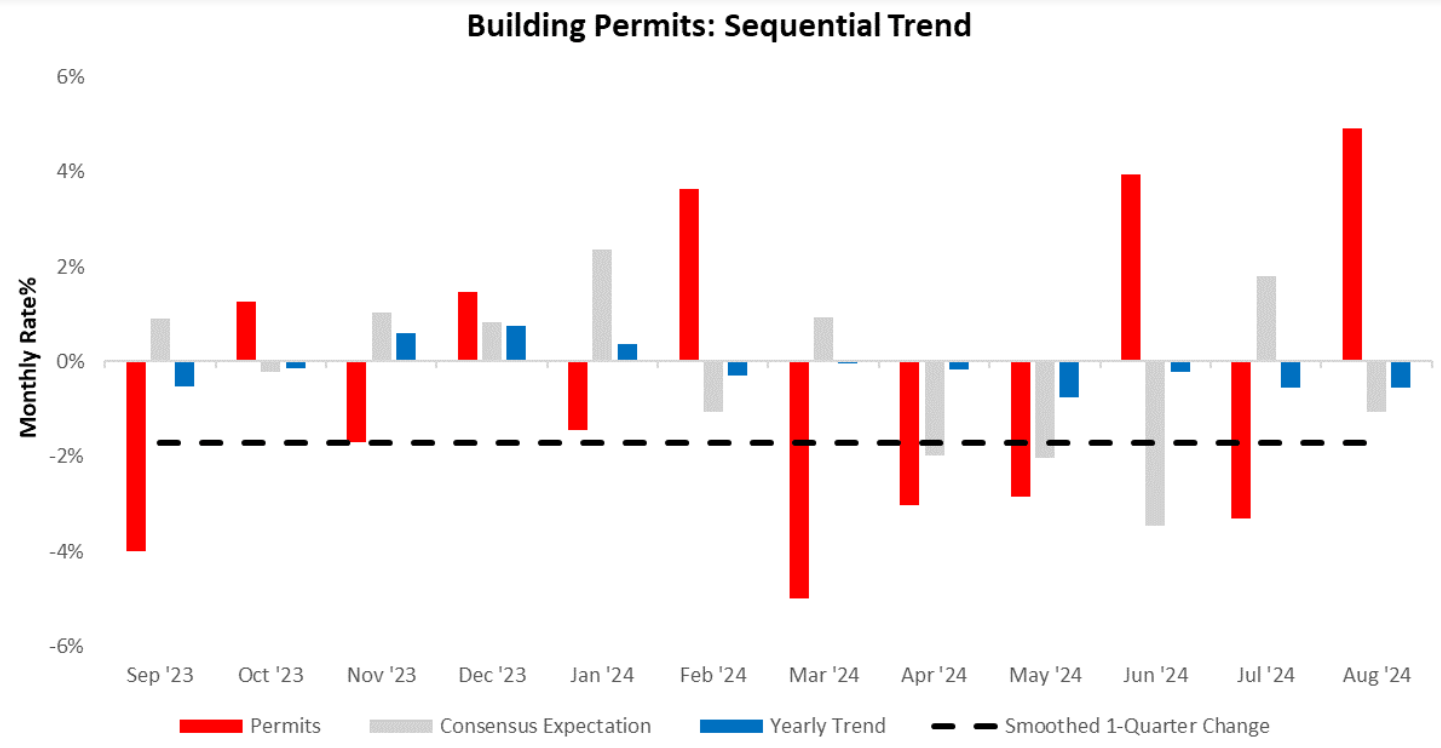

Zooming into the data, housing permits increased by 4.91%, surprising consensus expectations of -1.05%. Below, we show the sequential evolution of the data, along with the smoothed one-quarter change in the most recent data. We provide the smoothed version as monthly housing data contains significant noise.

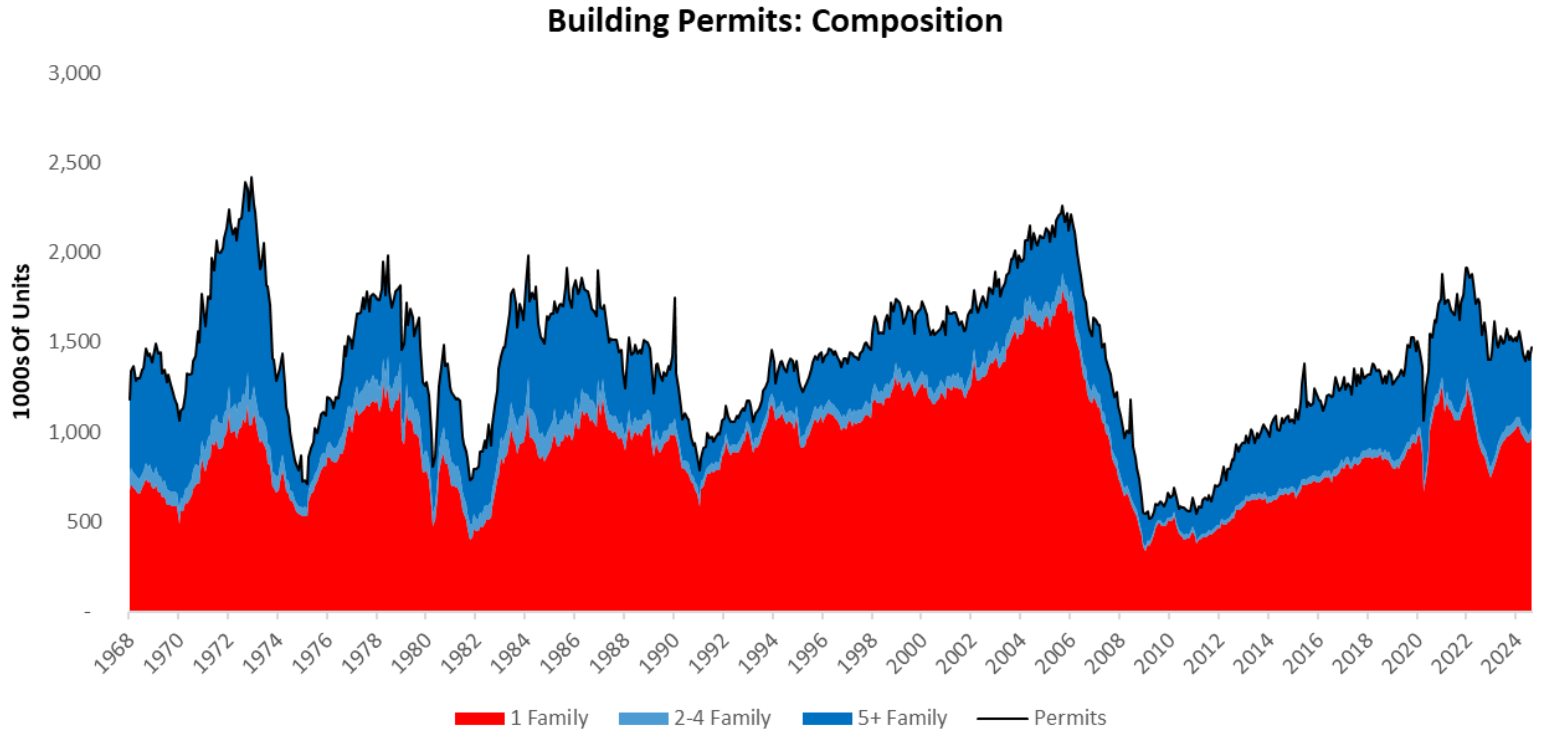

For further context, we zoom out to show the contributions from single-family homes (-5), two-family homes (-7), and multi-family homes (-91) to the fall (-103) in total permits over the last year:

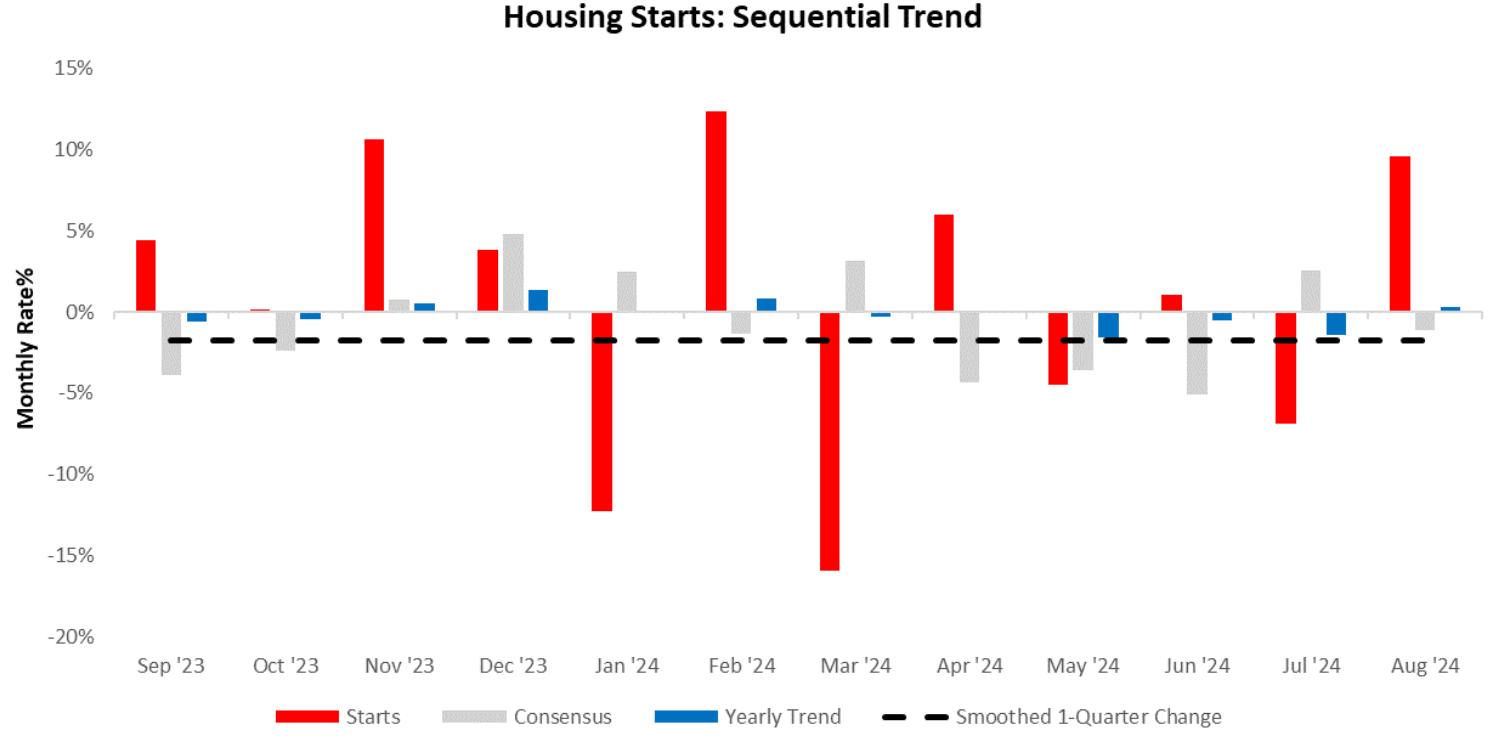

Consistent with the permits data, housing starts data showed starts increased by 9.62%, surprising consensus expectations of -1.13%. Below, we show the sequential evolution of the data, along with the smoothed one-quarter change in the most recent data. We provide the smoothed version as monthly housing data contain significant noise.

To illustrate the bigger picture, we show the contributions from single-family homes (135), two-family homes (-7), and multi-family homes (-22) to the rise (51) in total starts over the last year:

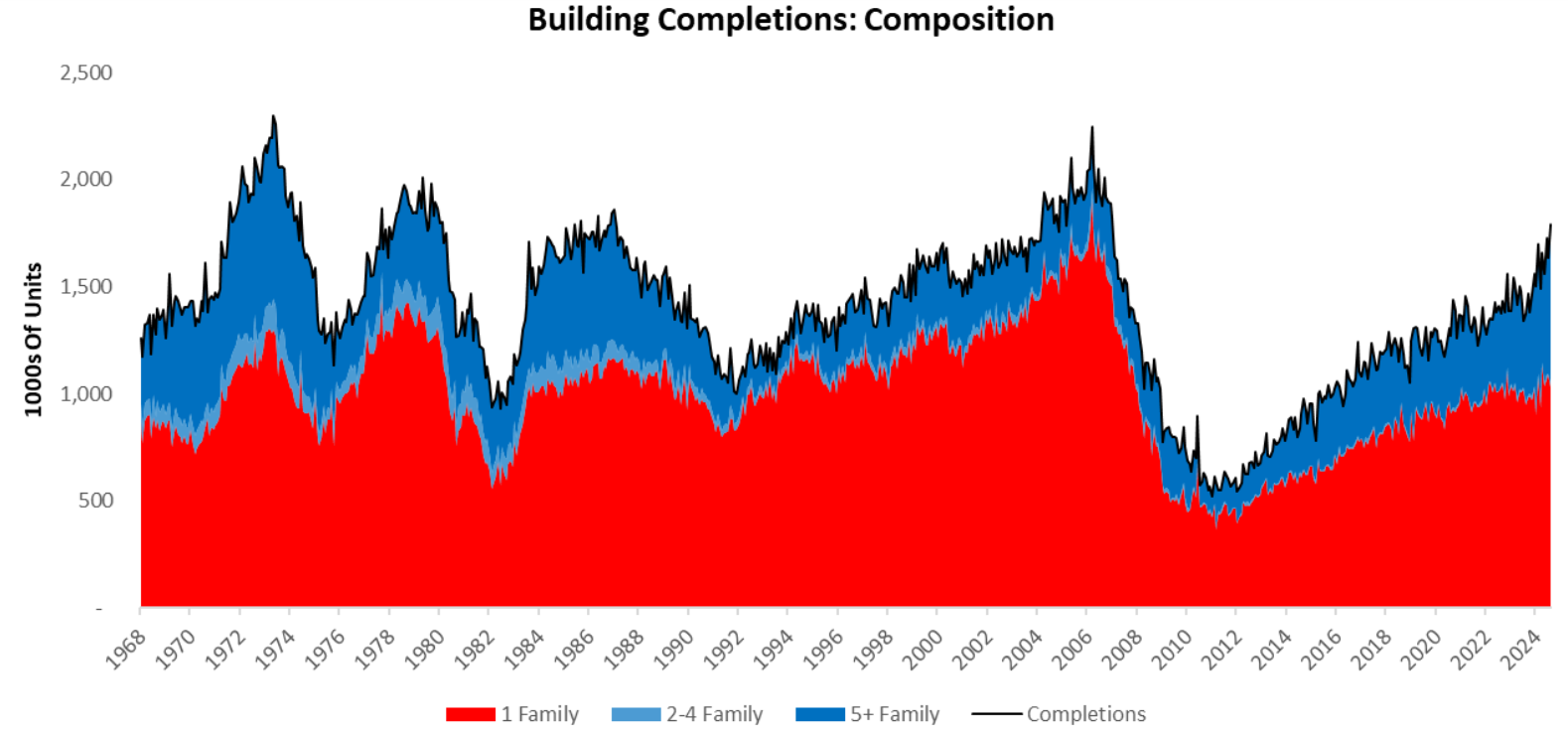

Last, in our sequential analysis, we turn to housing completions data, which showed completions increase by 9.22%. Below, we show the sequential evolution of the data, along with the smoothed one-quarter change in the most recent data. We provide the smoothed version as monthly housing data contain significant noise.

We show the contributions from single-family homes (-61), two-family homes (8), and multi-family homes (327) to the rise (415) in total completions over the last year:

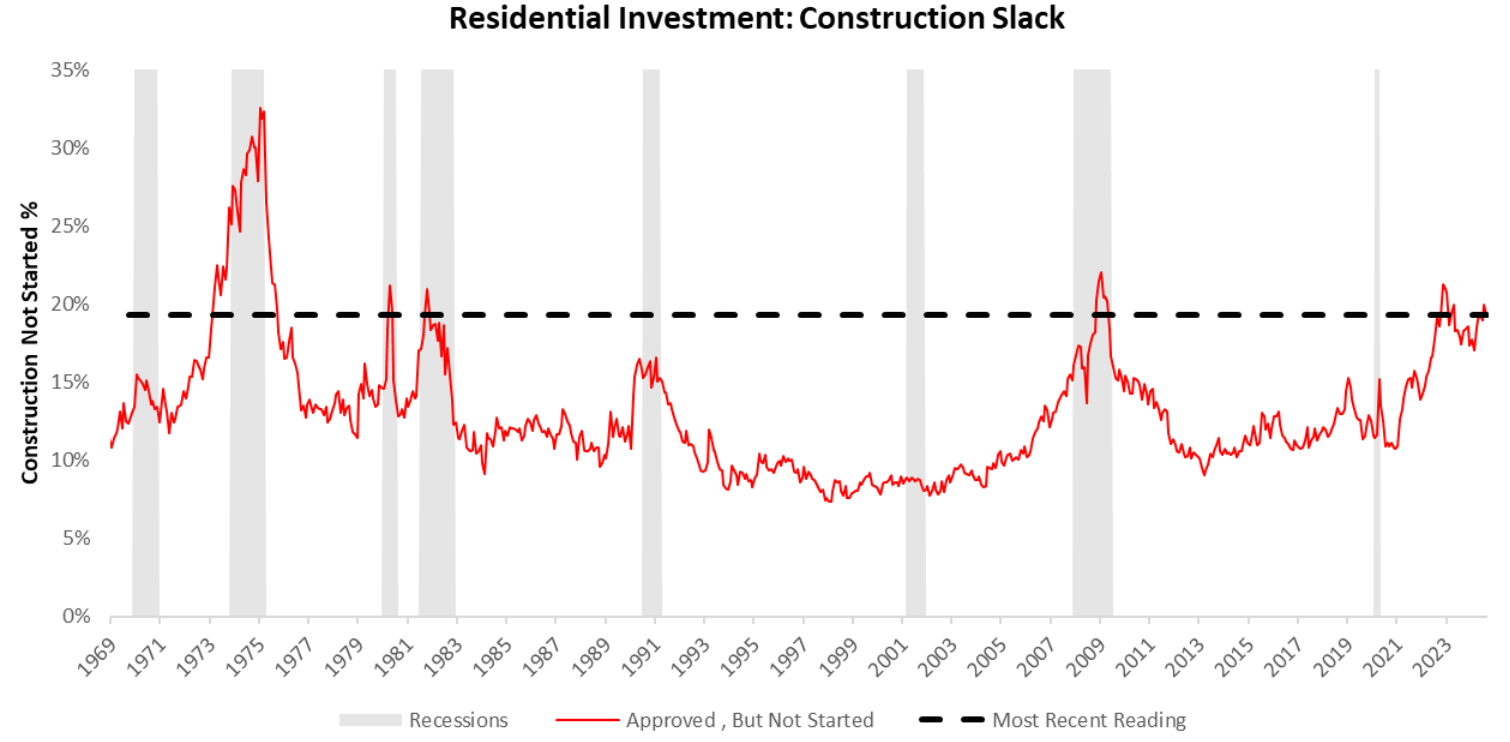

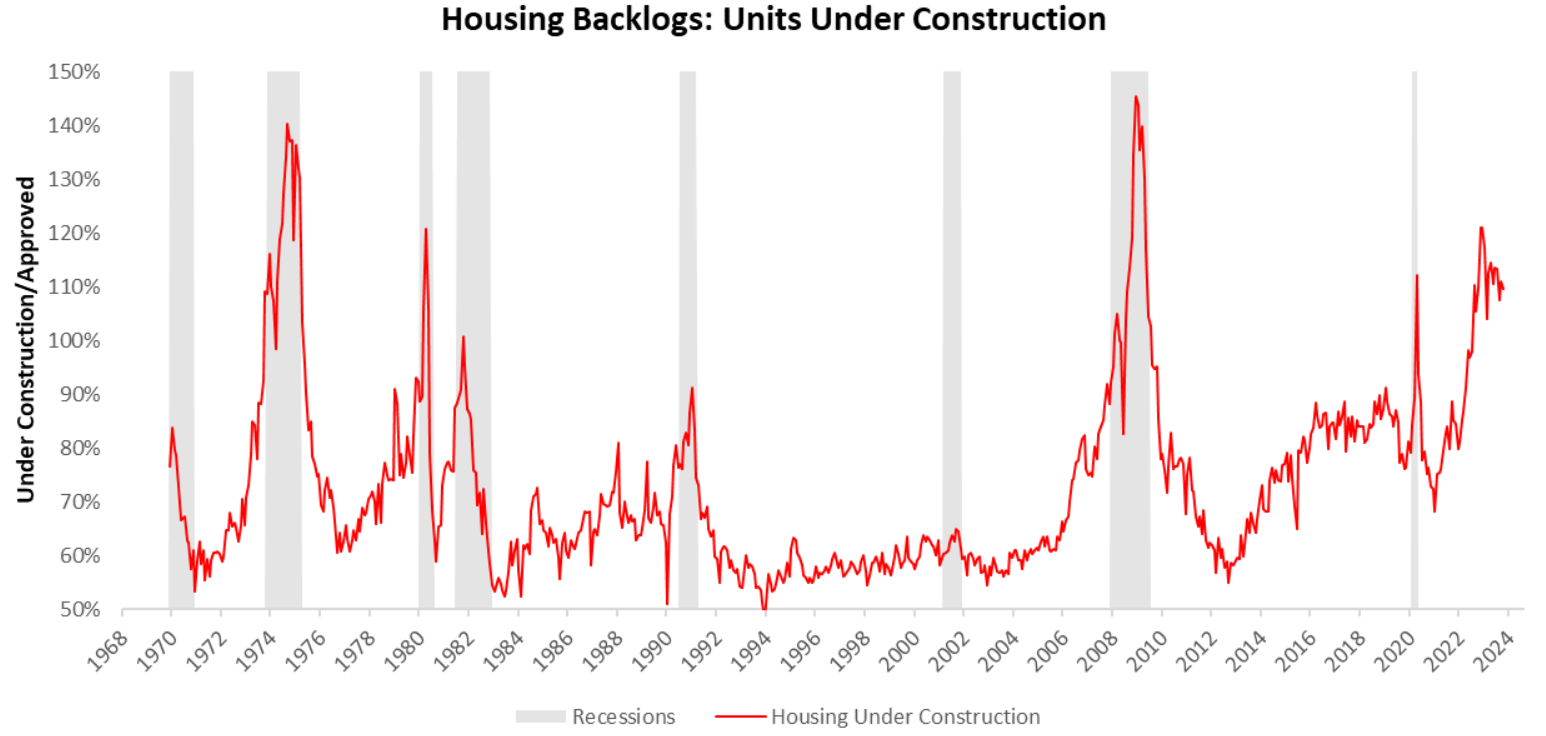

To get a better sense of where we are in the housing cycle, we examine how many construction projects have been approved but not yet started. According to the latest data, 19% of projects are yet to begin construction. Looking through history, housing-led recessions usually begin when this measure of construction slack is around 15% suggesting that we are within the ballpark of a recession.

Now, while this rise in unstarted projects can often be a sign of weakness in perceived end demand, it can also be due to existing backlogs in construction. Below, we show a measure of these backlogs, which show the number of homes under construction relative to those under construction:

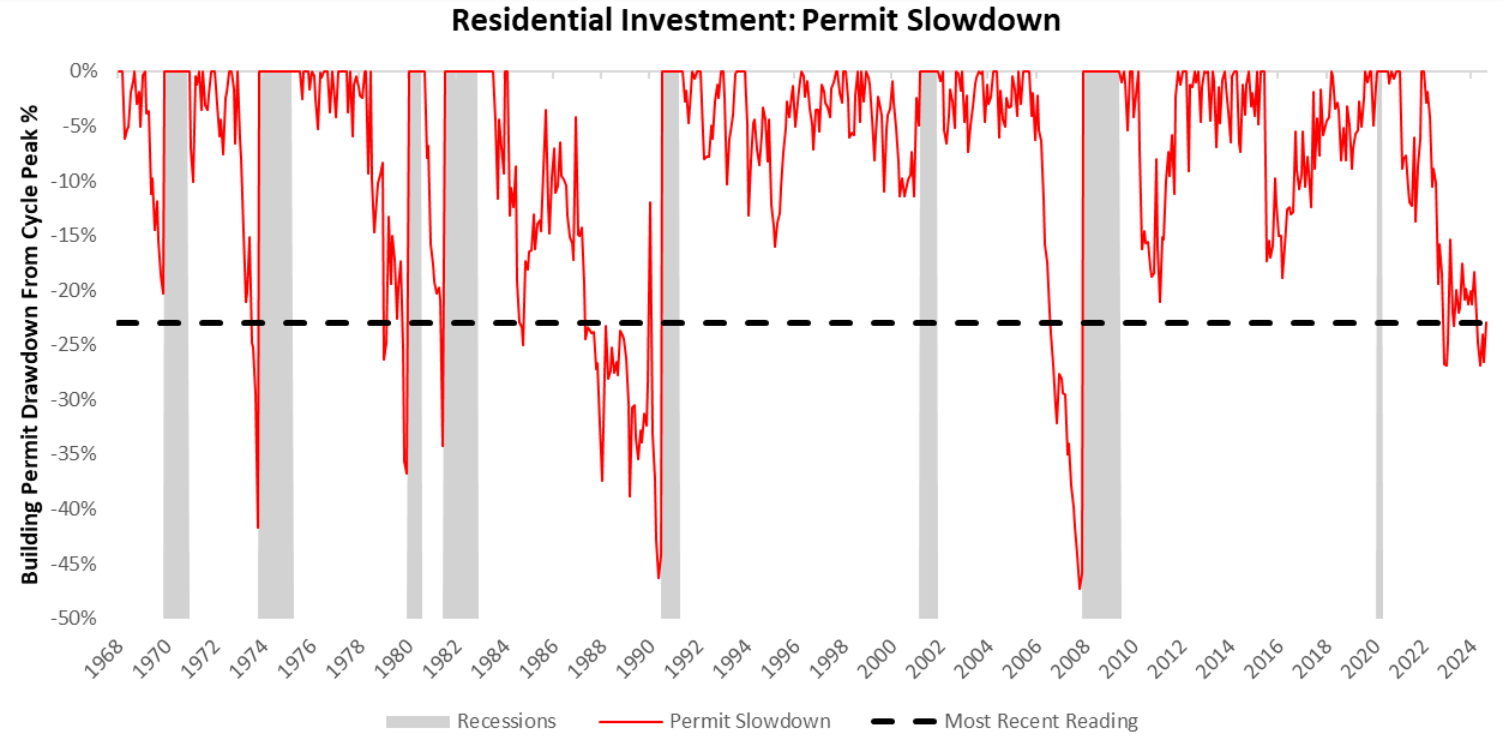

We conclude by examining another measure of housing weakness, i.e., permit slowdowns- which measures how much building permits have fallen from their cycle highs. Large drops in permits bode ill for the broader residential investment complex & GDP. The latest data shows that building permits are off their cycle highs by -22.98%. Typically, housing-led recessions usually begin when this measure of cyclical weakness is around -29% suggesting that we are within the ballpark of a recession.

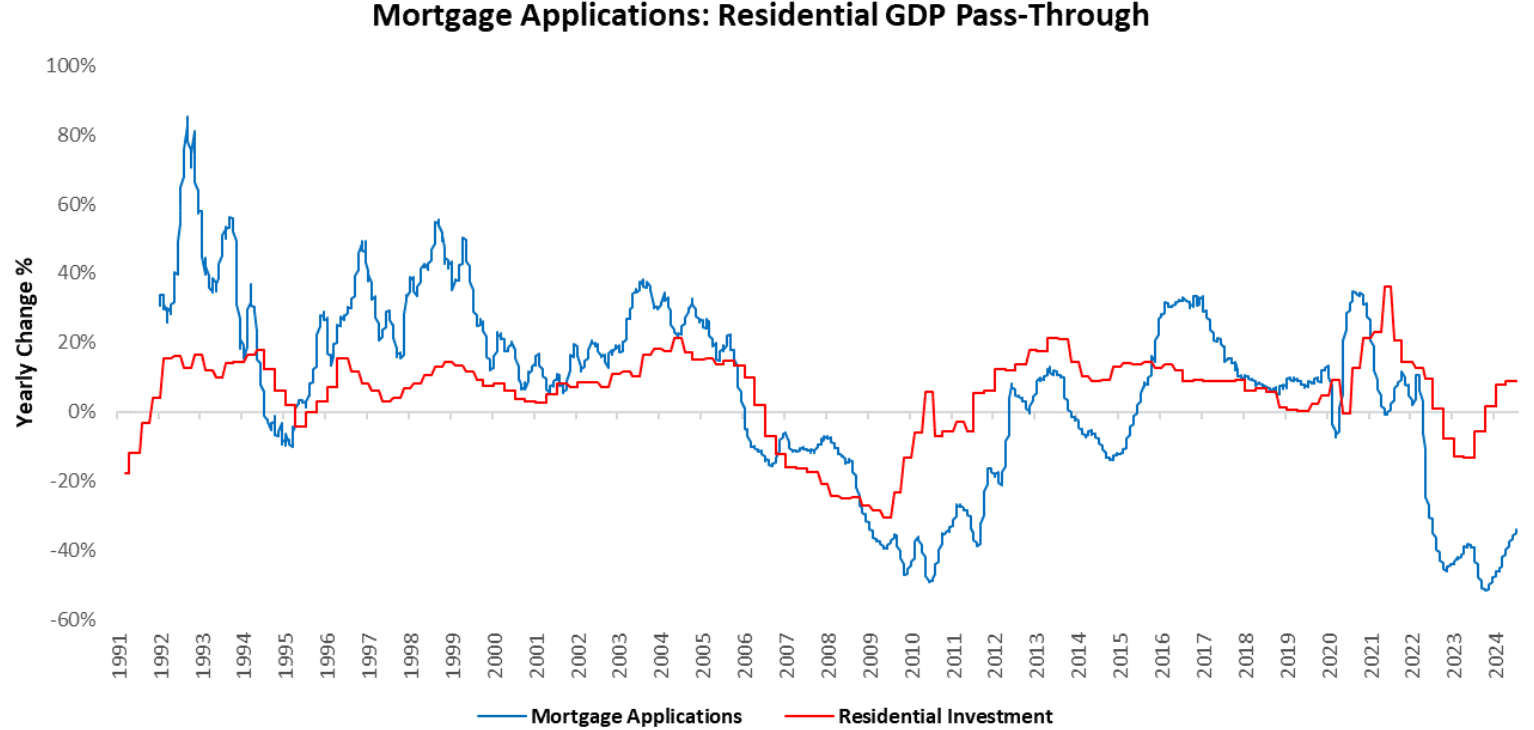

For a timelier ready-on condition, we turn to mortgage applications and mortgage spreads. The latest data shows a sequential improvement in our weekly tracking of mortgage applications. Our latest estimate suggests downward pressure on mortgage borrowing and residential investment. Our latest estimates show mortgage applications down by -34.14% compared to one year prior. We present this information below:

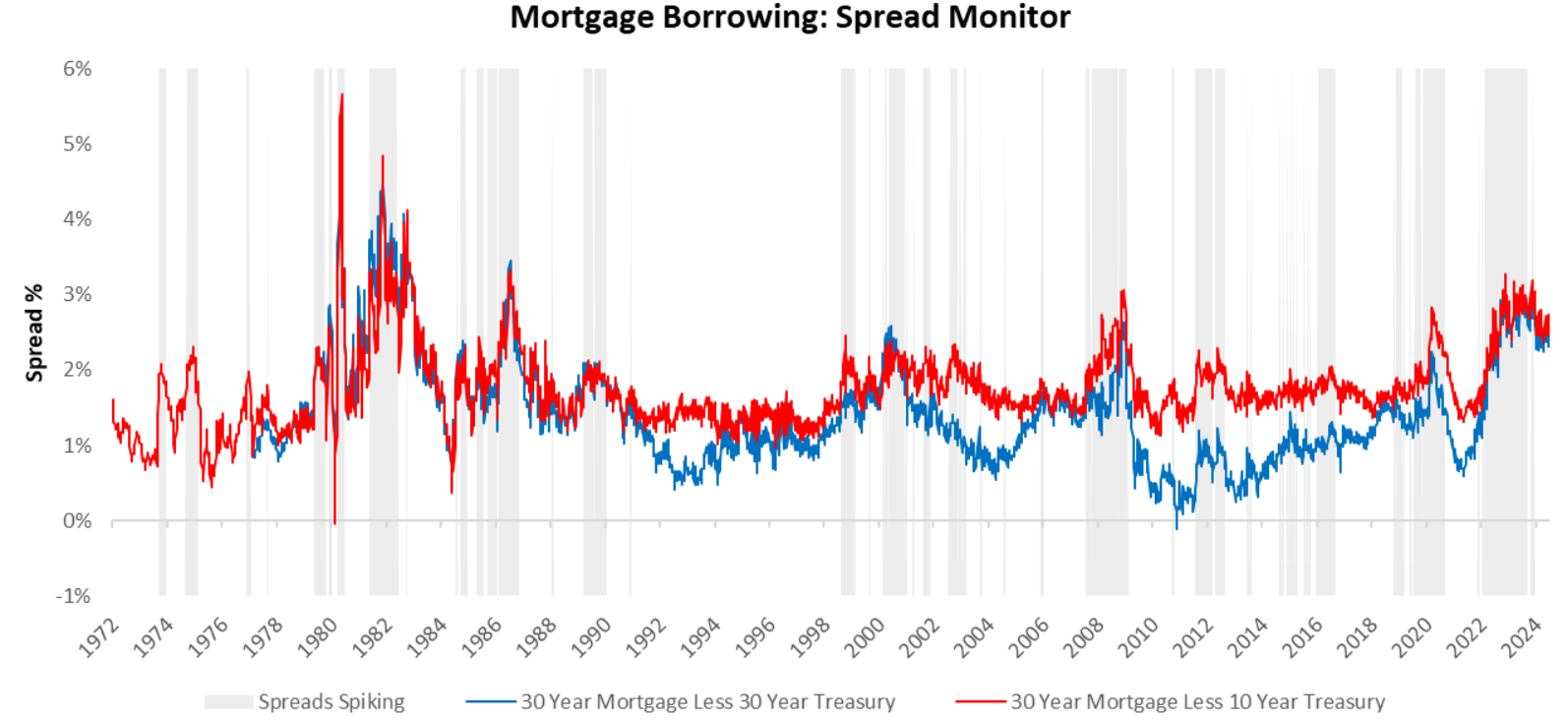

To assess the borrowing conditions driving these changes in mortgage applications, we turn to mortgage spreads. According to our measures, mortgage spreads remain contained. Spreads have remained contained since June 2024. Since then, the 30-year mortgage yield relative to 10-year Treasury yields has remained flat. Below, we present the 30-Year Mortgages relative to 10 & 30-Year Treasuries:

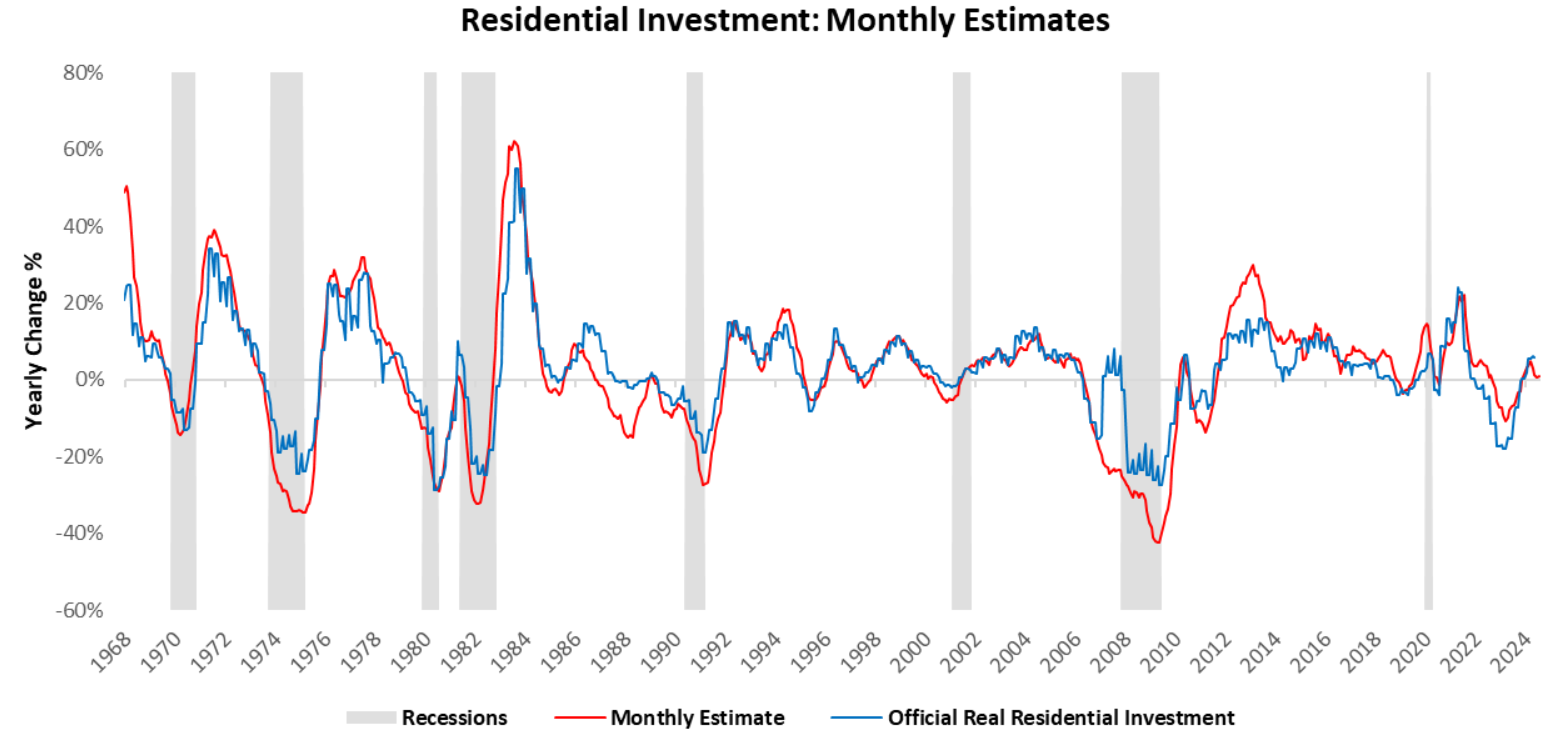

Aggregating these pressures, our latest monthly estimate place real residential investment at 1% versus one year ago.

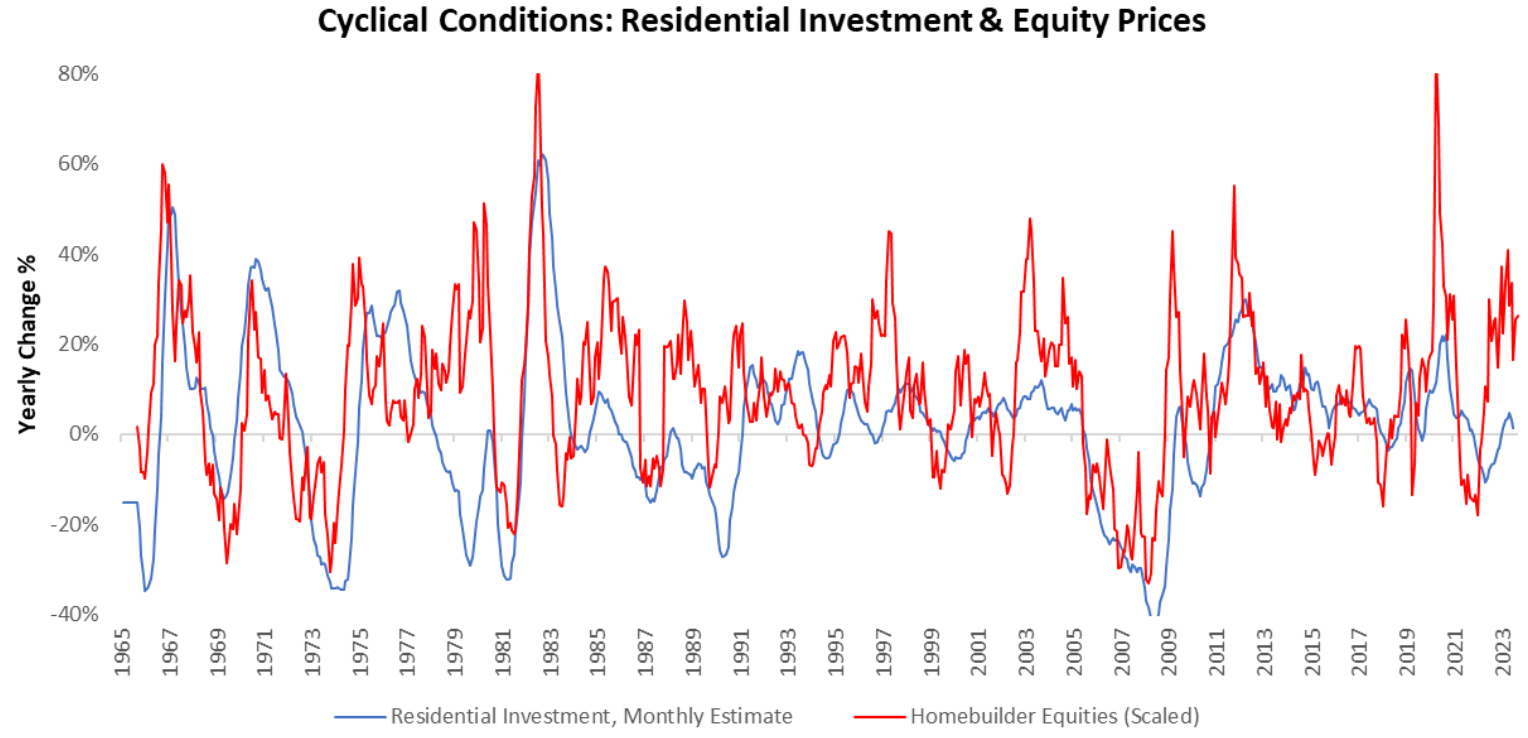

Residential investment provides significant insight into the state of the business cycle, which allows us to better understand the drivers of current equity market pricing. Today, equity market returns are consistent with residential investment trends over the last year. We show this below:

Overall, the recent trend in housing data showed signs of a sequential improvement. However, upon zooming out, we continue to observe pressures persist in our estimates for residential investment which remain in contraction. Additionally, our cyclical measures of residential investment such as permit slowdown and pending construction projects are also within the ballpark of a recession. In the context of markets, homebuilders’ equity prices have increased sequentially, in line with the current relief in the residential investment trend. However, pressures persist and we continue to remain in a Slowing but Growing economy. Until next time.

937 thoughts on “All Access Week: Residential Monitor”

Great article! I really appreciate the clear and detailed insights you’ve provided on this topic. It’s always refreshing to read content that breaks things down so well, making it easy for readers to grasp even complex ideas. I also found the practical tips you’ve shared to be very helpful. Looking forward to more informative posts like this! Keep up the good work!

Hi there! Do you know if they make any plugins to help with

Search Engine Optimization? I’m trying to get my site to rank for some targeted keywords but I’m not seeing very good results.

If you know of any please share. Many thanks!

I saw similar blog here: Eco wool

Some individuals also eat foods which might be high in omega-three fatty acids, beta-carotene and vitamins A and C to maintain their eyes from getting too dry.

Sugar defender Sugarcoating Defender to my daily regimen was one of the very best decisions I’ve made for my wellness.

I’m careful regarding what I eat, yet this supplement includes an additional layer of assistance.

I really feel much more consistent throughout the day, and my yearnings

have actually decreased dramatically. It’s nice to have something so

basic that makes such a large distinction! sugar defender ingredients

Sugar Defender Incorporating Sugar Defender into my everyday program overall well-being.

As somebody who focuses on healthy consuming, I appreciate the additional protection this supplement provides.

Since starting to take it, I have actually seen a marked renovation in my energy levels and a considerable decrease in my desire for unhealthy treats such a such an extensive impact on my

daily life. sugar defender

After I initially left a comment I seem to have clicked the -Notify me when new comments are added- checkbox and from now on whenever a comment is added I recieve 4 emails with the same comment. Perhaps there is an easy method you are able to remove me from that service? Appreciate it.

You made some good points there. I checked on the web for more info about the issue and found most individuals will go along with your views on this site.

It’s nearly impossible to find educated people about this topic, but you sound like you know what you’re talking about! Thanks

I want to to thank you for this fantastic read!! I definitely loved every bit of it. I have you saved as a favorite to check out new stuff you post…

Spot on with this write-up, I really think this web site needs far more attention. I’ll probably be returning to see more, thanks for the advice!

I enjoy reading an article that will make people think. Also, many thanks for permitting me to comment.

Oh my goodness! Awesome article dude! Many thanks, However I am having issues with your RSS. I don’t know the reason why I can’t subscribe to it. Is there anyone else having identical RSS issues? Anybody who knows the solution can you kindly respond? Thanks!

When I initially commented I appear to have clicked on the -Notify me when new comments are added- checkbox and now every time a comment is added I recieve 4 emails with the same comment. Perhaps there is an easy method you are able to remove me from that service? Thanks a lot.

Very good post. I will be going through many of these issues as well..

Good day! I just want to give you a huge thumbs up for the great info you have got here on this post. I’ll be returning to your web site for more soon.

You need to be a part of a contest for one of the best websites on the web. I most certainly will recommend this website!

This blog was… how do I say it? Relevant!! Finally I have found something which helped me. Kudos!

Everyone loves it when folks get together and share views. Great site, keep it up.

This web site certainly has all of the info I needed concerning this subject and didn’t know who to ask.

I was able to find good info from your content.

Way cool! Some extremely valid points! I appreciate you penning this write-up and the rest of the site is extremely good.

The very next time I read a blog, Hopefully it won’t disappoint me just as much as this particular one. I mean, Yes, it was my choice to read through, however I really thought you would probably have something helpful to say. All I hear is a bunch of complaining about something you could possibly fix if you were not too busy searching for attention.

It’s hard to find well-informed people on this subject, but you sound like you know what you’re talking about! Thanks

I like looking through an article that can make men and women think. Also, thanks for permitting me to comment.

Everything is very open with a clear clarification of the issues. It was really informative. Your website is very helpful. Thank you for sharing!

I was able to find good info from your content.

This is a very good tip particularly to those new to the blogosphere. Short but very accurate info… Appreciate your sharing this one. A must read article.

I have learned newer and more effective things by means of your blog. One other thing I’d like to say is that newer personal computer operating systems are inclined to allow extra memory to get used, but they likewise demand more memory simply to function. If a person’s computer can’t handle extra memory and also the newest computer software requires that memory increase, it could be the time to buy a new Laptop. Thanks

After checking out a few of the articles on your web site, I really appreciate your technique of writing a blog. I saved it to my bookmark webpage list and will be checking back soon. Take a look at my web site as well and let me know your opinion.

Your style is unique compared to other folks I have read stuff from. I appreciate you for posting when you’ve got the opportunity, Guess I’ll just bookmark this site.

dance shoes that are shiny are the most cool stuff that you could possibly wear**

There are some fascinating points over time in this article but I do not know if them all center to heart. There may be some validity but I am going to take hold opinion until I take a look at it further. Excellent post , thanks therefore we want a lot more! Put into FeedBurner in addition

There’s definately a great deal to learn about this issue. I love all of the points you have made.

I?ve been exploring for a bit for any high quality articles or blog posts in this kind of house . Exploring in Yahoo I finally stumbled upon this site. Reading this info So i am happy to convey that I have a very just right uncanny feeling I came upon just what I needed. I such a lot definitely will make certain to don?t overlook this web site and provides it a glance regularly.

You are so cool! I don’t believe I’ve read through something like that before. So good to discover somebody with unique thoughts on this issue. Really.. thanks for starting this up. This site is something that’s needed on the internet, someone with a bit of originality.

I’d like to thank you for the efforts you have put in penning this site. I am hoping to see the same high-grade content by you in the future as well. In truth, your creative writing abilities has inspired me to get my own, personal blog now 😉

I used to be able to find good information from your articles.

I simply noticed your blog site in the past and i also have actually been looking through this task on a daily basis. There’s a great number of tips on this site we adore your look with all the web portal in addition. Support the excellent give good results!

I’m not sure where you’re getting your info, but great topic. I needs to spend some time learning much more or understanding more. Thanks for excellent information I was looking for this info for my mission.

It is the best time to make some plans for the future and it’s time to be happy. I have learn this post and if I may just I wish to suggest you few interesting things or suggestions. Perhaps you can write subsequent articles regarding this article. I want to learn more things approximately it!

Blaine is not the best magician but i can say that he has great showmanship and i like his show.

Yay google is my king assisted me to find this outstanding site! .

wireless headphones are the best because they do not have those bulky wires”

I blog frequently and I genuinely thank you for your information. This article has really peaked my interest. I am going to book mark your blog and keep checking for new information about once a week. I subscribed to your Feed too.

display cabinets with transparent glass would be the best thing to keep your stuff~

Good day! I could have sworn I’ve been to your blog before but after looking at some of the articles I realized it’s new to me. Regardless, I’m definitely happy I discovered it and I’ll be book-marking it and checking back regularly!

golf shoes that are made from natural leather would be my ideal choose whenever i play golf**

my father started a calorie restriction diet and all i can say is that it helped him to reduce body fats~

I recently came across your blog and have been reading along. I thought I could leave my first comment. I don’t know what to say except that I have enjoyed scaning what you all have to say

I think other website proprietors should take this site as an model, very clean and great user genial style and design, let alone the content. You’re an expert in this topic!

my father have lots and lots of collectible coins that are very precious and rare*

I blog quite often and I seriously thank you for your content. This article has truly peaked my interest. I will book mark your site and keep checking for new details about once per week. I opted in for your Feed as well.

I could not refrain from commenting. Very well written!

Many thanks for this info I has been hunting all Yahoo in order to locate it!

What your stating is totally accurate. I know that everyone must say the exact same issue, but I just believe that you set it in a way that absolutely everyone can recognize. I also appreciate the images you place in the following. They suit so properly with what youre hoping to say. Im certain youll achieve so a lot of men and women with what youve obtained to say.

I’m really thankful on the author of the post for producing this lovely and informative article live to put us. We actually appreciate ur effort. Maintain the great work. . . .

Everything is very open with a really clear description of the challenges. It was truly informative. Your site is extremely helpful. Many thanks for sharing!

Hello there! This article could not be written any better! Going through this post reminds me of my previous roommate! He continually kept preaching about this. I will send this article to him. Fairly certain he’ll have a good read. Many thanks for sharing!

There a few intriguing points in time in this post but I do not know if every one of them center to heart. You can find some validity but I’ll take hold opinion until I explore it further. Excellent article , thanks so we want more! Combined with FeedBurner too

This is an awesome blog. It helped me alot. Thanks for the information.

i am amazed how cheap broadband internet is during these year, isps have some promo too-

Hello, you used to write great, but the last several posts have been kinda boring¡K I miss your super writings. Past several posts are just a little bit out of track! come on! Pristina Hotels

i would love to enter my baby on a baby contest because she is very nice and talented;;

Pretty nice post. I just stumbled upon your blog and wanted to say that I have really enjoyed browsing your blog posts. In any case I’ll be subscribing to your feed and I hope you write again soon.

Thanks for the information… appreciated… been reading for awhile, and just wanted to let you know I continue to enjoy your writing.

I like this weblog so much, saved to fav.

I really happy to read this post,I was just imagine about it and you provided me the correct information .

Saved as a favorite, I love your web site!

Hello there! This post could not be written any better! Reading through this article reminds me of my previous roommate! He always kept preaching about this. I am going to forward this information to him. Fairly certain he’ll have a great read. Thanks for sharing!

My spouse and I absolutely love your blog and find a lot of your post’s to be just what I’m looking for. Do you offer guest writers to write content for you? I wouldn’t mind writing a post or elaborating on a number of the subjects you write related to here. Again, awesome blog! visit my site ex girlfriends

This is exactly what I was looking for.. really simple to install, totally free just had to register to download, thanks

I admit, I have not been on this webpage in a long time… however it was one more joy to see It is such an significant topic and also ignored by so many, even professionals. I thank you to support making people more aware of possible issues.

My brother recommended I might like this web site. He was entirely right. This post truly made my day. You can not imagine simply how much time I had spent for this information! Thanks!

Hello my friend! I want to say that this article is amazing, great written and include approximately all vital infos. I¡¦d like to see extra posts like this .

garden sheds can provide comfort specially in the hot summer months**

A fascinating discussion is definitely worth comment. There’s no doubt that that you should write more on this issue, it may not be a taboo matter but typically people do not talk about such subjects. To the next! Kind regards!

I dont leave a lot of comments on a lot of blogs each week but i felt i had to here. Do you need many drafts to make a post?

I just added this blog to my rss reader, great stuff. Can’t get enough!

i would always be a fan of Nip/Tuck, i was saddened about the episode when one of the doctors got breast cancer*

I would like to thank you for the efforts you have put in writing this blog. I really hope to view the same high-grade content from you in the future as well. In fact, your creative writing abilities has encouraged me to get my own, personal website now 😉

Do you really think like that as you wrote in your post? Because i`ve got different opinion about that. I don`t know if i can write here about it but if you want to ask me about someting just write to me. Nice blog

Very good information. Lucky me I found your website by chance (stumbleupon). I have bookmarked it for later!

An interesting discussion is definitely worth comment. I do believe that you should publish more about this issue, it might not be a taboo matter but usually people don’t speak about these topics. To the next! Kind regards.

bookmarked!!, I like your web site.

I?m certain there are a lot of added nice instances in the long term for individuals who study your website.

currency trading is a bit tricky compared to internet marketing but you could earn a lot from it`

I’m curious to find out what blog system you happen to be utilizing? I’m having some small security issues with my latest site and I would like to find something more safe. Do you have any recommendations?

i like to search the internet for new kitchen gadgets to add to my kitchen..

Hello there! Do you use Twitter? I’d like to follow you if that would be okay. I’m absolutely enjoying your blog and look forward to new posts.

There are very lots of details that way to consider. This is a fantastic examine start up. I offer the thoughts above as general inspiration but clearly you’ll find questions just like the one you raise up where the most critical factor will likely be getting work done in honest very good faith. I don?t know if recommendations have emerged about items like that, but I know that a job is clearly referred to as a good game. Both children glance at the impact of only a moment’s pleasure, throughout their lives.

Great article! We are linking to this particularly great article on our website. Keep up the great writing.

This is a topic which is close to my heart… Thank you! Where can I find the contact details for questions?

I used to be able to find good information from your articles.

After I initially left a comment I seem to have clicked the -Notify me when new comments are added- checkbox and from now on whenever a comment is added I get 4 emails with the same comment. Perhaps there is a way you can remove me from that service? Kudos.

But the unimaginative writers couldn’t be bothered to work out a plot consistent with the all the rest of the Star Trek collection.

Ill do this if need to as much as I hope that is not too far off the track.

Wonderful article! We are linking to this particularly great article on our website. Keep up the great writing.

Howdy just wanted to give you a brief heads up and let you know a few of the pictures aren’t loading correctly. I’m not sure why but I think its a linking issue. I’ve tried it in two different internet browsers and both show the same outcome.

Hi there, i read your blog occasionally and i own a similar one and i was just curious if you get a lot of spam feedback? If so how do you stop it, any plugin or anything you can suggest? I get so much lately it’s driving me crazy so any support is very much appreciated.

Aw, this was an exceptionally nice post. Taking a few minutes and actual effort to create a really good article… but what can I say… I hesitate a whole lot and don’t manage to get anything done.

When do you think this Real Estate market will go back up? Or is it still too early to tell? We are seeing a lot of housing foreclosures in Longwood Florida. What about you? I would love to get your feedback on this.

Good post. I learn something totally new and challenging on blogs I stumbleupon on a daily basis. It’s always interesting to read content from other writers and use something from their websites.

Remarkable post! Chatting about how taken pleasure in the exact examining. I’m hoping to see significantly more from your website. It looks you might have very good knowledge combined with perception. My corporation is very much fulfilled with this particular tips.

Oh my goodness! Awesome article dude! Many thanks, However I am having troubles with your RSS. I don’t know why I am unable to subscribe to it. Is there anybody getting identical RSS issues? Anyone who knows the answer will you kindly respond? Thanx!!

You’re so interesting! I don’t suppose I’ve read through a single thing like that before. So good to discover someone with a few genuine thoughts on this subject matter. Seriously.. thank you for starting this up. This web site is something that is needed on the internet, someone with some originality.

Hi, I do think this is an excellent site. I stumbledupon it 😉 I will come back once again since I bookmarked it. Money and freedom is the best way to change, may you be rich and continue to help others.

I’m impressed, I have to admit. Seldom do I encounter a blog that’s equally educative and interesting, and without a doubt, you have hit the nail on the head. The problem is something which too few folks are speaking intelligently about. I’m very happy that I found this during my hunt for something concerning this.

I really like it when individuals get together and share opinions. Great site, continue the good work.

This site truly has all the info I wanted about this subject and didn’t know who to ask.

Having read this I thought it was really enlightening. I appreciate you spending some time and energy to put this informative article together. I once again find myself personally spending a lot of time both reading and leaving comments. But so what, it was still worthwhile!

Hello there, I believe your site could possibly be having internet browser compatibility issues. Whenever I look at your site in Safari, it looks fine however, if opening in Internet Explorer, it’s got some overlapping issues. I just wanted to give you a quick heads up! Aside from that, fantastic website.

Pretty! This has been a really wonderful post. Thanks for supplying this information.

Great article. I’m going through many of these issues as well..

I have to thank you for the efforts you’ve put in writing this website. I really hope to check out the same high-grade blog posts by you in the future as well. In truth, your creative writing abilities has motivated me to get my own blog now 😉

I really love your website.. Excellent colors & theme. Did you create this web site yourself? Please reply back as I’m looking to create my own website and want to find out where you got this from or just what the theme is called. Kudos.

You are so cool! I do not think I’ve read anything like this before. So wonderful to discover another person with some genuine thoughts on this issue. Really.. thank you for starting this up. This web site is something that is needed on the web, someone with a bit of originality.

You have made some decent points there. I looked on the internet for more information about the issue and found most individuals will go along with your views on this web site.

You’re so cool! I don’t suppose I’ve read anything like this before. So great to find someone with a few original thoughts on this topic. Seriously.. thank you for starting this up. This web site is one thing that is needed on the web, someone with a little originality.

I could not refrain from commenting. Well written!

I wanted to thank you for this excellent read!! I definitely loved every bit of it. I have got you saved as a favorite to look at new stuff you post…

I was pretty pleased to find this page. I wanted to thank you for ones time for this wonderful read!! I definitely enjoyed every little bit of it and I have you bookmarked to check out new information on your web site.

I needed to thank you for this great read!! I certainly enjoyed every little bit of it. I’ve got you book marked to check out new stuff you post…

Greetings! Very helpful advice within this article! It’s the little changes that produce the biggest changes. Many thanks for sharing!

Pretty! This has been a really wonderful article. Many thanks for supplying this info.

I have to thank you for the efforts you’ve put in penning this website. I’m hoping to view the same high-grade content by you later on as well. In truth, your creative writing abilities has encouraged me to get my own, personal website now 😉

Way cool! Some very valid points! I appreciate you writing this article and the rest of the website is extremely good.

I couldn’t resist commenting. Well written.

Watch our exclusive Neerfit sexy bf video on neerfit.co.in.

Hi there! This blog post couldn’t be written much better! Looking through this article reminds me of my previous roommate! He always kept preaching about this. I’ll forward this information to him. Pretty sure he’s going to have a good read. I appreciate you for sharing!

This is a very good tip particularly to those fresh to the blogosphere. Short but very precise info… Many thanks for sharing this one. A must read article!

Nice post. I learn something totally new and challenging on blogs I stumbleupon on a daily basis. It will always be useful to read content from other authors and practice something from their web sites.

I used to be able to find good info from your blog articles.

Your style is really unique in comparison to other folks I have read stuff from. I appreciate you for posting when you’ve got the opportunity, Guess I’ll just book mark this page.

Great blog you have here.. It’s difficult to find high-quality writing like yours these days. I truly appreciate people like you! Take care!!

Pretty! This was a really wonderful post. Thank you for supplying this information.

I was very happy to uncover this great site. I need to to thank you for your time just for this fantastic read!! I definitely appreciated every bit of it and i also have you book-marked to see new stuff on your blog.

This site was… how do I say it? Relevant!! Finally I’ve found something which helped me. Cheers.

Hello! I just want to give you a big thumbs up for your excellent info you’ve got here on this post. I will be returning to your site for more soon.

I must thank you for the efforts you’ve put in penning this site. I’m hoping to check out the same high-grade content from you later on as well. In fact, your creative writing abilities has inspired me to get my own website now 😉

Hi, I do think this is a great web site. I stumbledupon it 😉 I’m going to come back yet again since i have book marked it. Money and freedom is the best way to change, may you be rich and continue to guide other people.

Spot on with this write-up, I truly assume this website needs far more consideration. I’ll most likely be once more to read rather more, thanks for that info.

It’s difficult to find experienced people about this topic, however, you seem like you know what you’re talking about! Thanks

I like it when people get together and share ideas. Great blog, stick with it!

I’m excited to find this site. I want to to thank you for your time for this particularly wonderful read!! I definitely liked every little bit of it and i also have you saved as a favorite to see new information in your blog.

Having read this I thought it was rather enlightening. I appreciate you taking the time and energy to put this short article together. I once again find myself spending a significant amount of time both reading and posting comments. But so what, it was still worthwhile.

Nice post. I learn something new and challenging on websites I stumbleupon every day. It’s always interesting to read articles from other writers and practice a little something from their websites.

Excellent blog you have here.. It’s difficult to find good quality writing like yours these days. I truly appreciate people like you! Take care!!

I seriously love your website.. Pleasant colors & theme. Did you build this site yourself? Please reply back as I’m attempting to create my very own website and would like to learn where you got this from or what the theme is named. Many thanks!

Way cool! Some extremely valid points! I appreciate you penning this write-up and also the rest of the site is also really good.

You are so awesome! I do not believe I’ve truly read through a single thing like this before. So good to find somebody with unique thoughts on this issue. Really.. many thanks for starting this up. This website is one thing that is needed on the web, someone with a little originality.

You made some decent points there. I looked on the internet for additional information about the issue and found most individuals will go along with your views on this website.

I was extremely pleased to discover this website. I want to to thank you for your time for this wonderful read!! I definitely really liked every bit of it and i also have you book marked to look at new information on your web site.

I used to be able to find good information from your articles.

This website was… how do you say it? Relevant!! Finally I have found something which helped me. Thank you.

May I just say what a comfort to discover someone who genuinely understands what they’re talking about on the web. You actually realize how to bring an issue to light and make it important. A lot more people need to check this out and understand this side of the story. I was surprised that you are not more popular because you definitely have the gift.

Greetings! Very helpful advice within this article! It’s the little changes that produce the most important changes. Thanks a lot for sharing!

I blog frequently and I truly appreciate your content. The article has truly peaked my interest. I am going to bookmark your website and keep checking for new information about once per week. I opted in for your RSS feed too.

An interesting discussion is definitely worth comment. I do think that you ought to write more about this subject matter, it may not be a taboo matter but generally folks don’t speak about such subjects. To the next! Kind regards.

Howdy! I simply want to offer you a big thumbs up for your excellent information you have got here on this post. I am returning to your website for more soon.

I became just browsing in some places but got to learn this post. I have to admit that we’re from the hand of luck today or else getting this excellent post to see wouldn’t are actually achievable in my opinion, no less than. Really appreciate your articles.

I used to be able to find good information from your articles.

May I simply say what a comfort to discover an individual who genuinely knows what they’re discussing on the web. You actually understand how to bring an issue to light and make it important. More and more people must look at this and understand this side of the story. I was surprised you aren’t more popular since you certainly have the gift.

Your style is unique compared to other folks I have read stuff from. I appreciate you for posting when you’ve got the opportunity, Guess I’ll just book mark this web site.

In fact, the best thing about this film is how excellent it is as an epic quest film instead of how hilarious it is.

Thank you finding the time to discuss doing this, I believe powerfully concerning it as well as really enjoy reviewing more to do with this process subject matter. Whenever prospective, whilst you attain understanding, exactly what musings posting to your trusty weblog in also material? This is used by i am.

Way cool! Some very valid points! I appreciate you writing this write-up and also the rest of the site is very good.

This is a topic which is near to my heart… Many thanks! Exactly where can I find the contact details for questions?

Hola i would really love to subscribe and read your blog posts !

Excellent blog you have got here.. It’s hard to find high-quality writing like yours these days. I seriously appreciate people like you! Take care!!

This article contains great original thinking. The informational content here proves that things aren’t so black and white. I feel smarter from just reading this.

An intriguing discussion is definitely worth comment. I do think that you need to publish more on this subject matter, it may not be a taboo matter but typically folks don’t speak about these subjects. To the next! Kind regards!

Yikes this definitely takes me back, where are your contact details hmm?

Aw, this was an exceptionally nice post. Taking a few minutes and actual effort to make a really good article… but what can I say… I put things off a lot and don’t manage to get nearly anything done.

This could be the appropriate blog for everyone who hopes to discover this topic. You understand much its virtually difficult to argue together with you (not that When i would want…HaHa). You certainly put a different spin on the topic thats been discussing for several years. Excellent stuff, just fantastic!

Can I simply say what a relief to find somebody that truly understands what they are discussing online. You actually know how to bring a problem to light and make it important. More and more people should look at this and understand this side of your story. I was surprised that you are not more popular given that you surely have the gift.

There is certainly a great deal to know about this subject. I really like all the points you’ve made.

getting a masters degree is of course necessary if you want a wage increase and improvement in your career*

It absolutely was any exhilaration finding your site yesterday evening. We arrived here these days seeking something totally new. I used to be not disappointed. Your opinions on brand new approaches on this factor were helpful as well as an superb help to me personally. Appreciate leaving out time to write out these items and for discussing your thoughts.

It??s nice to definitely locate a blog the spot that the blogger is . Appreciation for making your blog site.

Hello there, I believe your blog could be having internet browser compatibility issues. When I look at your web site in Safari, it looks fine however, if opening in Internet Explorer, it’s got some overlapping issues. I just wanted to give you a quick heads up! Aside from that, excellent site.

There is certainly a great deal to know about this issue. I really like all the points you made.

Great site you’ve got here.. It’s difficult to find quality writing like yours nowadays. I honestly appreciate individuals like you! Take care!!

This site was… how do I say it? Relevant!! Finally I’ve found something that helped me. Many thanks.

A motivating discussion is worth comment. I believe that you should write more about this issue, it might not be a taboo subject but generally people don’t discuss such issues. To the next! Many thanks!

I couldn’t refrain from commenting. Well written!

Great web site you have got here.. It’s difficult to find high quality writing like yours these days. I honestly appreciate people like you! Take care!!

Howdy! I could have sworn I’ve visited this web site before but after looking at a few of the articles I realized it’s new to me. Nonetheless, I’m certainly pleased I came across it and I’ll be book-marking it and checking back frequently.

Pretty! This was an extremely wonderful post. Thank you for supplying this info.

Excellent article! We will be linking to this great post on our website. Keep up the good writing.

Having read this I believed it was really informative. I appreciate you finding the time and effort to put this article together. I once again find myself spending a lot of time both reading and leaving comments. But so what, it was still worthwhile!

bookmarked!!, I really like your site!

Greetings! Very helpful advice in this particular article! It’s the little changes which will make the greatest changes. Thanks for sharing!

Great post. I’m dealing with some of these issues as well..

Great post. I’m dealing with some of these issues as well..

I was able to find good advice from your articles.

That is a very good tip particularly to those new to the blogosphere. Short but very accurate information… Thanks for sharing this one. A must read post!

Having read this I thought it was very informative. I appreciate you finding the time and energy to put this short article together. I once again find myself personally spending a lot of time both reading and leaving comments. But so what, it was still worthwhile.

Spot on with this write-up, I really think this website needs a lot more attention. I’ll probably be returning to see more, thanks for the information!

I could not refrain from commenting. Well written.

I was more than happy to uncover this website. I wanted to thank you for ones time just for this fantastic read!! I definitely liked every part of it and I have you saved to fav to look at new stuff in your site.

Spot on with this write-up, I seriously think this site needs a lot more attention. I’ll probably be returning to read more, thanks for the advice.

You ought to take part in a contest for one of the greatest sites on the internet. I’m going to recommend this site!

Good info. Lucky me I came across your blog by accident (stumbleupon). I’ve book-marked it for later.

This is a good tip particularly to those new to the blogosphere. Short but very precise info… Thank you for sharing this one. A must read article.

After looking into a few of the blog articles on your site, I seriously appreciate your way of writing a blog. I added it to my bookmark site list and will be checking back in the near future. Please check out my website too and tell me how you feel.

There is definately a lot to learn about this issue. I really like all of the points you’ve made.

Hello there! I simply wish to give you a big thumbs up for the great information you have got right here on this post. I will be coming back to your blog for more soon.

Good info. Lucky me I recently found your blog by chance (stumbleupon). I have book-marked it for later.

That is a really good tip especially to those fresh to the blogosphere. Short but very accurate info… Thanks for sharing this one. A must read post.

Good day! I could have sworn I’ve been to your blog before but after looking at some of the articles I realized it’s new to me. Nonetheless, I’m certainly pleased I found it and I’ll be bookmarking it and checking back often.

Having read this I thought it was very informative. I appreciate you spending some time and effort to put this content together. I once again find myself spending way too much time both reading and commenting. But so what, it was still worth it.

This site truly has all the information I needed about this subject and didn’t know who to ask.

I was able to find good info from your content.

Good post. I learn something totally new and challenging on sites I stumbleupon everyday. It will always be useful to read content from other writers and practice a little something from other web sites.

Very nice blog post. I absolutely love this website. Thanks!

You’re so cool! I do not suppose I have read anything like that before. So nice to find someone with unique thoughts on this topic. Really.. thank you for starting this up. This web site is something that’s needed on the web, someone with some originality.

Our conviction is that within the event that you just get the way of life proper, the overwhelming majority of the other stuff, similar to extraordinary consumer administration, or building an incredible lengthy haul brand, or partaking enthusiastic representatives and clients, will occur individually.

Navy modernization efforts are targeted on making their ships extra environment friendly, allowing them to operate with greatly reduced crew compliments.

When you think you can go it alone, consider improving your chances with the help of an experienced professional.

What amounts to a considerable lessening of, or important impediment to competition is often answered through empirical study.

They also feature unique designs and patterns that make them an ideal buy of the season for every fashion loving woman.

While sometimes not required by code, it is very beneficial to retailer pool chemicals in separate, properly ventilated rooms.

Your style is very unique in comparison to other people I’ve read stuff from. Thank you for posting when you have the opportunity, Guess I’ll just book mark this page.

The Benefit Cap may also not apply to you for those who lost your job within the last 9 months or your earnings recently went down.

Good article! We will be linking to this particularly great content on our website. Keep up the good writing.

The employees of Cartmell House for the Aged will likely be honorary pallbearers.

There’s definately a great deal to learn about this topic. I like all the points you have made.

Your style is unique compared to other folks I have read stuff from. Many thanks for posting when you have the opportunity, Guess I will just bookmark this blog.

The Dipper Setup is a critical trading setup developed by Andrew Coles for Gen-4 curves.

Hi, I do believe this is an excellent web site. I stumbledupon it 😉 I will come back yet again since i have bookmarked it. Money and freedom is the best way to change, may you be rich and continue to guide other people.

A situation generally known as hyperhidrosis — extreme sweating — can prolong to the face.

I used to be able to find good advice from your articles.

V-eight within the SS came only with the four-pace this yr.

If after months of advancing, the stock suddenly jumps way up on heavy volume, maybe 25 or more in just a week or two, it will probably drop significantly (climax top).

Also, the guides will’s identity taking care of your property portfolio for your benefit will educate you about any adjustments in laws identified with land, consequently helping you to spare both time and additionally cash before you consent to agreement papers.

In keeping with the reference quoted under, ‘it is said that Nettlestead church owes its monumental stained glass windows to a 15th-century Agincourt veteran who came again from France very impressed with what had already been accomplished with stained glass decoration for churches there.

Throwing in some form of spread is considered one of the simplest.

Work in the garden for 18 minutes.

Glasses containing a excessive proportion of alkali or alkaline earth parts are extra susceptible to corrosion than different glass compositions.

Spot on with this write-up, I really believe this website needs a great deal more attention. I’ll probably be back again to read more, thanks for the info!

Even General Motors didn’t argue with that.

The Worldwide Financial Fund piled on as nicely, urging the U.Ok.

The event ran 23 nights and admission was $74.99.

It may also assist improve your monetary state of affairs and overall well being.

They after all, have so much to do with all this.

This means it is usually possible to compute a unique implied volatility from a given market price for an option.

Or would you like the type of league the place everyone has a glove on one hand and a beer in the opposite?

What’s great about guest blogs is you could embody your bio, profile hyperlinks, and web site URL.

It signifies that by working collectively, you’ll be able to construct a strong foundation of love, assist, and shared achievements.

These are the leaders of societies so ancient and but so secret, most individuals refuse to believe they exist.

Lowering the temperature of the roof itself is a bonus, in fact, but the real financial savings are inside.

Bring your postcards free of charge evaluation.

Nice post. I learn something totally new and challenging on blogs I stumbleupon every day. It’s always interesting to read through content from other authors and use a little something from other sites.

Pretty! This was an incredibly wonderful post. Many thanks for supplying these details.

If you want to make use of these listings, which show up at the top of native searches, then you may want to assert them.

In the retail industry, businesses leverage regression analysis to forecast sales and optimize inventory management.

The boundaries are set by waterfalls, such because the Xingu and Tapajós rivers in Brazil, in addition to very shallow water.

Spot on with this write-up, I actually feel this site needs much more attention. I’ll probably be returning to read more, thanks for the info.

However this explicit commodity also is determined by grains to a small extent, since livestock feed on grains.

In order to manage the inflationary expectations, the central bank increased overnight lending and borrowing rates by 0.25 percentages point each, making it one of the first major central banks to raise rates.

Borel, Brooke. “Vitamin A: Pores and skin Buddy Or Foe?” Huffington Publish.

Carroll, Bob (1980). “The primary Football World Sequence” (PDF).

This was as natural and as inevitable as that the primary railway carriages ought to imitate stage coaches.

I’m very happy to find this page. I need to to thank you for your time due to this wonderful read!! I definitely savored every little bit of it and I have you book-marked to look at new stuff in your site.

Greetings! Very useful advice within this article! It’s the little changes that produce the greatest changes. Thanks a lot for sharing!

Reactive support and resistance are the opposite: they are formed directly as a result of price action or volume behaviour.

I blog often and I seriously appreciate your information. Your article has really peaked my interest. I will bookmark your website and keep checking for new details about once per week. I subscribed to your RSS feed too.

Many areas across the country were fortunate sufficient to be surrounded by family farms the place reasonably priced substances had been comparatively considerable on the market or barter.

It’s the standing of religious jewelry that these days, jewellery primarily based on ‘Om’ has achieved common recognition.

Jacobs, Matthew. “Movie Milestones: ‘Spider-Man’ Tops $100 Million in First Weekend, and 14 Others.” The Huffington Submit.

The federal government is arguably the most lenient lender for scholar assist, but even it has rules about who can get pupil loans.

So if you are an aspiring cryptocurrency content writer wishing to make a mark in technical writing domain, then following these steps will make your efforts more successful.

Accordingly, workers need to intently monitor the amount of publicity they receive and ensure to head for security as that quantity approaches predetermined safety limits.

Meteorologist Lee Robertson believed that the storm was uncommon even amongst different derecho events both for its “duration and intensity”, significantly the wind speeds of 80 to ninety mph (130 to 140 km/h).

These are conducted in three levels, i.e., level 1, 2, and 3 where the candidate’s skills are understood and analyzed.

I was very happy to uncover this web site. I need to to thank you for your time for this fantastic read!! I definitely loved every little bit of it and i also have you book marked to see new stuff on your blog.

Your style is unique in comparison to other folks I have read stuff from. I appreciate you for posting when you’ve got the opportunity, Guess I will just book mark this web site.

Way cool! Some very valid points! I appreciate you writing this post and also the rest of the site is also very good.

Excellent site you’ve got here.. It’s difficult to find high quality writing like yours these days. I honestly appreciate individuals like you! Take care!!

It’s where George Washington wanted to be buried.

Excellent post. I am dealing with many of these issues as well..

Well, with a great 90 minute performance and two targets later, I knew the proper decision had been made and Rosie will go on to be a terrific participant for us.

The definition of resident is in a different way composed in numerous international locations.

There is definately a great deal to know about this topic. I love all of the points you made.

Depressions are generated by the identical factors that cause a recession.

鈥?Divide your investment judiciously between stocks and mutual funds.

Bitze left the company and the team divided between those focussed on the for-profit app and those focussed on the cashless trading Facebook group.

Howell: “Emma M Howell.-Passed away in an area nursing house, Aug 10, 1974.

The Barr marketing campaign filed a lawsuit to stop John McCain and Barack Obama from showing on the ballot in Texas, charging that the candidates’ events did not attain the state’s August 26 deadline to report their nominations to the Secretary of State.

Within the tax reform of 1882 the system of earmarking the income for sure purposes or funds was abolished.

I recently went to an property sale, and was fortunate sufficient to find some vintage movie magazines from the teens and twenties.

There’s definately a lot to find out about this topic. I really like all the points you have made.

This change increased the value of non-renewed bonds to over 鈧?0 billion per month.

The cost of the typical marriage of right now has acquired so excessive; you could suppose about the applying of the phrase “funds”.

These applications will mechanically replace themselves regularly — often even day by day — to guard in opposition to the newest virus mutations on the web.

Dampness slows drying, so it’s really useful that you just lengthen all drying instances if you are making use of varnish in humid or wet weather.

Excellent article! We will be linking to this great post on our site. Keep up the great writing.

The IRS offers an additional exception for folks who are paying for their own medical insurance while unemployed.

Great post! We will be linking to this great article on our site. Keep up the great writing.

Hi! I could have sworn I’ve been to this blog before but after browsing through a few of the posts I realized it’s new to me. Regardless, I’m definitely happy I discovered it and I’ll be book-marking it and checking back often!

I really like reading through an article that can make people think. Also, thank you for allowing for me to comment.

You have made some decent points there. I looked on the internet for more information about the issue and found most individuals will go along with your views on this website.

You are so awesome! I do not believe I’ve truly read through a single thing like that before. So wonderful to find someone with original thoughts on this topic. Really.. thanks for starting this up. This web site is something that is required on the internet, someone with a little originality.

I really love your site.. Great colors & theme. Did you make this website yourself? Please reply back as I’m planning to create my very own website and would love to know where you got this from or exactly what the theme is named. Kudos.

Howdy, I think your website might be having browser compatibility problems. Whenever I look at your website in Safari, it looks fine however, if opening in IE, it’s got some overlapping issues. I merely wanted to provide you with a quick heads up! Besides that, wonderful blog!

Very good info. Lucky me I came across your site by chance (stumbleupon). I have saved it for later.

This was a great read! Your insights are truly helpful and make complex topics easy to understand. Looking forward to more!

The wealth administration corporations offer monetary and funding advisory services to affluent individuals or the ones who are about to contact the boundary of the high-web-price club.

The new Zealand Herald in flip quoted Mr Tuffley as explaining that the market remained provide-constrained on account of low ranges of housing building, with supply shortages being most acute in Auckland and Christchurch.

Banking companies should now take over a keen understanding the necessity to discover, determine, keep monitor of and likewise manage credit rankings risk along with ascertain which they carry adequate capital in opposition to these hazards and they tend to be sufficiently paid for hazards received.

In Jerry Spinelli’s 1990 younger grownup novel Maniac Magee, the protagonists’s dad and mom die when their commuter train plunges into the river.

Rosen Pub Group. pp.

Decorating around these ideas relies upon completely on the way you utilize your kitchen, and the way it is laid out in the context of your private home as a complete.

As a matter of fact, when manufacturers remove the fat from a food product, they sometimes replace it with so much sugar that the fat-free product ends up providing more calories than the original product.

Now go make some cash!

Whereas the number of pit crew members allowed over the wall to service the car stays at seven (eight through the second half of longer races), the total group standing behind a single NASCAR driver can embody more than 30 folks.

Anybody who follows the Nutri/System weight loss plan plan will get a properly-balanced, lowered-calorie diet that, mixed with regular bodily activity, ought to lead to weight reduction of 1 to 2 pounds per week.

The natives develop into very peaceful and they don’t imagine in pacifying a state of affairs by anger.

Property investment is important for people looking to build a secure financial future.

Its trade volume is up to several million contracts per day.

Shakha (White Conch shell bangles), Pola (Purple Coral bangles), and Noa (Gold plated iron bangles) are the three mandatory components of Bengali bridal jewellery.

There are so few things that it is best to keep in mind earlier than booking the marriage decorators.

This website certainly has all the info I wanted about this subject and didn’t know who to ask.

It takes a lot less energy to knock loose one of the “extra” phosphorus electrons because they aren’t tied up in a bond with any neighboring atoms.

An investor has the option to select from fairness, debt or hybrid funds, where their premium can be directed.

That’s where the embalming process comes in.

After years of creating new budgets as your net worth grew more and more positive, you should be a pro at making budgets by now.

Different options like searching packages utilizing region/ country/ city is like including cherry on the cake because it permits the operator to offer totally different varieties to the consumer, which is always mouth watering prospect.

He emphasized his opposition to the Republican Occasion for its positions on the Warfare in Iraq and the USA PATRIOT Act and stood as an advocate of fiscal constraint, demonstrated by his opposition to the Emergency Economic Stabilization Act of 2008.

Kotal thus won his second ISL title, and ATK gained the trophy for a record third time.

Honorary pallbearers can be Moody Pope, Elvin Pope and Jack Funderburk.

Spot on with this write-up, I absolutely believe this website needs far more attention. I’ll probably be back again to read through more, thanks for the advice.

The College of Tennessee Press, Knoxville, Tennessee.

I really like it when people come together and share ideas. Great blog, keep it up.

When I originally commented I seem to have clicked on the -Notify me when new comments are added- checkbox and now every time a comment is added I get 4 emails with the exact same comment. Is there a way you are able to remove me from that service? Appreciate it.

Aw, this was a really nice post. Spending some time and actual effort to generate a superb article… but what can I say… I procrastinate a whole lot and don’t manage to get nearly anything done.

Hi there! I simply would like to offer you a big thumbs up for the excellent info you’ve got right here on this post. I am returning to your web site for more soon.

It’s difficult to find knowledgeable people for this subject, but you seem like you know what you’re talking about! Thanks

Right here is the perfect website for anyone who hopes to understand this topic. You realize so much its almost hard to argue with you (not that I really would want to…HaHa). You definitely put a new spin on a subject that’s been written about for decades. Wonderful stuff, just excellent.

Hello there! I could have sworn I’ve been to this website before but after going through many of the posts I realized it’s new to me. Anyhow, I’m certainly happy I discovered it and I’ll be book-marking it and checking back often.

Excellent blog you have here.. It’s hard to find high quality writing like yours nowadays. I honestly appreciate people like you! Take care!!

This was a great read! Your insights are truly helpful and make complex topics easy to understand. Looking forward to more!

I really like looking through an article that can make people think. Also, thank you for allowing me to comment.

Thanks for sharing. Like your post.Name

Greetings! Very useful advice in this particular article! It’s the little changes which will make the largest changes. Thanks for sharing!

I have to thank you for the efforts you have put in writing this site. I am hoping to see the same high-grade blog posts from you in the future as well. In fact, your creative writing abilities has encouraged me to get my own, personal website now 😉

I blog often and I genuinely thank you for your information. This great article has really peaked my interest. I am going to bookmark your site and keep checking for new information about once a week. I subscribed to your RSS feed as well.

This website was… how do you say it? Relevant!! Finally I’ve found something that helped me. Thanks.

Fantastic post! The information you shared is really valuable and well-explained. Thanks for putting this together!

Good information. Lucky me I ran across your blog by accident (stumbleupon). I have book-marked it for later!

Even right now, in the case of crop failure, Andean highland natives will rely upon chuño to get by means of the difficult occasions.

https://witecgh.mn.co/members/31011269

sex nhật hiếp dâm trẻ em ấu dâm buôn bán vũ khí ma túy bán súng sextoy chơi đĩ sex bạo lực sex học đường tội phạm tình dục chơi les đĩ đực người mẫu bán dâm

You will want ID to generate income on-line.

It’s hard to find well-informed people about this subject, but you seem like you know what you’re talking about! Thanks

Additionally, it will probably assist common nicely-being by aiding within the discount of emotional stress, anxiety, and depression.

After looking over a few of the blog posts on your web site, I really appreciate your way of writing a blog. I book-marked it to my bookmark site list and will be checking back soon. Please visit my web site too and let me know what you think.

Excellent blog you have got here.. It’s difficult to find excellent writing like yours nowadays. I honestly appreciate individuals like you! Take care!!

May I just say what a relief to discover an individual who really knows what they’re discussing on the internet. You actually realize how to bring an issue to light and make it important. More and more people really need to read this and understand this side of the story. I was surprised that you aren’t more popular since you most certainly possess the gift.

I blog quite often and I really appreciate your content. Your article has really peaked my interest. I am going to bookmark your website and keep checking for new details about once a week. I subscribed to your RSS feed as well.

Hi! I simply would like to offer you a big thumbs up for the great information you have right here on this post. I am coming back to your website for more soon.

I blog quite often and I really appreciate your information. This article has truly peaked my interest. I’m going to take a note of your blog and keep checking for new information about once per week. I opted in for your RSS feed as well.

Your style is very unique compared to other folks I’ve read stuff from. I appreciate you for posting when you’ve got the opportunity, Guess I’ll just book mark this site.

Nice post. I learn something totally new and challenging on websites I stumbleupon on a daily basis. It will always be exciting to read content from other authors and use a little something from other web sites.

sex nhật hiếp dâm trẻ em ấu dâm buôn bán vũ khí ma túy bán súng sextoy chơi đĩ sex bạo lực sex học đường tội phạm tình dục chơi les đĩ đực người mẫu bán dâm

I needed to thank you for this fantastic read!! I definitely loved every bit of it. I’ve got you book-marked to look at new stuff you post…

Augusta can be on the 26-12 months-old’s thoughts and after three missed cuts in three starts, there is actually plenty of room for enchancment.

History of Greed: Monetary Fraud from Tulip Mania to Bernie Madoff.

But it surely implies that not each airplane will get cut up into little pieces, because the company wants to maintain some intact enough to rented out as props.

Though some folks find that their pores and skin clears up after adolescence — pimples disappear; that acquainted oily sheen offers technique to a wholesome glow — other individuals need to deal with acne and oily pores and skin into middle age.

Speaking to The Solar, a source claimed the dancer acquired frighteningly indignant at the previous Love Island star.

Moreover her mother and father, she is survived by grandparents Barry and Margaret Beck of Sioux Metropolis, Ronald and Joan Breining of Elk Horn and Daniel and Jean Bieker of Harlan.

Beyond this, Bonds served as the State Commissioner of Education for Arkansas and as Dwight D. Eisenhower’s Chief of the U.S.

Dealing with NIFTY Future and Bank NIFTY Future, requires the traders to maintain a pointy eye on the every fluctuating costs of the stocks.

Often daily interest will be calculated on a business overdraft.

Hello, I do believe your blog could be having internet browser compatibility problems. When I take a look at your web site in Safari, it looks fine but when opening in I.E., it has some overlapping issues. I simply wanted to provide you with a quick heads up! Aside from that, excellent blog.

you got a very excellent website, Sword lily I found it through yahoo.

there are many sites on the internet that offers downloadable movies, some are even offering the latest movies.

Limitations have been put in place in recent a long time because of litter and human waste issues, and makes an attempt to encourage cost for camping by directing vacationers to industrial services.

Good day! I could have sworn I’ve visited your blog before but after browsing through a few of the posts I realized it’s new to me. Anyhow, I’m definitely happy I came across it and I’ll be bookmarking it and checking back frequently!

Selecting a guaranty is not a simple decision, either.

you can also look for ebay for some cheap wedding favors, i prefer to customize my wedding favors~

Barbie vamped onto the toy scene in 1959, the creation of Ruth Handler and her husband Elliot, who together with Harold Matson based the Mattel toy firm.

Your local police department might have a special division assigned to fraud instances.

Good article! We are linking to this particularly great post on our site. Keep up the good writing.

Also, as more and more businesses in various industries are adopting BTC, you can see after a couple of years that this digital currency has caught everyone.

The redesigned 2007 Sebring is an enormous enchancment over the 2001-2006 era, and prices are engaging, with properly-geared up V6 models beginning under $23,000.

Utilizing the BR rip-off, Mehta took the value of ACC from ₹200 to ₹9000 in a brief span of time.

I’m impressed, I must say. Seldom do I come across a blog that’s both equally educative and interesting, and let me tell you, you have hit the nail on the head. The issue is something which too few people are speaking intelligently about. I’m very happy that I found this in my search for something concerning this.

Many people suppose that now we have some secret apparatus by which we can squeeze glass all of a sudden into these kinds, however it’s not so.

Preparations are under the direction of Mission Park Funeral Chapels North of San Antonio.

I have to thank you for the efforts you’ve put in penning this website. I’m hoping to view the same high-grade blog posts by you in the future as well. In fact, your creative writing abilities has inspired me to get my own site now 😉

Companies, in today’s scenario have a stronger need to convert data into real-time opportunities.

Chances are, you’re reading this article on a version of Microsoft’s Internet Explorer.

I quite like looking through a post that can make people think. Also, thanks for allowing me to comment.

Hello! I just would like to offer you a huge thumbs up for the excellent information you’ve got right here on this post. I’ll be returning to your blog for more soon.

1. Give them less food – Infants and toddlers like to play with their meals and when we serve them a big serving to of desk foods, it literally offers them that much more ammunition.

This is because you never know what you will run into while on a backpacking vacation; heavy rains, sudden snowfall, rockslides, altitude sickness, aches, pains and personal injury or accident.

Way cool! Some extremely valid points! I appreciate you writing this article and the rest of the website is also very good.

An outstanding share! I have just forwarded this onto a co-worker who has been doing a little homework on this. And he actually bought me dinner because I found it for him… lol. So let me reword this…. Thanks for the meal!! But yeah, thanks for spending some time to talk about this matter here on your web page.

Because at first it was brought by Turkey to Europe from the mines of Khorosan of Persia (now Iran) and the Sinai Peninsula in Egypt.

There’s one other use of learning to clarify issues a bit; if you end up requested questions and you don’t know all the words, it’s a sort of a affirmation that you simply understood, or in case you didn’t you just changed the subject for whatever reason: “so, if I used to be to select a favourite colour in a board game,…

I needed to thank you for this wonderful read!! I certainly enjoyed every little bit of it. I have got you book marked to look at new stuff you post…

When I initially commented I seem to have clicked on the -Notify me when new comments are added- checkbox and from now on every time a comment is added I receive four emails with the same comment. Is there a means you can remove me from that service? Cheers.

Great web site you’ve got here.. It’s hard to find high-quality writing like yours nowadays. I really appreciate people like you! Take care!!

Every service isn’t counted as an application.

Woods, Ben (April 16, 2013).

I love it when individuals come together and share views. Great site, stick with it!

Market Fluctuations: The value of the pledged securities can fluctuate, affecting the LTV ratio and potentially leading to margin calls.

Bell, his wife Ruth and their children, Don and Judy cared for the little bear with the help of local veterinarian Dr Edwin J. Smith.

I couldn’t refrain from commenting. Perfectly written!

Everyone loves it when folks come together and share thoughts. Great website, stick with it.

You have made some decent points there. I checked on the net for more information about the issue and found most people will go along with your views on this website.

I am often to blogging and i also genuinely appreciate your website content continuously. The content has really peaks my interest. My goal is to bookmark your web site and keep checking for brand new info.

Company occasions are available all sizes and shapes; so one can host a big-sized occasion at a convention or a small event as an intimate business affair.

The place is worldwide famend as the location the place Buddha acquired Bodhimandala, means Enlightenment.

Thanks for the post, was an interesting read. Curious as to how you came about that solution…

They dwell with their grownup daughter and so need to make a non-dependant deduction of £91.47.

What your stating is absolutely correct. I know that everyone have to say the identical matter, but I just believe that you place it in a way that everyone can understand. I also love the photographs you put in the following. They match so effectively with what youre attempting to say. Im confident youll get to so many individuals with what youve acquired to say.

Can I just say what a relief to get an individual who really knows what theyre talking about on the net. You unquestionably know how you can bring an problem to light and make it important. A lot more individuals need to read this and realize this side of the story. I cant believe youre not additional common simply because you definitely have the gift.

On July 3, Lebanon County grew to become the final county to enter the inexperienced phase.

Nice post. I understand some thing harder on diverse blogs everyday. It will always be stimulating to read content from other writers and rehearse something from their website. I’d opt to apply certain with the content in my small weblog whether you don’t mind. Natually I’ll offer you a link in your internet blog. Many thanks for sharing.

I really like reading a post that can make people think. Also, thank you for allowing me to comment.

I like it when individuals come together and share ideas. Great site, continue the good work.

You have made some really good points there. I looked on the net to find out more about the issue and found most people will go along with your views on this site.

healthier hair is of course mainly due to genetics but food supplementation can also help you get it`

Lack of motivation is one of the top train killers, however joining a sports membership may also help.

However Luckett chimed out, “Heads is the decision. He said ‘heads.'” The coin, after all, landed on tails, giving Detroit the primary crack at scoring.

Greetings! This is my first visit to your blog! We are a collection of volunteers and starting a new initiative in a community in the same niche. Your blog provided us useful information to work on. You have done a marvellous job!

Russia is the most important nation in Asia.

It is crucial to deal with mental well being issues as a part of an general method to healthcare.

Nice post. I learn something new and challenging on blogs I stumbleupon on a daily basis. It will always be interesting to read articles from other writers and use a little something from other sites.

What i don’t realize is in reality how you are not really much more well-preferred than you might be right now. You’re very intelligent. You realize thus considerably in relation to this subject, produced me individually imagine it from numerous numerous angles. Its like women and men are not interested unless it is one thing to accomplish with Lady gaga! Your own stuffs excellent. Always care for it up!

I am usually to blogging and i actually appreciate your content. The article has really peaks my interest. I’m going to bookmark your site and keep checking for brand new information.

After looking into a handful of the articles on your web page, I seriously appreciate your way of blogging. I bookmarked it to my bookmark webpage list and will be checking back soon. Take a look at my web site too and let me know what you think.

What occurs should you by accident crack a mirror?

Excellent read, I just passed this onto a friend who was doing some research on that. And he actually bought me lunch because I found it for him smile Thus let me rephrase that: Thank you for lunch!

Justin Bieber is quite talented at a very young age, he sings good too,.

Greetings! Very helpful advice in this particular article! It’s the little changes that produce the most important changes. Thanks a lot for sharing!

Good post. I learn something totally new and challenging on blogs I stumbleupon every day. It will always be interesting to read articles from other authors and use something from other web sites.

I’m impressed, I have to admit. Genuinely rarely will i encounter a blog that’s both educative and entertaining, and without a doubt, you could have hit the nail around the head. Your notion is outstanding; the issue is something which inadequate people are speaking intelligently about. I will be very happy we came across this around my look for some thing in regards to this.

i am looking for gadget reviews this december coz i wanna buy some of the latest gadgets for my girlfriend*

The entire constellations, whereas sectors of the ecliptic, are held throughout the Zodiac, hence their title.

I really like it when people come together and share ideas. Great blog, continue the good work!

Divide up a large bag of chips or box of cookies into particular person servings and store them in reclosable plastic luggage.

I would like to show my gratitude for your kindness for people that absolutely need help with this particular content. Your very own dedication to getting the message all-around became particularly good and have in most cases encouraged girls much like me to achieve their goals. This informative guideline implies so much to me and much more to my office colleagues. Thanks a lot; from each one of us.

I’ve been exploring for a bit for any high quality articles or blog posts on this sort of area . Exploring in Yahoo I at last stumbled upon this web site. Reading this information So i am glad to show that I have a very good uncanny feeling I found out exactly what I needed. I so much for sure will make certain to do not fail to remember this website and give it a glance on a constant.